Battery Swapping Market Report Scope & Overview:

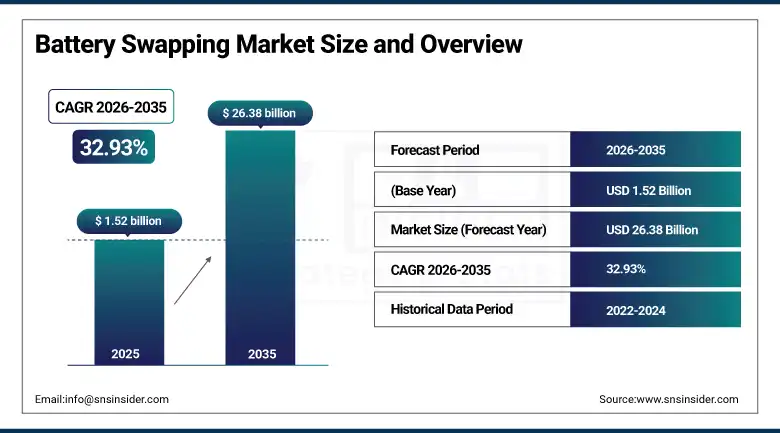

The battery swapping market was valued at USD 1.52 billion in 2025 and is expected to reach USD 26.38 billion by 2035, growing at a CAGR of 32.93% from 2026–2035.

The market for battery swapping services is witnessing unparalleled levels of growth owing to the rapidly shifting paradigm towards electric vehicles around the world along with the rising issues related to EV charging infrastructure. By providing instantaneous replenishment of energy, battery swapping technology presents an attractive solution to the problems associated with plug-in charging, thereby addressing the issue of range anxiety along with minimization of downtime. With an increasing uptake of electric two-wheelers and three-wheelers in highly populated regions like China, India, and Southeast Asia, there is considerable scope for development of a strong and scalable ecosystem for battery swapping. The implementation of the BaaS model helps reduce the overall cost of owning EVs.

Public policies like China’s National EV Promotion Subsidies, India’s Battery Swapping Policy through the FAME II program, the European Green Deal, and the U.S. Bipartisan Infrastructure Law have been responsible for directing a considerable amount of government funds towards renewable energy transport infrastructure development, including battery swapping facilities. Government-enforced targets for the deployment of electric vehicles (EVs) and carbon emission reductions pledged by leading economies have stimulated the collaboration between EV manufacturers to develop infrastructure networks. In conjunction with these favorable developments, recent breakthroughs in BMS and other station technologies, along with modular battery designs, are driving commercial adoption of battery swapping solutions.

Market Size and Forecast

-

Market Size in 2026E: USD 2.04 Billion

-

Market Size by 2035: USD 26.38 Billion

-

CAGR (2026–2035): 32.93%

-

Fastest Growing Region: Europe

-

Largest Region: Asia Pacific

To Get more information On Battery Swapping Market - Request Free Sample Report

Battery Swapping Market Trends

-

Rapid proliferation of BaaS and subscription-based models is decoupling battery ownership from vehicle ownership, significantly lowering EV adoption barriers across two-wheeler and commercial fleet segments.

-

Standards for module-based batteries and interoperable open systems have been created by OEMs, facilitating multiple brand battery swapping, and increasing efficiency at charging stations.

-

AI-driven robots and cloud-based battery management systems have decreased swap times to less than 3 minutes, greatly increasing efficiency at battery charging stations.

-

Technology for solid-state batteries is seen as a cutting-edge field for next-generation swapping systems that offer better energy density, fast charge storage, and better thermal stability than the currently existing lithium-ion batteries.

-

Commercial operators such as urban logistics companies, ride-sharing businesses, and last mile delivery services are turning to battery swapping systems to increase their operating time.

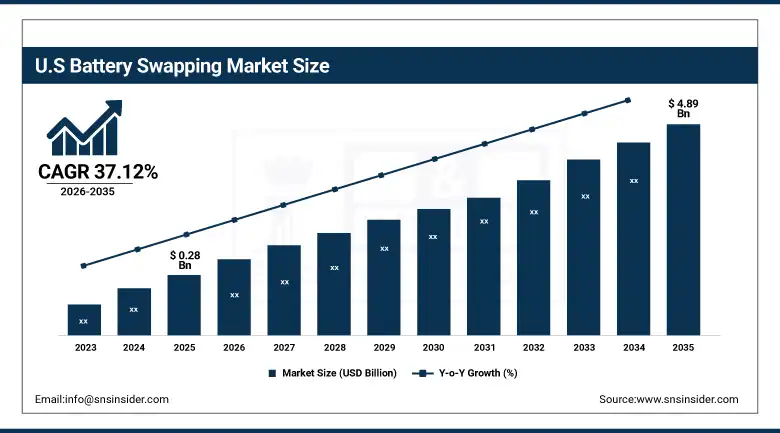

The U.S. Battery Swapping Market Size Outlook

The U.S. battery swapping market was valued at USD 0.28 billion in 2025 and is expected to reach around USD 4.89 billion by 2035, growing at a CAGR of 37.12% from 2026–2035.

While still considered to be in its early stages of development when compared to the Asia Pacific battery swapping market, the market in the United States looks set for strong growth due to increasing EV adoption, federal and state mandates for cleaner energy production, and the trend towards commercial fleets becoming fully electric vehicles. Companies like Ample Inc. are implementing modular, vehicle-agnostic battery swapping systems working with prominent automakers and fleet owners. Further contributing to the expected growth in the market in the United States will be the efforts by ride-sharing apps, logistics firms, and utility companies who are exploring opportunities to utilize EVs and battery swapping.

Aptly named Ample Inc., an energy technology company that specializes in the innovation of battery switching, made some notable progress in terms of its battery platform partnerships during 2025. In particular, this company reached partnership agreements with various international automotive OEMs and logistics companies, whereby they agreed to install Ample's automated battery switch stations on the commercial vehicle routes of North America.

Battery Swapping Market Segment Analysis

-

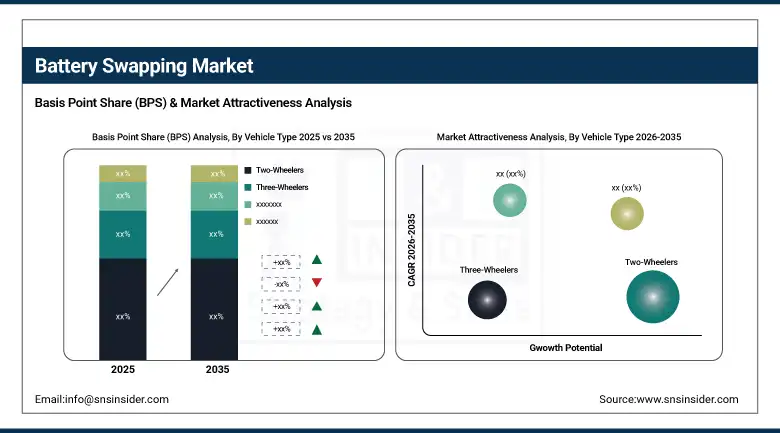

By Vehicle Type, the two-wheelers segment dominated the battery swapping market with a 41.25% share in 2025, while the three-wheelers segment is the fastest growing segment.

-

By Battery Technology, the lithium-ion segment dominated the battery swapping market with a 68.74% share in 2025, while solid-state batteries are the fastest growing segment.

-

By Swapping Technology, the automated/robotic segment dominated the battery swapping market with a 52.38% share in 2025, while the semi-automated segment is the fastest growing.

-

By Business Model, the Battery-as-a-Service (BaaS) segment dominated the battery swapping market with a 44.62% share in 2025, while the subscription-based segment is the fastest growing.

-

By End User, the fleet operators segment dominated the battery swapping market with a 58.47% share in 2025, while individual users are the fastest growing segment.

By Vehicle Type, the two-wheelers segment dominates, three-wheelers are the fastest-growing segment.

The two-wheelers segment was the dominant revenue contributor in the battery swapping market in 2025, accounting for 41.25% of total global market share. This supremacy comes from the huge penetration of two-wheeled electric vehicles in the Asia Pacific region, especially in China, India, Taiwan, and Vietnam, wherein commuter riding of motorcycles and scooters is an essential component of everyday transportation. The large number of vehicles combined with short inter-swap time and the efficiency offered by battery swap networks makes two-wheelers the most economically viable category of vehicles for swapping systems. Prominent companies like Gogoro in Taiwan and Battery Smart in India have created their own customized ecosystem for two-wheelers through swap stations located in urban routes to increase the number of swaps per station.

Three Wheelers is expected to hold the leading position in terms of CAGR during the forecast period of 2026 to 2035 owing to the fast pace at which auto-rickshaws, cargo trikes, and shared mobility three-wheelers are becoming electrified in the South and Southeast Asian region. The ambitious plan adopted by India to electrify their extensive commercial three-wheeler vehicle fleet through the FAME II and subsequent clean mobility initiatives is one of the major factors contributing towards this trend. In addition, battery swapping presents a more efficient method for three-wheelers due to the inability of operators to take time out for charging batteries, since battery swapping leads to increased earnings.

By Battery Technology, the lithium-ion segment dominates, solid-state batteries are the fastest-growing segment.

The most dominant type was the lithium-ion battery category that accounted for the largest revenue share of 68.74% in the year 2025, due to the high rate of commercialization, competitive pricing, and reliable performance associated with the technology. Lithium-ion batteries have established supply chains, excellent energy density features, and compatibility with current charging stations. The maturation of the technology is responsible for the quick development of standards for swappable lithium-ion batteries, which explains why the technology is the preferred one for most battery swapping projects around the globe. The declining costs in the production of lithium-ion cells and electronics for battery management are expected to continue fueling the growth of the segment over the early forecast period.

The solid-state battery segment is anticipated to achieve the highest CAGR between 2026 and 2035, propelled by significant R&D investments from global battery manufacturers and automotive OEMs targeting next-generation EV platforms. SSB technology allows for significantly higher energy density, greater stability in high temperatures, and a greatly lowered probability of thermal runaway issues when compared to existing lithium-ion batteries, which makes them a promising candidate for use in battery swapping technology solutions. Increasing commercialization timelines from players such as Toyota, QuantumScape, and CATL are expected to drive integration of solid-state packs into advanced swapping ecosystems toward the latter half of the forecast period.

By Swapping Technology, the automated/robotic segment dominates, semi-automated technology is the fastest-growing segment.

The automated and robotics swap technology category dominated the battery swapping industry in 2025 with a revenue market share of 52.38% since there was a marked inclination towards the use of swap technologies that offered consistent and reliable performance irrespective of manual intervention. The fully automated systems leverage robotic arm technology, smart vehicle positioning using artificial intelligence, and conveyor belt-based battery logistics management systems in order to deliver battery swap services within a range of 3–5 minutes, entirely free from any human assistance. An example of fully automated battery swapping stations can be seen in the Power Swap Station of NIO in China and the automated battery swap station of Aulton in China, capable of conducting over 300 swaps per station per day.

The semi-automated swapping technology segment will register the highest growth rate in the period 2026–2035, owing to the cost effectiveness of this technology compared to that of fully automated stations, as well as its applicability in a wider variety of installation locations, such as rural regions and emerging countries where cost constraints are more significant. The use of semi-automated technology involves minimum human intervention in terms of aligning vehicles and locking batteries; thus, it is not costly to install while ensuring fast swapping times. An increase in the use of this technology in small fleets and semi-automated network operators in Tier 2 and Tier 3 cities, as well as in emerging countries in Africa and Latin America, will fuel its growth through 2035.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.23% |

|

Europe |

Germany |

29.74% |

|

Asia Pacific |

China |

54.83% |

|

Middle East & Africa |

UAE |

18.34% |

|

Latin America |

Brazil |

42.15% |

North America Battery Swapping Market Insights

North America accounted for approximately 22.18% of the global battery swapping market revenue in 2025, establishing itself as the second-largest regional contributor globally. The United States leads regional momentum, driven by federal infrastructure investments, state-level zero-emission vehicle mandates, and the aggressive electrification strategies of commercial fleet operators. Increasing adoption of electric two-wheelers and cargo e-bikes for urban last-mile delivery, combined with growing investments from venture-backed swapping technology startups, is progressively building the commercial foundation for a mature North American battery swapping ecosystem. Canada's clean transportation incentives and growing urban EV adoption are contributing supplementary regional demand.

The Bipartisan Infrastructure Law and the Inflation Reduction Act passed by the United States have cumulatively committed billions of dollars towards the deployment of EV charging and energy infrastructure, while battery swap stations have emerged as additional infrastructural options that can be considered in tandem with vehicle electrification and urban mobility solutions. The growing cooperation between the Original Equipment Manufacturers (OEMs) and swap station providers like Ample is rapidly increasing the scale and scope of such deployments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Battery Swapping Market Insights

It is expected that Europe will become the leading region for battery swap adoption between 2026 and 2035 owing to the ambitious European Union policy called "Fit for 55" package, together with other initiatives, such as the European Green Deal, and national targets for EVs in some major countries like Germany, France, the Netherlands, Norway, and the UK. Regulations adopted by EU member states requiring zero emissions zones in city centers and fleet emission targets are making it mandatory for companies to speed up their transition to electric-powered vehicles through battery swap stations.

The European Commission’s Alternative Fuels Infrastructure Regulation (AFIR), along with the development of government-funded clean mobility infrastructure initiatives in Germany and France, is providing positive regulatory tailwinds for the development of battery swap station infrastructure. The efforts of European automotive and energy organizations to conduct strategic pilot projects, alongside the increasing focus of urban mobility platform providers, will lay the foundation for the deployment of battery swapping networks in important European metropolises over the forecast period.

Asia Pacific Battery Swapping Market Insights

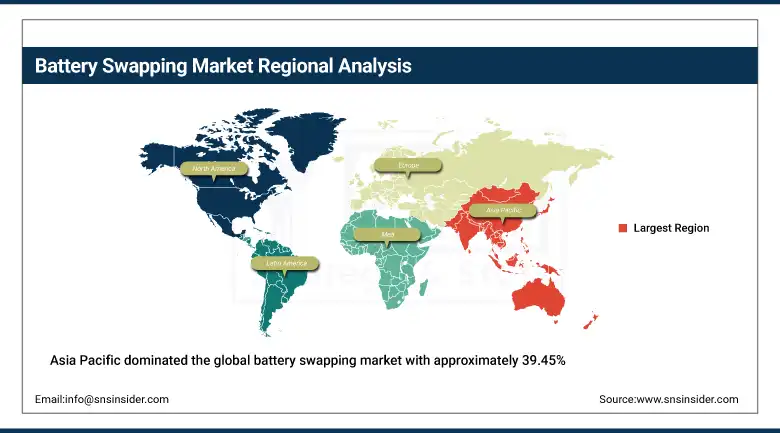

Asia Pacific dominated the global battery swapping market with approximately 39.45% of total revenue in 2025 and is expected to maintain its leading regional position throughout the 2026–2035 forecast period, growing at a CAGR of 34.72%. Being the largest market in the region, China possesses the best-developed battery swapping infrastructure that includes thousands of battery swap stations managed by such companies as NIO, Aulton, and public energy corporations. India is the fastest-growing market in the region due to FAME II policy, Battery Swapping Policy draft, and the need to make electric the large fleet of vehicles used in the country including two-wheelers and three-wheelers. Countries such as Japan, South Korea, Taiwan, and ASEAN nations provide growing demand for battery swapping thanks to government policies aimed at promoting the use of electric vehicles.

The Ministry of Industry and Information Technology (MIIT) in China has also sped up its efforts to standardize the process of battery swapping, developing interoperable standards for battery swap specification requirements and station communications protocols. This includes state-owned energy companies such as CNPC and Sinopec providing battery-swapping facilities within their vast fuel station networks, thus significantly broadening the geographical scope of battery swapping stations and integrating the practice into the mainstream of EV charging.

Middle East & Africa and Latin America Battery Swapping Market Insights

In relation to market opportunities, the Middle East & Africa and Latin American regions are identified as emerging frontiers of battery swapping, driven by the trend toward urbanization, rising awareness on EVs, and strategic investments by governments in the development of green transport infrastructure. In the case of the MEA region, battery swapping is being led by the UAE and Saudi Arabia due to their strategic focus on developing smart cities and modernizing transportation infrastructure in alignment with Vision 2030. Electric two-wheeler adoption for commuter and last-mile delivery use is driving early-stage battery swapping adoption in countries such as South Africa and Egypt. Within Latin America, the main contributing markets include Brazil and Mexico, which have favorable green transportation policies as well as rising production of electric two-wheelers.

The transportation modernization efforts being undertaken by Saudi Arabia under its Vision 2030 plan and the UAE clean energy diversification drive are allocating resources towards development of EV charging networks, which also includes trials of battery swapping stations for use in municipal fleets and city mobility applications. The Brazilian ROTA 2030 initiative and Mexico's EV push programs are similarly driving the uptake of electric two-wheelers and commercial vehicles, paving the way for establishment of battery swapping networks in Latin America.

Market Dynamics

Growth Drivers: Surging global EV adoption and the need for rapid energy replenishment solutions are accelerating battery swapping infrastructure deployment worldwide.

The widespread uptake of electric vehicles in two-wheelers, three-wheelers, and commercial vehicles segments around the world is the key underlying driver of demand in battery swapping markets. As electric vehicles gain greater traction in densely populated urban centers, the weaknesses in the existing traditional charging methods due to their expensive initial installations, lengthy charging periods, and physical space requirements are becoming more apparent, thereby favoring battery swapping systems. Increasing pressure on commercial businesses to optimize vehicle uptime within logistics, ride-hailing, and mobility sharing sectors is adding more value to battery swapping services where fast energy replenishment within less than 5 minutes leads to increased daily revenues from each vehicle. Electric vehicle mandates by governments, carbon emissions reductions pledges, and transport subsidies are among the factors contributing to the development of battery swapping infrastructure.

Restraints: Lack of universal battery standardization and high station capital expenditure are constraining large-scale battery swapping network expansion globally.

The lack of globally agreed technical standards for the form factor of batteries that can be swapped out, connector systems, and communication protocols is the key structure that restricts the development of the battery-swap market on a global level. Absent standardized solutions, network operators and OEMs are forced to create their own proprietary systems of battery swap infrastructure that result in low utilization of swapping stations and the development of fragmented, non-compatible networks, which are costly to implement on a large scale. A high investment in setting up a fully automated swapping station, which varies from US$150,000 to more than US$500,000 depending on the degree of automation and station capacity, is a significant entry barrier that requires a long time to recover costs. High utilization rates, which prove difficult to achieve in less saturated markets, are crucial for station viability.

Opportunities: Growing integration of smart energy management and grid services into battery swapping ecosystems is opening significant new revenue streams and investment opportunities.

The combination of battery swapping infrastructure along with smart grid technology is a revolutionary business opportunity for network operators, electricity providers, and technology companies. Battery swapping stations that aggregate a large number of batteries at various charge capacities can serve as a source of energy storage that will help balance the load, respond to the grid, and shift energy through V2G and B2G technologies. The application of artificial intelligence and big data in analyzing the health state of batteries and providing predictive maintenance along with cloud computing to manage the fleet of batteries and cars have resulted in lucrative IT services revenues on top of the transactional revenues earned from battery swapping activities. Increasing collaboration between battery swapping businesses and renewable energy companies along with active recycling of batteries have raised the economic attractiveness of battery swapping networks.

Recent Developments

-

2025: NIO expanded its Power Swap Station network to over 3,000 locations globally, including its first European stations in Norway, Denmark, and Germany, marking a significant milestone in the international commercialization of passenger car battery swapping and demonstrating the operational scalability of fully automated swapping infrastructure beyond its core Chinese market.

-

2025: Gogoro and Hero MotoCorp deepened their India market partnership, accelerating the rollout of Gogoro's modular battery swapping network infrastructure across Indian cities to support Hero's growing electric two-wheeler product lineup, targeting rapid expansion of swap station density in Tier-1 and Tier-2 urban markets across the country.

-

2024: CATL launched its EVOGO battery swapping platform commercial expansion, extending its block-shaped modular swappable battery architecture to additional vehicle OEM partners and initiating multi-city swapping station deployments in China, positioning CATL as a major ecosystem player spanning both battery manufacturing and swapping network operations.

Battery Swapping Market Key Players are:

-

NIO Inc.

-

Gogoro Inc.

-

Ample Inc.

-

Sun Mobility

-

Contemporary Amperex Technology Co., Limited (CATL)

-

Aulton New Energy Automotive Technology

-

BAIC Group

-

Battery Smart

-

Geely Technology Group

-

KYMCO (Kwang Yang Motor Co., Ltd.)

-

BYD Co. Ltd.

-

Gachaco Inc.

-

Honda Motor Co., Ltd.

-

TGOOD Electric Co., Ltd.

-

Leo Motors Inc.

-

Panasonic Corporation

-

Lithion Power Pvt. Ltd.

-

BattSwap Inc.

-

Swiftmile

-

Selex Motors

Battery Swapping Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.52 Billion |

| Market Size by 2035 | USD 26.38 Billion |

| CAGR | CAGR of 32.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Vehicle Type (Two-Wheelers, Three-Wheelers, Commercial Vehicles, Passenger Cars) • By Battery Technology (Lithium-Ion, Solid-State, Nickel-Metal Hydride, Others) • By Swapping Technology (Automated/Robotic, Semi-Automated, Manual) • By Business Model (Battery-as-a-Service (BaaS), Subscription-Based, Pay-Per-Use, Others) • By End User (Fleet Operators, Individual Users) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NIO Inc., Gogoro Inc., Ample Inc., Sun Mobility, Contemporary Amperex Technology Co., Limited (CATL), Aulton New Energy Automotive Technology, BAIC Group, Battery Smart, Geely Technology Group, KYMCO (Kwang Yang Motor Co., Ltd.), BYD Co. Ltd., Gachaco Inc., Honda Motor Co., Ltd., TGOOD Electric Co., Ltd., Leo Motors Inc., Panasonic Corporation, Lithion Power Pvt. Ltd., BattSwap Inc., Swiftmile, Selex Motors |

Frequently Asked Questions

The major growth factor is the surging global adoption of electric vehicles, particularly two-wheelers and three-wheelers.

The battery swapping market was valued at USD 1.52 billion in 2025.

The battery swapping market is expected to grow at a CAGR of 32.93% from 2026 to 2035.

Get in Touch