Biorationals Market Report Scope & Overview:

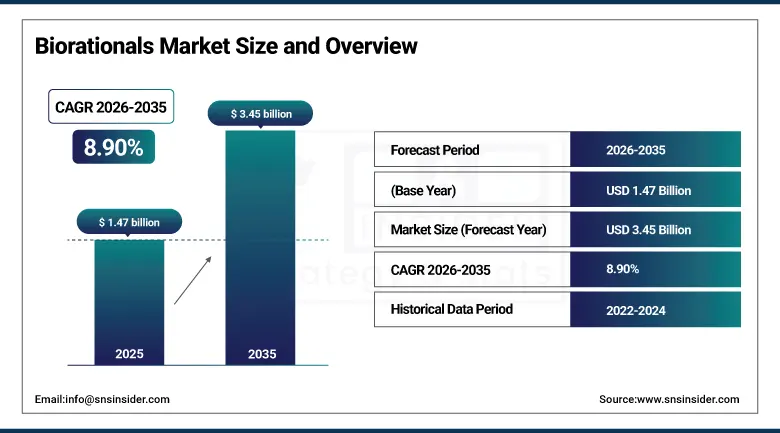

The Biorationals Market was valued at USD 1.47 Billion in 2025 and is expected to reach USD 3.45 Billion by 2035, growing at a CAGR of 8.90% from 2026–2035.

The Biorationals Market is experiencing significant growth because of growing demands for eco-friendly and sustainable crop protection techniques as people increasingly prefer natural products instead of using harmful chemicals like pesticides. There is growing worry about soil conditions, food safety, and the effect of harmful chemicals on the environment. The rising practice of organic farming and stringent international regulations regarding synthetic agrochemicals will help boost the demand for biorationals in the coming years. Moreover, the increased resistance of pests against pesticides is another reason behind adopting biorationals.

According to the Food and Agriculture Organization (FAO), global pesticide use exceeds 3.5 million tonnes annually, increasing pressure for safer and low-toxicity alternatives such as biorationals. The FAO and UN Environment Programme (UNEP) highlight that nearly 33% of global soils are degraded, intensifying demand for soil-friendly pest control solutions. The International Federation of Organic Agriculture Movements (IFOAM) reports that organic farming now covers more than 70 million hectares of farmland globally, further accelerating reliance on bio-based pest management tools.

Market Size and Forecast:

-

Market Size in 2026E: USD 1.60 Billion

-

Market Size by 2035: USD 3.45 Billion

-

CAGR: 8.90% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Biorationals Market - Request Free Sample Report

Biorationals Market Trends:

-

Pheromone mating disruption systems are replacing insecticide sprays in premium grape, apple, and stone fruit production for export residue compliance.

-

Microbial bio-pesticide formulation advances using encapsulation technology are extending field efficacy and improving UV stability for outdoor crop applications.

-

Digital pest monitoring integration with biorational programme management is enabling threshold-based application timing that improves programme cost-effectiveness.

-

Regulatory phase-out of synthetic broad-spectrum insecticides in Europe and California is creating non-discretionary biorational adoption in affected crop categories.

-

Seed treatment biologicals combining rhizobacteria and mycorrhizal fungi are expanding biorationals from foliar pest control into plant nutrition and establishment.

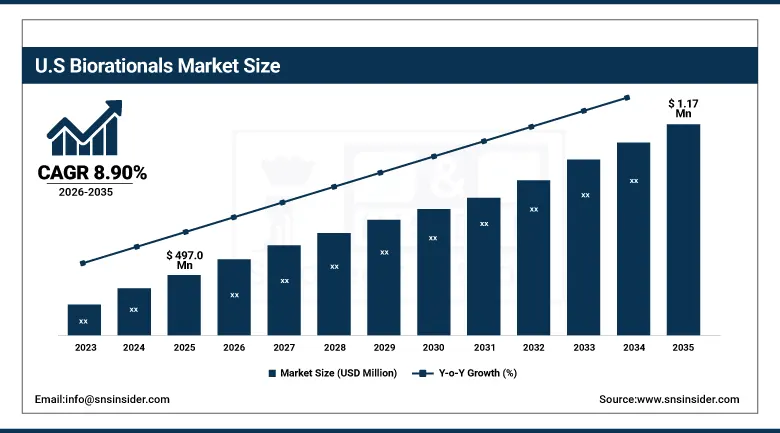

U.S. Biorationals Market Outlook:

The U.S. Biorationals Market was valued at approximately USD 497.0 Million in 2025 and is expected to reach approximately USD 1.17 Billion by 2035, growing at a CAGR of approximately 8.90%.

The United States leads North American biorational revenues through its large organic farming sector, stringent EPA pesticide re-registration programme creating synthetic pesticide phase-out that drives biorational substitution, and the concentration of premium export-oriented specialty crop production in California, Florida, and the Pacific Northwest whose residue compliance requirements create above-average biorational adoption. Certis USA, Valent BioSciences, and Marrone Bio Innovations sustain domestic biorational market leadership through their comprehensive product portfolios spanning microbials, botanicals, and semiochemicals.

According to the U.S. Environmental Protection Agency (EPA), biopesticides are a growing segment of pest control products and are widely used in organic farming and Integrated Pest Management (IPM) systems, supporting the shift toward safer crop protection methods.

Biorationals Market Segment Analysis:

-

By Product, Bio-pesticides segment dominated the Biorationals Market in 2025 with 44% share; Insect Pheromones segment is the fastest growing segment.

-

By Crop Type, Fruits & Vegetables segment dominated the market in 2025 with 38% share; Plantation Crops segment is the fastest growing segment.

-

By Application Mode, Foliar Spray segment dominated the market in 2025 with 52% share; Seed Treatment segment is the fastest growing segment.

By Product, bio-pesticides segment dominates the biorationals market, while insect pheromones segment is the fastest-growing segment

The Bio-pesticides segment dominated the Biorationals Market due to the significant increase in global demand for bio-based alternatives that do not harm the environment. The use of pesticide formulations derived from natural ingredients is increasingly becoming common among farmers who are seeking to eliminate chemical residues, protect soil health, and promote organic farming. This, combined with strict restrictions concerning the use of synthetic agrochemicals and high consumer demand for chemicals-free foods, plays an instrumental role in making bio-pesticides one of the key segments in the market.

The Insect Pheromones segment is the fastest growing due to the increasing adoption of bio-friendly and targeted pest control solutions. The compounds are effective in managing pest populations since they affect insects' ability to mate. There has been a rise in the demand for pest management systems that do not have any negative impacts on ecosystems or beneficial organisms. The trend, coupled with innovation within this technology space, is contributing to its rapid growth.

By Crop Type, fruits & vegetables segment dominates the biorationals market, while plantation crops segment is the fastest-growing segment

The Fruits & Vegetables segment dominated the Biorationals Market Due to their increased susceptibility to pest attacks and the growing demand for pesticide-free fruits, this particular segment accounted for the largest market share. Farmers' tendency to adopt more bio-based crop protection measures has increased with rising food safety and export demands. This particular segment accounts for high economic returns which also contribute to its dominance due to increased spending in advanced pest control measures. The health consciousness of consumers and regulations concerning chemical residues also account for its dominance across regions.

The Plantation Crops segment is the fastest growing because of rising awareness about sustainable farming methods used in crops like tea, coffee, rubber, and palm oil. These crops need effective and environmentally friendly pest control treatments in order to remain productive. An increase in demand for plantation crops all over the world and increased production driven by exports is responsible for this growth trend. Growing environmental consciousness and reduction in chemical dependency have accelerated the adoption of biorationals in this segment.

By Application Mode, foliar spray segment dominates the biorationals market, while seed treatment segment is the fastest-growing segment

The Foliar Spray segment dominated the Biorationals Market owing to the efficiency of delivering bio-based insecticides directly onto plants. It allows for fast absorption, fast action, and efficient protection against various types of pests. The farmers find foliar spray more convenient and economical compared to other application methods and integrate it easily into their integrated pest management systems. Moreover, healthy crops, high-quality yield, and even distribution make the foliar spray an increasingly popular method all around the world.

The Seed Treatment segment is the fastest growing owing to the increased importance being attributed to protecting crops from disease-causing organisms, pests, and stressful environments at the time of germination. It helps in strengthening the initial growth of the crops. The growing interest in sustainable agriculture has led to an increased adoption of this approach. Seed treatment is more effective in enhancing the yields of crops without chemicals.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

India |

38.5% |

|

Middle East & Africa |

Israel |

22.8% |

|

Latin America |

Brazil |

48.6% |

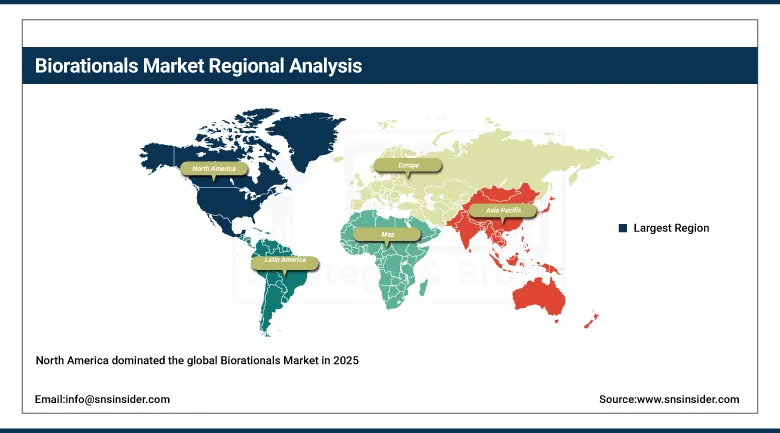

North America Biorationals Market Insights

North America dominated the global Biorationals Market in 2025 through its mature organic farming sector, the EPA’s progressive synthetic pesticide re-registration programme creating structural substitution demand, and the concentration of premium specialty crop production whose export residue compliance and organic certification requirements create above-average biorational adoption. The United States accounts for approximately 82.5% of North American revenues through Certis USA, Valent BioSciences, and BioWorks’ commercial leadership.

The U.S. Department of Agriculture (USDA) reports that organic farmland in the United States exceeds 5 million acres, increasing demand for approved biological crop protection solutions. The USDA also actively promotes Integrated Pest Management (IPM) adoption across farms to reduce reliance on synthetic pesticides and improve soil health and long-term agricultural sustainability.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Biorationals Market Insights

Europe is a technically sophisticated biorationals market where the EU’s Farm to Fork strategy targeting 50% reduction in synthetic pesticide use by 2030, the progressive withdrawal of synthetic active ingredients under the EU’s comparative assessment framework, and mandatory integrated pest management requirements for professional pesticide users collectively create the strongest structural policy environment for biorational adoption globally. Germany accounts for approximately 22.4% of European revenues through its large conventional and organic farming sectors’ biorational programme adoption.

According to Eurostat, organic farming accounts for around 10% of total agricultural land in the European Union, reflecting strong regional demand for non-chemical crop protection methods. The European Environment Agency (EEA) highlights that pesticide use is a key driver of biodiversity loss, supporting policy shifts toward bio-based alternatives across the region.

The EU Farm to Fork Strategy further targets a 50% reduction in chemical pesticide use by 2030, significantly accelerating the adoption of biorationals and sustainable agricultural practices.

Asia Pacific Biorationals Market Insights

Asia Pacific is the fastest-growing regional biorationals market, driven by agricultural modernisation across India, China, Japan, and Southeast Asia, rising organic farming acreage for domestic consumption and export, and government programmes promoting sustainable crop protection as alternatives to synthetic pesticides whose groundwater and food safety impacts are creating regulatory and consumer pressure. India accounts for approximately 38.5% of Asia Pacific revenues through its large organic farming sector and the growing domestic awareness of chemical residue reduction in fresh produce.

According to the Agricultural and Processed Food Products Export Development Authority (APEDA), India has more than 4.5 million hectares under organic farming, significantly increasing demand for bio-pesticides and botanical crop protection solutions.

China’s domestic organic food market’s growth creating biorational demand for domestic production, Japan’s advanced integrated pest management programmes in premium horticulture, and Southeast Asia’s export-oriented tropical fruit and vegetable production sector’s growing adoption of biorational residue management collectively sustain Asia Pacific’s fastest-growing regional trajectory. Koppert’s regional expansion and local production partnerships are progressively increasing biorational access in markets previously served only by imported products.

In China, the Ministry of Agriculture and Rural Affairs (MARA) has implemented policies aimed at reducing pesticide consumption and promoting green agriculture development, further supporting the adoption of biological crop protection alternatives.

MEA & Latin America Biorationals Market Insights

Israel leads MEA revenues at approximately 22.8% through its world-class precision agriculture technology sector’s integration of biorationals into high-value greenhouse and field crop programmes, the export-oriented cut flower and vegetable sector’s residue compliance requirements, and domestic biorational companies’ product development for drip-irrigation application systems. Morocco and Kenya contribute growing African market demand through their fresh produce export sectors’ residue management investment.

Brazil leads Latin American revenues at approximately 48.6% through its world-leading soybean, corn, and tropical fruit production sectors’ growing biological input adoption, driven by the National Biological Control Programme’s investment in scaling domestic production of microbial bio-insecticides, and the premium tropical export fruit sector’s residue compliance requirements for European and North American import markets.

Market Dynamics:

Growth Drivers: Regulatory phase-out of synthetic pesticides and organic farming expansion creating structured non-discretionary biorational adoption

The biorationals market’s most structurally certain growth driver is the regulatory framework’s progressive restriction of synthetic broad-spectrum pesticide active ingredients whose replacement creates structured non-discretionary biorational adoption in affected crop categories. The EU’s active substance re-evaluation programme, the EPA’s pesticide registration review, and California’s Safer Consumer Products Programme collectively create a regulatory replacement pipeline whose annual synthetic pesticide cancellations create protected market space for biorational alternatives. Each synthetic insecticide or fungicide whose registration is cancelled or restricted creates farmer demand for biorational alternatives whose pest control efficacy must substitute for the withdrawn product.

Organic farming’s expansion creates a growing structurally committed biorational demand base whose procurement is non-discretionary within the organic management system. Global certified organic farmland exceeding 74 million hectares in 2023 and growing at approximately 3% annually creates proportional biorational input procurement growth independent of conventional farming’s biorational adoption rate. Each new organic farm certification and each conventional producer transitioning land to organic creates permanent biorational adoption whose replacement of synthetic inputs is a certification requirement rather than an economic choice.

Restraints: Higher cost per treated acre versus synthetics and shorter field residual efficacy limiting biorational adoption in cost-sensitive commodity production

Biorational products’ per-treated-acre cost premium of 20 to 200% relative to equivalent synthetic pesticide applications, combined with their generally shorter field persistence requiring more frequent application, creates economic adoption barriers in cost-sensitive commodity crop production whose thin margin structure limits premium input expenditure. Each grower evaluating biorational adoption in corn, soybean, or wheat production whose conventional pesticide programme costs reflect decades of generic active ingredient price competition creates an economic comparison that biorationals must overcome through documented yield protection or premium market access value.

Biorational products’ sensitivity to UV radiation, temperature extremes, and rainfall events that degrade microbial viability and botanical stability creates efficacy variability in field conditions that reduces grower confidence in biorational pest control reliability compared to synthetic chemical alternatives whose stability under adverse weather conditions is well-documented. Each crop failure attributable to biorational programme underperformance during stress conditions creates adoption reluctance that delays repeat purchase.

Opportunities: Precision application technology integration and biologicals registration data sharing creating commercial accelerators for biorational market expansion

The integration of biorational application programmes with precision agriculture technology including real-time pest population monitoring through IoT trap networks, remote sensing-based crop stress detection, and AI-powered application timing recommendation creates a commercial value proposition whose decision support capability improves biorational efficacy by optimising application timing to pest population thresholds that maximise product performance. Each digital agriculture platform that integrates biorational programme management reduces the knowledge barrier that grower adoption of technically complex biorational programmes has historically required.

Regulatory pathway acceleration through data sharing among biorational registrants, where collaborative minor use registration programmes and registration data pooling for biological active ingredients with broad pest and crop activity profiles reduce the per-product regulatory cost, creates commercial expansion into crop categories and pest targets where individual company registration investment economics were previously insufficiently attractive. Each joint registration programme that extends biorational label coverage at shared cost creates addressable market expansion.

Recent Developments:

-

2024: FMC Corporation broadened its biorational portfolio with biological and digital solutions integrating bio-pesticide products with digital pest monitoring platforms enabling precision application timing to pest thresholds identified through real-time trap count data.

-

2024: Valent BioSciences expanded its microbial insecticide portfolio with enhanced Bt formulations providing improved UV stability and faster knockdown activity for lepidopteran pest management in fruit and vegetable crops with tight pre-harvest interval requirements.

-

2024: Koppert Biological Systems launched its new Trianum Shield bio-fungicide formulation with enhanced Trichoderma harzianum activity for soil-borne pathogen management in greenhouse and high-tunnel vegetable production, expanding its biological soil health programme.

Biorationals Market Key Players are:

-

BASF SE

-

Syngenta AG

-

Bayer AG

-

Corteva Agriscience

-

FMC Corporation

-

UPL Limited

-

Koppert Biological Systems

-

Marrone Bio Innovations

-

Novozymes A/S

-

Isagro S.p.A.

-

Valent BioSciences LLC

-

Certis Biologicals

-

Andermatt Biocontrol AG

-

BioWorks Inc.

-

Stockton Bio AG

-

Seipasa S.A.

-

Russell IPM Ltd.

-

Biobest Group NV

-

Sumitomo Chemical Co., Ltd.

-

Lallemand Plant Care

Biorationals Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.47 Billion |

| Market Size by 2035 | USD 3.45 Billion |

| CAGR | CAGR of 8.90% from 2026–2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Bio-pesticides, Botanicals, Insect Pheromones, Insect Growth Regulators, Semiochemicals, Others) • By Crop Type (Fruits & Vegetables, Field Crops, Cereals & Grains, Plantation Crops, Others) • By Application Mode (Foliar Spray, Soil Treatment, Seed Treatment, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Syngenta AG, Bayer AG, Corteva Agriscience, FMC Corporation, UPL Limited, Koppert Biological Systems, Marrone Bio Innovations, Novozymes A/S, Isagro S.p.A., Valent BioSciences LLC, Certis Biologicals, Andermatt Biocontrol AG, BioWorks Inc., Stockton Bio AG, Seipasa S.A., Russell IPM Ltd., Biobest Group NV, Sumitomo Chemical Co., Ltd., Lallemand Plant Care |

Frequently Asked Questions

The Biorationals Market is expected to grow at a CAGR of 8.90% from 2026 to 2035.

The Biorationals Market was valued at USD 1.47 Billion in 2025.

Regulatory phase-out of synthetic pesticides creating non-discretionary biorational adoption, organic farming expansion creating a structurally committed demand base, and export produce residue compliance requirements driving specialty crop biorational programmes are the primary growth factors.

Bio-pesticides dominated the Biorationals Market with the largest share in 2025, while Botanicals is the fastest growing product with a CAGR of approximately 10.2%.

North America dominated the Biorationals Market in 2025.

Get in Touch