Hollow Fiber Membranes Market Report Scope & Overview:

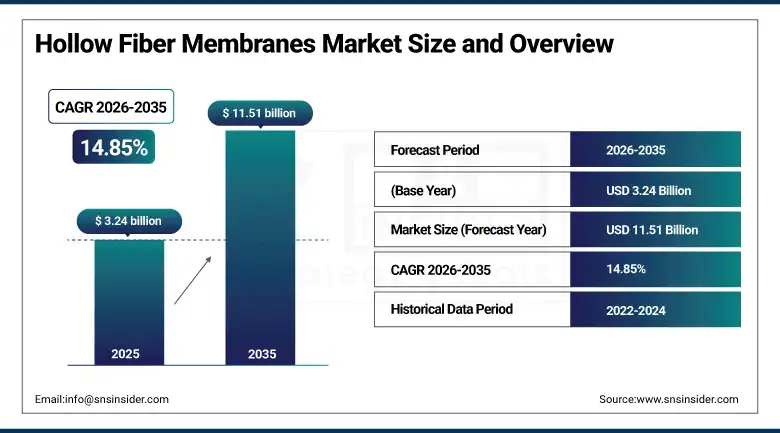

The Hollow Fiber Membranes Market was valued at USD 3.24 Billion in 2025 and is expected to reach USD 11.51 Billion by 2035, growing at a CAGR of 14.85% from 2026 to 2035.

Hollow fiber membranes are tubular semi-permeable filtration structures whose fine cylindrical geometry, with outer diameters typically ranging from 0.5 to 2.0 millimetres and wall thicknesses of 0.1 to 0.5 millimetres, creates an extraordinarily high surface area-to-volume ratio that enables compact, high-throughput filtration module construction at operational footprints and capital costs that flat-sheet and spiral-wound membrane alternatives cannot approach. The hollow core of each fiber serves simultaneously as the permeate collection channel and the structural element that maintains fiber separation and prevents collapse under transmembrane pressure, creating a self-supporting membrane element whose simplicity of manufacture and assembly enables the modular scalability from laboratory-scale cartridges to municipal-scale filtration trains that makes hollow fiber membrane technology uniquely versatile across the full spectrum of industrial and municipal fluid treatment applications.

In 2023, Arkema, Polymem, and Tergys announced a strategic partnership to develop innovative autonomous filtration systems for drinking water supply in remote and water-stressed communities. The collaboration combines Arkema's specialty polymer materials for hollow fiber membrane manufacturing, Polymem's hollow fiber module design and production expertise, and Tergys's solar-powered autonomous water treatment system engineering to create energy-self-sufficient membrane filtration units deployable without grid electricity connection. The partnership demonstrated the growing commercial importance of sustainable, decentralized hollow fiber membrane water treatment solutions for the underserved populations in water-scarce developing markets whose access to centralized water infrastructure cannot be assumed within acceptable deployment timelines.

Market Size and Forecast

-

Market Size in 2026E: USD 3.72 Billion

-

Market Size by 2035: USD 11.51 Billion

-

CAGR: 14.85% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Hollow Fiber Membranes Market - Request Free Sample Report

Hollow Fiber Membranes Market Trends

-

Single-use hollow fiber membrane systems are gaining adoption in biopharmaceutical manufacturing due to reduced contamination risks and simplified operations.

-

Advanced anti-fouling coatings are improving membrane durability, efficiency, and operational lifespan across water treatment and industrial applications.

-

Hybrid membrane systems integrating ultrafiltration, nanofiltration, and reverse osmosis are enabling higher treatment performance and water reuse capabilities.

-

Ceramic hollow fiber membranes are witnessing increased demand in harsh industrial environments requiring superior thermal and chemical resistance.

-

Growing regulations on PFAS and other emerging contaminants are driving adoption of advanced hollow fiber membrane technologies in water treatment applications.

The U.S. Hollow Fiber Membranes Market Outlook

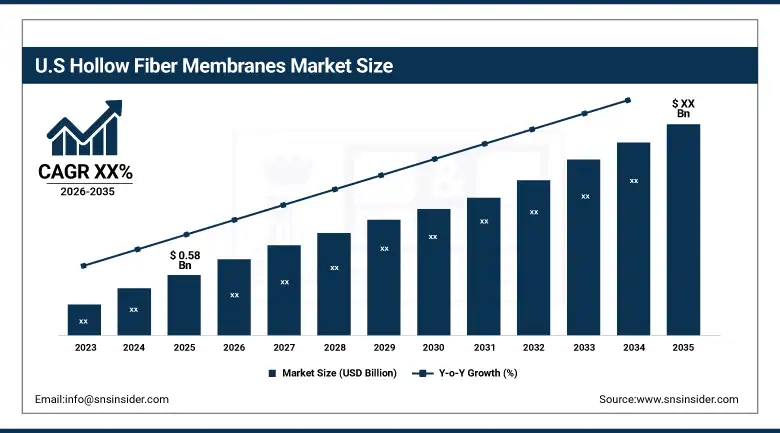

The U.S. Hollow Fiber Membranes Market was valued at approximately USD 0.58 Billion in 2025 and is expected to grow significantly through 2035. North America shows steady growth driven by stringent water quality regulations, technological advancements, and increasing adoption in medical and industrial applications.

The United States hollow fiber membrane market is driven by the EPA's progressively stringent drinking water contaminant regulations, including the PFAS National Primary Drinking Water Regulation whose 4 parts per trillion maximum contaminant level for PFOA and PFAS creates an enormous infrastructure investment requirement across U.S. public water systems, the large and growing U.S. biopharmaceutical manufacturing sector's single-use membrane process technology adoption, and the food and beverage industry's membrane-based processing investment. The U.S. haemodialysis market, whose approximately 550,000 end-stage renal disease patients requiring three-times-weekly dialysis treatment creates among the world's largest per-capita hollow fiber dialysis membrane consumption rates, provides a clinically essential and commercially significant medical device membrane market segment whose demand is driven by chronic disease burden rather than discretionary investment cycles.

In 2025, Koch Membrane Systems launched its TARGA HF high-flux hollow fiber ultrafiltration module series incorporating next-generation polysulfone hollow fiber chemistry with enhanced hydrophilic surface modification that demonstrates 35% higher clean water flux and 40% lower specific energy consumption compared to the company's previous generation HF ultrafiltration products. The improved flux and energy efficiency performance significantly reduces the capital cost per unit of treated water capacity and the operating energy cost per cubic metre of permeate, strengthening hollow fiber ultrafiltration's competitive economics versus competing membrane technologies and conventional coagulation-filtration processes in large-scale municipal and industrial water treatment applications.

Hollow Fiber Membranes Market Segment Analysis

-

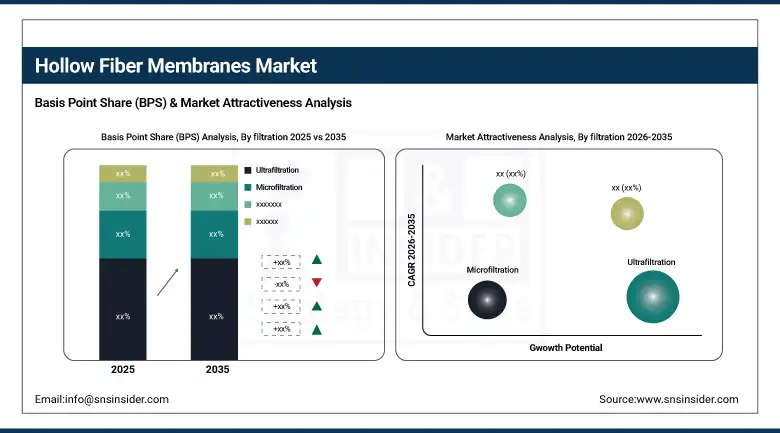

By Filtration Type, ultrafiltration segment dominated the hollow fiber membranes market with approximately 42% market share in 2025, while the reverse osmosis hollow fiber membranes segment is projected to be the fastest growing, registering a CAGR of around 8.1% during 2026–2035.

-

By Membrane Material, polymer membranes dominated the Hollow Fiber Membranes market with the largest share in 2025, while ceramic membranes are the fastest growing material type during the forecast period.

-

By End-Use Industry, water & wastewater treatment dominated the Hollow Fiber Membranes market with the largest share in 2025, while pharmaceuticals & chemicals is the fastest growing end-use industry during 2026 to 2035.

By Filtration Type, ultrafiltration dominates, reverse osmosis grows fastest

Ultrafiltration generated the dominant filtration type revenue share in 2025, reflecting its position as the highest-volume hollow fiber membrane application across the broadest range of municipal and industrial end uses. Municipal drinking water treatment, whose removal of bacteria, protozoa, viruses, and turbidity is the most commercially significant single hollow fiber membrane application by installed module volume, is dominated by ultrafiltration whose pore size provides reliable microbiological barrier performance that regulators classify as equivalent to conventional media filtration. Biopharmaceutical tangential flow filtration for protein concentration, buffer exchange, and viral clearance uses ultrafiltration hollow fiber membranes whose molecular weight cut-off specifications are matched to the protein therapeutic's size, with reproducibility and extractable profile documentation critical for regulatory submissions.

Reverse osmosis hollow fiber applications are growing fastest as desalination capacity expansion across water-scarce Middle Eastern, North African, and South Asian markets, combined with the PFAS removal mandates in North American municipal water systems, creates investment in RO systems whose hollow fiber configuration provides superior packing density and lower operating pressure compared to spiral-wound RO alternatives in certain application contexts. The growing adoption of water recycling and reuse in industrial facilities, driven by both water scarcity and zero liquid discharge regulatory mandates, creates additional demand for RO hollow fiber systems whose concentrated reject stream management requires integration with evaporative or crystallization technologies.

By End-Use Industry, water & wastewater treatment dominates, pharmaceuticals grows fastest

Water and wastewater treatment generated the dominant end-use industry revenue share in 2025, accounting for well over half of global hollow fiber membrane consumption across municipal drinking water production, industrial process water purification, industrial effluent treatment, and water reuse applications whose combined treatment capacity requirements create the world's largest single application category for hollow fiber membrane modules. The global water treatment infrastructure investment imperative is structurally driven by population growth, urbanization, industrial expansion, and climate change-driven hydrological stress that collectively increase both the volume of water requiring treatment and the stringency of treatment quality standards across every regional market.

Pharmaceuticals and chemicals is growing fastest as the biopharmaceutical industry's shift toward single-use bioprocessing architecture, the increasing complexity of biological therapeutic molecules requiring advanced membrane-based purification processes, and the growing regulatory scrutiny of biopharmaceutical manufacturing contamination prevention collectively create accelerating demand for hollow fiber ultrafiltration and diafiltration systems. Each new biologics manufacturing facility represents a substantial hollow fiber membrane procurement event whose single-use membrane volume per product run, multiplied across the multiple purification steps in a biologics downstream processing train, creates significant recurring consumable demand that generates durable aftermarket revenue for hollow fiber membrane suppliers with established biopharmaceutical customer relationships.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

42.84% |

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Middle East & Africa |

Saudi Arabia |

28.47% |

|

Latin America |

Brazil |

43.84% |

North America Hollow Fiber Membranes Market Insights

North America held a significant share of global Hollow Fiber Membranes revenues in 2025, driven by stringent drinking water quality regulations, advanced industrial water treatment adoption, a large biopharmaceutical manufacturing sector, and the large existing haemodialysis patient population. The United States accounts for approximately 82.47% of regional revenue through its EPA-driven water treatment infrastructure investment, its world-leading biopharmaceutical industry's single-use membrane system adoption, and its large installed base of membrane bioreactor wastewater treatment systems. The PFAS regulatory mandate, whose implementation across thousands of U.S. public water systems requires capital investment in advanced membrane treatment, represents one of the most commercially significant single regulatory drivers for hollow fiber membrane market expansion in any major economy over the next decade.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Hollow Fiber Membranes Market Insights

Europe held a significant share of global Hollow Fiber Membranes revenues in 2025. Germany, France, the United Kingdom, the Netherlands, and Scandinavia are the leading national markets whose well-developed water treatment regulatory frameworks, large pharmaceutical manufacturing sectors, and sophisticated food and beverage processing industries create diverse hollow fiber membrane demand. Germany accounts for approximately 28.47% of European revenues through its large chemical and pharmaceutical manufacturing sectors, the commercial presence of major membrane manufacturers including MICRODYN-NADIR and Inge Watertechnologies, and its stringent water quality standards that sustain consistent municipal and industrial membrane investment. The European Union's Water Framework Directive and Urban Wastewater Treatment Directive are sustaining infrastructure investment in membrane-based secondary and tertiary wastewater treatment across member states.

Asia Pacific Hollow Fiber Membranes Market Insights

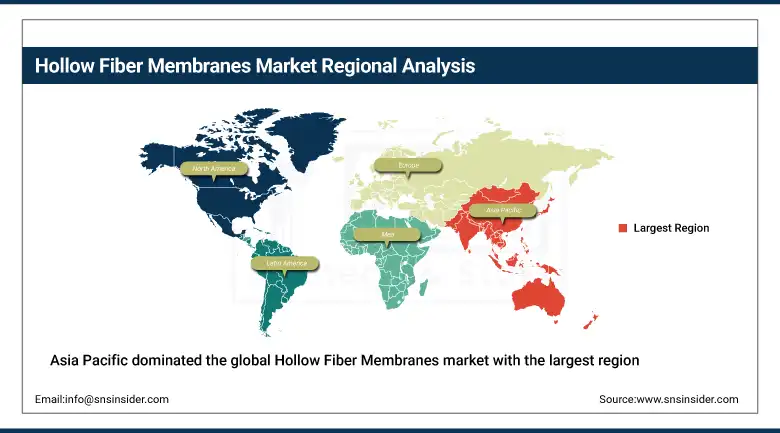

Asia Pacific dominated the global Hollow Fiber Membranes market with the largest regional share of around 41% in 2025, driven by rapid industrialization, urbanization, and increasing investment in municipal and industrial water treatment infrastructure. China accounts for approximately 42.84% of Asia Pacific revenues as both the world's largest producer and a major consumer of hollow fiber membrane modules, whose domestic manufacturing industry has undergone transformative development from import-dependence to export-competitive capability in reverse osmosis and ultrafiltration membrane production. India is growing rapidly as government initiatives including the Jal Jeevan Mission targeting household tap water connections for all rural households by 2024 and the Atal Mission for Rejuvenation and Urban Transformation create large-scale municipal water treatment infrastructure investment that drives hollow fiber membrane procurement.

MEA & Latin America Hollow Fiber Membranes Market Insights

Middle East and Latin America are growing Hollow Fiber Membranes markets where water scarcity, industrial expansion, and progressive regulatory frameworks are creating expanding commercial demand. Saudi Arabia leads MEA revenues at approximately 28.47% of the regional total through its world-class desalination infrastructure investment, the industrial water treatment requirements of its petrochemical processing sector, and Vision 2030's ambitious water security programme whose NEOM and Red Sea Project components require advanced water treatment technology at unprecedented scale. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large municipal water treatment infrastructure investment, substantial food and beverage processing sector, and growing pharmaceutical manufacturing industry whose membrane-based process technology adoption is progressively aligning with international GMP standards.

Market Dynamics

Growth Drivers: Intensifying global water scarcity driving municipal and industrial water treatment infrastructure investment

The hollow fiber membranes market's exceptional growth rate is powered by the convergence of a physical resource scarcity imperative and a biopharmaceutical technology transition. Water scarcity, whose economic consequence is a documented 6% GDP growth reduction in affected regions, creates government investment in water treatment infrastructure whose membrane content per plant is growing with tightening effluent quality standards. The biopharmaceutical industry's transition from reusable stainless steel to single-use membrane systems creates a recurring consumable demand stream whose growth scales with biologics manufacturing capacity additions that the global pipeline's progression from development to commercialization is generating at historically unprecedented rates.

Restraints: High initial capital cost of hollow fiber membrane systems and membrane fouling management complexity create adoption barriers in price-sensitive markets

The capital cost of hollow fiber membrane filtration systems, whose membrane module procurement, pressure vessel housing, pumping infrastructure, and control system integration collectively represent investments ranging from hundreds of thousands to tens of millions of dollars per installation depending on treatment capacity, creates procurement barriers in developing market municipal applications where public water utility financing capacity may be insufficient without concessional financing support from development finance institutions. Membrane fouling, the progressive deposition of organic matter, scaling precipitates, microbial biofilm, and suspended particles on membrane surfaces that reduces permeate flux and increases transmembrane pressure over operational time, requires systematic management through chemical cleaning cycles whose frequency, chemical consumption, and membrane integrity monitoring add operational complexity.

Opportunities: PFAS removal regulatory mandates and gas separation applications for the hydrogen economy represent transformative new commercial frontiers

The EPA's PFAS National Primary Drinking Water Regulation finalized in 2024 creates mandatory treatment obligations affecting over 66,000 U.S. public water systems whose combined capital investment requirement of USD 1.5 to USD 3.0 billion annually represents one of the largest single regulatory drivers of environmental infrastructure investment in U.S. history. Hollow fiber nano-filtration and reverse osmosis membranes achieving the required PFAS rejection are positioned as preferred treatment technologies whose multi-year adoption will create sustained hollow fiber membrane demand. Gas separation hollow fiber membranes for hydrogen purification from electrolysis and steam methane reforming represent an emerging high-value application growing with the hydrogen economy's infrastructure development.

Recent Developments:

-

2025: Koch Membrane Systems launched its TARGA HF high-flux hollow fiber ultrafiltration module series with next-generation polysulfone chemistry delivering 35% higher clean water flux and 40% lower specific energy consumption versus the previous generation, substantially improving municipal and industrial water treatment economics.

-

2024: Toray Industries expanded its hollow fiber membrane manufacturing capacity in China through a new production facility investment targeting the growing Asia Pacific municipal water treatment and industrial process water markets, increasing Toray's regional production capability for its TORAYFIL and ROMEMBRA hollow fiber membrane product lines.

-

2023: Arkema, Polymem, and Tergys announced a strategic partnership to develop autonomous solar-powered hollow fiber membrane filtration systems for drinking water supply in remote and water-stressed communities, combining specialty polymer membrane materials with energy-self-sufficient system design for decentralized deployment.

Hollow Fiber Membranes Market Key Players are:

-

Asahi Kasei Corporation

-

Toray Industries, Inc.

-

Koch Separation Solutions

-

DuPont Water Solutions

-

Hydranautics

-

Pentair plc

-

Veolia Water Technologies

-

Mitsubishi Chemical Group

-

SUEZ Water Technologies & Solutions

-

Merck KGaA

-

Repligen Corporation

-

Danaher Corporation

-

3M Company

-

Pall Corporation

-

Toyobo Co., Ltd.

-

Microdyn-Nadir GmbH

-

Synder Filtration, Inc.

-

Membrana GmbH

-

W. L. Gore & Associates, Inc.

-

LG Chem Ltd.

Hollow Fiber Membranes Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.24 Billion |

| Market Size by 2035 | USD 11.51 Billion |

| CAGR | CAGR of 14.85% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Filtration Type (Microfiltration, Ultrafiltration, Nanofiltration, Reverse Osmosis) • By Membrane Material (Polymer, Ceramic) • By End-Use Industry (Water & Wastewater Treatment, Food & Beverages, Biotechnology, Pharmaceuticals & Chemicals, Medical Devices & Dialysis, Gas Separation, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Asahi Kasei Corporation, Toray Industries, Inc., Koch Separation Solutions, DuPont Water Solutions, Hydranautics, Pentair plc, Veolia Water Technologies, Mitsubishi Chemical Group, SUEZ Water Technologies & Solutions, Merck KGaA, Repligen Corporation, Danaher Corporation, 3M Company, Pall Corporation, Toyobo Co., Ltd., Microdyn-Nadir GmbH, Synder Filtration, Inc., Membrana GmbH, W. L. Gore & Associates, Inc., and LG Chem Ltd. |

Frequently Asked Questions

The hollow fiber membranes market is expected to grow at a CAGR of 14.85% from 2026 to 2035.

The hollow fiber membranes market was valued at USD 3.24 Billion in 2025.

Rising global water treatment investments, growing adoption of single-use bioprocessing technologies, increasing PFAS and water quality regulations, expanding municipal and industrial filtration demand, and advancements in anti-fouling membrane technologies are driving the hollow fiber membranes market.

The water & wastewater treatment segment dominated the hollow fiber membranes market in 2025.

Asia Pacific dominated the hollow fiber membranes market in 2025, holding the largest regional share.

Get in Touch