Bevacizumab Biosimilars Market Report Scope & Overview:

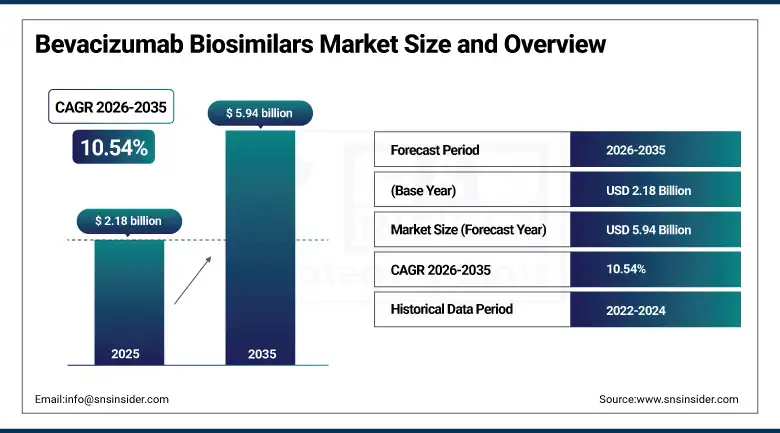

The bevacizumab biosimilars market was valued at USD 2.18 billion in 2025 and is expected to reach USD 5.94 billion by 2035, growing at a CAGR of 10.54% from 2026–2035.

The market of bevacizumab biosimilars has seen steady growth in recent times, owing to the rising number of incidences of cancer patients all around the world, the expiry of patents of reference biologic Avastin (bevacizumab, Roche/Genentech) and a growing need for affordable cancer drugs in payer and health care systems. Bevacizumab, a recombinant humanized monoclonal antibody against vascular endothelial growth factor A (VEGF-A) has become an integral part of the therapy for patients of metastatic colorectal cancer, non-small cell lung cancer, glioblastoma, renal cell carcinoma, cervical cancer, and ovarian cancer from 2004 when it was approved by the FDA. Thanks to the availability of biosimilars having comparable analytical, functional, clinical, and immunogenic properties to the reference drug, the prices of the drugs have drastically reduced.

Regulatory frameworks established by the U.S. Food and Drug Administration (FDA) under the Biologics Price Competition and Innovation Act (BPCIA), the European Medicines Agency (EMA) through its well-established biosimilar approval pathway, and analogous guidelines from regulatory bodies in Japan, South Korea, Australia, Canada, and India have collectively created an enabling global environment for the commercialization of bevacizumab biosimilars. Policy interventions including mandated biosimilar substitution policies in several European nations, Medicaid and Medicare incentives in the United States for biosimilar prescribing, and national formulary inclusions in emerging markets are collectively accelerating the uptake of bevacizumab biosimilars across oncology treatment settings globally.

Market Size and Forecast

-

Market Size in 2026E: USD 2.42 Billion

-

Market Size by 2035: USD 5.94 Billion

-

CAGR: 10.54% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Bevacizumab Biosimilars Market - Request Free Sample Report

Bevacizumab Biosimilars Market Trends

-

The growing approvals for regulatory processes in the US, EU, Japan, and emerging markets will create a larger competitive environment for the industry, along with improved affordability of anti-VEGF drugs for cancer patients.

-

The formulary adoption at hospitals along with the mandated biosimilar substitution in countries such as Germany, France, Norway, and Denmark is leading to increased market penetration by bevacizumab biosimilars.

-

Growing oncology pipeline activity from emerging market biopharmaceutical manufacturers in India, China, and South Korea is intensifying market competition and enabling further price reductions for bevacizumab biosimilars globally.

-

The wider application of biosimilars of bevacizumab to ophthalmology in terms of wet AMD and DME is now providing additional sources of income apart from the approved indications in oncology.

-

The strategic alliance between large-scale pharmaceutical companies and regional distributors has increased the availability of bevacizumab biosimilars in cancer care markets that are underserved in South and Southeast Asia, Latin America, and Africa.

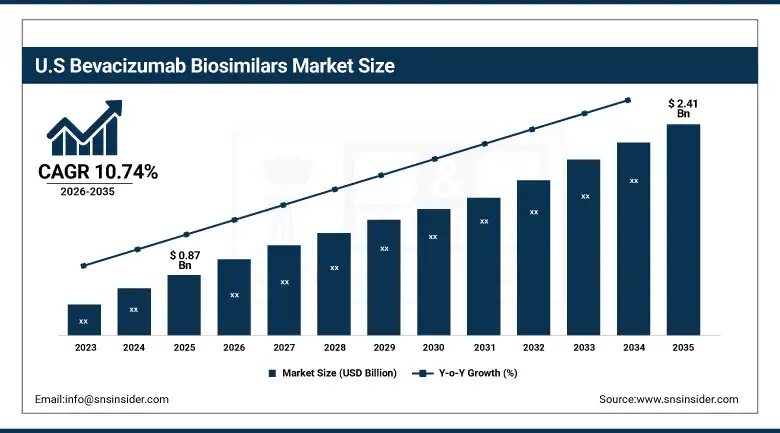

The U.S. Bevacizumab Biosimilars Market Size Outlook

The U.S. bevacizumab biosimilars market was valued at USD 0.87 billion in 2025 and is expected to reach around USD 2.41 billion by 2035, growing at a CAGR of 10.74% from 2026–2035.

The United States represents the single largest national market for bevacizumab biosimilars globally, driven by one of the world's highest cancer incidence burdens, a well-developed oncology care infrastructure, and increasing adoption of biosimilar biologics supported by CMS reimbursement policies and private payer formulary incentives. As a result of the effective pathway developed by the FDA for the evaluation of interchangeable biosimilars through the BPCIA, an increasing number of biosimilars of bevacizumab have received market approval, including Mvasi (Amgen) and Zirabev (Pfizer). The biosimilar pricing incentives created by the Centers for Medicare & Medicaid Services (CMS) and the reimbursement policy for part B drugs have played a significant role in the adoption of these biosimilars in hospital and practice settings that provide treatments for Medicare beneficiaries with cancer.

Amgen Inc. continued to increase their presence in the United States by boosting the commercial reach of Mvasi (bevacizumab-awwb), which included expanding their oncology biosimilar line-up by securing greater contractual arrangements with the top pharmacy benefit managers, integrated delivery networks, and GPOs, thereby enhancing the adoption rate of Mvasi in hospitals and outpatient oncology infusion centers across the country.

Bevacizumab Biosimilars Market Segmentation Analysis

-

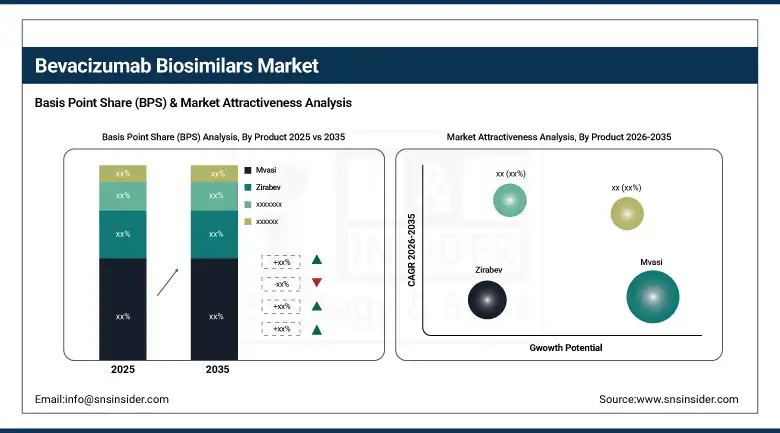

By Product, the Mvasi segment dominated the bevacizumab biosimilars market with 28.46% share in 2025, while Zirabev is the fastest growing product segment.

-

By Application, the colorectal cancer segment dominated the bevacizumab biosimilars market with 37.85% share in 2025, while the cervical cancer segment is the fastest growing application.

-

By Distribution Channel, the hospital pharmacies segment dominated the bevacizumab biosimilars market with 63.74% share in 2025, while online pharmacies are the fastest growing distribution channel.

-

By End User, the hospitals & oncology clinics segment dominated the bevacizumab biosimilars market with 57.62% share in 2025, while specialty care centers are the fastest growing end user segment.

By Product, the Mvasi segment dominates the bevacizumab biosimilars market, while Zirabev is the fastest-growing segment.

The biosimilar bevacizumab drug Mvasi (bevacizumab-awwb), manufactured by Amgen and partnered with Allergan, had the highest market share of bevacizumab biosimilar drugs in the year 2025, having a 28.46% share of global revenue in its product segment. Given that Mvasi was the first biosimilar to receive approval from the FDA for the treatment of cancer diseases back in 2017, the product has seen great success due to the first mover advantage and robust commercial contracting networks coupled with broad insurance coverage in key U.S. and Europe countries. In addition, effective clinical package studies, HTA application processes, and patient assistance programs have all contributed to Mvasi's strong market position.

It is anticipated that Zirabev (bevacizumab-bvzr), marketed by Pfizer, will register the most substantial CAGR among bevacizumab biosimilar brands during the projected period of 2026-2035 owing to aggressive marketing by Pfizer worldwide, competitive pricing, and contractual capabilities within hospital and oncology centers. Regulatory approval for Zirabev has been obtained in the United States, EU countries, Canada, and a number of emerging economies, increasing its market footprint. The robust connections enjoyed by Pfizer with hospitals and oncology centers, along with effective product lifecycle management and biosimilars market development, are anticipated to contribute to the market share gains of Zirabev in the coming years.

By Application, the colorectal cancer segment dominates the bevacizumab biosimilars market, while the cervical cancer segment is the fastest-growing.

The colorectal cancer application sector was the largest revenue holder in the bevacizumab biosimilar market at 37.85% in 2025, considering that bevacizumab biosimilar has long been the first-line drug approved in combination with standard chemotherapy for metastatic colorectal cancer (mCRC). Bevacizumab has been used to manage mCRC over the last couple of decades, and its availability in biosimilar formulations has contributed greatly towards improving treatment affordability amidst rising costs within healthcare organizations. Given the prevalence rate of colorectal cancer across the world and considering that bevacizumab has clinical evidence that has been accepted by oncological societies such as ESMO and NCCN, there is consistent and strong institutional demand for bevacizumab biosimilars in this therapeutic area.

The cervical cancer application segment is projected to register the highest CAGR among all bevacizumab biosimilar applications during 2026–2035, driven by the increasing adoption of bevacizumab in combination with chemotherapy for persistent, recurrent, or metastatic cervical cancer following the landmark GOG 240 trial findings. Rising cervical cancer incidence in low- and middle-income countries, combined with growing healthcare infrastructure investments, expanding oncology specialist workforces, and biosimilar affordability advantages, are catalyzing the use of bevacizumab biosimilars in this indication across emerging healthcare markets in Asia, Africa, and Latin America. Increasing screening program investments and earlier-stage detection patterns globally are expected to sustain a growing patient pool eligible for bevacizumab-based treatment protocols.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.34% |

|

Europe |

Germany |

31.28% |

|

Asia Pacific |

China |

35.74% |

|

Middle East & Africa |

UAE |

15.82% |

|

Latin America |

Brazil |

43.19% |

North America Bevacizumab Biosimilars Market Insights

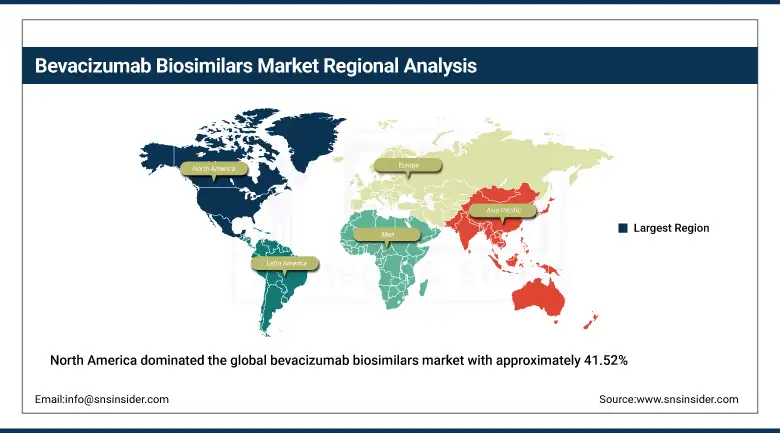

North America dominated the global bevacizumab biosimilars market with approximately 41.52% of total revenue share in 2025, led by the United States which commands the largest individual national market globally. An advanced oncology care delivery system, high incidence rate of cancer cases, reimbursement coverage of FDA approved biosimilars under Medicare Part B and other commercial insurance companies, as well as biosimilar market ecosystem that is already established in the region contribute to the North America's regional supremacy. FDA's scientific process of approval of bevacizumab biosimilars coupled with CMS guidelines for reimbursement of biosimilars and PBM strategies for promoting biosimilars are fast tracking formulary acceptance in the U.S. healthcare environment. Contributions from Canada through approval process by Health Canada and listing of biosimilars by drug benefit programs in Canada complement regional demand.

The U.S. Inflation Reduction Act’s provisions providing the opportunity to negotiate prices for Medicare prescription drugs with respect to high-cost biologics and additional incentives for biosimilars are contributing to tailwinds towards bevacizumab biosimilars use in the entire U.S. oncology landscape. The growing prevalence of hospital biosimilar switching programs and biosimilar purchasing facilitated through group purchasing organizations is driving the transition from the brand bevacizumab to biosimilars within institutional settings.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Bevacizumab Biosimilars Market Insights

Europe is a critical and commercially mature region in the global bevacizumab biosimilars market, accounting for approximately 28.94% of total revenue in 2025. In this regard, the robust biosimilar approval process employed by the EMA and scientifically based since 2006 has played a vital role in making Europe one of the first regions in the world in the penetration of the biosimilars market. Germany, France, Italy, Spain, UK, and Scandinavian countries have become the main national contributors, having introduced a policy of prescribing biosimilars, prescribing through the use of INNs, and incentives for substituting at the level of payers, which has considerably expedited the adoption of bevacizumab biosimilars in oncology applications. The European hospital tender system for pharmaceuticals, as well as health technology assessment processes within various countries, have played a crucial role here.

Pharmaceutical Strategy for Europe from the European Commission and healthcare cost containment initiatives by individual member states within the EU due to national austerity measures continue to provide significant policy-level backing towards the adoption of biosimilars. This is especially so following the enactment of compulsory tender substitution laws for biosimilars in countries such as Norway and Denmark, leading to over 85 percent market share of bevacizumab biosimilars among the total bevacizumab volume, an example which is being followed by other EU countries as well.

Asia Pacific Bevacizumab Biosimilars Market Insights

Asia Pacific is projected to be the fastest-growing regional market for bevacizumab biosimilars during 2026–2035, expanding at a CAGR of approximately 13.28% driven by the region's rapidly increasing cancer burden, growing healthcare expenditure, expanding oncology care infrastructure, and increasing regulatory approvals of bevacizumab biosimilars across China, Japan, South Korea, Australia, India, and Southeast Asian nations. China represents the largest and most rapidly growing country-level market within Asia Pacific, supported by the National Medical Products Administration (NMPA) biosimilar approval framework, the National Reimbursement Drug List (NRDL) inclusion of bevacizumab biosimilars, and the volume-based procurement (VBP) program which has driven dramatic price reductions and corresponding volume increases for biologics including bevacizumab. Japan and South Korea contribute significant regional demand, supported by mature biosimilar regulatory frameworks and high cancer treatment rates.

The VBP procurement model adopted by China has significantly transformed the dynamics of the bevacizumab market landscape by centralizing procurement tenders, which have resulted in the pricing of bevacizumab biosimilars to a tiny fraction of that charged by the originator product, leading to an equally substantial increase in patient treatment volumes among public hospital oncology departments. Chinese companies such as Henlius Biotech and Innovent Biologics have received NMPA approvals for their bevacizumab biosimilars, allowing them to capture meaningful market share not only in China but even globally.

Middle East & Africa and Latin America Bevacizumab Biosimilars Market Insights

The Middle East & Africa and the Latin America regions emerge as increasingly lucrative frontier markets for the commercialization of bevacizumab biosimilants. This growth opportunity is underpinned by an increase in the number of cancer cases, increased government spending on building cancer infrastructure, and improved awareness among health insurers regarding the cost-effectiveness offered by biosimilant biological products. In the case of the MEA region, the UAE, Saudi Arabia, South Africa, Egypt, and Turkey are leading countries that will drive the market. The vision to modernize the Saudi Arabian healthcare infrastructure, in addition to expansion plans in the UAE’s health system, are directing investments in cancer facilities, thus creating more patients for bevacizumab biosimilants.

Brazil represents the largest and most commercially developed Latin American market for bevacizumab biosimilars, supported by ANVISA's biosimilar regulatory framework and the National Cancer Institute's (INCA) oncology treatment guidelines which endorse bevacizumab-based regimens. Mexico, Argentina, and Colombia are supplementary growth markets, with national public health procurement programs increasingly including bevacizumab biosimilars on national essential medicines lists to address the affordability and access challenges associated with originator biologic pricing in resource-constrained healthcare systems across the region.

Growth Drivers: Surging global cancer incidence and the healthcare system imperative to reduce oncology biologics expenditure are accelerating the adoption of bevacizumab biosimilars.

With increasing demand from the global rise in cancer prevalence and the estimate of roughly 35 million new cases worldwide by 2050 according to the World Health Organization, there arises the most basic demand-pull factor for the introduction of bevacizumab biosimilars. Treatment protocols relying on bevacizumab are an integral component of established care guidelines used for the treatment of several common cancer types such as colorectal, lung, ovarian, and cervical cancers, and thus constitute significant system-level demand for the agent. Until now, the exorbitant price of reference bevacizumab (Avastin) has been an impediment to patient access across numerous territories, but with biosimilar versions being available at lower price levels, the expansion of bevacizumab treatment access in the context of controlled total oncology spending has become possible. The pressure on national healthcare budgets, especially in single-payer schemes like those prevalent in Europe and other emerging market economies, provides significant incentive for biosimilar prescribing.

Restraints: Complex manufacturing processes, stringent regulatory comparability requirements, and immunogenicity concerns are limiting the market penetration.

The development of bevacizumab biosimilars needs sophisticated biopharmaceutical production techniques, advanced characterization analytics, and extensive clinical data packages which are major hurdles and investments required by manufacturers not having the capability to produce such monoclonal antibodies. Regulators like the FDA, EMA, and PMDA require high standards for the approval of biosimilars through which considerable pre-clinical and clinical investments have been involved; hence, it takes time and money to develop a market-ready drug candidate. Prescribers' and patients' concerns related to safety and interchangeability in some populations within oncology may lead to reluctance to prescribe the biosimilars when they are available on the market despite inclusion in insurance company formularies. In developing countries, a lack of regulatory capacity and pharmacovigilance may cause hesitation in accepting biosimilars due to concerns about their safety.

Opportunities: Expanding into ophthalmology off-label applications and underpenetrated emerging market oncology systems presents significant growth potential for manufacturers.

With the off-label use of intravitreal bevacizumab for wet AMD, DME, and other neovascular disorders being well-documented over the years, there is a very promising commercial potential for the manufacture of biosimilars of bevacizumab in the context of its off-label applications. As far as intravitreal bevacizumab is concerned, there is an abundance of data confirming its clinical effectiveness and safety. However, due to the fact that prices on such VEGF-inhibitors used in ophthalmic practice as ranibizumab and aflibercept are quite high, the ability of biosimilar manufacturers to offer affordable and quality bevacizumab can be viewed as a profitable opportunity. The progressive expansion of oncology care access in high-growth emerging markets including India, Indonesia, Vietnam, Nigeria, and Kenya, supported by international oncology NGOs and national cancer care investment programs, is expected to generate additional long-term demand for affordable bevacizumab biosimilar products.

Recent Developments

-

2025: Biocon Biologics advanced the international commercialization of Abevmy (bevacizumab biosimilar), expanding its regulatory submissions and commercial partnerships across European, Canadian, and emerging market territories.

-

2025: Dr. Reddy's Laboratories expanded the commercial reach of Versavo (bevacizumab biosimilar) across multiple European markets following its 2024 UK launch, building distribution partnerships with regional oncology specialty distributors.

-

2024: Samsung Bioepis received EMA approval for Aybintio (bevacizumab biosimilar) and advanced its global commercialization strategy in collaboration with Biogen.

-

2024: Pfizer advanced Zirabev's global market access strategy, securing additional national formulary inclusions and hospital formulary approvals across European markets.

Bevacizumab Biosimilars Market Key Players are:

-

Mylan N.V. (Viatris Inc.)

-

Celltrion Healthcare Co., Ltd.

-

Boehringer Ingelheim GmbH

-

Biocon Biologics Ltd.

-

Dr. Reddy's Laboratories Ltd.

-

Henlius Biotech, Inc.

-

Innovent Biologics, Inc.

-

AryoGen Pharmed

-

mAbxience S.A.

-

Prestige Biopharma Ltd.

-

Zydus Lifesciences Ltd.

-

Sandoz International GmbH (Novartis)

-

Teva Pharmaceutical Industries Ltd.

-

Fujifilm Kyowa Kirin Biologics Co., Ltd.

-

EirGenix Inc.

-

Fresenius Kabi AG

-

Coherus BioSciences, Inc.

Bevacizumab Biosimilars Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.18 Billion |

| Market Size by 2035 | USD 5.94 Billion |

| CAGR | CAGR of 10.54% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Mvasi, Zirabev, Aybintio, Onbevzi, Vegzelma, Others) • By Application (Colorectal Cancer, Non-Small Cell Lung Cancer, Renal Cell Carcinoma, Glioblastoma, Cervical Cancer, Ovarian Cancer, Others) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) • By End User (Hospitals & Oncology Clinics, Specialty Care Centers, Ambulatory Surgical Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amgen Inc., Pfizer Inc., Mylan N.V. (Viatris Inc.), Samsung Bioepis Co., Ltd., Celltrion Healthcare Co., Ltd., Boehringer Ingelheim GmbH, Biocon Biologics Ltd., Dr. Reddy's Laboratories Ltd., Henlius Biotech, Inc., Innovent Biologics, Inc., AryoGen Pharmed, mAbxience S.A., Prestige Biopharma Ltd., Zydus Lifesciences Ltd., Sandoz International GmbH (Novartis), Teva Pharmaceutical Industries Ltd., Fujifilm Kyowa Kirin Biologics Co., Ltd., EirGenix Inc., Fresenius Kabi AG, Coherus BioSciences, Inc. |

Frequently Asked Questions

The major growth factor is the rising global incidence of cancer, combined with healthcare system cost-containment imperatives and patent expiration of reference bevacizumab (Avastin).

The bevacizumab biosimilars market was valued at USD 2.18 billion in 2025.

Get in Touch