Board-to-Board Connectors Market Report Scope & Overview:

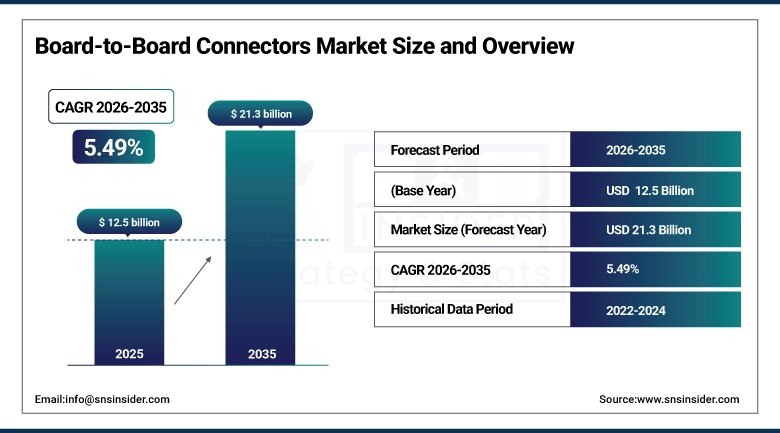

The Board-to-Board Connectors Market was valued at USD 12.5 billion in 2025 and is expected to reach USD 21.3 billion by 2035, growing at a CAGR of 5.49% from 2026–2035.

The Board-to-Board Connectors Market is witnessing a steady and broad-based growth trajectory on account of the increasing need for miniaturized, high-density, and high-speed interconnects in electrical systems for connecting printed circuit boards. The board-to-board connector acts as a fundamental component that provides inter-PCB connectivity, thus allowing for a modular design approach to electronic systems, whereby different modules are independently developed and assembled together into an integrated system.

Board-to-Board Connectors Market Size and Forecast

-

Market Size in 2025: USD 12.5 Billion

-

Market Size by 2035: USD 21.3 Billion

-

CAGR: 5.49% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Board-to-Board Connectors Market - Request Free Sample Report

Board-to-Board Connectors Market Trends

-

Accelerating miniaturization of consumer electronics driving adoption of sub-0.3 mm pitch board-to-board connectors in smartphones, wearables, and compact IoT devices.

-

Growing integration of board-to-board connectors in automotive electronics as EV adoption and ADAS deployment increase per-vehicle electronic content.

-

Rising demand for high-speed board-to-board connectors supporting data rates above 56 Gbps for AI computing, 5G base stations, and data center applications.

-

Increasing adoption of sustainable, RoHS-compliant connector materials and designs responding to ESG requirements across global electronics supply chains.

-

Growing use of vertical board-to-board connectors enabling higher component density in space-constrained industrial and medical electronic assemblies.

-

Rising demand for socket-type board-to-board connectors in telecom and industrial applications requiring modular, serviceable electronic architectures.

-

Expanding deployment of board-to-board connectors in advanced medical devices including wearable health monitors, implantable electronics, and hospital equipment.

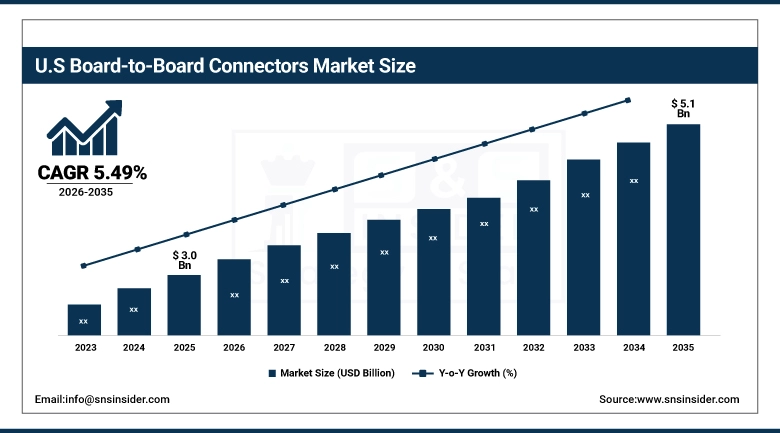

U.S. Board-to-Board Connectors Market was valued at USD 3.0 billion in 2025 and is expected to reach USD 5.1 billion by 2035, registering a CAGR of 5.49% during 2026–2035.

The U.S. Board-to-Board Connectors Market is driven by the country’s leadership in advanced semiconductor and electronics design, the strong presence of leading connector manufacturers including TE Connectivity, Amphenol, and Molex, and robust demand from automotive electronics, aerospace and defense, healthcare technology, and high-performance computing sectors. The CHIPS and Science Act-catalyzed domestic semiconductor manufacturing expansion is creating new demand for specialized board-to-board connectors in advanced chip packaging and semiconductor test systems.

Board-to-Board Connectors Market Segment Insights

-

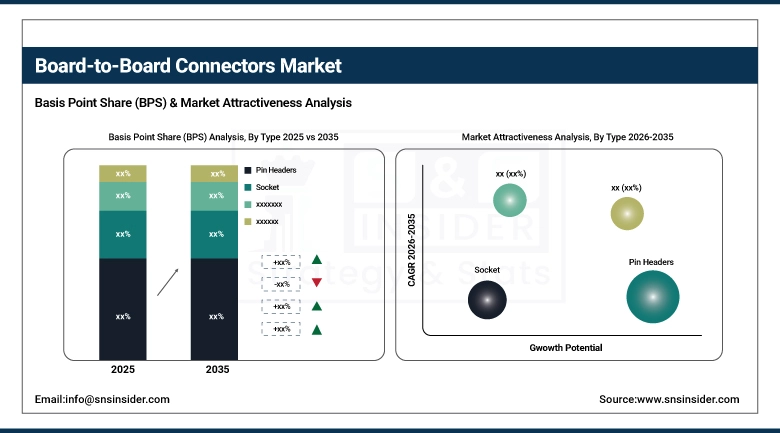

By Type, Pin Headers accounted for the largest market share ~59.8% in 2025; Socket Connectors expected to be the fastest-growing segment (CAGR).

-

By Component, 1 mm to 2 mm segment accounted for the largest market share ~48.7% in 2025; Above 2 mm expected to be the fastest-growing segment (CAGR).

-

By End User, Consumer Electronics accounted for the largest market share ~31.5% in 2025; Automotive expected to be the fastest-growing segment (CAGR).

Board-to-Board Connectors Market Segment Analysis

By Type, Pin Headers dominate, Socket Connectors expected to grow fastest

The Pin Header dominated the largest share with an estimate of approximately 59.8% of the market value in 2025, thanks to its universal application in almost all electronic assemblies, low-cost production, compact size, and easy mounting on PCBs. The pin header serves as the standard board-to-board connection for the mass-market consumer electronics and industrial electronics products that account for a large portion of connector usage globally. Pin headers can be available in a variety of pitches, number of pins, and orientations, making them the most flexible board-to-board connector.

Socket Connectors will record the fastest Compound Annual Growth Rate (CAGR) over the forecast period ending 2035 due to rising demand for more modular, upgradeable, and serviceable electronic architecture in telecommunications infrastructure, industrial automation, and defense electronics applications. Socket Connectors provide removable connections between PCBs, thus making it possible to replace, upgrade, or test the components separately without disturbing others in the system.

By Component, 1 mm to 2 mm segment dominates the market, Above 2 mm segment expected to grow fastest.

The 1 mm – 2 mm segment held the largest market share in 2025 because of its widespread use in automotive, electronics, industrial machinery, and manufacturing industries. This size provides a perfect combination of durability, flexibility, lightweight, and cost-effectiveness that is appropriate for precise operations. The manufacturers prefer such components because of their efficiency in terms of standard manufacturing and assembly processes, which helped the segment gain leadership across various end-user segments.

The Above 2 mm segment was projected to witness the highest growth rate because of the rising demand for heavy duty, strong, and durable components for construction, aerospace, transportation, and energy applications. Thick materials have a greater load-bearing capacity and ensure better operational stability and reliability for long periods. Fast infrastructure expansion, industrialization, and investments in modern engineering projects will boost the uptake of above 2 mm materials in the coming years.

By End User, Consumer Electronics leads, Automotive expected to grow fastest

Consumer electronics applications accounted for the highest share in the B2B connectors market at around 31.5%, which can be attributed to the large number of devices such as smartphones, tablets, laptops, wearable tech, and smart home devices that have multiple B2B connectors for establishing connection between the main printed circuit board and other devices such as display, camera, battery, antenna, and other additional boards. The constant need for upgrading consumer electronic products is leading to the continual development of connectors.

The Automotive segment is expected to register the highest CAGR from 2026 to 2035, driven by the transformational increase in electronic content per vehicle associated with EV powertrain electrification, ADAS sensor integration, and in-vehicle infotainment system expansion. Modern electric vehicles contain substantially more inter-PCB connectivity than conventional internal combustion engine vehicles, with battery management systems, motor control units, inverters, and ADAS domain controllers each requiring multiple high-reliability board-to-board connections. The growing adoption of centralized domain and zonal vehicle electrical architectures is further increasing the number and performance requirements of automotive board-to-board connectors.

Board-to-Board Connectors Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

74% |

|

Europe |

Germany |

30% |

|

Asia Pacific |

China |

52% |

|

Middle East & Africa |

UAE |

36% |

|

Latin America |

Brazil |

48% |

Asia Pacific Board-to-Board Connectors Market Insights

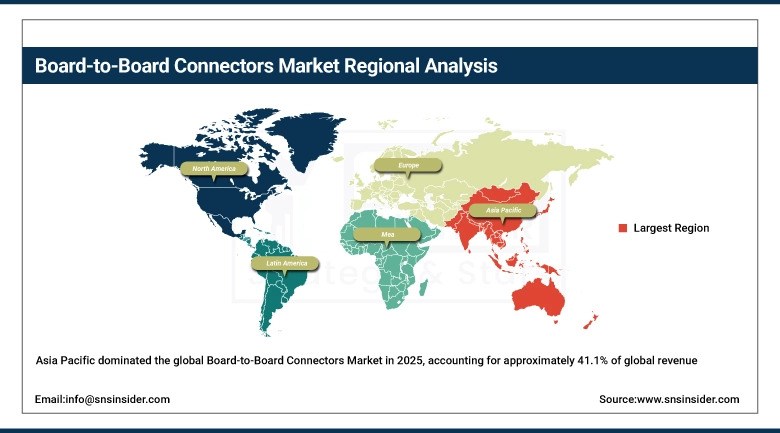

Asia Pacific dominated the global Board-to-Board Connectors Market in 2025, accounting for approximately 41.1% of global revenue. The region’s dominance reflects its overwhelming concentration of global electronics manufacturing in China, Japan, South Korea, and Taiwan, where the world’s largest smartphone, tablet, computer, automotive electronics, and industrial equipment production facilities create the highest global volumes of board-to-board connector demand. China’s EV manufacturing boom and consumer electronics production scale are particularly significant demand drivers for board-to-board connector volume.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Board-to-Board Connectors Market Insights

North America maintained a significant Board-to-Board Connectors Market position in 2025, anchored by the U.S.’ strong position as a global connector technology development and manufacturing hub. Leading connector manufacturers including TE Connectivity, Amphenol, Molex, and Samtec are headquartered or have major R&D operations in North America, with strong demand from aerospace and defense, medical technology, high-performance computing, and automotive electronics. The expanding domestic semiconductor manufacturing base and growing EV production capacity are creating new sources of domestic connector demand.

Europe Board-to-Board Connectors Market Insights

Europe maintained a meaningful share of the global Board-to-Board Connectors Market in 2025, driven by the region’s strong automotive electronics industry, advanced industrial automation sector, and leading aerospace and medical device manufacturers. Germany’s automotive OEMs and Tier-1 suppliers represent the most significant demand concentration, with growing EV platform development driving the evolution of automotive-grade board-to-board connector specifications toward higher operating temperature ranges, enhanced vibration resistance, and improved EMI shielding characteristics.

Middle East & Africa and Latin America Board-to-Board Connectors Market Insights

The Middle East & Africa and Latin America Board-to-Board Connectors Markets represent emerging growth opportunities aligned with regional electronics manufacturing development, industrial automation adoption, and infrastructure modernization. Gulf Cooperation Council nations are investing in technology manufacturing zones and electronics assembly facilities that create demand for connector components. Latin America’s growing automotive assembly industry and expanding electronics manufacturing base are creating consistent regional connector demand growth.

Board-to-Board Connectors Market Growth Drivers:

-

Increasing electronics density and automotive electrification driving board-to-board connector demand

The primary growth driver for the Board-to-Board Connectors Market is the relentless increase in electronic system complexity and functional density across all end-use industries, requiring ever-more sophisticated inter-PCB connectivity solutions capable of handling higher data rates, denser contact arrangements, and more challenging operating environments. The automotive industry’s rapid electrification is creating the most significant incremental board-to-board connector demand growth, as EVs contain substantially more electronic content than conventional vehicles and require automotive-grade connectors with enhanced environmental resistance. The expansion of 5G infrastructure, AI computing, and data center capacity is simultaneously driving demand for high-speed board-to-board connectors in telecommunications and computing applications.

Board-to-Board Connectors Market Restraints

-

Miniaturization limits and signal integrity challenges at advanced pitch sizes constraining design flexibility

A significant restraint on Board-to-Board Connectors Market growth is the fundamental physical and manufacturing challenges associated with sub-0.3 mm pitch connector production, including the precision assembly requirements, contact reliability risks, and signal integrity challenges that become increasingly severe as pitch sizes decrease. Ultra-miniature connectors require highly controlled manufacturing environments, specialized assembly equipment, and rigorous quality verification processes that add cost and limit production yield. Signal integrity degradation at high data rates through traditional connector metallurgy is also constraining adoption in the most demanding high-speed computing and telecommunications applications.

Board-to-Board Connectors Market Opportunities

-

EV electronics expansion and next-generation AI computing creating high-performance connector demand

The convergence of EV adoption driving exponential growth in automotive electronics content and AI computing deployment demanding ultra-high-bandwidth inter-board connectivity represents a dual transformative opportunity for the Board-to-Board Connectors Market. Automotive-grade connector platforms optimized for EV power electronics, battery management, and ADAS applications command premium pricing and require advanced engineering capabilities that create meaningful competitive differentiation. Simultaneously, the development of specialized high-speed board-to-board connectors for GPU-dense AI training servers, high-bandwidth memory (HBM) stacking, and optical compute interconnects represents a high-growth adjacent market opportunity for connector manufacturers willing to invest in next-generation signal integrity engineering.

Recent Developments:

-

2026: TE Connectivity launched a new generation of automotive-grade board-to-board connectors with enhanced operating temperature ranges of -40°C to +125°C and improved vibration resistance specifically designed for EV battery management and power electronics applications. Amphenol introduced ultra-high-speed board-to-board connector systems supporting 112 Gbps PAM-4 signaling for next-generation AI server and networking switch applications.

-

2024 (December): Hirose Electric launched the FH79 Series 0.3 mm pitch FPC connector for automotive applications, featuring high heat resistance and compact design optimized for advanced LiDAR, camera module connectivity, and ADAS sensor fusion systems, addressing the growing demand for miniaturized, high-reliability automotive-grade interconnects.

-

2024 (December): Yamaichi Electronics introduced the CN214 Series interface connector compatible with 1.6 Tbps Ethernet for next-generation optical communication modules, establishing a new performance benchmark for ultra-high-speed board-to-board connectivity in data center and telecommunications switching infrastructure applications.

Key Players

Some of the Board-to-Board Connectors Market Companies

-

TE Connectivity

-

Amphenol Corporation

-

Molex

-

Hirose Electric Co. Ltd.

-

Japan Aviation Electronics Industry (JAE)

-

Samtec

-

Kyocera Corporation

-

HARTING Technology Group

-

Foxconn Interconnect Technology (FIT)

-

JST Mfg. Co. Ltd.

-

ERNI Electronics

-

Delphi Technologies

-

YAMAICHI Electronics

-

Advanced Interconnect

-

CSCONN Corporation

-

Omron Corporation

-

Fujitsu Components Limited

-

ITT Cannon

-

Phoenix Contact

-

Würth Elektronik

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.5 Billion |

| Market Size by 2035 | USD 21.3 Billion |

| CAGR | CAGR of 5.49% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Pin Headers, Socket) • By Component (Less than 1mm, 1mm to 2mm, Greater than 2mm) • By End User (Consumer Electronics, Industrial Automation, Telecommunication, Automotive, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | TE Connectivity, Amphenol Corporation, Molex, Hirose Electric Co. Ltd., Japan Aviation Electronics Industry (JAE), Samtec, Kyocera Corporation, HARTING Technology Group, Foxconn Interconnect Technology (FIT), JST Mfg. Co. Ltd., ERNI Electronics, Delphi Technologies, YAMAICHI Electronics, Advanced Interconnect, CSCONN Corporation, Omron Corporation, Fujitsu Components Limited, ITT Cannon, Phoenix Contact, Würth Elektronik |

Frequently Asked Questions

Asia Pacific dominated the Board-to-Board Connectors Market in 2025, accounting for approximately 41.1% of global revenue, driven by the region’s concentration of global electronics and automotive electronics manufacturing.

The Consumer Electronics segment dominated the Board-to-Board Connectors Market in 2025, accounting for approximately 31.5% of global revenue, while the Automotive segment is expected to register the highest CAGR through 2035.

Increasing electronics density and automotive electrification driving inter-PCB connectivity demand, combined with growing requirements for high-speed data transmission in AI computing and 5G telecommunications infrastructure.

The Board-to-Board Connectors Market was valued at USD 12.5 billion in 2025.

The Board-to-Board Connectors Market is expected to grow at a CAGR of 5.49% from 2026 to 2035.

Get in Touch