Automotive Embedded Systems Market Report Scope & Overview:

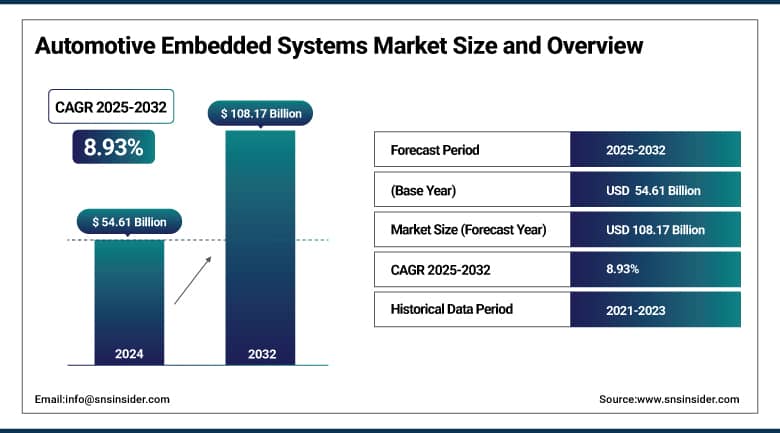

The Automotive Embedded Systems Market size was valued at USD 54.61 billion in 2024 and is expected to reach USD 108.17 billion by 2032, growing at a CAGR of 8.93% over 2025-2032.

The automotive embedded systems market is undergoing rapid transformation, driven by the evolution of software-defined vehicles (SDVs), electrification, and advancements in in-vehicle connectivity and automation. Major OEMs and Tier 1 suppliers, such as Mahindra, NXP, Infineon, STMicroelectronics, and Continental, are investing heavily in embedded software and hardware development to enable next-generation vehicle architectures. For instance, Mahindra’s partnership with Vector Informatik aims to develop SDV-ready platforms, while Infineon has launched the first automotive-grade RISC-V MCU family, signaling a shift toward open-source hardware architectures. Pioneer’s new R&D center in Bengaluru and Green Hills Software's collaboration with NXP reflect the global focus on building scalable and secure embedded ecosystems.

In June 2024, NXP's acquisition agreement with TTTech Auto supports the expansion of reliable middleware for zonal architectures in SDVs, aligning with industry shifts toward centralized vehicle software stacks.

Increasing demand for OTA updates, centralized computing, and AI-integrated safety features is propelling development. Moreover, Emerson’s launch of a HIL embedded test suite and Lauterbach-Corellium collaboration for enhanced debugging highlight the strengthening of the embedded validation infrastructure. R&D spending in automotive software and electronics continues to rise, exemplified by Renesas’s introduction of the first 3nm automotive SoC, a leap in processing capability. Regulatory mandates surrounding safety and cybersecurity are also pushing OEMs to adopt advanced embedded architectures that comply with standards like ISO 26262 and WP.29.

In May 2024, STMicroelectronics’ launch of extensible memory solutions for MCUs improves performance and flexibility, catering to the demand for more intelligent, real-time automotive applications, especially in EVs and ADAS domains.

To Get More Information On Automotive Embedded Systems Market - Request Free Sample Report

Market Dynamics:

Drivers:

-

Technological advancement and rising demand for connected, autonomous, and electric mobility are driving embedded system adoption in the automotive sector

The automotive embedded systems market is experiencing strong momentum driven by the increasing demand for smart, connected, and autonomous vehicles. A key growth driver is the surge in ADAS and EV integration, both of which require robust embedded software and hardware systems.

According to Capgemini, 72% of automakers have already shifted significant investment toward software development, and nearly USD 80 billion was spent on automotive R&D in 2023 globally, much of it focused on embedded systems.

The rise of domain and zonal architectures, as introduced by companies like Aptiv and Bosch, is accelerating the deployment of centralized embedded platforms. Moreover, regulatory mandates such as UN R155 and ISO 21434 are pushing OEMs to integrate secure and functional embedded solutions. The push for vehicle-to-everything (V2X) communication and OTA updates further fuels embedded software demand. Additionally, the growing use of AI-powered processors for real-time decision-making in autonomous navigation and predictive maintenance systems is creating new supply chain investments. Companies like Arm and Qualcomm have introduced automotive-grade chipsets with AI inference capabilities, tailored for edge applications. The increasing collaboration between OEMs and software specialists (e.g., Amazon-Aurora, Microsoft-ZF) is another testament to this software-first transformation.

Restraints:

-

System Complexity, Cybersecurity Risks, And the Lack of Standardized Software Architectures Are Key Restraints Impacting Embedded System Scalability in Automotive

One of the major restraints hindering the growth of the automotive embedded systems market is the rising complexity of system integration and the fragmented ecosystem of proprietary hardware-software stacks. The absence of universal standards makes interoperability between components challenging, leading to delays and increased costs. According to a 2024 report by McKinsey, over 35% of software recalls in the automotive industry were linked to integration failures or software malfunctions. The growing reliance on millions of lines of code in modern vehicles, often surpassing that of commercial aircraft, increases the scope for software bugs and failures. Additionally, the rise of cyber threats is a major concern.

The 2023 Auto-ISAC report revealed a 268% increase in automotive cyberattacks over the past two years, particularly targeting control systems and vehicle-to-cloud interfaces. Compliance with evolving cybersecurity standards (e.g., ISO/SAE 21434) adds to development overheads. Furthermore, the global shortage of semiconductor components continues to affect embedded system supply chains. Although companies like TSMC and GlobalFoundries are expanding automotive chip fabrication, lead times for MCUs and SoCs still exceed 30–40 weeks on average, creating supply bottlenecks. The shortage of skilled embedded software engineers further constrains innovation cycles and delays product launches.

Segmentation Analysis:

By Type

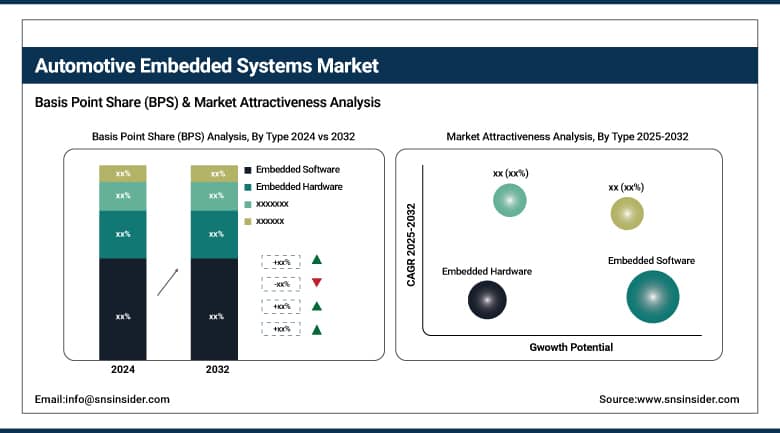

In 2024, Embedded Software dominated the automotive embedded systems market by type, accounting for 59.2% of the total share. This dominance is attributed to the rapid adoption of software-defined vehicle (SDV) architectures and the increasing demand for advanced driver assistance systems (ADAS), connectivity, and over-the-air (OTA) update functionalities. The fastest-growing segment is Embedded Hardware, driven by continuous advancements in high-performance computing units and the integration of complex sensors and control modules in EVs and autonomous platforms.

By Component

By component, Microcontrollers (MCUs) held the largest share in 2024, commanding around 38.7% of the market, owing to their critical role in managing real-time control operations across safety, infotainment, and powertrain systems. The fastest-growing component segment is Memory Devices, driven by the growing demand for high-capacity storage to support large-scale data processing and software-intensive applications like navigation, AI, and telematics.

By Vehicle Type

Among vehicle types, Passenger Cars dominated with 72.5% of the market share in 2024 due to higher production volumes, increased infotainment demand, and rapid electrification. Meanwhile, Commercial Vehicles emerged as the fastest-growing segment as fleet management, safety regulations, and logistics optimization accelerated embedded system integration.

By Electric Vehicle

Within electric vehicles, Battery Electric Vehicles (BEVs) led the market, capturing 64.1% share in 2024, supported by government incentives, expanding charging infrastructure, and zero-emission targets. However, Plug-In Hybrid Electric Vehicles (PHEVs) are the fastest-growing segment due to their dual advantage of electric range and fuel flexibility, appealing in regions with limited charging networks.

By Application

In terms of application, Safety & Security dominated the market with a 33.8% share in 2024, driven by stringent safety norms and increased installation of electronic stability control, airbags, and ADAS. The fastest-growing application is Infotainment & Telematics, fueled by consumer demand for connectivity, real-time diagnostics, smart dashboards, and integrated entertainment systems.

Regional Analysis:

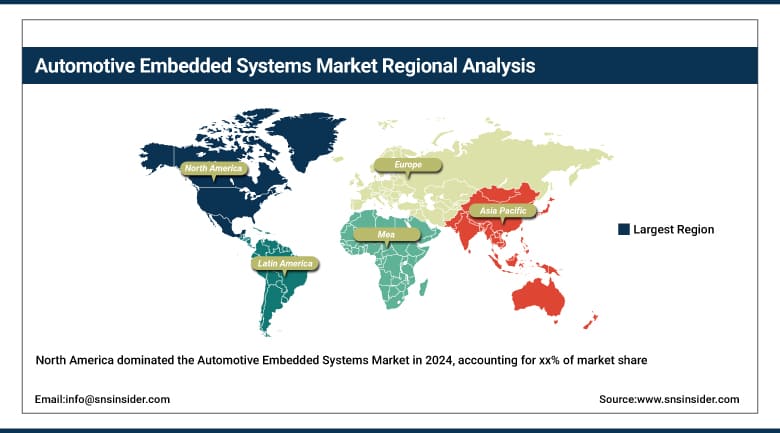

North America remains a dominant region in the automotive embedded systems market, primarily due to the United States' robust automotive innovation ecosystem and the high adoption rate of electric and autonomous vehicles. The U.S. leads the region, accounting for a majority share, driven by significant R&D investments from tech-automotive partnerships such as GM-Cruise and Ford-Google. In 2024, the U.S. Department of Transportation expanded its support for autonomous vehicle testing, further accelerating embedded system integration. Canada is focusing on EV technology and connectivity solutions, while Mexico's expanding automotive manufacturing base is attracting investments in embedded hardware production. The U.S. alone accounts for over 60% of the North American embedded systems market due to its strong EV and software-defined vehicle (SDV) transition pace.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe holds a significant position in the market, with Germany dominating due to its leadership in automotive engineering and high concentration of premium OEMs like BMW, Daimler, and Volkswagen. These companies are rapidly integrating zonal architectures and advanced embedded solutions to support electric and semi-autonomous vehicles. Germany's push for software-oriented platforms and compliance with EU cybersecurity and emissions regulations makes it a central hub. The UK and France are also advancing through heavy investments in connected vehicle tech and pilot deployments of intelligent transport systems. Eastern European nations, like Poland, are emerging as cost-efficient manufacturing centers for embedded components. Europe is the second fastest-growing region, driven by rising electrification, EU-backed green mobility initiatives, and mandatory adoption of ADAS under General Safety Regulation (GSR) mandates from 2024 onward.

Asia Pacific is the fastest-growing region, fueled by high vehicle production, increasing EV adoption, and a rapidly expanding middle-class population demanding advanced features. China dominates the region, supported by its position as the world’s largest auto market and government-led policies promoting smart electric mobility. In 2024, China accounted for over 35% of global EV sales, creating enormous demand for embedded systems in EV platforms. Japan continues to lead in embedded hardware innovations, particularly in sensor technologies, with companies like DENSO and Renesas driving R&D. India is also witnessing strong growth due to expanding EV startups, FAME II incentives, and the "Make in India" push that has attracted embedded hardware manufacturing. South Korea's focus on autonomous technologies and local giants like Hyundai and LG Electronics advancing in connected mobility further boost the regional landscape.

Key Players:

Leading automotive embedded systems companies in the comprise Infineon Technologies, Texas Instruments, Panasonic, Renesas, Analog Devices, Qualcomm, Hyundai Mobis, NXP Semiconductors, STMicroelectronics, Continental AG, Aptiv, Robert Bosch, NVIDIA, and DENSO.

Recent Developments:

In January 2025, NXP announced a USD 625 million acquisition of Austria-based TTTech Auto to integrate its safety-focused middleware, critical for ensuring OTA updates don’t disrupt safety systems, directly into NXP’s automotive chip portfolio.

In January 2025, BlackBerry’s QNX introduced its “industry-first” cockpit hypervisor at CES, enabling high-performance, OS‑agnostic digital cockpit architectures that support Android Automotive and Linux guest OSes, all with automotive safety certification.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 54.61 billion |

| Market Size by 2032 | USD 108.17 billion |

| CAGR | CAGR of 8.93% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Embedded Hardware, Embedded Software) • By Component (Sensors, (Temperature Sensors, Pressure Sensors, Image Sensors, Radar Sensors, Lidar Sensors), Microcontrollers (MCU), Transceivers, Memory Devices) • By Vehicle Type (Passenger Cars, Commercial Vehicles) • By Electric Vehicle (Battery Electric Vehicle (BEV), Hybrid Electric Vehicle (HEV), and Plug-In Hybrid Electric Vehicle (PHEV)) • By Application (Infotainment & Telematics, Body Electronics, Powertrain & Chassis Control (Automatic Transmission, Electric Power Steering, Active Suspension), Safety & Security (ADAS, Electronic Brake System (Antilock Brake System (ABS), Electronic Stability Control (ESC), Traction Control System (TCS)), Airbags) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Infineon Technologies, Texas Instruments, Panasonic, Renesas, Analog Devices, Qualcomm, Hyundai Mobis, NXP Semiconductors, STMicroelectronics, Continental AG, Aptiv, Robert Bosch, NVIDIA, and DENSO. |

Frequently Asked Questions

Ans: North America is the dominant region in the Automotive Embedded Systems market.

Ans: System complexity, cybersecurity risks, and the lack of standardized software architectures are key restraints impacting embedded system scalability in automotive.

Ans: Technological advancement and rising demand for connected, autonomous, and electric mobility are driving embedded system adoption in the automotive sector.

Ans: By 2032, the Automotive Embedded Systems Market is expected to reach USD 108.17 billion, up from USD 54.61 billion in 2024.

Ans: The Automotive Embedded Systems Market is projected to grow at a CAGR of 8.93% during the forecast period.

Get in Touch