Organosilicon Polymers (Polysiloxane) Market Report Scope & Overview:

Get E-PDF Sample Report on Organosilicon Polymers (Polysiloxane) Market - Request Sample Report

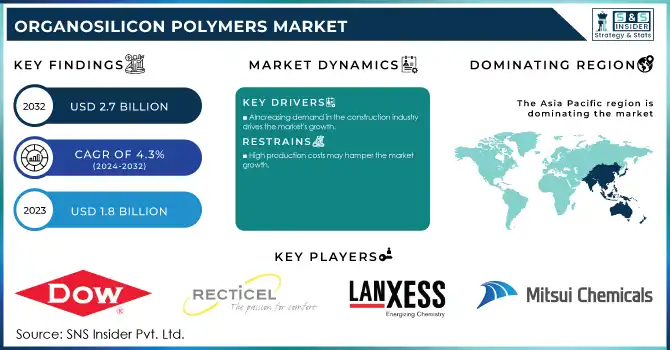

The Organosilicon Polymers Market was USD 1.8 billion in 2023 and is expected to reach USD 2.7 billion by 2032, growing at a CAGR of 4.3% over the forecast period of 2024-2032.

One of the biggest factors contributing to the global development of the organosilicon polymers (polysiloxane) market is the demand for these high-performance materials, as they possess unique properties like thermal stability, chemical inertness, and durability. As such, these materials are increasingly used where reliability under extreme conditions is required, such as in the aerospace, automotive, and electronics industries. Polysiloxanes may also be utilized in many uses including sealants, adhesives, and protective coatings due to their unique temperature. As industries evolve to new ideas and require new materials, polysiloxanes will gain a much larger footprint as they continue to allow for novel applications with performance benefits.

In the United States, the Department of Energy (DOE) has been actively investing in the development and deployment of high-performance materials. In November 2024, the DOE announced a USD 7 million investment to advance high-performance computing for energy innovation, which includes projects aimed at enhancing material performance in energy applications.

The demand for Organosilicon Polymers (Polysiloxane) both in the personal care and consumer product industry is expected to drive the growth of the Organosilicon Polymers (Polysiloxane) market significantly. Polysiloxanes have been found to be extensively used in cosmetics and skin care formulations as they provide a smooth application and a non-greasy, silky feel with the ability to form a film that is breathable yet protective to the skin. They also play a crucial role in the development of water-resistant and long-lasting formulations in sunscreens, primers, and also in hair care products. Beyond cosmetics, polysiloxanes are used in household items from stove pans to sealants and lubricants, as high durability and environmental resistance allow for permanent uses. Growing disposable incomes and urbanization, alongside a shift in consumer propensity towards premium and multifunctional product entities, also remain key propelling agents in terms of the adoption of silicone-based solutions in these markets. Such a trend is in tune with the generic changing landscape toward innovative and sustainable formulations that are only going to further the demand for polysiloxanes.

The growth of the Organosilicon Polymers (Polysiloxane) market is significantly influenced by increasing demand in the personal care and consumer products sectors. In 2022, the personal care products industry in the United States generated a trade surplus of USD 2.6 billion, underscoring its global economic significance.

Organosilicon Polymers Market Dynamics:

Drivers

-

Increasing demand in the construction industry drives the market's growth.

One of the major factors contributing to the growth of the organosilicon polymers (polysiloxane) market is the rising demand from the construction sector. Polysiloxanes possess outstanding properties such as high thermal stability, excellent weather resistance, and superior water repellency, and therefore they are consumed in high amounts for construction applications. These polymers play a key role in the manufacturing of coatings, sealants or protective layers, and adhesives which ultimately contribute to the longevity and beauty of building materials. In addition, continuing steady growth in the global construction industry, especially in developing regions such as India and China where there is a significant expansion of infrastructure and urbanization, drives this demand. Further, increasing focus on the use of sustainable and energy-efficient construction materials has paved the way for the demand for polysiloxane-based coatings that provide energy savings and long-lasting structures. Supported by governmental missions for green construction practices, this trend offers lucrative opportunities to the market for Organosilicon Polymers.

In 2022, Dow introduced a new line of high-performance polysiloxane-based coatings designed for use in the construction and infrastructure sectors. These coatings are formulated to enhance the durability of exterior surfaces exposed to extreme weather conditions, helping to meet the growing demand for sustainable building materials.

-

Utilised a lot while applying for industrial coatings and protection purposes.

Restraint

-

High production costs may hamper the market growth.

The major restraints controlling the growth of the Organosilicon Polymers (Polysiloxane) market are high production costs. Polysiloxanes need unique raw materials and sophisticated processing techniques, and this translates to high operational costs. The production of organosilicon polymers requires high-purity silanes and catalysts as well as energy-consuming processes that require rigorous control and sophisticated equipment. All of this makes the general cost of production higher, leading to certain industries, especially in price-sensitive markets, not being able to afford polysiloxane-based products. Moreover, due to supply chain issues, the costs of raw materials may increase from time to time, exerting pressures on the production costs of polysiloxanes and thus causing difficulties for manufacturers to ensure product quality and profitability. Consequently, this could limit the commercialization of polysiloxane solutions because of the production costs as high-priced materials limit their applicable scope to applications where higher prices can be accepted, such as some industrial cases, but not emerging economies, nor smaller scale projects.

Opportunity:

-

Widely used in a variety of materials as fire retardants

Organosilicon Polymers Market Segmentation

By Product

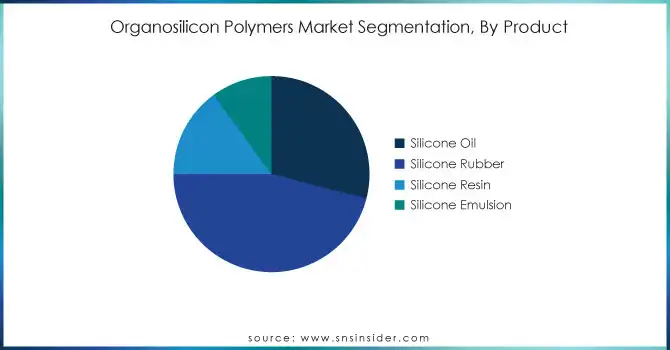

Silicone Rubber held the largest market share around 46% in 2023. Silicon rubber has toughness, flexibility is so remarkable, high-temperature resistibility, etc., which experiences high stability to thermal splitting and can be used in automobile, building, health care, and electronics industries. Its high service temperature, oxidation resistance, and durability make it suitable for high-end applications such as seals, gaskets, electrical insulated, and medical equipment. Furthermore, with the increasing need for sustainable, sustainable, and energy-efficient materials in the automotive and development industries silicone rubber has gained significant growth. Silicone rubber has seen increasing demand due to a gain in penetration of electric vehicles (EVs), coupled with frequent demand for construction-grade materials that function as insulators and weatherproofing partners. Consequently, it provides enhanced performance properties and investigative applicability to an array of different industrial needs, rendering it a dominant form of the polysiloxane market.

By Application

The coatings segment held the largest market share around 34% in 2023. It is owing to the remarkable properties exhibited by polysiloxane-based coatings, making them suitable for a large number of applications. Characterized by exceptional durability, resistance to weather and environment including moisture, UV attack, and extreme temperatures, these coatings are prized and long-lasting. Polysiloxane coatings are being adopted widely in the construction, automotive, and industrial sectors as sustainability and energy efficiency become a more important focus for the industry. The other use in the construction industry is as protective to building facades to prolong the life of exposed building materials from floods and extreme weather events. In addition, polysiloxane coatings play a crucial role in the automotive sector due to their anti-corrosion and anti-scratch features that enhance the durability and aesthetic looks of vehicles.

Organosilicon Polymers Market Regional Analysis

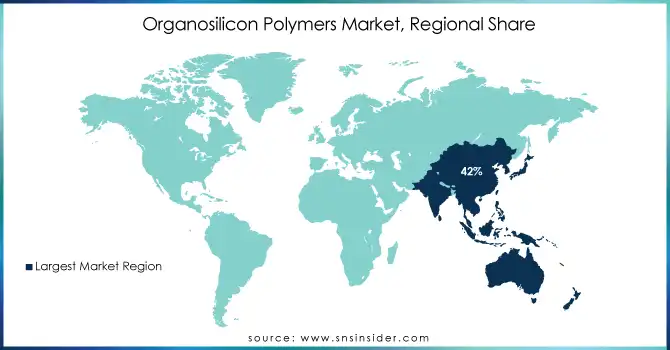

Asia Pacific held the largest market share around 42% in 2023. This is owing to rapid industrialization and urbanization, and high growth in key end-use industries including construction, automotive, and electronics. Infrastructural and manufacturing development is expanding at a remarkable scale in the region, which is home to some of the fastest-growing economies in the world including China, India, and South-East Asian countries. However, the demand for polysiloxane-based coatings and sealants is also driven by the booming construction industry in developing countries such as China and India because they are required to improve the durability and weather resistance of building materials. Besides, the automotive industry in the Asia Pacific, especially in China and Japan, is a key end-user for various silicone rubber and coatings in EVs, its components, and anti-corrosion applications. Additionally, the strong electronics manufacturing sector in the region is a significant end-use industry for polysiloxane-based materials used in semiconductors and electronic devices. The aforementioned factors, in addition to access to inexpensive raw materials and labor, have made Asia Pacific the largest organosilicon polymers market, globally.

Get Customized Report as Per Your Business Requirement - Request For Customized Report

Key Players:

-

Dow (Sylgard, DOWSIL)

-

Recticel (RectiFoam, RectiSil)

-

LANXESS (Silopren, BaySilicone)

-

Mitsui Chemicals (Silicone Rubber, Silsoft)

-

Covestro (Desmodur, Bayhydur)

-

Kuwait Polyurethane Industry w.l.l (KPU, KFlex)

-

BCI Holding (BCI-Sil, BCI-Rubber)

-

Huntsman International (SilForm, EPDM)

-

Tosoh Corporation (Tosflex, Tosilox)

-

ASF SE (ASF-Sil, ASF-Silco)

-

DIC Corporation (DIC-Sil, DIC-Pur)

-

Rogers Corporation (Rogers Silicones, Poron)

-

Wacker Chemie AG (Elastosil, SilGel)

-

Shin-Etsu Chemical Co., Ltd. (KE-132, Silastic)

-

Momentive Performance Materials Inc. (Silopren, RTV Silicone)

-

SABIC (Sabic Silicones, LEXAN)

-

Kraton Polymers (Kraton D, Kraton Polymers SS)

-

Arkema (Sartomer, Altuglas)

-

China National Petroleum Corporation (CNPC) (PetroSil, PolySil)

-

Evonik Industries (Silbond, VESTOSINT)

-

Organosilicon Polymers (Polysiloxane)

Recent Development:

- Dow (2023): Dow introduced its new line of DOWSIL Silicone Coatings specifically designed for sustainable building applications. These coatings offer enhanced energy efficiency and durability, supporting the construction industry's shift toward more eco-friendly materials.

- Recticel (2022): Recticel launched RectiSil, a new high-performance silicone rubber material. This product is designed to meet the growing demand for energy-efficient insulation solutions, particularly in the automotive and construction sectors.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 1.8 Billion |

| Market Size by 2032 | US$ 2.7 Billion |

| CAGR | CAGR of 4.3% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Silicone Oil, Silicone Rubber, Silicone Resin, Silicone Emulsion) • By Application (Coatings, Elastomers, Foams, Adhesives & Sealants, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Organosilicon Polymers (Polysiloxane), Dow (US), Recticel (Belgium), LANXESS (Germany), Mitsui Chemicals (Japan), Covestro (Germany), Kuwait Polyurethane Industry w.l.l (Kuwait), BCI Holding (UAE), Huntsman International (US), Tosoh Corporation (Japan), ASF SE (Germany), DIC Corporation (Japan), Rogers Corporation (US). |

| Key Drivers | • Increasing demand in the construction industry drives the market's growth. • Utilised a lot while applying coatings for industrial and protection purposes. |

| Restraints | • High production costs may hamper the market growth. |

Frequently Asked Questions

Ans: Manufacturers, Consultant, aftermarket players, association, Research institute, private and universities libraries, suppliers and distributors of the product.

Ans: Demand, supply, inventory, and logistics, among other business factors around the world, have all been influenced by the COVID-19 epidemic. The global COVID-19 pandemic has caused a shortage of products, mostly because production facilities in Asia-Pacific, Europe, and the Americas have reduced their working capabilities. As they work to mitigate the effects of the new coronavirus pandemic, governments and businesses are facing an unprecedented catastrophe in 2020 and the first few months of 2021.

Ans: Widely used in a variety of materials as fire retardants are the opportunity for Organosilicon Polymers (Polysiloxane) Market.

Ans: Increasing demand in the construction industry drives the market's growth, Utilised a lot while applying coatings for industrial and protection purposes and Demand from applications in the construction industry is what is driving the market's expansion are the drivers for Organosilicon Polymers (Polysiloxane) Market.

Ans: Organosilicon Polymers (Polysiloxane) Market Size was valued at USD 1.8 billion in 2023, and expected to reach USD 2.7billion by 2032, and grow at a CAGR of 4.3 % over the forecast period 2024-2032.

Get in Touch