Bioherbicides Market Report Scope & Overview:

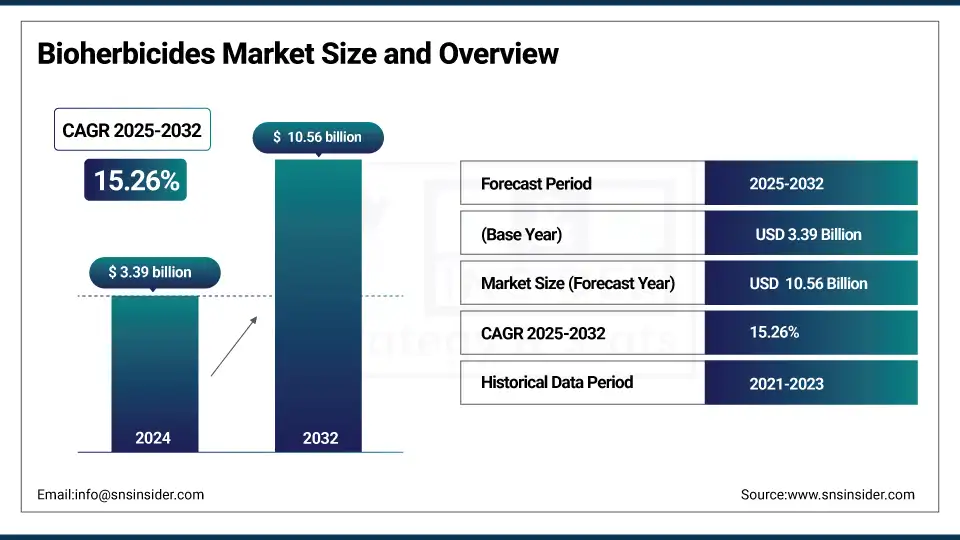

The Bioherbicides market size was valued at USD 3.39 billion in 2024 and is expected to reach USD 10.56 billion by 2032, growing at a CAGR of 15.26% over the forecast period of 2025-2032.

The growth of the bioherbicides market is attributed to rising demand for bio-chemicals in organic farming, efficient weedicide performance, and integrated weed management practices. Developments in microbial herbicides, seed treatment procedures, and foliar spray methods are driving the business growth. Supportive government policies by the U.S. EPA for biopesticides with low-risk profiles, and rising public-private partnerships between ag-tech companies and universities have been driving the bioherbicides market/fungicide market. Key companies are part of the continuous bioherbicides market trends, and they are adopting advanced solutions in order to increase their bioherbicides market share.

To Get more information On Bioherbicides Market - Request Free Sample Report

Organic cropland acres increased by 79 percent to 3.6 million acres between 2011 and 2021, the U.S.D.A. said. Marrone Bio Innovations’ trials for a bioherbicide that is microbial for glyphosate-resistant weeds in corn and soybeans were successful in February 2024, and the growth of the market for bioherbicides is strong. These new developments are highlighted as examples of how the bioherbicides industry is advancing and making sustainable weed control a reality across the globe.

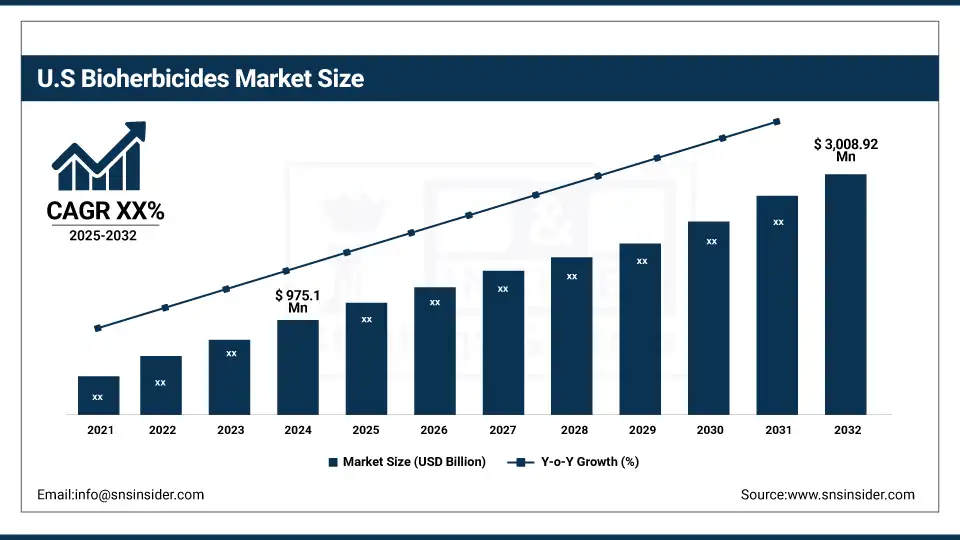

North America is led by the U.S. and has a market size of USD 975.1 million in 2024, and is anticipated to reach USD 3,008.92 million in 2032, with a market share of approximately 77%. The factors that explain the dominance are a large amount of organic farming and sturdy institutions that back that up. The EPA’s biopesticide registration program provides a simplified approach to registering microbial herbicides and fosters innovation. Marrone Bio Innovations, for instance, launched both Regalia and Stargus, which are labeled for fruits and specialty crops. Furthermore, the United States Department of Agriculture’s Organic Transition Initiative provides financial support to assist farmers in transitioning from conventional to biological inputs and has also contributed to the bioherbicide market growth in the country for various crop types.

Market Dynamics:

Drivers:

-

Expansion of organic farming practices globally accelerates demand for bioherbicides in weed control

The growing exploitation of organic farming worldwide offers an international market for bioherbicides as a substitute for chemical control of weeds. According to the International Federation of Organic Agriculture Movements (IFOAM), the current number of organic farmland has reached over 76 million hectares worldwide and is still increasing. Farmers are increasingly resorting to microbial herbicides and organic farming chemicals to ensure sustainable agricultural practices. This is in line with the recent bioherbicides market trends and increases the bioherbicides market share, particularly in cereals, fruits, and pulses, where the organic standards prohibit the use of synthetic substances.

-

Government incentives and regulatory support enhance the bioherbicides market growth worldwide

Regulatory and monetary benefits are still promoting the bioherbicides market on a worldwide basis. The European Commission’s “Farm to Fork Strategy” will see the use of chemical pesticides halved by 2030, adding a powerful policy incentive to develop natural alternatives such as microbial herbicides. There are also grants and subsidies being provided by national governments worldwide to promote innovation in and adoption of sustainable crop protection. These stimulatory actions are responsible for augmenting the bioherbicides industry and promoting companies to innovate their products.

Restraints:

-

Variability in bioherbicide performance under diverse environmental conditions limits consistent weed control

The effectiveness of bioherbicides in the field can vary due to environmental variability, making the method unreliable. The success of bioherbicides, such as Phoma macrostoma, in weed control is affected by weather and, in particular, temperature and relative humidity. This sensitivity is a barrier to widespread adoption, especially in areas that have changing weather patterns. These challenges diminish the growth of the bioherbicides market share and indicate the requirement to develop strong strains to enhance field consistency and global bioherbicides market trends.

Segmentation Analysis:

By Source

Microbials dominated the bioherbicides market in 2024 with a 60.5% share, attributed to their high compatibility with organic farming and eco-safety. These comprise friendly bacteria, fungi, and viruses that attack particular weed species without affecting crops. 3.3 Low-Risk Biopesticide Registration supports. The U.S. EPA provides technical assistance for microbial herbicides by expediting low-risk biopesticide registration. This allows for accelerated commercialization and implementation across both organic and conventional systems. The adoption of microbial herbicides in integrated weed management has led to their being preferred as a sustainable agricultural option.

Biochemicals are projected as the fastest-growing source in the bioherbicides market, registering a CAGR of 15.6% during 2025–2032. These herbicides have natural products, such as allelochemicals and plant extracts, as active ingredients for specific weed control. The European Commission’s Farm to Fork Strategy encourages cutting down on the use of chemicals to control pests and increasing demand for safer biochemical alternatives. Their growing popularity in certified organic farming and low toxicity factors fuel adoption in fruits, vegetables, and specialty crops, which is likely to push the market growth of biochemical bioherbicides.

By Formulation

Granular formulations dominated with the largest market share of 52.6% in the bioherbicides market in 2024 on account of their easy application, storage stability, and controlled release. Granulated bioherbicides are especially popular in extensive cereal and grain farming, as they can be targeted into the soil with a long-term effect. Granular bioherbicides are advocated by the USDA in sustainable crop programs as they are efficient and have limited respray requirements. Their compatibility with chemical control measures makes them more acceptable in integrated weed management practices.

Liquid bioherbicides are the fastest-growing formulation with a CAGR of 15.42% through 2032, owing to developments in foliar spray technologies and their compatibility with precision farming systems. These products can be easily applied via conventional spray equipment, such as that used for vegetables and row crops. Liquid microbial herbicides have been registered by the EPA under the Biopesticides Program and are thus available on the market. Their compatibility with most formulations, quick absorption, and homogeneous spreading have gained them growing acceptance for weed suppression sustainably and cost-effectively.

By Mode of Application

Soil application dominated the bioherbicides market in 2024, accounting for 36.8% market share, on account of its effectiveness on pre-emergent weed control and root zone targeting. It provides enhanced microbial activity and a longer residual effect, reducing the necessity of several applications. Soil-applied bioherbicides are being acknowledged by the USDA in its conservation and soil health programs, which should further encourage adoption. Most Effective In-between Row Crop and Cereals. This technology is one of the most important steps towards building up top healthy soils while at the same time providing excellent time management of weeds.

Seed treatment emerged as the fastest growing segment in bioherbicides with a CAGR of 15.59% through 2032, attributed to the increase in advancements in seed coating technologies as well as early weed suppression advantages. This process allows for direct application at germination, decreasing total herbicide and labor expense. Studies conducted on seed treated with fungi like Trichoderma and by many agri-tech firms and the USDA have shown improved germination and early growth. It is being relied on more and more in crops like soybean and corn, where early weed resistance is considered an important factor in productivity.

By Crop Type

Fruits and vegetables dominated the bioherbicides market in 2024 with a 34.7% share, driven by strict pesticide residue norms and growing preference for organic fruits and vegetables. Organic fruits and vegetables are the biggest category in U.S. organic food sales, according to the Organic Trade Association. Growers are transitioning to microbial herbicides to satisfy the organic mandate and, increasingly, consumers. Formulators are developing bioherbicides for high-value crops in order to save yield and remove chemicals.

Turf and ornamental grass is the fastest-growing segment in the bioherbicides market with a CAGR of 16.06% through 2032, owing to the rising demand for eco-friendly landscaping and minimum use of pesticides in public places. Cities and golf courses are turning to microbial herbicides to comply with regulations. Agriculture and Agri-Food Canada has demonstrated that the use of bioherbicides such as Phoma macrostoma can control weeds such as Dandelions in turf grass for a minimum of three successive seasons of growth and are as effective with the same consistent standards as traditional chemical weed control (chemical phytotoxicants MCPP). This market is anticipated to account for a substantial share of the overall market in the future.

Regional Analysis:

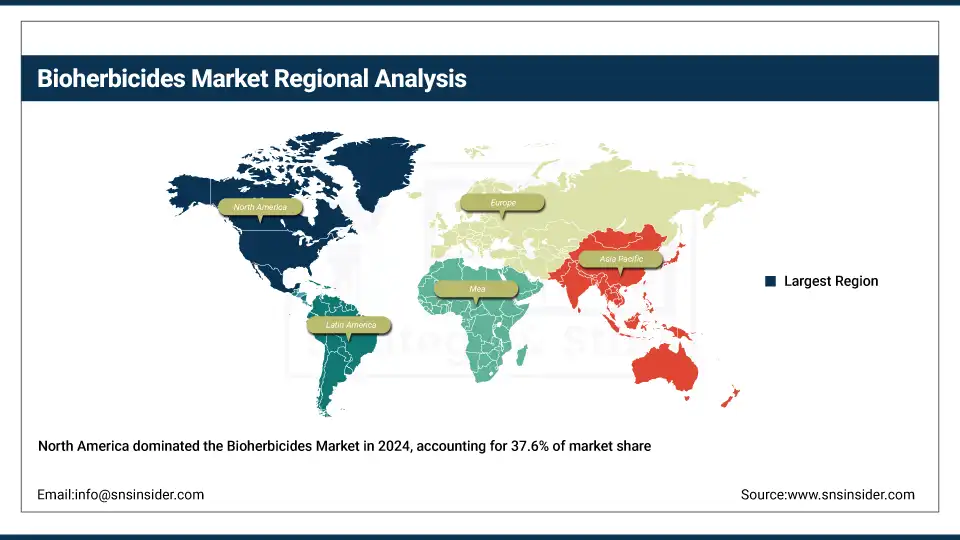

The bioherbicides market from North America accounted for a dominant share of about 37.6% in 2024, which is attributed to large organic farm practices and supportive regulations. In enabling these microbial herbicides to be developed, government agencies such as the Department of Agriculture and the Environmental Protection Agency have provided funding for research and eliminated bureaucratic obstacles to approval under the biopesticides program. USDA data also displayed that over 4.8 million gross acres of land were certified organic last year, thus continuing to drive the switch to organic farming chemicals and sustainable weed control techniques in the area.

Get Customized Report as per Your Business Requirement - Enquiry Now

The bioherbicides market in Asia Pacific is the fastest-growing market and is expected to witness a CAGR of 15.89% during the forecast period 2025-2032. Market growth is mainly attributed to increasing adoption of organic farming practices, government support and sustainable weed control measures. India has shown the way through initiatives such as the Paramparagat Krishi Vikas Yojana and the National Mission on Sustainable Agriculture. The Indian Council of Agricultural Research (2018) has encouraged the growing of microbial herbicides such as Trichoderma viride in vegetables. These efforts along with rising popularity of organic farming chemicals are likely to make India a strong contributor to the regional bioherbicides market.

Key Players:

The major bioherbicides market competitors include Marrone Bio Innovations, Inc., Certis Biologicals (Certis USA L.L.C.), Koppert Biological Systems, BioWorks, Inc., Valent BioSciences LLC, Agrauxine by Lesaffre, Andermatt Biocontrol AG, Vestaron Corporation, Bioworks Australia Pty Ltd, and STK Bio-Ag Technologies (Stockton Group)

Recent Developments:

-

In April 2024, Syngenta partnered with Lavie Bio to accelerate biopesticide R&D using AI-driven microbial discovery, aiming to cut development time by 2–3 years and boost innovation in biological weed control.

-

In March 2024, Moa Technology signed a 10-year deal with Croda to develop next-gen bioherbicides, combining AI herbicide discovery with marine microbiome research to combat resistant weeds like pigweed and water hemp.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.39 billion |

| Market Size by 2032 | USD 10.56 billion |

| CAGR | CAGR of 15.26% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Source (Microbials, Biochemicals, and Others) •By Formulation (Liquid, and Granular) •By Mode of Application (Foliar Spray, Soil Application, Seed Treatment, and Post-Harvest) •By Crop Type (Grains & Cereals, Oil seeds, Fruits & Vegetables, Turf & Ornamental Grass, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Marrone Bio Innovations, Inc., Certis Biologicals (Certis USA L.L.C.), Koppert Biological Systems, BioWorks, Inc., Valent BioSciences LLC, Agrauxine by Lesaffre, Andermatt Biocontrol AG, Vestaron Corporation, Bioworks Australia Pty Ltd, and STK Bio-Ag Technologies (Stockton Group) |

Frequently Asked Questions

Herbicide resistance in weeds increases demand for bioherbicides as effective, eco-friendly alternatives to conventional chemical treatments.

USDA, EPA, and EU subsidies and regulatory frameworks significantly support bioherbicides companies and sustainable weed control adoption.

Rising organic farming, regulatory incentives, and demand for sustainable weed control drive bioherbicides market growth and adoption.

North America dominates the bioherbicides market, followed by Europe, while Asia Pacific is the fastest-growing region globally.

The bioherbicides market is expected to grow at a compound annual growth rate of 15.26% from 2025 to 2032.

Get in Touch