Automotive Seat Belts Market Report Scope & Overview:

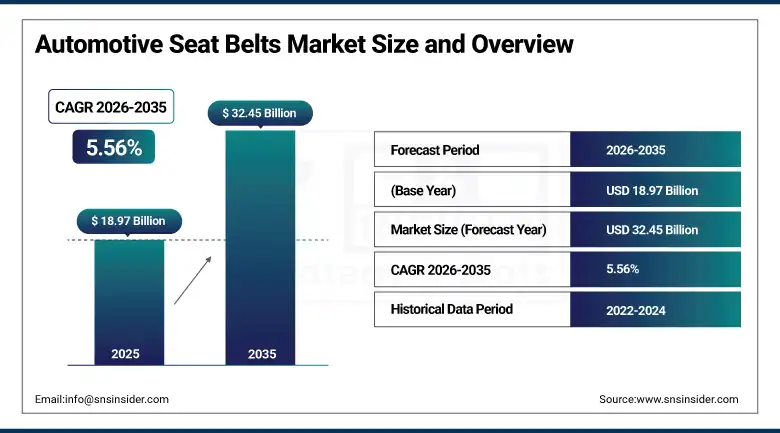

The Automotive Seat Belts Market was valued at USD 18.97 Billion in 2025 and is expected to reach USD 32.45 Billion by 2035, growing at a CAGR of 5.56% from 2026–2035.

The global automotive seat belts market is advancing on the back of tightening vehicle safety regulations, rising global vehicle production, and the progressive integration of intelligent restraint technologies that transform the seat belt from a passive safety component into an active occupant protection system. Governments across North America, Europe, and Asia Pacific are strengthening seat belt mandate enforcement and raising minimum performance standards. These regulatory obligations create non-discretionary demand that sustains the market through automotive production cycle variations.

Joyson Safety Systems launched its Smart-Tension active seat belt technology in March 2025, featuring sensor integration for adaptive force limiting based on occupant size and position. This launch reflects the broader commercial transition occurring across the restraint systems industry, where OEMs are specifying adaptive occupancy-aware seat belt performance as a standard requirement in new vehicle safety packages rather than as a premium optional feature confined to luxury vehicle programmes.

Market Size and Forecast

-

Market Size in 2026E: USD 20.02 Billion

-

Market Size by 2035: USD 32.45 Billion

-

CAGR: 5.56% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Automotive Seat Belts Market - Request Free Sample Report

Automotive Seat Belts Market Trends

-

Rising integration of pretensioner and load limiter technology across mainstream vehicle segments is elevating seat belt system complexity and per-unit value, shifting the market from commodity component supply toward engineered safety system procurement.

-

Growing development of smart and active seat belt systems that adapt restraint force based on occupant size, position, and crash severity is creating premium market segments with above-average margin contribution for tier-1 safety system suppliers.

-

Increasing EV production is creating new seat belt design requirements, as the absence of engine noise makes cabin comfort and belt mechanism sound suppression a measurable quality attribute that OEM procurement teams now specify alongside structural safety performance.

-

Expanding enforcement of seat belt legislation in developing markets across South and Southeast Asia is creating first-time adoption demand among vehicle segments that previously carried minimal restraint system specifications as standard equipment.

-

Rising consumer awareness of occupant safety ratings published by NCAP programmes in multiple regions is compelling automakers to invest in seat belt systems that deliver measurably improved crash test outcomes rather than meeting minimum statutory compliance thresholds only.

U.S. Automotive Seat Belts Market Outlook

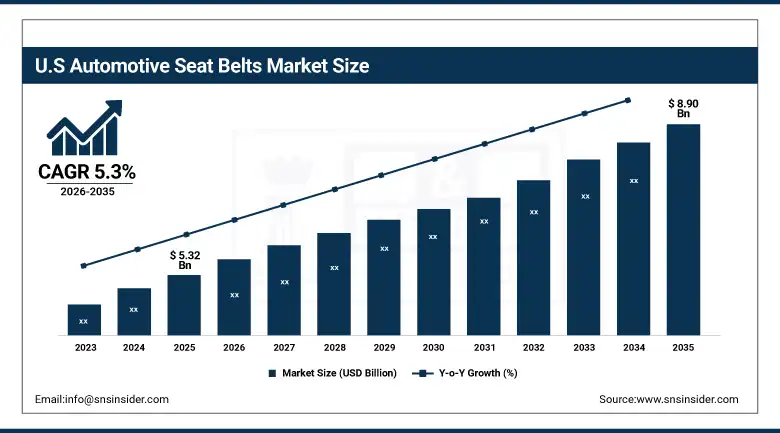

The U.S. Automotive Seat Belts Market was valued at approximately USD 5.32 Billion in 2025 and is expected to reach approximately USD 8.90 Billion by 2035, growing at a CAGR of approximately 5.3%.

Demand in the U.S. market is driven by NHTSA Federal Motor Vehicle Safety Standard 208, which mandates seat belt performance across all passenger vehicle categories and creates a compliance-driven procurement floor that sustains market volume independent of consumer preference dynamics. American vehicle production involves some of the most technically demanding seat belt specifications globally. OEMs require pretensioner and load limiter integration as standard across virtually all new vehicle platforms. Seat belt usage rates exceed 90% among U.S. front-seat occupants, creating strong actuarial justification for continued regulatory investment in restraint system performance improvement.

In May 2025, Robert Bosch GmbH obtained ECE R16 certification for its new modular buckle pretensioner that has been designed for ease of implementation within electric vehicle platforms in Europe. This certification endorses the design concept of leveraging existing pyrotechnic restraint technology within a framework that is constrained by the design parameters of EV battery platforms.

Automotive Seat Belts Market Segment Analysis

-

By Belt Type, three-point seat belts dominated with approximately 65% market share in 2025, providing the most effective occupant restraint across chest and lap zones during frontal and side impact events. Two-point and other configurations retain aftermarket relevance for specific seating positions, but three-point specification is expanding across all seating positions in new vehicle platforms globally.

-

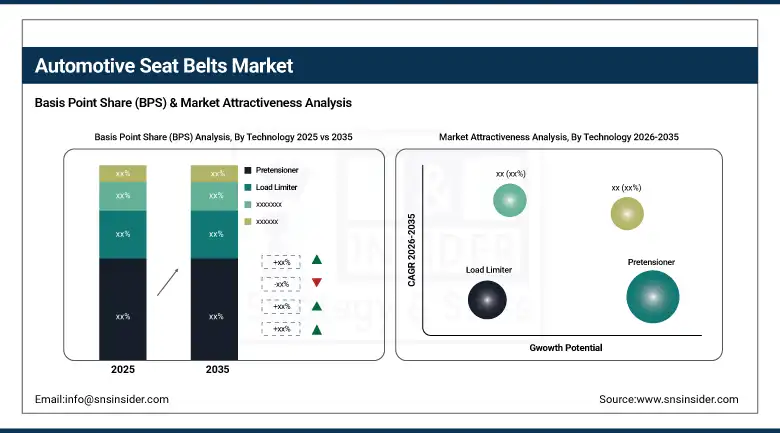

By Technology, pretensioner seat belts dominated with approximately 64% market share in 2025 through their role in eliminating belt slack at crash onset and substantially reducing occupant forward displacement during frontal impact events. Active and smart seat belt systems are the fastest-growing technology segment.

-

By Vehicle Type, passenger cars dominated with approximately 64% market share in 2025 as the highest-production vehicle segment generating the greatest aggregate seat belt procurement volume across OEM and aftermarket channels globally. Commercial vehicles are the fastest-growing vehicle type segment.

-

By Sales Channel, OEM dominated the automotive seat belts market in 2025, reflecting the seat belt's integration into vehicle safety system architecture from the earliest engineering stages of each new vehicle programme. The aftermarket is the fastest-growing sales channel.

By Technology, pretensioners dominate, active seat belts grow fastest

Pretensioner seat belts retained the dominant technology position with approximately 64% of the automotive seat belts market in 2025. Their commercial dominance reflects the established engineering consensus around pretensioner effectiveness in reducing occupant injury severity during frontal impact events. Pretensioners eliminate belt slack by rapidly retracting the webbing at crash onset, ensuring that the occupant is positioned correctly against the belt before their body begins to move forward. This action reduces the forward displacement distance that determines chest and head injury severity. Regulatory crash test protocols across NCAP programmes and statutory standards globally reward pretensioner-equipped restraint systems with improved ratings that directly influence OEM procurement specifications and consumer vehicle purchase decisions.

Active and smart seat belt systems are the fastest-growing technology segment because they address performance limitations that conventional pretensioner systems cannot resolve. Conventional pretensioners are reactive; they respond to a crash event after its onset. Active systems are proactive. They monitor occupant position, body weight estimates, and pre-crash threat signals from ADAS sensors to adjust belt tension before impact is confirmed. Joyson Safety Systems’ Smart-Tension system and Nissan’s Intelligent Seatbelt reflect the commercial realisation of this concept. Connected seat belt systems using 5G-enabled interlocking that verifies belt engagement before vehicle ignition represent a further commercial evolution whose road safety benefit is compelling sufficient to attract regulatory interest as a potential future mandatory safety feature.

By Vehicle Type, passenger cars dominate, commercial vehicles grow fastest

Passenger cars retained the dominant vehicle type position with approximately 64% of the automotive seat belts market in 2025. Global passenger car production volumes are the primary driver. Each vehicle produced requires a complete complement of seat belt assemblies for every seating position. The technical sophistication of passenger car seat belt specifications has risen consistently across each vehicle generation cycle. Entry-level passenger cars now carry pretensioner and load limiter equipment as standard that was previously confined to premium vehicle segments. This specification elevation has simultaneously expanded the total seat belt content per vehicle and increased the average revenue per OEM belt assembly, sustaining market value growth above the rate of vehicle production volume growth alone.

Commercial vehicles are the fastest-growing vehicle type segment in the automotive seat belts market. The commercial driver is legislative reform. Bus and truck cab occupant safety has historically received less regulatory attention than passenger car occupant protection in many developing markets. This is changing. India’s progressive strengthening of CMVR commercial vehicle safety standards, China’s GB safety regulations for commercial vehicle cab occupants, and Brazil’s expanding seat belt enforcement for public transport vehicles are each independently creating new first-time statutory demand for compliant seat belt systems across commercial vehicle categories that previously operated with minimal restraint equipment. Each regulatory upgrade event creates a fleet-wide procurement requirement whose volume impact exceeds individual consumer purchase decisions.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.4% |

|

Asia Pacific |

China |

54.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Automotive Seat Belts Market Insights

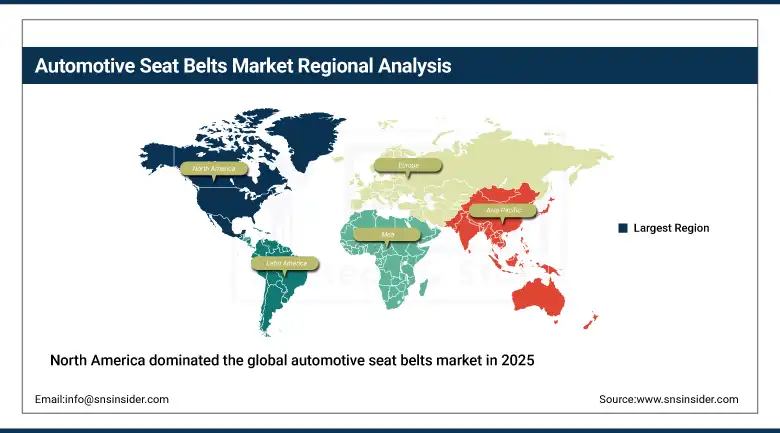

North America dominated the global automotive seat belts market in 2025, with the United States accounting for approximately 82.5% of North American revenues. The market is structurally supported by NHTSA’s comprehensive FMVSS 208 regulatory framework, above-average seat belt usage enforcement, and the premium vehicle segment’s demand for advanced restraint technology that sustains above-average per-unit revenue across the North American OEM supply base. Autoliv, ZF LIFETEC, Joyson Safety Systems, and Tokai Rika collectively serve the majority of North American OEM seat belt procurement through established Tier-1 supply relationships whose long qualification timelines create meaningful competitive barriers for new market entrants.

Canada contributes approximately 17.5% of North American revenues through its significant vehicle assembly operations producing both domestic market and export-oriented vehicles. Canadian assembly plants mirror the seat belt technology specifications of their U.S. counterpart programmes, creating consistent procurement alignment across the North American OEM production system that allows seat belt suppliers to serve the North American market as a unified procurement geography rather than requiring distinct product development for each national market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Automotive Seat Belts Market Insights

Europe is a technically sophisticated automotive seat belts market where EU occupant protection regulations under UN ECE R16 and the Euro NCAP assessment programme’s progressive strengthening of restraint system performance criteria are compelling automakers to invest in seat belt technology beyond regulatory compliance minima. Germany accounts for approximately 28.4% of European revenues as the region’s largest automotive manufacturing market. Volkswagen Group, BMW, Mercedes-Benz, and Stellantis’ European operations represent the most demanding OEM seat belt procurement specifications in the market, as premium vehicle programmes require the highest-performance pretensioner, load limiter, and increasingly active restraint system capabilities to achieve the Euro NCAP five-star ratings whose commercial importance to European vehicle sales performance is now a primary engineering programme investment driver.

ZF’s establishment of its LIFETEC division as an independent passive safety business unit in FY 2024 demonstrates the strategic commercial importance that major automotive component suppliers assign to the restraint systems category. LIFETEC operates globally across more than 20 countries and opened a new headquarters in Shanghai to serve the Asian market. This organisational investment signals the long-term commercial commitment that tier-1 suppliers are making to the seat belts and restraint systems segment as technology complexity and per-unit value continue to increase across successive vehicle programme generations.

Asia Pacific Automotive Seat Belts Market Insights

Asia Pacific is the fastest-growing regional automotive seat belts market, driven by the region’s combination of the world’s highest annual vehicle production volumes, rapidly tightening occupant safety regulations across multiple national markets, and the progressive expansion of seat belt technology specifications from premium to mainstream vehicle segments. China accounts for approximately 54.6% of Asia Pacific revenues through its extraordinary vehicle production scale and an active domestic seat belt regulatory enforcement programme that has raised compliance rates progressively across the country’s large commercial and passenger vehicle fleet.

India and Southeast Asia represent the most commercially significant emerging market growth opportunities within Asia Pacific. India’s progressive tightening of CMVR safety standards and the growing influence of Bharat NCAP crash test ratings on domestic vehicle purchase decisions are creating commercial motivation for Indian OEMs to invest in seat belt technology upgrades across their mainstream vehicle programmes. Tokai Rika’s expansion of its manufacturing operations to support North American and Asian OEM demand, and Hyundai Mobis’ partnership with Bosch to develop next-generation smart pretensioner technology, reflect the supply chain investment the region’s growing OEM demand is attracting.

MEA & Latin America Automotive Seat Belts Market Insights

The Middle East and Africa and Latin America are growing automotive seat belts markets where rising vehicle production, expanding mandatory seat belt legislation, and the entry of international vehicle brands establishing regional manufacturing operations are creating growing demand for compliant restraint systems across both OEM and aftermarket channels. Saudi Arabia leads MEA revenues at approximately 31.2% of the regional total through its significant vehicle import volume, a domestic seat belt enforcement programme whose compliance rate has improved materially under Vision 2030’s road safety objectives, and the establishment of local vehicle assembly operations that require compliant seat belt supply.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its significant domestic vehicle production base. Brazilian regulatory CONTRAN seat belt enforcement applies to all vehicle occupants and creates structural procurement demand for replacement and OEM seat belt assemblies. The aftermarket channel is commercially significant in Brazil, where the large in-service fleet age and above-average annual mileage create consistent brake pad and seat belt maintenance replacement events that sustain independent aftermarket distributor and retailer activity across the country’s geographically extensive automotive service network.

Market Dynamics

Growth Drivers: Tightening global occupant safety regulations, rising vehicle production in emerging markets, and smart restraint technology elevating per-unit content value across OEM programmes

Regulatory strengthening is the most reliable commercial growth driver in the automotive seat belts market. Mandatory seat belt legislation creates non-discretionary procurement demand that is independent of consumer preference and largely insulated from economic cycle pressures. Each time a government raises the minimum performance standard for occupant restraint systems, the per-vehicle seat belt content value increases as existing compliant products require engineering upgrades. This regulatory escalation cycle has been consistent across North America, Europe, and progressively across Asia Pacific and Latin America.

Smart restraint system technology is simultaneously expanding per-unit commercial value beyond regulatory compliance requirements. OEMs competing for five-star NCAP ratings specify pretensioner, load limiter, and increasingly active restraint capabilities that each add engineering content and revenue value to the seat belt assembly. This technology investment cycle is compounding with vehicle production volume growth to create market revenue growth that substantially exceeds the underlying vehicle unit production growth rate.

Restraints: Commodity pressure on standard webbing and retractor components, vehicle production cycle volatility affecting OEM order volumes, and aftermarket counterfeit seat belt product penetration

Standard seat belt webbing, retractors, and buckle assemblies face significant commodity pricing pressure in markets where multiple approved suppliers compete for OEM contracts on cost. This margin compression is particularly challenging for suppliers whose product mix is concentrated in standard-specification components without significant pretensioner or active system content. The pricing floor established by lower-cost Asian manufacturers serving emerging market OEMs creates reference price pressure that influences procurement negotiations even for higher-specification products in mature markets.

Counterfeit seat belt products in the aftermarket represent both a safety risk and a commercial challenge. Substandard replacement belts that fail to meet original performance specifications circulate in price-sensitive aftermarket segments, particularly in developing markets where enforcement of automotive safety component quality standards is limited. This counterfeit penetration reduces the addressable premium replacement market for legitimate seat belt manufacturers whose certified-quality products compete against uncertified alternatives at materially lower price points.

Opportunities: EV-specific restraint system adaptation, active seat belt integration with ADAS pre-crash systems, and regulatory expansion into previously unregulated commercial vehicle occupant positions

Electric vehicle platform architectures create specific commercial opportunities for seat belt system adaptation. Battery floor integration in EVs modifies the seat mounting geometry and restraint anchor point positioning relative to conventional ICE vehicles. Seat belt suppliers who develop EV-specific pretensioner and anchor configurations that are validated for EV structural platforms gain first-mover specification advantages in OEM programmes. Bosch’s ECE R16 approval for its modular buckle pretensioner designed for EV platform integration reflects the commercial importance that regulatory pre-approval carries in accelerating EV programme adoption timelines.

ADAS pre-crash integration with seat belt active tensioning represents the most commercially advanced near-term development pathway, where radar and camera-detected pre-crash threat information triggers belt pre-tensioning before impact confirmation rather than at crash onset. This performance advantage is quantifiable in reduced occupant injury severity during real-world crash events. OEMs whose crash test performance demonstrates this capability are achieving improved NCAP ratings that create direct commercial return on the system investment.

Recent Developments:

-

2025: Joyson Safety Systems launched its Smart-Tension active seat belt technology in March 2025, featuring occupant-aware sensor integration that adapts restraint force based on occupant size and seating position, representing the commercial realisation of adaptive restraint technology that OEM safety engineering teams had been developing in collaboration with tier-1 suppliers across multiple vehicle programme generations.

-

2025: Robert Bosch GmbH received ECE R16 regulatory approval for its new modular buckle pretensioner in May 2025, designed specifically for simplified integration into electric vehicle floor architectures in European markets, validating the engineering approach of adapting proven pyrotechnic restraint technology to the spatial constraints that battery platform architectures impose on safety component packaging design.

-

2024: Hyundai Mobis and Bosch entered a strategic partnership in Q2 2024 to jointly develop next-generation smart seat belt pretensioner systems, combining real-time crash detection sensing with adaptive restraint force management to improve occupant protection outcomes in the increasingly complex collision scenarios that higher-speed mixed-traffic environments create across global road networks.

Automotive Seat Belts Market Key Players

-

Autoliv Inc.

-

ZF Friedrichshafen AG

-

Joyson Safety Systems

-

Continental AG

-

Robert Bosch GmbH

-

Tokai Rika Co., Ltd.

-

Hyundai Mobis Co., Ltd.

-

Denso Corporation

-

Toyoda Gosei Co., Ltd.

-

Ashimori Industry Co., Ltd.

-

Key Safety Systems Inc.

-

Far Europe Inc.

-

Goradia Industries

-

Schrader International Inc.

-

AmSafe Inc.

-

Takata Corporation

-

Nihon Plast Co., Ltd.

-

Special Devices Inc.

-

Holmbergs Safety System Holding AB

-

Seatbelt Solutions LLC

Automotive Seat Belts Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.97 Billion |

| Market Size by 2035 | USD 32.45 Billion |

| CAGR | CAGR of 5.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Belt Type (Three-Point, Two-Point, Others) • By Technology (Pretensioner, Load Limiter, Active/Smart Seat Belts, Inflatable Seat Belts, Others) • By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles) • By Sales Channel (OEM, Aftermarket) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Autoliv Inc., ZF Friedrichshafen AG , Joyson Safety Systems, Continental AG, Robert Bosch, GmbH, Tokai Rika Co., Ltd., Hyundai Mobis Co., Ltd., Denso Corporation, Toyoda Gosei Co., Ltd., Ashimori Industry Co., Ltd., Key Safety Systems Inc., Far Europe Inc., Goradia Industries, Schrader International Inc., AmSafe Inc., Takata Corporation , Nihon Plast Co., Ltd., Special Devices Inc., Holmbergs Safety System Holding AB, Seatbelt Solutions LLC |

Frequently Asked Questions

North America dominated the Automotive Seat Belts Market in 2025, with the United States accounting for approximately 82.5% of North American revenues.

Pretensioner seat belts dominated with approximately 64% of market revenues in 2024.

Tightening global occupant safety regulations creating non-discretionary compliance-driven procurement demand, rising vehicle production volumes in emerging markets expanding the total seat belt addressable market, and smart restraint technology integration elevating per-unit commercial value across OEM programmes beyond the level that commodity webbing and retractor supply generates.

The Automotive Seat Belts Market was valued at USD 18.97 Billion in 2025.

The Automotive Seat Belts Market is expected to grow at a CAGR of 5.56% from 2026 to 2035.

Get in Touch