Healthcare Technology Management Market Report Scope & Overview:

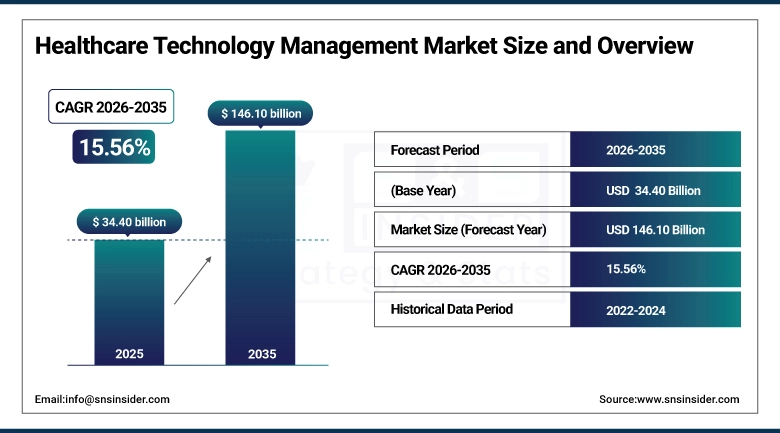

The Healthcare Technology Management Market size was valued at USD 34.40 Billion in 2025 and is projected to reach USD 146.10 Billion by 2035, growing at a CAGR of 15.56% during 2026–2035.

High adoption of advanced medical devices and digital health solutions for remote monitoring along with their maintenance is the key factor driving the growth of healthcare technology management market. The rising number of healthcare spend, increase in geriatric population, and the need for providing high-quality patient care are driving hospitals and clinics to invest in technology lifecycle management. Furthermore, market growth is further fueled by regulatory compliance, increasing demand for predictive maintenance, and AI-driven asset monitoring. The introduction of IoT, telemedicine, data analytics, etc. is changing the trajectory of demand for healthcare technology management solutions in the sector.

Healthcare Technology Management Market Size and Forecast:

-

Market Size in 2025: USD 34.40 Billion

-

Market Size by 2035: USD 146.10 Billion

-

CAGR: 15.56% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Healthcare Technology Management Market - Request Free Sample Report

Healthcare Technology Management Market Key Trends:

-

The increasing adoption of advanced healthcare technologies is driving hospitals and clinics to upgrade their equipment management and maintenance practices.

-

Digital health platforms and IoT-enabled medical devices are transforming patient monitoring, data collection, and remote care delivery.

-

Collaborations between healthcare providers, technology vendors, and service companies are enhancing operational efficiency and patient outcomes.

-

Growing emphasis on compliance and regulatory standards is stimulating the integration of advanced tracking, reporting, and safety systems.

-

The rising demand for predictive maintenance and asset lifecycle management is creating opportunities for AI-powered healthcare technology solutions.

-

AI and analytics-driven decision support systems are revolutionizing equipment utilization, reducing downtime, and improving clinical efficiency.

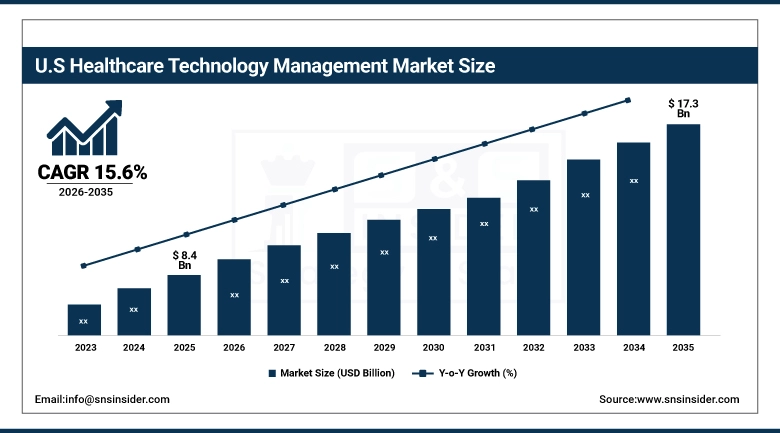

In the United States, the Healthcare Technology Management Market was valued at around USD 8.4 billion in 2025 and is projected to reach approximately USD 17.3 billion by 2035, growing at a CAGR of about 15.6 % over the forecast period 2026-2035. The U.S. Healthcare Technology Management Market is growing due to increasing adoption of advanced medical devices, rising demand for efficient equipment maintenance, regulatory compliance requirements, aging populations, and the integration of AI, IoT, and digital health solutions in hospitals and clinics.

Healthcare Technology Management Market Key Drivers:

-

Rising adoption of advanced medical devices and digital health solutions is boosting demand for efficient equipment management.

Some of the major driving factors for Healthcare Technology Management Market are rising adoption of complex medical units, increasing healthcare expenditure, and propelling demand for high quality clinical services. Hospitals and clinics are investing in asset lifecycle management, predictive maintenance, and AI-driven monitoring solutions. The improved operational efficiency coupled with reduced downtime and better patient outcomes invariably contribute to market growth, which is also driven by IoT and telemedicine integrations as well as analytics.

Healthcare Technology Management Market Key Restraints:

-

High implementation costs, lack of skilled personnel, and complex regulatory requirements are limiting market growth.

Healthcare Technology Management Market is currently hindered by high operational costs of advanced healthcare technology management systems, lack of trained professionals, and stringent compliance requirements. Investment in advanced systems may come difficult for smaller hospitals and clinics, and added operational challenges are posed by the complex healthcare regulations. Inconsistency of growth in the market is also limited due to regionalise in technology adoption for institutions which tend to slow down the uptake and also increasing difficulty of implementation.

Healthcare Technology Management Market Key Opportunities:

-

Integration of AI, IoT, and predictive maintenance solutions is creating new avenues for market expansion.

The increasing adoption of artificial intelligence (AI)-driven analytics, internet of things (IoT)-enabled devices, and predictive maintenance is expected to create lucrative growth opportunities for the Healthcare Technology Management Market in the hospitals segment. Remote monitoring, digital health platforms, and cloud-based management solutions result in optimizations, and reduces the cost through minimizing asset idle time. These trends set to accelerate will further benefit providers that are able to deploy data-driven technology management services and increased training and support on behalf of their IT clients.

Healthcare Technology Management Market Segments:

-

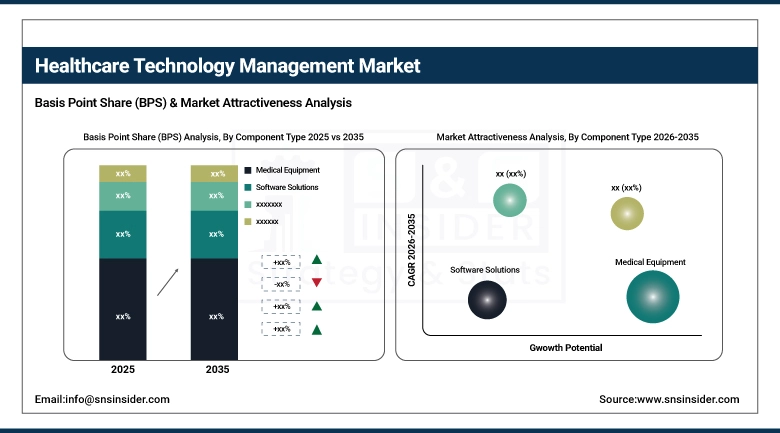

By Component Type: In 2025, Medical Equipment dominated with 50% share; Software Solutions fastest growing segment during 2026–2035

-

By Technology: In 2025, IoT-enabled Devices dominated with 48% share; AI & Predictive Analytics fastest growing segment during 2026–2035

-

By Application: In 2025, Equipment Monitoring & Maintenance dominated with 45% share; Asset Lifecycle Management fastest growing segment during 2026–2035

-

By End User: In 2025, Hospitals & Clinics dominated with 53% share; Ambulatory Care & Surgery Centers fastest growing segment during 2026–2035

Healthcare Technology Management Market Segment Analysis:

By Component Type, Medical Equipment Dominates While Software Solutions Expands Rapidly:

Due to the continuous requirement of maintaining and monitoring high-value devices, the Medical Equipment segment dominated the market as hospitals and clinics spend more capital on high-value devices. Demand remains steady owing to advanced diagnostic and therapeutic devices. Over 45 thousands units of different medical equipment installations took place in the year 2025.

Software Solutions are the fastest growing segment, powered by AI-based analytics, cloud-based management, and predictive maintenance tools. How operational efficiency, regulatory compliance and cost saving increases the value of it. The software deployment hit 12,000 installations in 2025.

By Technology, IoT-enabled Devices Dominate While AI & Predictive Analytics Expands Rapidly:

Real-time monitoring of medical equipment powered by IoT-enabled Devices minimizes downtime, and promotes patient care prompting higher share for IoT-enabled Devices market. Hospitals want quicker, faster services for efficiency, and consideration for devices need to be taken care of even at the time of purchase (connected devices are preferred for preventive maintenance and support). 48% of deployments were IoT-enabled devices in 2025.

AI & Predictive Analytics is the fastest growing subsegment, mainly driven by the need for predictive maintenance, data-driven insights, and optimizing operations. These technologies are increasingly being adopted by hospitals for more strategic decision making. The number of AI & predictive analytic tools installations hit 15,000 in 2025.

By Application, Equipment Monitoring & Maintenance Dominates While Asset Lifecycle Management Expands Rapidly:

As healthcare organizations, seeks to reduce the downtime of devices, as well as maximize device utilization, the Equipment Monitoring & Maintenance held the largest market share in 2019. Ongoing monitoring guarantees both safety for the patient and efficiency in operations. Within the year 2025, monitoring companies have been about 50,000 bits of equipment.

The best growth segment is Asset Lifecycle Management which is driven by hospitals in order to optimize costs and achieve device life extension and central management. The integration of AI and web-enabled tools will augment the planning and reporting process. Managed 18,000 devices using lifecycle management solutions in 2025.

By End User, Hospitals & Clinics Dominate While Ambulatory Care Expands Rapidly:

Due to the large installed base of medical equipment and the need for comprehensive technology management, the Hospitals & Clinics segment dominated the market Patients are on the high-volume side, and this drives ongoing adoption. In 2025, hospitals made up 60% of market share.

The fastest-growing segment, Ambulatory Care & Surgery Centers, is fueled by small facilities expressing a need for efficiency and cost savings in managing their medical devices with the utilization of cloud solutions. Until 2025, at roughly 8,000 devices throughout ambulatory care facilities had solutions implemented.

Healthcare Technology Management Market Regional Analysis:

North America Healthcare Technology Management Market Insights:

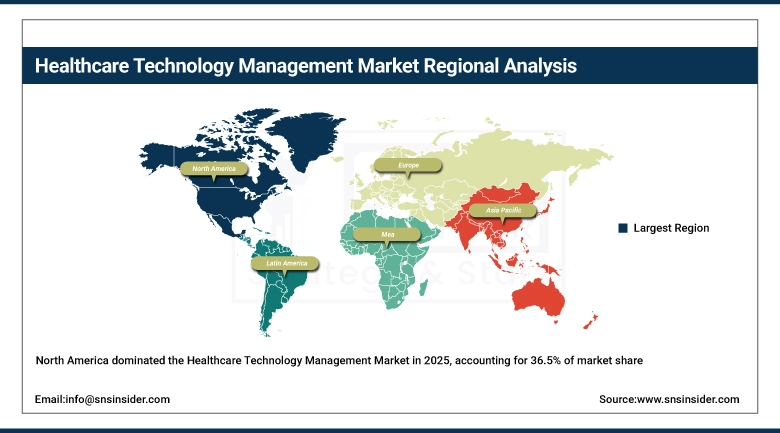

North America held the highest share in the Healthcare Technology Management Market in 2025, at 36.5%, due to large healthcare spending, rapid adoption of advanced medical devices and large hospital infrastructure. AI equipment management, predictive maintenance and cloud-based health care solutions operational efficiency and patient care quality are on the frontline for the United States and Canada. A large share of the North America market is attributed to strong government support, favorable regulations, and growing digital health initiatives in the region.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Healthcare Technology Management Market Insights:

The fastest-growing is the Asia-Pacific market with an expected impressive CAGR of 16.2% for the period of 2026–2035. It is fueled by growing healthcare infrastructure expenditure in emerging economies such as China, India, Japan, and South Korea, increasing medical tourism, and increasing adoption of IoT enabled devices and AI-based healthcare management solutions. Factors such as increasing middle-class population, increasing awareness regarding cost effective healthcare services and rising access to digital health platforms are rapid-driving the growth of the market.

Europe Healthcare Technology Management Market Insights:

High adoption of advanced medical device bloodstream infection control technology, as well as a small number of well-regulated healthcare system markets and high focus on compliance, compliance, and patient safety, drives Europe. Germany, the UK, and France are examples of countries investing in AI enabled monitoring, predictive maintenance coupled with cloud-based management tools. Through established hospital infrastructure in addition to government-generated digital health programs, operational efficiency improves, and this, in turn, will be reflected in Europe, where the sustained growth of healthcare technology management is shackled to time and age.

Latin America Healthcare Technology Management Market Insights:

Growing Latin American countries with rising price range investments in healthcare, modernization of the medical institution infrastructure, and an upsurge in want for proactive equipment management. Key Takeaways: Brazil, Mexico, and Argentina represent major markets characterised by growing telehealth initiatives from the private sector, adoption of various AI-enabled solutions, and increased adoption in private hospitals. Programs focused on e-health and technology at the regional level add to the penetration of the market and the adoption of technology.

Middle East & Africa (MEA) Healthcare Technology Management Market Insights:

Factors driving growth in the MEA market include increasing healthcare infrastructure expenditure, government efforts aimed at modernizing hospitals, and adoption of digital solutions to manage health conditions. Within these, key markets were identified such as the UAE, Saudi Arabia, and South Africa. The key factors that are driving the growth of predictive maintenance market are increasing patient demand, rising medical tourism, and a surge in the integration of predictive maintenance and IoT-enabled devices. Further the rapid expansion of private sector is further steering the adoption of predictive maintenance technology.

Healthcare Technology Management Market Competitive Landscape:

Siemens Healthineers AG is a global leader in medical technology, imaging systems, diagnostics, and therapeutic solutions that enable healthcare providers to deliver high‑quality patient care. Its portfolio spans from advanced CT, MRI, X‑ray, ultrasound, and laboratory diagnostics to software solutions that assist boost operational efficiency, powered by data and AI. Siemens Powers Up Precision Medicine, Digital Health Solutions, Device Management, Stacking Up Its Powerhouse Position Throughout Health Systems Worldwide.

-

In 2025, Siemens Healthineers launched new AI‑enhanced diagnostic imaging solutions that further integrate predictive analytics for equipment performance and patient workflow optimization, reinforcing its healthcare technology management leadership.

Based in the United States, GE HealthCare is a global leader in medical technology and digital solutions, with a focus on imaging, monitoring, biomanufacturing, and cell and gene therapy technologies, as well as integrated radiology and enterprise imaging. For over 125 years, GE HealthCare has been the ongoing pursuit of the kind of products and services that improve clinical decision‑making, drive operational improvement in the hospital, and enable personalized care delivery. It sells imaging systems, advanced visualization tools, software platforms, and turnkey equipment service programs.

-

In 2025, GE HealthCare expanded its HTM services with multivendor maintenance and analytics platforms that optimize asset utilization and cost‑effective lifecycle management for healthcare providers worldwide.

Healthcare Technology Management Market Key Players:

-

Siemens Healthineers AG

-

GE HealthCare

-

Koninklijke Philips N.V.

-

TriMedx

-

Sodexo S.A.

-

Nuvolo (Trane Technologies)

-

Phoenix Data Systems

-

FSI LLC

-

Brightly Software, Inc.

-

Maintainly

-

Eptura

-

IBM

-

Oracle

-

ServiceNow

-

Zebra Technologies Corp

-

Sonitor Technologies

-

Accruent

-

Securitas Healthcare LLC

-

TeleTracking Technologies

-

Crothall Healthcare

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 34.40 Billion |

| Market Size by 2035 | USD 146.10 Billion |

| CAGR | CAGR of 15.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component Type: (Medical Equipment, Software Solutions, Maintenance Services) • By Technology: (IoT-enabled Devices, AI & Predictive Analytics, Cloud-based Management Systems) • By Application: (Asset Lifecycle Management, Equipment Monitoring & Maintenance, Regulatory Compliance & Reporting) • By End User: (Hospitals & Clinics, Diagnostic Centers, Ambulatory Care & Surgery Centers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Siemens Healthineers AG, GE HealthCare, Koninklijke Philips N.V., TriMedx, Sodexo S.A., Nuvolo (Trane Technologies), Phoenix Data Systems, FSI LLC, Brightly Software, Inc., Maintainly, Eptura, IBM, Oracle, ServiceNow, Zebra Technologies Corp, Sonitor Technologies, Accruent, Securitas Healthcare LLC, TeleTracking Technologies, Crothall Healthcare |

Frequently Asked Questions

Ans: The Healthcare Technology Management Market is expected to grow at a CAGR of 15.56 % during 2026–2035.

Ans: The market was valued at USD 1.94 Billion in 2025 and is projected to reach USD 4.15 Billion by 2035.

Ans: The key drivers of the Healthcare Technology Management Market are rising adoption of advanced medical devices, increasing healthcare expenditure, regulatory compliance, and AI/IoT integration.

Ans: Medical Equipment (Hardware) segment dominated during the projected period.

Ans: North America dominated the Healthcare Technology Management Market in 2025.

Get in Touch