Balloon Valvuloplasty Devices Market Size & Trends:

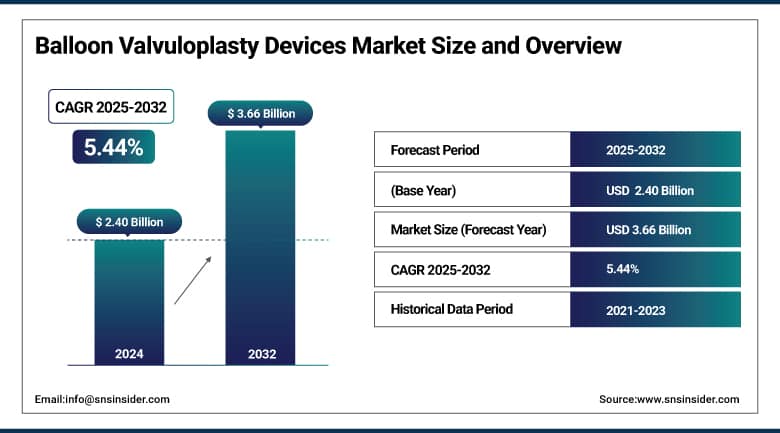

The Balloon Valvuloplasty Devices Market size was valued at USD 2.40 billion in 2024 and is expected to reach USD 3.66 billion by 2032, growing at a CAGR of 5.44% over the forecast period of 2025-2032.

The global balloon valvuloplasty devices market is projected to observe steady growth owing to the increasing number of valvular heart diseases, such as aortic and pulmonary stenosis, among the aging population. Decline of open heart surgeries and increasing applications of pediatric surgeries are also driving the growth of the market. Other factors contributing to the growth of the market are technological advancements in balloon design and increased use in ambulatory settings. Emerging economies with favorable reimbursement policies will help the market to continue to grow through 2032.

To Get More Information On Balloon Valvuloplasty Devices Market - Request Free Sample Report

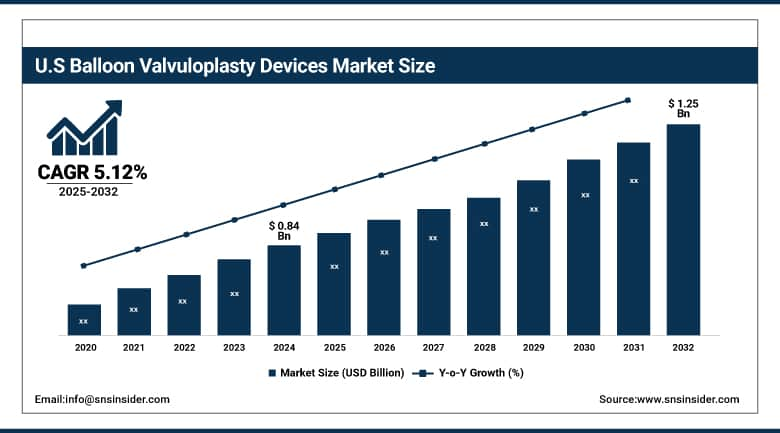

The U.S. Balloon Valvuloplasty Devices Market size was valued at USD 0.84 billion in 2024 and is expected to reach USD 1.25 billion by 2032, growing at a CAGR of 5.12% over the forecast period of 2025-2032.

In North America, the U.S. is anticipated to be a significant contributor balloon valvuloplasty devices market growth, owing to its advanced healthcare infrastructure, early adoption of minimally invasive cardiac procedures, and a high prevalence of valvular heart diseases. Coupled with robust clinical research infrastructure, a large number of interventional cardiologists, and favorable reimbursement policies, the country remains a leader within the region.

Balloon Valvuloplasty Devices Market Dynamics:

Drivers

-

Increased Incidence of Heart Disorders Related to Valves is Driving the Market Growth

Valvular heart diseases, especially aortic and pulmonary valve stenosis, are becoming more prevalent globally, particularly in the elderly population. For instance, calcific aortic stenosis is one of the most frequently diagnosed valve diseases in the elderly and is generally due to age-related calcification of the valve. The global burden of these diseases continues to increase due to aging populations, emerging lifestyle-related risk factors (especially hypertension and diabetes), and advancements in diagnostic technology. Balloon valvuloplasty is a less invasive procedure that is suitable for patients who are not best suited for open-heart surgery. It is the procedure of choice in the high-risk and elderly patient population. With the increasing number of cases being diagnosed, the need for an effective treatment modality, such as balloon valvuloplasty is on the rise.

-

Advancements in Device Technology are Propelling the Market Growth

Major advancements in technology have made balloon valvuloplasty a safer, more precise, and more successful procedure. Currently available new-generation balloons, including high-pressure balloons and scoring balloons, provide greater control in handling on dilation with effective treatment even in heavily calcified or fibrotic valves. They are designed to provide more localized and controlled expansion, hence causing less injury to adjacent tissues and lower rates of complications such as restenosis or valve rupture. Furthermore, enhanced delivery systems for the catheter, and image integration, have made the procedure more accurate and attracted interventional cardiologists to the larger utilization of this approach. Advance in technology makes the treatment more effective and also broaden the scope of patients suitable for balloon valvuloplasty.

Restraints:

-

Short-Term Efficacy and Risk of Restenosis are Restraining the Market from Growing

The main disadvantage of balloon valvuloplasty is its transient effect, particularly in adults with aortic valve stenosis. Although this technique effectively widens a stenosed valve and allows blood to flow more freely in the short term, the valve often then becomes stenosed again after some time, a process called restenosis. In the majority of adult cases, this recurrence can occur within 6 to 12 months after the procedure, necessitating repeat interventions or valve replacements.

In older patients, valve structures are calcified and fibrotic, resulting in less responsive tissue to balloon dilation and hence an increased risk of restenosis. Consequently, balloon valvuloplasty is more of a palliative or bridging treatment rather than a definitive treatment. This short durability is less desirable than more durable therapies such as TAVR or surgical valve replacement, especially in patients who are well enough to consider them.

Balloon Valvuloplasty Devices Market Segmentation Analysis:

By Product Type

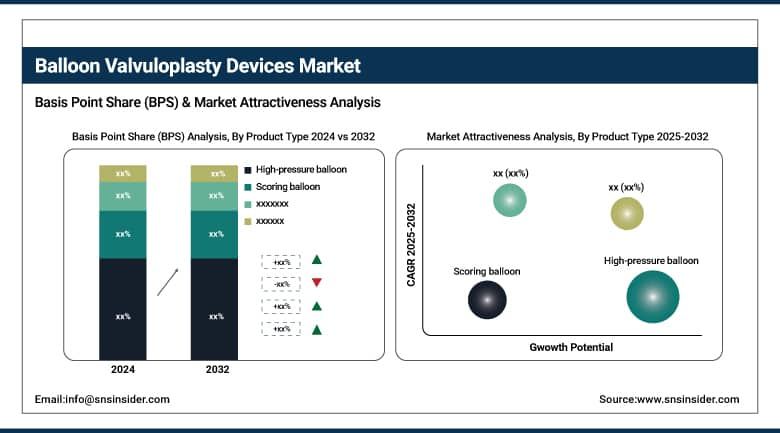

The high-pressure balloon segment accounted for the largest market share in 2024, with a 45.80% market share. These are much more powerful balloons with higher burst pressure and are useful for opening heavily stenosed valves, especially in elderly patients with calcific aortic stenosis. The ability to be used independently or as preparation for transcatheter valve replacements has further added to their adoption in hospitals and cardiac centers, making them the leading market share holder.

The scoring balloon segment is expected to register the fastest growth during the forecast period. The demand for precision with controlled plaque modification in complex valvular cases drives this growth. These scoring balloons contain special components that exert a concentrated force, producing a more efficient dilation with minimal vessel injury. Scoring balloons are gaining popularity among interventional cardiologists as these devices achieve both an improved safety and procedural success profile with the continuing evolution of minimally invasive skills, which are needed particularly in complex and high-risk patient populations.

By Application

In 2024, the aortic valve stenosis segment led the balloon valvuloplasty devices market share with 66.2%, owing to the high population with this condition among the geriatric population. Aortic stenosis is among the commonest and most serious of valvular heart diseases and is one of the most frequent indications for intervention in the older population. Balloon aortic valvuloplasty (BAV) is often employed as a bridge-to-surgery or TAVR in high-risk surgical patients. The high share of the segment is mainly driven by the increasing prevalence of degenerative valve diseases and the high availability of interventional cardiology services in developed regions.

The pulmonary valve stenosis segment is expected to grow at the fastest rate in the forecast period on account of the growing number of congenital heart defects in neonates and pediatrics. Balloon pulmonary valvuloplasty is a standard treatment for these patients and has recorded good outcomes in pediatric cohorts over the long term. A rise in the need for pediatric cardiology is propelled by increased utilization of technology, awareness, and increasing access to advanced care in developing markets. In addition, the advancements in neonatal screening along with early intervention strategies are increasing the treatment rates and this segment is projected to grow at a healthy pace.

By Age Group

In 2024, the adult segment dominated the balloon valvuloplasty devices market with an 84.25% market share, due to the rapidly growing degenerative valvular diseases seen in the elderly population, especially aortic valve stenosis. Calcific valve disease is primarily found in adults, more often than not in older patients aged over 65 years, and typically treated least invasively (balloon valvuloplasty), as a treatment or at least as a bridge to operative valve replacement. This segment's dominance can be attributed, in part, to improved availability of diagnostic tools, interventional facilities, and established reimbursement frameworks in developed regions.

The fastest growth is anticipated in the Pediatric segment. This growth is mainly driven by a greater awareness and increased identification of congenital heart defects, including a stenosis of the pulmonary valve, that are more common in children. Minimally invasive and with excellent long-term results, balloon valvuloplasty is often the first indication that the condition exists in pediatric cases. Moreover, investing in introducing more pediatric cardiac care, advancement in neonatal screening programs, and adaptation toward pediatric cardiology services in developing economies will also drive this segment most rapidly.

By End-Use

In 2024, the Hospitals segment dominated the balloon valvuloplasty devices market with a 63.11% market share due to the infrastructure and expertise to address and treat high-risk and complicated valvular procedures. The deployment of comprehensive cardiac healthcare practices facilitates the repair of multiple valvular regions while minimizing hospital stay times through the use of balloon valvuloplasty devices. Hospitals tend to be the main location for complex cardiovascular interventions such as balloon valvuloplasty, especially with acute or emergent care.

The Ambulatory Surgical Centres (ASCs) segment is expected to witness the fastest growth during the forecast period as the cost-effective nature and value of same-day cardiac procedures drive demand. With the development of newer balloon catheter technologies and enhanced patient safety practices, it has become feasible for select valvuloplasty cases to be performed in an outpatient setting. Analysis notes that the ASC model provides shorter procedures, shorter hospital stays, and therefore lower cost of care, all of which may contribute to its growing preference among its patient and provider base. The trend toward value-based care and less invasive procedures remains a tailwind, and it continues to bolster ASC growth across developed and emerging markets.

Balloon Valvuloplasty Devices Market Regional Insights:

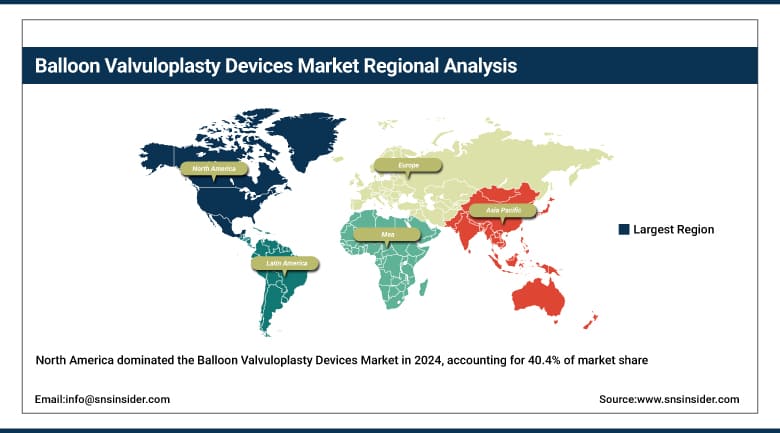

The balloon valvuloplasty devices market is dominated by North America with a 40.4% market share in 2024 due to having an ideal healthcare infrastructure, a large population, good awareness regarding structural heart diseases, advanced cardiac intervention technology, early adoption for diagnostics and treatment, and evolving reimbursement policies. Despite the limitations in the procedure, balloon valvuloplasty is performed globally, and constant clinical research activity and leading MD companies are present in India, which together explain the overuse of this procedure, especially in aortic valve stenosis.

Get Customized Report as Per Your Business Requirement - Enquiry Now

The fastest growing region in the balloon valvuloplasty devices market is in Asia Pacific with a 6.00% CAGR over the forecast period due to the increasing accessibility to health care services, increasing incidence of rheumatic and congenital cardiovascular diseases, along with an aging population. Growth of the market include rapid development of healthcare infrastructure, rising investments by international and domestic device manufacturing companies, and increasing awareness toward the advanced treatment methods, including minimally invasive techniques, which are primarily boosting the growth of the market. In addition, the increasing medical tourism in countries, such as India, China, and Thailand, along with favorable government initiatives, is contributing to the growth of the region.

The balloon valvuloplasty devices market in the European region is growing at a significant rate due to the increases in the healthcare infrastructure and the number of interventional cardiology procedures. The presence of a large geriatric population is resulting in a higher prevalence of valvular heart diseases in the region, which, in turn, will continue to spur the demand for balloon valvuloplasty, as it is preferred in hospitals for minimally invasive treatment of VHD. In addition, high adoption of enhanced medical devices and availability of well-established medical centers in countries, such as Germany, France, and the U.K. are expected to maintain steady market growth.

Moderate growth of the balloon valvuloplasty devices market is in Latin America due to a growing focus on minimally invasive cardiac procedures and improving healthcare infrastructure. As access to interventional cardiology services expands in countries, there is a slow but increasing adoption of balloon valvuloplasty. Despite the issues, such as restricted reimbursement coverage and economic constraints in the region, continuous funding for public health care and awareness generation is responsible for the balloon valvuloplasty devices market growth.

Moderate growth in the MEA region is supported by high incidences of cardiovascular diseases and growing efforts in the modernization of healthcare systems. Higher-income countries with much higher access to technology (and health-care), such as Saudi Arabia, the UAE, and South Africa, there is more growth concentrated. The growth of the market is still being restrained by slower conditions of advanced medical technology adoption and inequitable access to health services that are still prevailing in many places throughout the region. However, the renewed focus on enhancing cardiac care is anticipated to uphold a steady but gradual growth of the market despite these challenges.

Balloon Valvuloplasty Devices Market Key Players:

-

Edwards Lifesciences Corporation

-

Boston Scientific Corporation

-

Meril Life Sciences Pvt. Ltd.

-

B. Braun Melsungen AG

-

Cordis (a Cardinal Health company)

-

Balton Sp. o.o.

-

JenaValve Technology, Inc.

-

Translumina Therapeutics LLP

Recent Developments in the Balloon Valvuloplasty Devices Market:

-

March 2024 – Boston Scientific Corporation announced that it has received approval from the U.S. Food and Drug Administration (FDA) for its AGENT Drug-Coated Balloon (DCB). The device is cleared for the treatment of coronary in-stent restenosis (ISR) in patients with coronary artery disease. ISR is the re-narrowing or blockage of a stented blood vessel that occurred previously due to plaque accumulation or scarring.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.40 Billion |

| Market Size by 2032 | USD 3.66 Billion |

| CAGR | CAGR of 5.44% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Standard Balloon, Cutting Balloon, Scoring Balloon, High-Pressure Balloon, Low-Pressure Balloon) • By Application (Aortic Valve Stenosis, Pulmonary Valve Stenosis) • By Age Group (Pediatric, Adult) • By End-use (Hospitals, Ambulatory Surgical Centres, Specialty Clinics, Other End-users) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Boston Scientific Corporation, Edwards Lifesciences Corporation, Medtronic plc, Meril Life Sciences Pvt. Ltd., B. Braun Melsungen AG, Cordis (a Cardinal Health company), Lepu Medical Technology Co., Ltd., Balton Sp. z o.o., JenaValve Technology, Inc., Translumina Therapeutics LLP, and other players. |

Frequently Asked Questions

Ans: North America dominated the Balloon Valvuloplasty Devices Market in 2024.

Ans: The “Aortic valve stenosis” segment dominated the Balloon Valvuloplasty Devices Market.

Ans: Increased incidence of heart disorders related to valves is driving the market growth.

Ans: The Balloon Valvuloplasty Devices Market was USD 2.40 billion in 2024 and is expected to reach USD 3.66 billion by 2032.

Ans: The Balloon Valvuloplasty Devices Market is expected to grow at a CAGR of 5.44% from 2025 to 2032.

Get in Touch