Autonomous Last Mile Delivery Market Report Scope & Overview:

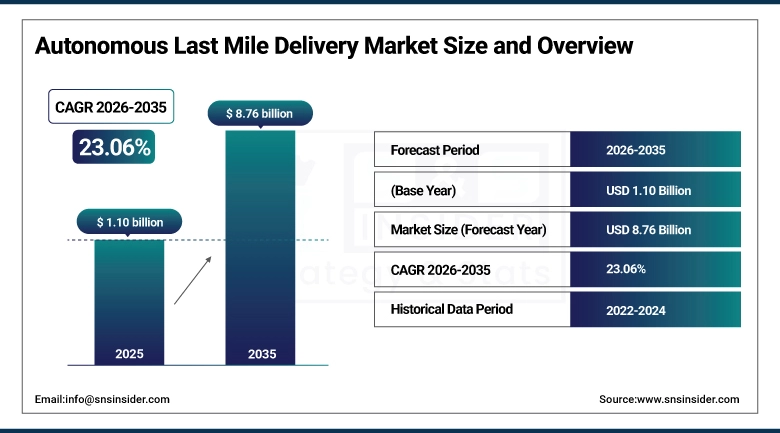

The Autonomous Last Mile Delivery Market size was valued at USD 1.10 Billion in 2025 and is projected to reach USD 8.76 Billion by 2035, growing at a CAGR of 23.06 % during 2026–2035.

Autonomous Last Mile Delivery Market is growing at a rapid pace due to the increase in the number of e-commerce transactions, the rising need for faster and touchless delivery services, and the increase in labor costs. Improvements in artificial intelligence, robotics, and drones are providing the means for efficient and assured delivery services. Congestion is also a factor because of the requirement to reduce the time for deliveries. In addition, government regulations are also encouraging the deployment of autonomous last-mile delivery due to the development of smart cities.

Autonomous Last Mile Delivery Market Size and Forecast:

-

Market Size in 2025: USD 1.10 Billion

-

Market Size by 2035: USD 8.76 Billion

-

CAGR: 23.06% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Autonomous Last Mile Delivery Market - Request Free Sample Report

Key Autonomous Last Mile Delivery Market Trends:

-

Drone & Robotic Deliveries: Increasing deployment of autonomous drones and ground robots for faster and efficient deliveries.

-

AI & Route Optimization: Growing use of AI-driven analytics for real-time tracking, route planning, and fleet management.

-

Contactless Delivery Demand: Rising preference for safe, touch-free delivery solutions among consumers.

-

Electric & Sustainable Vehicles: Adoption of eco-friendly autonomous vehicles to reduce carbon emissions.

-

E-commerce Expansion: Rapid growth in online shopping driving demand for faster last mile delivery solutions.

-

Smart City Integration: Increasing alignment with smart city infrastructure for seamless and automated logistics operations.

U.S. Autonomous Last Mile Delivery Market Size Outlook:

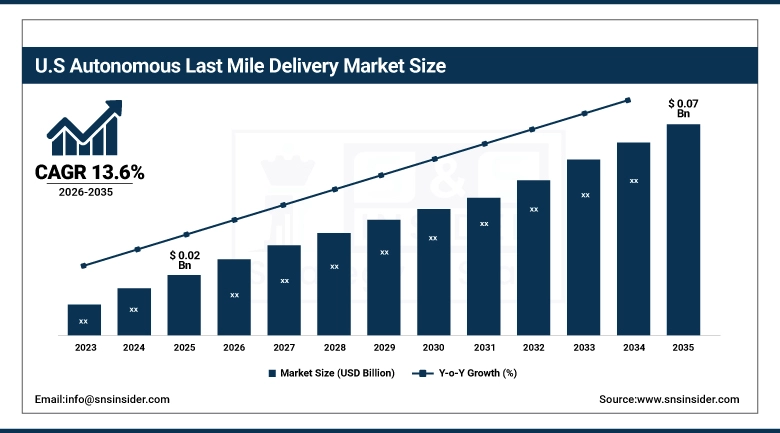

The U.S. Autonomous Last Mile Delivery Market was valued at USD 0.02 Billion in 2025 and is projected to reach USD 0.07 Billion by 2034, growing at a CAGR of 13.6% during the forecast period, Growth factors include increasing e-commerce demand, labor shortages, advancements in autonomous vehicles, cost efficiency in last-mile logistics, and regulations, which help facilitate faster, safe, and efficient deliveries while cutting costs for retailers and logistics companies.

Autonomous Last Mile Delivery Market Key Drivers:

-

The importance of autonomous vehicles in addressing the need for quicker, affordable solutions in the e-commerce industry.

With the development of e-commerce and online shopping, there is an enormous influence on the demand for fast and efficient last-mile delivery. More and more customers resort to e-commerce and need their purchases to be delivered as soon as possible. Subsequently, businesses that establish and offer these delivery services face the necessity of developing added value for their customers by accelerating and optimizing the process of delivery. At the same time, there is the challenge of reducing operational costs, and many companies solve it with the help of autonomous delivery vehicles as the solution to the challenges of last-mile delivery. The advantages of online shopping for customers have aggravated the situation with different aspects of delivery. Customers want to benefit from instrumental convenience and order their desired purchases online. However, the same customers demand the delivery of these purchases shortly and as soon as possible. These factors determine the benefits and the promise of implementing autonomous last-mile delivery systems.

Autonomous Last Mile Delivery Market Key Restraints:

-

Addressing safety concerns and public acceptance challenges in the autonomous last mile delivery market.

Public acceptance and safety concerns present major restraints for the Autonomous Last Mile Delivery Market. While autonomous vehicles offer many advantages, safety concerns, and their potential unreliability give cause for concerns. High-profile accidents and other instances of autonomous vehicles malfunctioning can erode public faith in these vehicles, thereby reducing public acceptance of autonomous delivery solutions. Safety concerns for autonomous systems extend beyond single events and vehicle operators. Autonomous vehicles will need to operate in complex urban environments, at much lower speeds than many other vehicles, and so must take into account many variables such as pedestrians, cyclists, other vehicles, road conditions, and weather. The relatively high number of variables that may change rapidly makes it difficult to predict all potential issues for autonomous vehicles, thereby necessitating constant testing and monitoring.

Autonomous Last Mile Delivery Market Key Opportunities:

-

Autonomous Last Mile Delivery Market Growth Opportunities Driven by E-commerce Expansion and Contactless Delivery Demand

The growing popularity of electronic commerce platforms and the changing nature of consumers’ needs for speedy delivery of products without human contact are key growth opportunities for the Autonomous Last Mile Delivery Market. As the popularity of electronic commerce is rising rapidly, the need for same-hour or same-day delivery is becoming an imperative for retailers. The autonomous delivery system is an opportunity for the future of logistics because it is helping the retail industry to be more efficient. In addition, the growing needs for contactless delivery are also adding to the growth of the autonomous delivery system.

Autonomous Last Mile Delivery Market Segments:

-

By Platform: In 2025, Ground Delivery Vehicles dominated with 58% share; Aerial Delivery Drones fastest growing segment during 2026–2035

-

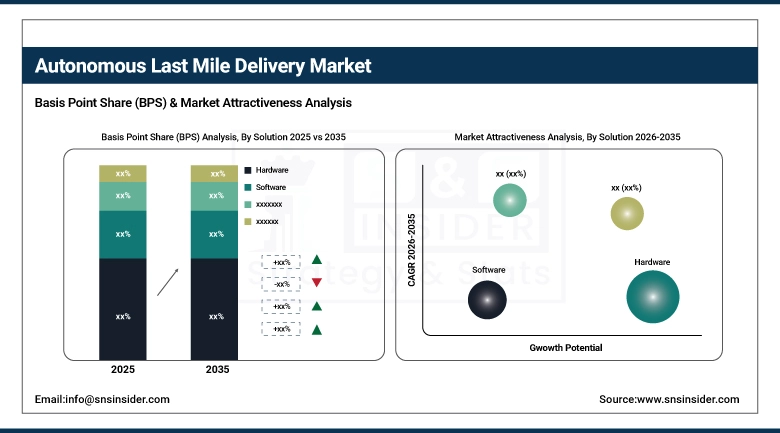

By Solution: In 2025, Hardware dominated with 55% share; Software fastest growing segment during 2026–2035

-

By Range: In 2025, Short Range dominated with 62% share; Long Range fastest growing segment during 2026–2035

-

By End User: In 2025, Retail dominated with 46% share; Healthcare fastest growing segment during 2026–2035

By Solution: Hardware Leads as Software Expands Rapidly

Hardware is the dominant segment of the market because it includes the necessary equipment like sensors, cameras, LiDAR, and autonomous vehicles/drones, etc., necessary for the delivery process. High initial investment is also a key factor for the dominance of the hardware segment because of the investments made in the equipment. Continuous innovation in robotics technology is also adding to the dominance of the segment.

The software segment is growing at a faster rate because of the increasing requirement for route optimization, fleet management, real-time tracking, etc. The requirement for advanced autonomous technology is increasing due to the complexities of autonomous technology.

By Platform: Ground Delivery Vehicles Lead as Aerial Delivery Drones Expand Rapidly

Ground Delivery Vehicles lead in the Autonomous Last Mile Delivery Market owing to their higher load-carrying capacity and reliability. These vehicles are widely used by various logistics companies and retailers for grocery, parcel, and food deliveries over short distances. In addition, their use of existing infrastructure and fewer regulatory hurdles also contribute to their leadership.

Aerial Delivery Drones are growing rapidly in the Autonomous Last Mile Delivery Market owing to their faster delivery times, especially in areas where traffic is heavy and distances are long, such as in urban and rural areas. In addition, their ability to circumvent traffic and save time also contributes significantly to their growth in the Autonomous Last Mile Delivery Market. Advances in technology and approvals for their use also contribute to their growth.

By Range: Short Range Leads as Long Range Expands Rapidly

Short Range dominates the market share as most last mile deliveries take place within a short distance, which is usually within a few kilometers. These solutions are used for food delivery services, grocery services, etc., as they require timely completion.

Long Range solutions are witnessing tremendous growth with advancements in battery technology and better navigation tools. These solutions are gaining popularity for deliveries between cities and rural areas, which lack proper infrastructure for logistics.

By End User: Retail Leads as Healthcare Expands Rapidly

Retail leads in the Autonomous Last Mile Delivery Market because of the increase in e-commerce and online shopping. Retail businesses depend on efficient last mile delivery services to ensure timely delivery to customers. This has led to a significant increase in the adoption of autonomous technologies in retail businesses.

Healthcare is another segment that is witnessing significant growth in autonomous delivery services. Autonomous delivery services are being increasingly used to transport medicines, medical supplies, and laboratory samples. Autonomous delivery services are being used in hospitals to ensure timely delivery in critical situations.

Autonomous Last Mile Delivery Market Regional Analysis:

North America Autonomous Last Mile Delivery Market Insights:

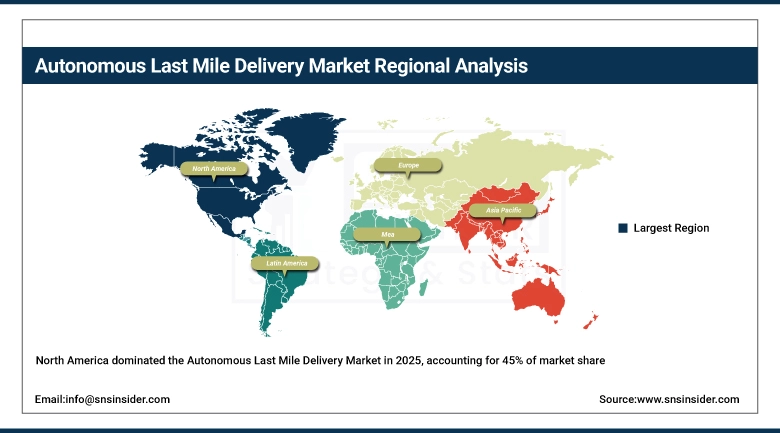

North America dominated the market in 2025, capturing a market share of 45%. This is because of advanced technological infrastructure, high investment in research and development of autonomous vehicles, and a large number of technology leaders. Amazon and Google are setting the pace in the market. Amazon is deploying autonomous robots for delivery in some areas, and Alphabet, the parent company of Google, is making large investments in autonomous vehicle technology through Waymo. The regulations in the U.S. and Canada, and their large consumer base, are helping the region hold a strong position in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Autonomous Last Mile Delivery Market Insights:

The Asia-Pacific region is stated to experience a faster CAGR in the forecast period of 2026-2035. This can be explained by the high rate of urbanization, rise in the number of people in the middle class, and the rise in investments in smart city initiatives. China and Japan are at the forefront of embracing autonomous delivery technology, with different corporations channeling funds towards autonomous delivery robots and drones. For instance, delivery robots from JD.com can be seen in different parts of China.

Europe Autonomous Last Mile Delivery Market Insights:

Europe also accounts for a considerable portion of the Autonomous Last Mile Delivery Market due to robust regulatory support, high levels of infrastructure, and a high rate of adoption of automation technologies. Countries like Germany, the UK, and France are leading in terms of autonomous delivery robot and drone pilots. The focus on sustainable development and reduction of carbon emissions in Europe is also acting as a booster to autonomous delivery vehicles.

Latin America Autonomous Last Mile Delivery Market Insights:

The Autonomous Last Mile Delivery Market in Latin America is observing a positive growth trend with the increasing popularity of e-commerce and better digital technologies. Brazil and Mexico are among the countries adopting Autonomous Last Mile Delivery solutions to resolve issues related to urban congestion. Investments in logistics technologies and demand for speedy deliveries are contributing to the growth of the market.

Middle East & Africa (MEA) Autonomous Last Mile Delivery Market Insights:

The MEA region is seen as a new promising market for autonomous last-mile delivery as there is an increase in smart city initiatives and investments in advanced technology. Countries such as the UAE and Saudi Arabia are exploring autonomous delivery by drones and autonomous vehicles to boost the efficiency of logistics in their regions. Moreover, there is a need to overcome infrastructure challenges in accessing remote areas.

Autonomous Last Mile Delivery Market Competitive Landscape:

Airbus S.A.S is a renowned aerospace and autonomous mobility company that is currently involved in the Autonomous Last Mile Delivery Market through the development of advanced drone technology and urban air mobility systems. The company has been utilizing its experience in aviation, automation, and navigation systems to provide efficient and scalable aerial delivery services, especially in logistics and emergency situations.

-

In 2025, Airbus expanded its autonomous drone initiatives by enhancing its cargo drone capabilities, focusing on improved payload capacity and long-distance delivery efficiency for commercial logistics operations.

Matternet is a leading autonomous drone delivery service that provides urban logistics and medical delivery networks. Its services combine drone delivery systems with cloud-based software platforms to facilitate efficient, reliable, and secure transportation of medical supplies, laboratory specimens, and small packages in a populated environment.

-

In 2025, Matternet strengthened its partnerships with healthcare providers and logistics firms to expand its drone delivery networks, improving operational efficiency and reducing delivery times in urban environments.

Flirtey is an innovative drone delivery company committed to creating autonomous aerial solutions for e-commerce, food delivery, and healthcare industries. It has been recognized for pioneering drone delivery services and pushing the boundaries for approvals for commercial drone use.

-

In 2025, Flirtey advanced its next-generation drone systems with enhanced safety features and extended flight range, supporting broader adoption of autonomous delivery services across commercial applications.

Autonomous Last Mile Delivery Companies are:

-

Airbus S.A.S.

-

Flirtey

-

Drone Delivery Canada

-

Flytrex

-

Amazon.com

-

JD.com Inc.

-

Marble Robot

-

Savioke

-

DHL International GmbH

-

United Parcel Service of America, Inc.

-

DPD

-

Amazon

-

Starship Technologies

-

Nuro

-

Wing (Alphabet)

-

FedEx

-

UPS

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.10 Billion |

| Market Size by 2035 | USD 8.76 Billion |

| CAGR | CAGR of 23.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Ground Delivery Vehicles, Aerial Delivery Drones) • By Solution (Hardware, Software, Services) • By Range (Short Range, Long Range) • By End User (Food & Beverages, Retail, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Airbus S.A.S., Matternet, Flirtey, Drone Delivery Canada, Flytrex, Amazon.com, JD.com Inc., Marble Robot, Starship Technologies, Savioke, DHL International GmbH, United Parcel Service of America, Inc., DPD, Amazon, Starship Technologies, Nuro, Wing (Alphabet), FedEx, UPS. |

Frequently Asked Questions

The Autonomous Last Mile Delivery Market size was valued at USD 1.10 Billion in 2025 and is projected to reach USD 8.76 Billion by 2035.

The Autonomous Last Mile Delivery Market is expected to grow at a CAGR of 23.06% during 2026-2035.

The importance of autonomous vehicles in addressing the need for quicker, affordable solutions in the e-commerce industry.

The Ground Delivery Vehicles segment dominated the Autonomous Last Mile Delivery Market.

North America dominated the Autonomous Last Mile Delivery Market in 2025.

Get in Touch