Ethylene Carbonate Market Report Scope & Overview:

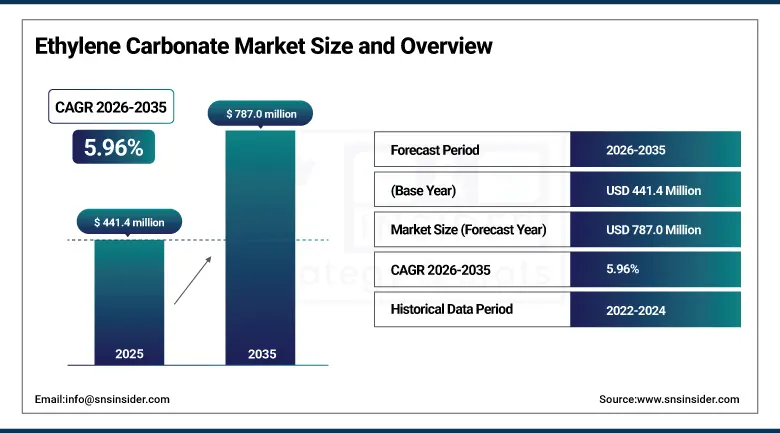

The Ethylene Carbonate Market was valued at USD 441.4 Million in 2025 and is expected to reach USD 787.0 Million by 2035, growing at a CAGR of 5.96% from 2026–2035.

The Ethylene Carbonate Market is experiencing growth because of increased usage of lithium-ion batteries that are used in electric vehicles and energy storage solutions, where ethylene carbonate acts as the primary electrolyte solvent. Increased use of electric mobility, renewable energy sources, and portable electronic devices is another factor contributing to the growth of ethylene carbonate consumption. Growing industrial applications including those in lubricant production, plasticizers, and surface coating is adding up to the market growth as well. Advances in technology and government support are making a significant contribution towards market growth.

According to the International Energy Agency (IEA), global electric car sales reached approximately 14 million units in 2023, accounting for around 18% of total global car sales, significantly driving demand for lithium-ion battery materials including ethylene carbonate. The U.S. Department of Energy (DOE) reports that lithium-ion battery demand has increased more than tenfold over the past decade, primarily driven by the rapid expansion of electric vehicles and grid-scale energy storage systems, reinforcing strong upstream demand for electrolyte solvents.

Ethylene Carbonate Market Size and Forecast:

-

Market Size in 2026E: USD 467.7 Million

-

Market Size by 2035: USD 787.0 Million

-

CAGR: 5.96% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information on Ethylene Carbonate Market - Request Free Sample Report

Ethylene Carbonate Market Trends:

-

Rapid EV production growth is intensifying demand for battery-grade high-purity ethylene carbonate as a primary lithium-ion electrolyte co-solvent.

-

IRA and EU battery regulation domestic content requirements are creating regional ethylene carbonate production capacity investment in North America and Europe.

-

Green lubricant formulation incorporating ethylene carbonate as a biodegradable high-performance base is expanding industrial and automotive lubricant applications.

-

Surface coating innovation using ethylene carbonate as a reactive diluent is improving adhesion and environmental compliance in low-VOC coating formulations.

-

Pharmaceutical sector adoption of ethylene carbonate as a low-toxicity ICH Class 3 solvent is progressively substituting more hazardous restricted alternatives.

U.S. Ethylene Carbonate Market Outlook:

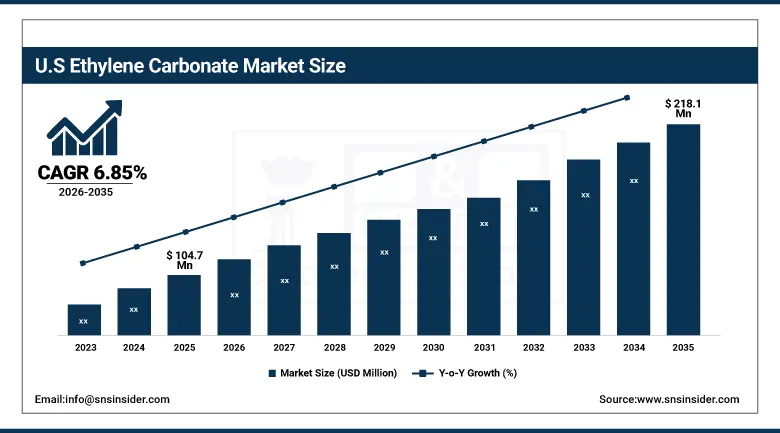

The U.S. Ethylene Carbonate Market was valued at approximately USD 104.7 Million in 2025 and is expected to reach approximately USD 218.1 Million by 2035, growing at a CAGR of approximately 6.85%.

U.S. Ethylene Carbonate Market Growth can be attributed to substantial expansion in electric vehicle usage and lithium ion battery production. The rising demand for energy storage technologies, growing consumption in industrial segments such as lubricants and paints, and clean energy policies are factors fueling the market. Increasing technological advances in chemical processing, along with sustainable energy practices, are also contributing to market growth.

According to the U.S. Energy Information Administration (EIA), electric vehicles accounted for approximately 9–10% of new light-duty vehicle sales in 2023–2024 trend estimates, reflecting steady adoption growth and strengthening demand for lithium-ion battery materials.

Ethylene Carbonate Market Segment Analysis:

-

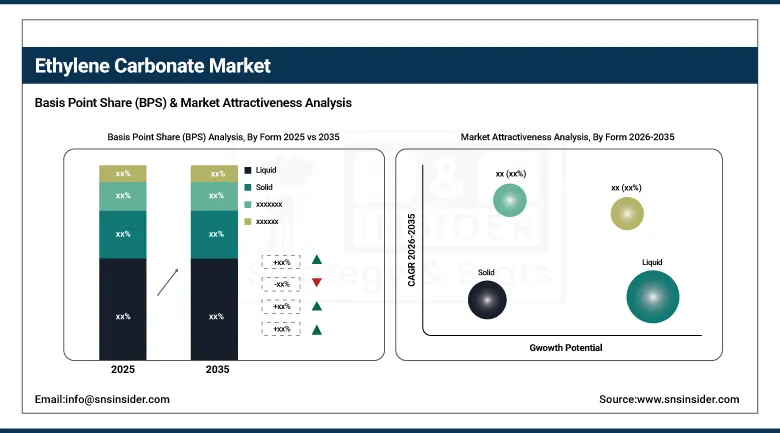

By Form, Liquid segment dominated the Ethylene Carbonate Market in 2025 with 71% share; Solid segment is the fastest growing segment.

-

By Application, Lithium Battery Electrolyte segment dominated the market in 2025 with 68% share; Lubricants segment is the fastest growing segment.

-

By End-use, Automotive segment dominated the market in 2025 with 46% share; Medical segment is the fastest growing segment.

By Form, liquid segment dominates the ethylene carbonate market, while solid segment is the fastest-growing segment

The Liquid segment dominated the Ethylene Carbonate Market owing to its application in lithium-ion batteries and chemicals industry. With a high dielectric constant and excellent solubility properties, it is suitable for large scale applications. Increased demands from the chemical and battery manufacturers contribute to the dominance of the segment. Moreover, ease of handling, efficient processing capabilities, and established logistics networks have also contributed towards its dominance across the global market.

The Solid segment is the fastest growing driven by the rising demand for advanced material in the chemical and energy industry applications. The solid ethylene carbonate has better stability than liquid ethylene carbonate. In addition, advancements in the application field such as solid-state batteries are also boosting the growth of the segment. Besides, growing research activities along with high demand for next-generation energy storage system is expected to drive the market growth in the coming years.

By Application, lithium battery electrolyte segment dominates the ethylene carbonate market, while lubricants segment is the fastest-growing segment

The Lithium Battery Electrolyte segment dominated the Ethylene Carbonate Market owing to its significant contribution towards improving the ionic conductivity and stability of lithium-ion batteries. This segment finds usage in electric vehicles and consumer electronic devices, as well as energy storage systems. Growth in the production of batteries, increase in adoption of EVs, and high demand for energy storage systems have enabled market domination by this segment. Innovations in battery chemistry further bolster its significance in the worldwide energy applications.

The Lubricants segment is the fastest growing due to the increasing adoption of ethylene carbonate as a functional additive for better lubrication properties. The compound increases the viscosity control, thermal stability, and efficiency of the system. Higher industrial automation rates, increased production capacity, and growing demand for more energy-efficient equipment are driving the usage of ethylene carbonate-based lubricants. Additionally, advances in lubricants formulations for modern machines are boosting growth.

By End-use, automotive segment dominates the ethylene carbonate market, while medical segment is the fastest-growing segment

The Automotive segment dominated the Ethylene Carbonate Market due to high demand for Ethylene Carbonate in applications related to electric and hybrid cars. Ethylene Carbonate is vital in enhancing the performance and energy efficiency of EV batteries. With the fast spread of EVs around the world because of stringent emission norms and increasing production of automobiles, this segment would continue to remain dominant in the coming years through investments in EV manufacture and battery technology.

The Medical segment is the fastest growing owing to increasing use of ethylene carbonate in medicines, biomedical applications, and specialty chemicals. The growth in healthcare innovations and increased demand for drug delivery mechanisms is fueling its growth. In addition, the purity and stability of ethylene carbonate make it highly suitable for use in this application. Increasing investments in healthcare are also fueling growth in this sector.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

56.8% |

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Middle East & Africa |

Saudi Arabia |

28.4% |

|

Latin America |

Brazil |

43.8% |

Asia Pacific Ethylene Carbonate Market Insights

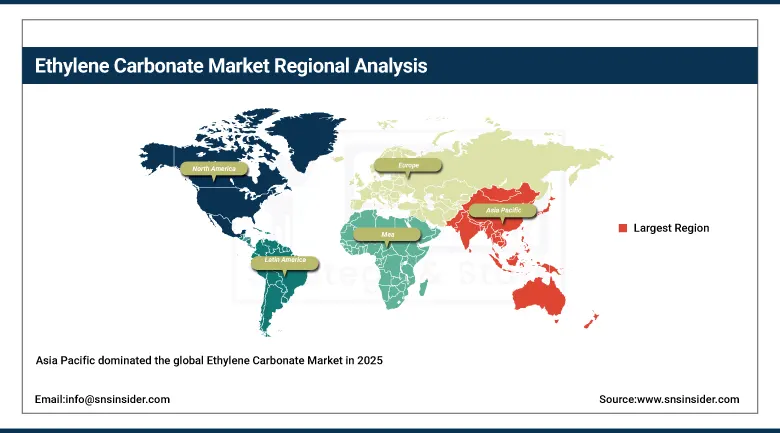

Asia Pacific dominated the global Ethylene Carbonate Market in 2025, accounting for the largest regional revenue share through its concentration of lithium-ion battery manufacturing in China, South Korea, and Japan, the world-leading electronics complex creating EC demand for portable device batteries, and the rapidly expanding EV industry whose battery procurement creates the largest regional EC consumption. China accounts for approximately 56.8% of Asia Pacific revenues through CATL, BYD, and CALB’s battery manufacturing whose combined EC electrolyte consumption defines the market’s demand trajectory.

According to China’s Ministry of Industry and Information Technology (MIIT), China remains the world’s largest producer of lithium-ion batteries, with annual production exceeding several hundred GWh, reinforcing its dominant role in the global battery supply chain and related material demand.

Japan and South Korea contribute premium regional demand through Toyota’s, Panasonic’s, and Samsung SDI’s battery technology programmes whose high-specification electrolyte requirements create pharmaceutical-grade EC procurement. India is the most commercially dynamic emerging market within Asia Pacific, where domestic EV manufacturing investment under the Production Linked Incentive scheme and growing battery manufacturing capacity are creating new EC demand progressively attracting domestic production investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Ethylene Carbonate Market Insights

North America is the fastest-growing regional ethylene carbonate market with a CAGR of approximately 6.85%, driven by the IRA’s USD 369 billion clean energy investment mobilising domestic EV and battery manufacturing that requires localised EC supply chains. The United States accounts for approximately 82.5% of North American revenues through its growing gigafactory network whose combined battery production capacity creates substantial domestic EC procurement above historical import-dependent baseline consumption.

The U.S. Department of Energy (DOE), under the Inflation Reduction Act, highlights large-scale federal incentives and tax credits aimed at accelerating domestic EV adoption and expanding battery manufacturing capacity across the supply chain.

According to the U.S. Department of Energy (DOE), more than USD 40 billion in battery manufacturing investments have been announced in the United States since 2022, supporting rapid expansion of domestic lithium-ion battery production infrastructure.

Canada contributes supplementary North American revenues through the Stellantis-LG Energy Solution battery plant in Windsor and the progressive EV adoption creating growing battery EC demand. Canadian specialty chemical companies are progressively evaluating EC production investment to serve the North American battery supply chain whose domestic content requirements create commercial motivation for regional chemical intermediate manufacturing closer to gigafactory end users.

Europe Ethylene Carbonate Market Insights

Europe is a significant ethylene carbonate market where the EU Battery Regulation’s supply chain sustainability requirements, automotive industry’s electrification investment, and specialty solvent consumption create consistent and growing demand. Germany accounts for approximately 24.6% of European revenues through BASF’s specialty carbonate chemical production, the automotive OEM battery supply chain’s EC procurement, and the industrial lubricant sector’s high-performance additive consumption from its world-leading automotive and machinery manufacturing sectors.

According to the European Commission, electric vehicle battery demand in Europe is projected to exceed 400 GWh annually by 2030, reflecting strong growth in EV adoption and associated demand for lithium-ion battery materials. The European Commission’s REPowerEU plan emphasizes rapid expansion of energy storage systems to support large-scale renewable energy integration, strengthening long-term demand for advanced battery technologies and related electrolyte components.

MEA & Latin America Ethylene Carbonate Market Insights

Saudi Arabia leads MEA revenues at approximately 28.4% through ARAMCO’s chemical complex creating specialty chemical production, the industrial lubricant sector’s EC demand from petrochemical and oilfield operations, and Vision 2030’s chemical industry diversification investment creating domestic specialty chemical infrastructure. The UAE’s growing EV adoption and chemical manufacturing investment contribute growing regional demand for battery and industrial applications.

Brazil leads Latin American revenues at approximately 43.8% through its automotive sector’s EV transition, the industrial lubricant market’s specialty additive adoption, and the pharmaceutical sector’s specialty solvent procurement. Mexico’s large automotive manufacturing sector’s growing EV production for the North American market creates above-regional-average EC demand growth aligned with battery supply chain localisation investment.

Market Dynamics:

Growth Drivers: Electric vehicle production acceleration driving battery electrolyte demand and industrial lubricant consumption sustaining diversified market growth

The ethylene carbonate market’s most structurally significant growth driver is the global EV industry’s production ramp-up whose battery electrolyte EC consumption scales directly with each vehicle produced and each kWh manufactured. The IEA’s projection of 40 to 50 million annual EV sales by 2030 from 17 million in 2024 creates a battery EC demand trajectory that transforms a specialty solvent into a strategically important industrial chemical. Supply chain localisation under IRA and EU Battery Regulation domestic content requirements creates regional EC production capacity investment whose commercial returns depend on sustained domestic battery manufacturing competitiveness through the forecast period.

Industrial lubricant demand for ethylene carbonate as a high-performance additive providing superior boundary lubrication, thermal stability, and biodegradability creates a commercially resilient parallel demand stream whose growth tracks industrial equipment production and the transition from mineral to synthetic lubricant formulations. The lubricant market’s sustained procurement provides commercial stability that mitigates battery market procurement cyclicality and sustains consistent overall market revenue growth through periods of battery investment volatility.

Restraints: Ethylene oxide feedstock price volatility and environmental compliance requirements creating cost pressure for EC producers

Ethylene carbonate production’s dependence on ethylene oxide as the primary feedstock creates manufacturing cost sensitivity to pricing whose volatility tracks crude oil and natural gas feedstock costs external to EC producers’ commercial control. Each ethylene oxide price spike that increases EC production costs creates margin pressure on manufacturers whose customer pricing agreements may not allow rapid cost pass-through, constraining investment in new capacity during high feedstock cost periods. REACH solvent classification review and potential reclassification of EC’s environmental profile creates compliance uncertainty for producers serving European markets.

Environmental regulation in Asia Pacific markets, particularly China’s chemical safety and compliance requirements for specialty chemical manufacturers, creates compliance investment requirements that increase production cost for smaller domestic producers. Each regulatory tightening requiring upgraded emissions control, wastewater treatment, and worker safety infrastructure adds production cost whose impact on competitive market pricing compresses margins in commodity industrial-grade EC segments where price competition from multiple Asian producers is most intense.

Opportunities: Solid-state battery electrolyte development and pharmaceutical solvent substitution creating premium EC market expansion

Solid-state battery technology development, where ethylene carbonate derivatives and carbonate-based solid electrolytes are evaluated as next-generation lithium-ion conductor materials, creates a potential new EC application whose commercial realisation would expand demand beyond liquid electrolyte into solid electrolyte material supply. Each solid-state battery programme demonstrating carbonate-based electrolyte performance creates procurement relationships whose premium pricing and technology leadership position create commercial value above commodity EC markets, attracting both established chemical producers and specialist materials companies to invest in EC derivative research.

Pharmaceutical solvent substitution represents a near-term commercial opportunity as REACH’s progressive restriction of NMP, DMF, and other Class 2 reproductive toxicity solvents creates pharmaceutical API manufacturers’ active evaluation of ethylene carbonate as a less hazardous ICH Q3C Class 3 solvent alternative. Each successful pharmaceutical process validation replacing a restricted solvent with EC creates a permanent pharmaceutical-grade procurement relationship whose quality specifications and supply continuity requirements sustain long-term commercial relationships with premium pricing above commodity EC markets.

Recent Developments:

-

2024: Mitsubishi Chemical Holdings expanded battery-grade ethylene carbonate production capacity at its Yokkaichi facility in Japan, targeting growing demand from domestic and export lithium-ion battery electrolyte manufacturers supplying the automotive EV powertrain market requiring consistent high-purity supply.

-

2024: BASF SE launched enhanced-purity ethylene carbonate grades for battery electrolyte applications, providing sub-ppm metallic impurity specifications and improved electrochemical stability documentation meeting next-generation lithium-ion battery electrolyte qualification requirements of automotive OEM programmes.

-

2023: Huntsman Corporation announced expansion of its cyclic carbonate chemical portfolio in North America, addressing growing domestic demand for ethylene carbonate in battery electrolyte, specialty lubricant, and industrial solvent applications driven by IRA-stimulated EV manufacturing investment.

Ethylene Carbonate Market Key Players are:

-

BASF SE

-

Mitsubishi Chemical Corporation

-

Asahi Kasei Corporation

-

UBE Corporation

-

Huntsman Corporation

-

Shandong Shida Shenghua Chemical Group

-

Lotte Chemical Corporation

-

China Petroleum & Chemical Corporation (Sinopec)

-

LG Chem Ltd.

-

Merck KGaA

-

Mitsubishi Gas Chemical Company Inc.

-

Dalian Kimphar Pharmaceutical Chemical Co., Ltd.

-

Huntsman Advanced Materials

-

Toagosei Co., Ltd.

-

Nippon Shokubai Co., Ltd.

-

SABIC

-

Zhejiang Capchem Technology Co., Ltd.

-

Shandong Haike Chemical Group Co., Ltd.

-

Formosa Plastics Corporation

-

Huntsman Petrochemical LLC

Ethylene Carbonate Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 441.4 Million |

| Market Size by 2035 | USD 787.0 Million |

| CAGR | CAGR of 5.96% from 2026–2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Form (Solid, Liquid) •By Application (Lubricants, Surface Coatings, Lithium Battery Electrolyte, Plasticizers, Others) •By End-use (Automotive, Industrial, Oil & Gas, Medical, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Mitsubishi Chemical Corporation, Asahi Kasei Corporation, UBE Corporation, Huntsman Corporation, Shandong Shida Shenghua Chemical Group, Lotte Chemical Corporation, China Petroleum & Chemical Corporation (Sinopec), LG Chem Ltd., Merck KGaA, Mitsubishi Gas Chemical Company Inc., Dalian Kimphar Pharmaceutical Chemical Co., Ltd., Huntsman Advanced Materials, Toagosei Co., Ltd., Nippon Shokubai Co., Ltd., SABIC, Zhejiang Capchem Technology Co., Ltd., Shandong Haike Chemical Group Co., Ltd., Formosa Plastics Corporation, Huntsman Petrochemical LLC |

Frequently Asked Questions

The Ethylene Carbonate Market is expected to grow at a CAGR of 5.96% from 2026 to 2035.

The Ethylene Carbonate Market was valued at USD 441.4 Million in 2025.

Rising adoption of lithium-ion battery electrolytes driven by EV production acceleration, industrial lubricant market growth, and pharmaceutical solvent substitution from more hazardous restricted alternatives are the primary growth factors.

The Lubricants segment dominated the Ethylene Carbonate Market with approximately 35.24% share in 2025.

Asia Pacific dominated the Ethylene Carbonate Market in 2025.

Get in Touch