Infant Incubator Market Overview and Scope

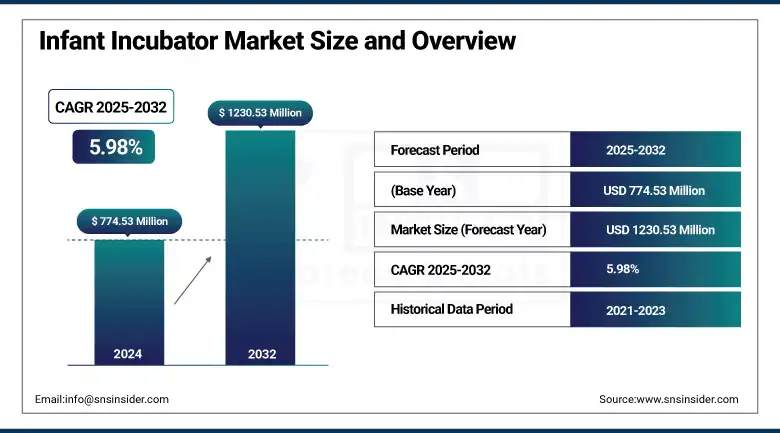

The Infant Incubator Market size was valued at USD 774.53 million in 2024 and is expected to reach USD 1230.53 million by 2032, growing at a CAGR of 5.98% over 2025-2032.

The global infant incubator market is moving on a sound momentum due to rising neonatal mortality, premature prevalence, and innovation in neonatal care technologies. According to the WHO, around 2.3 million newborns died in 2022, frequently due to preventable causes. With a recorded 15 million premature births every year, the requirement for reliable thermal regulation and respiration assistance has snowballed, furthering infant incubator industry expansion.

To Get more information On Infant Incubator Market - Request Free Sample Report

Investment in the U.S. infant incubator market (organizations, such as the FDA are speeding up incubator approvals e.g. the 2024 FDA conclusion that more recently manufactured incubators are now safe to prevent airborne chemical exposure) With a rise in R&D spending such as research projects funded by NIH covering the sensor-based and IoT-based incubators, will better product innovation. Technological and regulatory convergence into AI, IoT, and remote monitoring is becoming a driver for the market expansion of the infant incubator globally. Meanwhile, the CDC has also reported that the black infant mortality rate is 2.4x the rate for white infants, leading to an increase in healthcare equity-related investments. Hospitals mimicking neonatal ICU mannequins are also driving the global infant incubator market demand. Companies are working to close the supply gap created by manufacturing discontinuances and look to scale toward sustainable options such as hybrid or modular incubators.

By 2024, the FDA had once again cleared safety in newly manufactured neonatal incubators, debunking previous fears, and this has rekindled the production and innovation of the infant incubator companies. The emerging trends in the infant incubator market trends that are currently becoming more apparent shows AI is being used for predictive infant health modeling and better compliance with the U.S. and EU regulations.

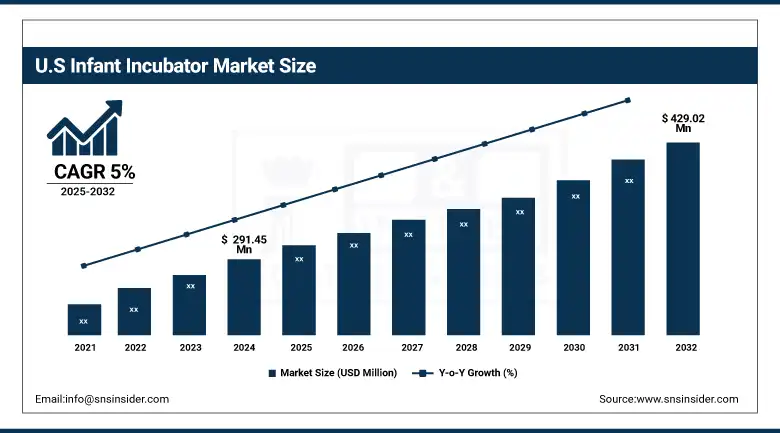

The U.S. infant incubator market size was valued at USD 291.45 million in 2024 and is expected to reach USD 429.02 million by 2032, growing at a compound annual growth rate (CAGR) of 5% over 2025-2032. The U.S. dominates the field in the region with advanced NICU infrastructure, increasing preterm birth rates (about 1 in 10 (CDC) babies are born too early in the U.S.), and continued investment in neonatal R&D.

Infant Incubator Market Dynamics

Drivers:

-

Technological Advancement and Increasing Neonatal Care Demand Are Propelling the Infant Incubator Market Forward

The increasing prevalence of low birth weight and related neonate problems is driving the infant incubator market globally. With about 1 in 10 babies being born preterm globally (WHO), there is a huge demand for neonatal care infrastructure. New generation incubators with built-in phototherapy, automatic oxygen regulation, and remote monitoring are being bought by hospitals and clinics on a large scale. For instance, Philips and GE Healthcare are both launching new neonatal product suites and data-driven incubators with AI and real-time analytics. In addition, the increasing number of neonatal intensive care units (NICUs) due to modernization of the healthcare sector has increased demand.

Based on data published by the NIH, the R&D spend on neonatal devices grew by 15% YoY in 2023, signaling the momentum in product innovation. Furthermore, increasingly rigorous safety requirements in the clearance of newer technologies (510(k)) by the FDA demonstrate a growing regulatory support. The rise of public-private partnerships and nonprofit funding dedicated to maternal and neonatal care, such as those at the Gates Foundation, accelerates innovation and accounts for adoption. The infant incubator market analysis points out that this trend is expected to continue, as global health organizations continue to converge on reducing neonatal fatalities with the aid of cutting-edge clinical technologies. The emerging need for portable and energy-efficient incubators for use in rural or emergency settings is also contributing to the infant incubator market growth.

Restraints:

-

Cost Barriers, Device Maintenance Issues, And Limited Access in Underdeveloped Regions Hamper the Market's Progress

A typical neonatal incubator has a price range of USD 10,000 to USD 30,000; having this quantity of incubators for distribution to rural clinics is not frugal for the budget. It is also arduous for non-specialized hospitals due to the complexity of operation and the requirement of a professional operator. A 2023 CDC investigation discovered that almost 40% of the U.S.-based rural healthcare providers experienced challenges trying to repair or replace out-of-date neonatal equipment due to supply chain shortages and delayed servicing. Red tape further obstructs the penetration rate, and achieving ISO 13485 and FDA QSR compliance usually necessitates a lot of testing and certification, which means time-to-market is delayed. Besides, there are an ample number of recalls, such as the ones that are recorded in the FDA MAUDE database, which raises fear among the purchasing officers.

Moreover, little R&D investment takes place in developing countries, which also amplifies the technology divide. Whereas in developed countries, innovation is driven due to computers are outdated or provided by donors with barely functional hand-me-downs. It never catches on to any significant extent, however, due to both the difficulty of interoperability between the system and the kinds of systems already installed in the hospital IT system, and the trouble and cost of deploying power in an unstable-grid-based setting. These restraining factors cumulatively moderate what is an otherwise upsurge profile of the global infant incubator market, even though there are favorable infant incubator market trends globally.

Infant Incubator Market Segmentation Analysis:

By Product

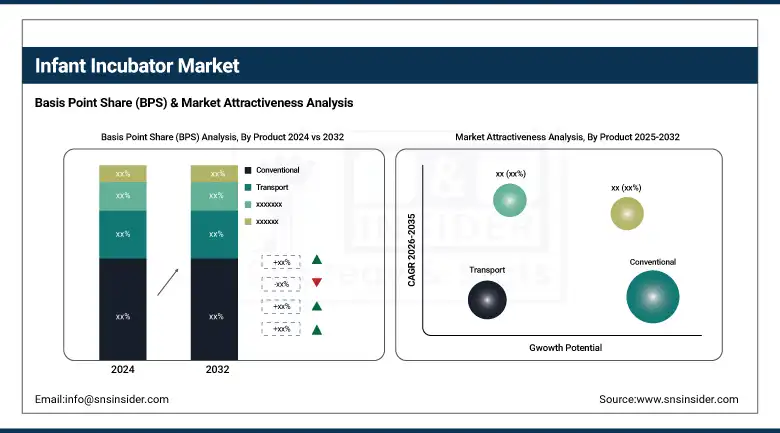

In 2024, the conventional infant incubator segment was the largest segment with a 48.2% share of the global infant incubator market. These incubators are still the mainstay around the neonatal wards due to their ruggedness, low cost, and universal availability, especially in public hospitals and in developing countries where new technology finds acceptance slowly. These designs are simple and well-tested in the clinic, which has led to their continued use globally.

The hybrid sub-segment, which is a combination of open system and closed system, is expected to be the one with the highest CAGR over 2025-2032, owing to the increasing need for flexible and multi-functionality incubators to provide both thermal regulation and minimize the risk of infection. The capability to provide integrated monitoring and phototherapy has rendered them appealing in high-acuity NICUs and tertiary-care environments.

By Type

The open incubator segment dominated the market in 2024, accounting for about 42.7% of the global market share. These modules enable easy access for caregivers and are frequently used in situations where neonates are being handled continuously, for instance, in the case of premature infants. They are particularly useful in high-birth-rate, resource-poor settings with high rates of acute intervention.

On the contrary, closed incubators are expected to witness the fastest growth on account of rising focus on infection control and superior thermal insulation. The use of such a device is increasing in the contemporary NICUs as the reduction of environmental exposure is a clinical challenge.

By End-user

In 2024, the hospital segment held the largest share of the infant incubators market as they are early adopting centers for both birthing and neonatal intensive care, leading to increased penetration of advanced incubator systems. There is also a well-developed NICU infrastructure, a skilled healthcare workforce, and financial resources, which add to their dominance.

Specialty clinics are projected to see the fastest growth, due to the increased development of standalone neonatal care units and of maternal health clinics that specialize in patient-specific care. This increase is underlined by a rise in technological facilities and investments in pediatric infrastructure in urban and semi-urban areas.

Infant Incubator Market Regional Insights

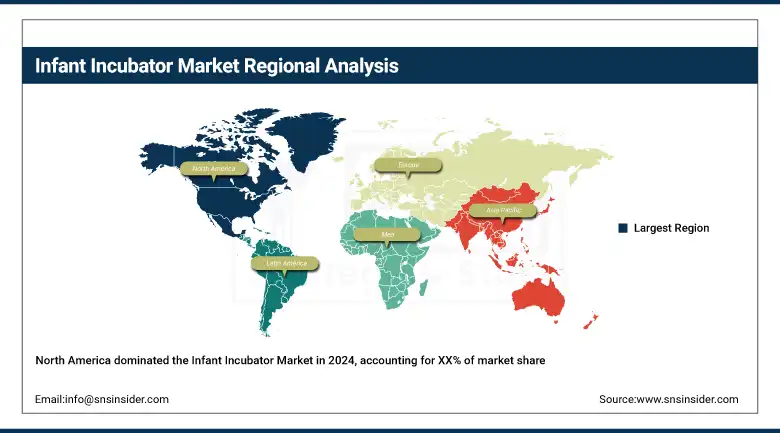

North America held a major infant incubator market share in 2024 owing to well-established healthcare facilities, superior neonatal care quality, and favorable government support.

Get Customized Report as per Your Business Requirement - Enquiry Now

In addition, the FDA approvals and innovations by major manufacturers of infant incubators, such as GE HealthCare and Philips, have been increasing the activities of the market. Even in Canada, there's consistent demand, with government subsidies for public healthcare expanding and policies that encourage maternal-child health. The government hospitals' infrastructure is slowly developing, and imports of medical devices help. North America dominates the infant incubator market with high per capita healthcare expenditure and technology penetration.

Europe is the second-largest infant incubator market in terms of growth rate, with the increasing maternal child birth age and higher NICU admissions in EU countries. Germany is spearheading the region with their excellent neonatal care and technology early adoption. Public-healthcare spending and partnerships with world companies (Drägerwerk AG) support uptake. The U.K. and France observe significant investments in neonatal infrastructure (the U.K.’s NHS supports specialized neonatal units). Countries in Eastern Europe, including Poland and Turkey, are expanding through foreign assistance and healthcare modernization efforts. One of the reasons for the growth of the infant incubator market is that the common regulation structure of the European Union under MDR will support innovation while maintaining patient safety.

The Asia Pacific is growing at the highest CAGR in the infant incubator market research, driven by an increasing number of live births, better healthcare infrastructure, and government-supported programs for the care of newborn babies. China has the largest amount of investment in maternal and child health in the region and second second-highest number of births (~9.56 million in 2022). Government support for rural healthcare expansion and local manufacturing in China further contributes to accessibility.

India is next in line, but both public and private hospitals are involved, and the response can be quite robust due to the large neonatal mortality and preterm births. National initiatives such as the India Newborn Action Plan (INAP) further long-term investment in neonatal technologies. Demand is sustained in Japan and South Korea by high-tech healthcare environments and ageing parental demographics. Growth is further facilitated by local production and the growing number of infant incubator companies in the area.

Key Infant Incubator Market Players

Major infant incubator companies in the market include Atom Medical Corp., Bistos Co., Ltd., Drägerwerk AG & Co. KGaA, GE HealthCare, Fanem, Koninklijke Philips N.V., MEDICOR Zrt., SS TECHNOMED (P) LTD., NOVOS, Natus Medical Incorporated, and AVI Healthcare Pvt. Ltd.

Recent Developments in the Infant Incubator Industry

In April 2024, GE HealthCare announced a major update to its neonatal incubators by reducing formaldehyde emissions to below detectable levels, enhancing safety and air quality for infants in clinical settings.

In June 2023, Samsung Medison, a subsidiary of Samsung Electronics, announced plans to acquire a 100% stake in Korea’s largest infant incubator manufacturer, MEDICOR, marking a strategic move to strengthen its position in the infant incubator market and expand its footprint in the neonatal care segment.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 774.53 million |

| Market Size by 2032 | USD 1230.53 million |

| CAGR | CAGR of 5.98% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Hybrid, Conventional, and Transport) • By Type (Open, Closed) • By End-user (Hospitals, Specialty Clinics, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Atom Medical Corp., Bistos Co., Ltd., Drägerwerk AG & Co. KGaA, GE HealthCare, Fanem, Koninklijke Philips N.V., MEDICOR Zrt., SS TECHNOMED (P) LTD., NOVOS, Natus Medical Incorporated, and AVI Healthcare Pvt. Ltd. |

Frequently Asked Questions

Ans: North America dominated the infant incubator market.

Ans: Cost barriers, device maintenance issues, and limited access in underdeveloped regions hamper the market's progress.

Ans: The increasing prevalence of low birth weight and related neonate problems is driving the infant incubator market globally.

Ans: The market is expected to reach USD 1230.53 million by 2032, increasing from USD 774.53 million in 2024.

Ans: The Infant Incubator market is anticipated to grow at a CAGR of 5.98% from 2025 to 2032.

Get in Touch