Newborn Screening Market Report Scope & Overview:

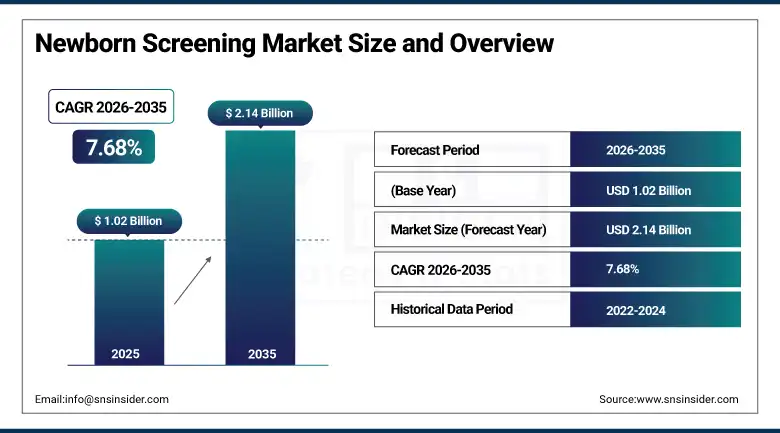

The Newborn Screening Market was valued at USD 1.02 Billion in 2025 and is expected to reach USD 2.14 Billion by 2035, growing at a CAGR of 7.68% from 2026–2035.

The global newborn screening market is advancing as an essential public health programme that enables early detection of genetic, metabolic, endocrine, and congenital disorders in neonates shortly after birth, allowing treatment initiation before irreversible organ damage, disability, or mortality occurs from conditions including phenylketonuria, congenital hypothyroidism, sickle cell disease, cystic fibrosis, and spinal muscular atrophy. Government mandates for universal newborn screening, rising parental awareness of preventable genetic disorders, and the expansion of national screening panels to include progressively rare conditions collectively sustain above-average market growth. In 2023, the United States, Germany, and Japan led global adoption through well-established screening programmes with the broadest disorder panels.

In January 2024, the U.S. Food and Drug Administration approved a new newborn screening test for spinal muscular atrophy developed by Bio-Rad Laboratories, enabling SMA detection from dried blood spot cards within the standard 24-hour screening window. The approval significantly advanced early SMA diagnosis because treatment with approved gene therapies is most effective when administered before motor neuron loss, making the pre-symptomatic identification window that newborn screening provides the critical clinical intervention point for achieving the best functional outcomes in affected infants.

Market Size and Forecast

-

Market Size in 2026E: USD 1.10 Billion

-

Market Size by 2035: USD 2.14 Billion

-

CAGR: 7.68% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Newborn Screening Market - Request Free Sample Report

Newborn Screening Market Trends

-

Next-generation sequencing integration into newborn screening panels is enabling simultaneous detection of hundreds of conditions from a single dried blood spot specimen.

-

Whole genome sequencing pilots in national programmes are expanding detectable disorder scope beyond metabolic conditions to include genomic structural variants.

-

AI-driven data analytics platforms are improving interpretation accuracy and flagging borderline screening results for expert clinical review in real time.

-

Point-of-care newborn screening devices are enabling bedside testing in neonatal intensive care units and remote health centres without laboratory infrastructure.

-

Expanded screening mandates for spinal muscular atrophy and severe combined immunodeficiency are creating growing demand for specialised enzyme and molecular assays.

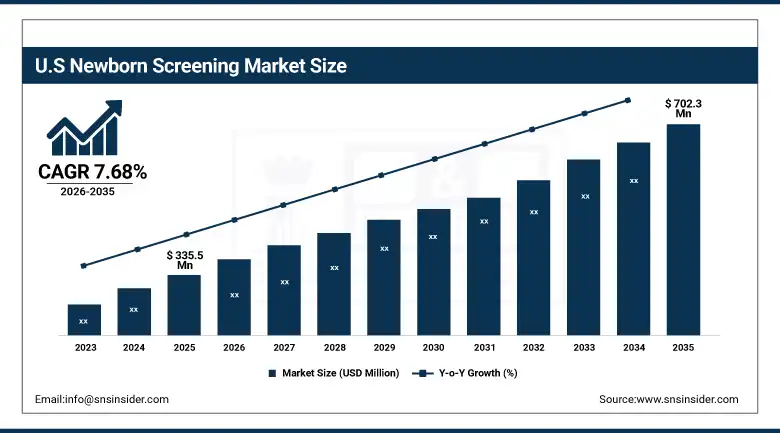

The U.S. Newborn Screening Market Outlook

The U.S. Newborn Screening Market was valued at approximately USD 335.5 Million in 2025 and is expected to reach approximately USD 702.3 Million by 2035, growing at a CAGR of approximately 7.68%.

The United States leads the global newborn screening market through its well-established mandatory state screening programmes, the broadest recommended uniform screening panel of 35 core and 26 secondary conditions, and sustained NIH funding for screening technology development. PerkinElmer, Bio-Rad Laboratories, and Natus Medical provide the primary domestic supply of screening instruments and reagents. The IRA’s expanded healthcare access provisions and the federal government’s Recommended Uniform Screening Panel updates that progressively add new disorders sustain above-average U.S. procurement growth independent of birth rate fluctuations.

In 2023, PerkinElmer launched a next-generation newborn screening platform integrating tandem mass spectrometry with advanced data analytics, improving accuracy and efficiency for multi-disorder metabolic screening from dried blood spot specimens. The platform’s simultaneous detection of over 50 metabolic and endocrine conditions from a single specimen within standard laboratory processing time reduced per-specimen cost while expanding detectable disorder scope, demonstrating the commercial direction of newborn screening toward higher-throughput, lower-cost multiplex testing platforms.

Newborn Screening Market Segment Analysis

-

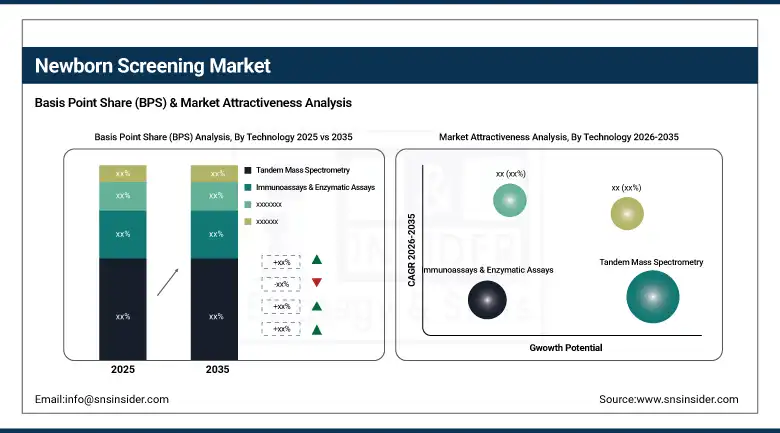

By Technology, tandem mass spectrometry segment dominated the newborn screening market with approximately 42.3% share in 2025, while the DNA Assays & Next-Generation Sequencing segment is the fastest growing with a CAGR of approximately 11.2%.

-

By Test Type, dry blood spot test segment dominated the newborn screening market with approximately 62.5% share in 2025, while the critical congenital heart disease test segment is the fastest growing with a CAGR of approximately 9.8%.

-

By Disorder Type, metabolic disorders segment dominated the newborn screening market with approximately 38.7% share in 2025, while the immune deficiency disorders segment is the fastest growing driven by expanding SCID and SMA screening mandates.

-

By End User, hospitals segment dominated the newborn screening market with approximately 51.2% share in 2025, while the diagnostic centres segment is the fastest growing with a CAGR of approximately 9.4%.

By Technology, tandem mass spectrometry dominates, NGS grows fastest

Tandem mass spectrometry retained the dominant technology position with approximately 42.3% of the newborn screening market in 2025. Its commercial primacy reflects the unmatched multiplexing capability that enables simultaneous quantification of over 40 amino acids, acylcarnitines, and organic acids from a single dried blood spot punched from a standard Guthrie card in under two minutes of instrument analysis time. The technology’s analytical sensitivity and specificity across the full panel of metabolic disorders included in most national uniform screening programmes, combined with the established laboratory infrastructure, validated reference ranges, and certified proficiency testing frameworks that decades of TMS newborn screening deployment have built, sustain TMS specification preference across new laboratory installations and programme expansions globally. PerkinElmer and Waters Corporation dominate TMS instrument supply for newborn screening laboratory applications.

DNA assays and next-generation sequencing are growing fastest at approximately 11.2% CAGR because their ability to detect conditions undetectable by metabolite-based TMS, including severe combined immunodeficiency, spinal muscular atrophy, and an expanding range of lysosomal storage diseases, creates mandatory adoption as national screening panels add these conditions. Each new FDA-approved molecular screening test for a previously unscreened condition creates non-discretionary procurement across the national network of newborn screening laboratories whose test menu expansion requirements sustain sequential assay kit and instrument procurement cycles.

By Disorder Type, metabolic disorders dominate, immune deficiency disorders grow fastest

Metabolic disorders retained the dominant disorder type position with approximately 38.7% of the newborn screening market in 2025, reflecting the foundational status of amino acid, fatty acid oxidation, and organic acid disorder screening that constitutes the original and still largest component of every national newborn screening programme globally. The 28 core metabolic conditions on the U.S. RUSP, the 30+ metabolic disorders on European national panels, and equivalent Asian programme coverage collectively create the largest per-disorder-category newborn screening test volume sustained by mandatory legal requirements in virtually every high-income and growing middle-income country. Each birth in a mandatory screening country generates a metabolic disorder panel specimen regardless of perceived risk.

Immune deficiency disorders are the fastest-growing category as the FDA approval of SCID and SMA newborn screening tests and their progressive adoption into mandatory state and national panels creates new test volume that grows with each jurisdiction adding these conditions to its required panel. The urgency of early SCID identification, where bone marrow transplantation before six months of age delivers dramatically superior outcomes compared to post-symptomatic diagnosis, creates a compelling public health case that is progressively overcoming the per-test cost barrier as screening reagent costs decline with manufacturing scale.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.6% |

|

Europe |

Germany |

23.8% |

|

Asia Pacific |

China |

42.4% |

|

Middle East & Africa |

Saudi Arabia |

28.4% |

|

Latin America |

Brazil |

43.8% |

North America Newborn Screening Market Insights

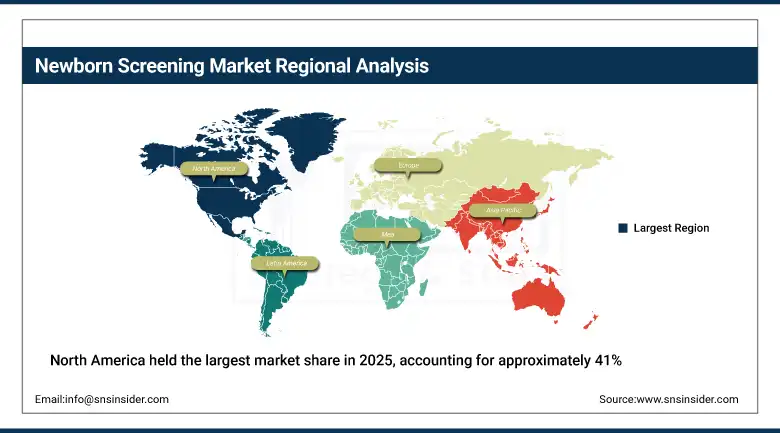

North America held the largest market share in 2025, accounting for approximately 41% of the total market revenue. This is driven by the United States’ comprehensive mandatory state screening programmes, the world’s broadest RUSP panel, and sustained federal and state public health investment in laboratory infrastructure upgrades. The United States accounts for approximately 82.6% of North American revenues through PerkinElmer’s dominant instrument supply position, Bio-Rad Laboratories’ immunoassay and molecular assay reagent leadership, and the NIH’s Eunice Kennedy Shriver NICHD-funded research in screening technology advancement.

Canada contributes supplementary regional revenues through its provincial screening programmes whose panel breadth progressively aligns with U.S. RUSP recommendations and whose laboratory modernisation investment creates consistent instrument and reagent procurement. Canadian Inherited Metabolic Diseases Research Network activities sustain academic-commercial collaboration in screening technology that reinforces the country’s adoption of emerging NGS-based screening approaches earlier than most other international markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Newborn Screening Market Insights

Europe is a technically sophisticated newborn screening market where national programme variation creates diverse technology adoption patterns ranging from Germany’s comprehensive tandem mass spectrometry panel covering 14 core disorders to the United Kingdom’s nine-condition panel and Eastern European programmes with more limited scope. Germany accounts for approximately 23.8% of European revenues through its advanced screening laboratory infrastructure, the commercial presence of PerkinElmer’s European operations, and the highest newborn screening programme completeness and follow-up rate in the European Union.

France, the Netherlands, and Italy are significant secondary European markets whose public health investment in newborn screening infrastructure modernisation creates consistent reagent and instrument procurement. European Newborn Screening Task Force harmonisation efforts are progressively narrowing panel variation across EU member states, creating growing demand for the tandem mass spectrometry and molecular assay capability required to implement expanded panel recommendations whose adoption creates systematic new test procurement across national laboratory networks.

Asia Pacific Newborn Screening Market Insights

Asia Pacific is the fastest-growing regional newborn screening market, driven by the large birth cohorts in China, India, Japan, and Southeast Asia whose newborn volumes create substantial screening test demand even at current programme coverage rates, and the rapid expansion of public health screening programmes whose government investment is progressively extending mandatory screening coverage to previously unscreened birth cohorts. China accounts for approximately 42.4% of Asia Pacific revenues through its national newborn screening programme’s multi-disorder TMS panel adoption, provincial health authority laboratory investment, and growing domestic instrument manufacturing capability.

India represents the most commercially dynamic emerging market within Asia Pacific, where the National Health Mission’s Rashtriya Bal Swasthya Karyakram programme’s progressive expansion to include metabolic disorder screening, private hospital sector’s voluntary expanded panel adoption driven by increasing parental awareness, and the growing domestic reagent manufacturing industry collectively create above-average market growth. Japan’s comprehensive screening programme and South Korea’s advanced newborn care infrastructure contribute premium regional demand through sophisticated test panel expansion.

MEA & Latin America Newborn Screening Market Insights

Saudi Arabia leads MEA revenues at approximately 28.4% through its Saudi Food and Drug Authority-mandated comprehensive newborn screening programme, the King Faisal Specialist Hospital’s leadership in regional screening programme development, and Vision 2030’s healthcare quality investment that has expanded both the screening panel breadth and laboratory infrastructure capacity. South Africa and the UAE contribute growing regional demand through their public health investment in expanded newborn screening coverage.

Brazil leads Latin American revenues at approximately 43.8% through its Programa Nacional de Triagem Neonatal’s mandatory screening coverage, the public health system’s progressive panel expansion to include PKU, congenital hypothyroidism, sickle cell disease, cystic fibrosis, and biotinidase deficiency, and the growing private hospital sector’s voluntary extended panel adoption. Mexico and Colombia are growing secondary markets where newborn screening programme formalization and laboratory infrastructure investment are progressively extending coverage.

Market Dynamics

Growth Drivers: Expanding government-mandated screening panels and technological advances enabling broader multi-disorder detection from single specimens

Rising government investment in preventive neonatal healthcare is the newborn screening market’s most structurally certain commercial growth driver. Mandatory universal screening programmes create non-discretionary annual test volumes that scale directly with national birth rates and are largely insensitive to healthcare budget cycles whose discretionary spending fluctuations do not affect legally mandated clinical programmes. Each new disorder added to a national recommended screening panel creates procurement across the entire national laboratory network for the new assay’s reagents, controls, and quality assurance materials. Tandem mass spectrometry’s ability to detect multiple disorders simultaneously from a single dried blood spot specimen, combined with declining per-specimen reagent costs as screening volumes grow, is progressively improving the healthcare economics of expanded panels that add new conditions at minimal marginal cost per specimen.

Restraints: High screening false positive rates and limited follow-up infrastructure in low-resource settings creating programme quality concerns

Newborn screening false positive rates create clinical and family distress, unnecessary follow-up testing costs, and potential erosion of family confidence in screening programmes when confirmatory testing consistently demonstrates false-positive results. Each new condition added to the screening panel introduces a specific false positive rate that compounds with existing conditions to create aggregate recall rates that overwhelm follow-up metabolic specialist capacity at expanded panel sizes. In low-resource healthcare settings across Asia, Africa, and Latin America, the absence of confirmatory testing laboratories, metabolic disease specialists, and treatment access infrastructure creates a disconnect between screening capability and treatment delivery that limits the public health benefit justification for expanded screening programmes and constrains external funding support.

Opportunities: Whole genome sequencing newborn screening pilots and dried blood spot biobanking for secondary research creating commercial frontiers

Whole genome and whole exome sequencing applied to newborn dried blood spot specimens represents the most transformative potential expansion of newborn screening capability, enabling simultaneous identification of thousands of genetic conditions from a single specimen at costs approaching USD 200 per sample that declining sequencing costs are making progressively accessible for population-scale public health programmes. National genomic newborn screening pilot programmes in the United States, United Kingdom, and Australia are generating clinical utility and economic data whose positive outcomes are expected to create regulatory and policy momentum for genome sequencing as a newborn screening modality. Dried blood spot biobanking creates a secondary commercial opportunity where long-term storage of residual newborn specimens enables retrospective genomic research, epidemiological studies, and future diagnostic testing as new biomarkers are identified.

Recent Developments:

-

2024: The U.S. FDA approved Bio-Rad Laboratories’ newborn screening test for spinal muscular atrophy, enabling pre-symptomatic SMA identification from dried blood spot specimens within the standard screening window and significantly improving outcomes for infants treated with approved gene therapies before motor neuron loss.

-

2023: PerkinElmer launched its next-generation newborn screening platform integrating tandem mass spectrometry with advanced data analytics for simultaneous detection of over 50 metabolic and endocrine conditions from a single dried blood spot specimen, improving throughput and reducing per-disorder detection cost.

-

2023: SCIEX introduced the Echo MS system adapted for newborn screening applications, providing acoustic ejection mass spectrometry-based sample introduction that eliminates chromatographic separation requirements and reduces per-specimen analysis time by approximately 80% versus conventional TMS workflows.

Newborn Screening Market Key Players are:

-

PerkinElmer Inc.

-

Bio-Rad Laboratories Inc.

-

Natus Medical Incorporated

-

Waters Corporation

-

SCIEX (Danaher Corporation)

-

Agilent Technologies Inc.

-

Masimo Corporation

-

Baebies Inc.

-

Covidien PLC (Medtronic)

-

Chromsystems Instruments & Chemicals GmbH

-

Sebia SA

-

Recipe Chemicals & Instruments GmbH

-

Abionic SA

-

Metascreen Srl

-

PerkinElmer Genetics Inc.

-

Trivitron Healthcare Pvt. Ltd.

-

OZ Systems Inc.

-

Harmony Biosciences Holdings Inc.

-

Natera Inc.

-

Guardant Health Inc.

Newborn Screening Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.02 Billion |

| Market Size by 2035 | USD 2.14 Billion |

| CAGR | CAGR of 7.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Tandem Mass Spectrometry, Immunoassays & Enzymatic Assays, Hearing Screening Technology, DNA Assays & Next-Generation Sequencing, Pulse Oximetry, Others) • By Test Type (Dry Blood Spot Test, Hearing Screening Test, Critical Congenital Heart Disease Test) • By Disorder Type (Metabolic Disorders, Endocrine Disorders, Haemoglobin Disorders, Immune Deficiency Disorders, Others) • By End User (Hospitals, Maternity & Specialty Clinics, Diagnostic Centres) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | PerkinElmer Inc., Bio-Rad Laboratories Inc., Natus Medical Incorporated, Waters Corporation, SCIEX (Danaher Corporation), Agilent Technologies Inc., Masimo Corporation, Baebies Inc., Covidien PLC (Medtronic), Chromsystems Instruments & Chemicals GmbH, Sebia SA, Recipe Chemicals & Instruments GmbH, Abionic SA, Metascreen Srl, PerkinElmer Genetics Inc., Trivitron Healthcare Pvt. Ltd., OZ Systems Inc., Harmony Biosciences Holdings Inc., Natera Inc., and Guardant Health Inc. |

Frequently Asked Questions

The Newborn Screening Market is expected to grow at a CAGR of 7.68% from 2026 to 2035.

The Newborn Screening Market was valued at USD 1.02 Billion in 2025.

Expanding government-mandated screening panels, technological advances in tandem mass spectrometry and NGS enabling broader multi-disorder detection, and rising parental awareness of preventable genetic disorders are the primary growth factors.

Tandem Mass Spectrometry dominated the Newborn Screening Market with approximately 42.3% share in 2025.

North America dominated the Newborn Screening Market in 2025, with the United States accounting for approximately 82.6% of North American revenues through its comprehensive mandatory RUSP screening programme.

Get in Touch