Printed Circuit Board Market Report Scope & Overview:

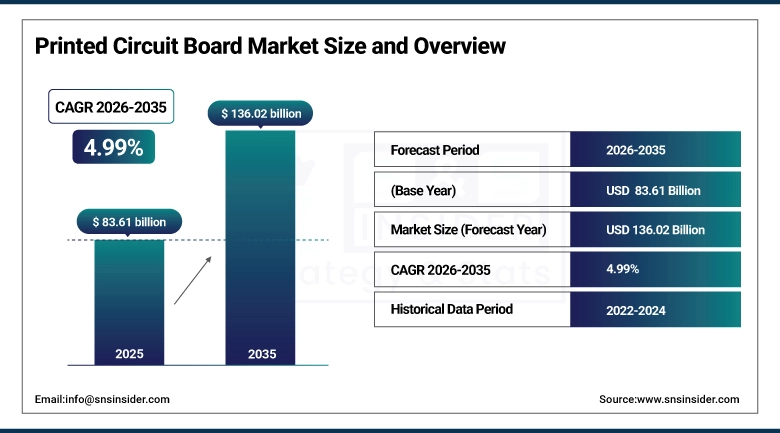

The Printed Circuit Board Market size was valued at USD 83.61 billion in 2025 and is expected to reach USD 136.02 billion by 2035, growing at a CAGR of 4.99% from 2026–2035.

Printed Circuit Boards (PCBs) are crucial electronic components that physically hold and electrically link electronic components by providing conductive paths through copper traces and laminated substrates. The application of PCBs is widespread in many industries such as consumer electronics, automotive, telecommunication, industrial automation, medical, aerospace & defense, and data center due to their capability to integrate circuits in a compact manner. Some common types of PCBs include single-layer, double-layer, multi-layer, flex, rigid-flex, and high-density interconnect (HDI). Growing demand for compact-sized electronic devices, fast-paced development of 5G network, growing production of electric vehicles, and increasing deployment of artificial intelligence-based computer systems are some key factors driving the market. In addition, increased utilization of Internet of Things (IoT) devices, cloud computing platforms, advanced driver assistance systems (ADAS), and semiconductor packaging technology is further boosting the global PCB market.

Multilayer printed circuit boards accounted for the largest share of the global Printed Circuit Board Market in 2024, accounting for about 54.2% of the overall market revenue due to their wide range of applications in smartphones, servers, networking devices, automotive components, and industrial automation equipment. The increasing popularity of multilayer printed circuit boards will continue in 2025 and 2026 owing to their high circuit density, small physical size, outstanding electrical properties, and suitability for complex electronic designs. The rising investment by governments and technology firms in AI servers, 5G base stations, electric vehicles, and high-performance computing infrastructure in 2025 and 2026 is expected to further boost segment dominance.

Printed Circuit Board Market Size and Forecast

-

Market Size in 2025: USD 83.61 Billion

-

Market Size by 2035: USD 136.02 Billion

-

CAGR: 4.99% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Printed Circuit Board Market - Request Free Sample Report

Printed Circuit Board Market Trends

-

There is a fast increase in the development of AI servers, cloud computing solutions, and hyperscale data centers, which is creating a greater need for high-quality multi-layer PCBs and HDI PCBs.

-

The manufacture of electric cars, driverless car technology, and automotive electronics is increasing the uptake of automotive PCBs.

-

The establishment of 5G infrastructure, IoT components, and edge computing solutions is encouraging the adoption of high-speed and high-performance PCB products.

-

The reduction in size of consumer electronics and wearable technology is increasing the uptake of flexible and rigid-flexible PCBs.

-

Intelligent PCB testing and manufacturing using AI and other technologies is improving manufacturing efficiency and product quality management systems.

-

Investments in semiconductor packaging and PCB substrate technologies are creating more demand for advanced PCBs in 2025 and 2026.

-

A greater focus on sustainable production and halogen-free PCB substrates is enabling the creation of sustainable green PCB manufacturing systems.

U.S. Printed Circuit Board Market Size Outlook:

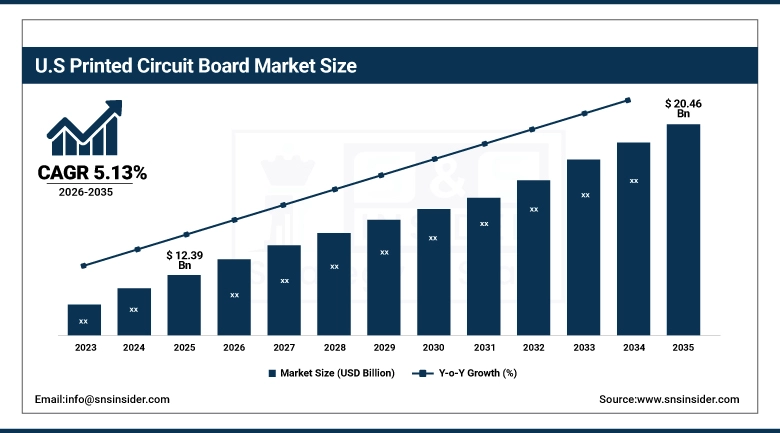

The U.S Printed Circuit Board Market was valued at USD 12.39 billion in 2025 and is expected to reach USD 20.46 billion by 2035, at a CAGR of 5.13% from 2026 to 2035. Some of the primary growth drivers of the U.S. Printed Circuit Board Market include increased investment in the production of semiconductors, increase in AI infrastructure, growth in electric vehicle production, and increase in the need for advanced electronics in defense, telecommunications, health care, and industrial automation industries. The increased adoption of multilayer PCBs, HDI PCBs, flexible circuits, and substrate-like PCBs for use in data centers, autonomous cars, consumer electronics, and 5G network equipment will be playing a key role in market growth. The government's initiatives under the CHIPS and Science Act, coupled with growing investments in domestic electronics manufacturing in 2025 and 2026, will be adding to PCB production capabilities.

Investments in AI servers, cloud computing infrastructure, and aerospace & defense electronics are expected to create additional avenues of revenues for PCB manufacturers in the U.S. market. Rising investments in high-speed computing solutions, advanced semiconductor packaging, and future generation network infrastructure is expected to increase PCB manufacturing capacity and capabilities by these companies to meet the rising demand. Some of the prominent U.S. companies that include TTM Technologies, AdvancedPCB, and Sanmina Corporation are focusing on increasing investments in PCBs and other circuit boards.

Printed Circuit Board Market Segment Insights

-

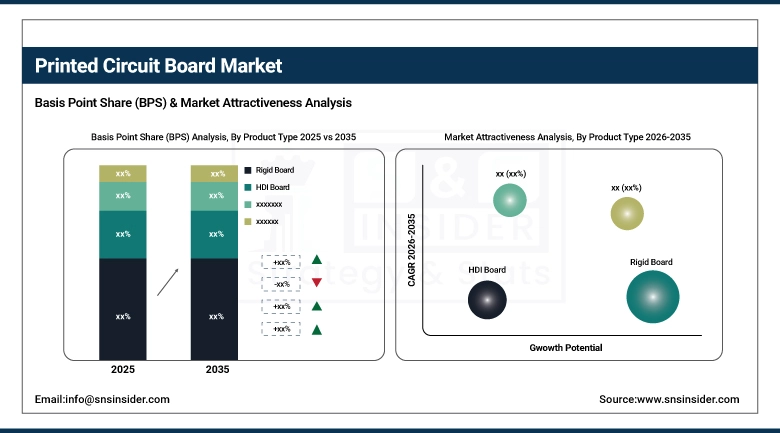

Based on Product Type, Rigid Board dominated the Printed Circuit Board Market in 2025 with around 40% market share.

-

Based on Application, Consumer Electronics held the largest market share, around 38%, in 2025.

By Product Type: Rigid Board (Largest Share), High-Density Interconnect (HDI) Board (Fastest Growing)

Rigid Board was the major segment within the Printed Circuit Board market in 2025, driven by its massive applications in consumer electronics, industrial machinery, telecommunications, automotive electronics, and computing devices. Rigid PCBs possess characteristics such as high durability, mechanical strength, cost efficiency, and high electrical performance. As a result, rigid PCBs dominate the Printed Circuit Board market and are the most commonly used PCB technology for mass-scale electronic manufacturing. Rigid PCBs have wide applications ranging from smartphones, laptops, television sets, servers, networking devices, and various control systems. Increasing demand for artificial intelligence-based computing systems, development of 5G networks, and manufacturing of hardware in data centers within North America and Asia Pacific regions contribute to the growing dominance of rigid boards.

The High-Density Interconnect (HDI) Board market will have the highest CAGR during the forecast period due to growing requirements for smaller, lighter, and faster electronic products. The HDI PCB allows for more compact circuits and improved signal integrity and lower power usage; hence, it is suitable for use in smartphone manufacturing, wearable electronics, automobiles, aircraft systems, and high-performance computing. The increasing application of AI servers, ADAS, IoT, and communication technologies is boosting the demand for HDI PCBs.

By Application: Consumer Electronics (Largest Share), Automotive (Fastest Growing)

Consumer Electronics was the most dominant segment in the Printed Circuit Board Market in 2025 due to increased manufacturing of smartphones, tablets, laptops, gaming consoles, television sets, and other wearable electronic products around the world. PCBs are considered the primary components of modern-day consumer electronics because they allow efficient and effective circuit integration, high-speed processing, and enhanced connectivity features. Increased global consumption of smart devices, artificial intelligence-enabled electronics, and other advanced consumer technologies is helping in the continuous growth of the segment. High investments in semiconductor integration, miniaturization of electronic parts, and computing devices in Asia Pacific and North America regions are boosting the market growth in consumer electronics manufacturing.

The Automotive segment is likely to witness the highest growth rate during the forecast period on account of growing manufacturing of electric vehicles, adoption of autonomous driving technology, and quick adoption of advanced electronics in cars. Automotive PCBs are extensively used in the manufacturing of batteries, battery management system, infotainment system, ADAS platform, sensors, electric drive trains, and vehicle-to-vehicle communication solutions. High investment in EV manufacturing, intelligent mobility solutions, and software-defined cars during 2025 and 2026 are boosting demand for reliable and highly durable automotive PCBs.

Printed Circuit Board Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

79% |

|

Europe |

Germany |

26% |

|

Asia Pacific |

Australia |

43% |

|

Middle East & Africa |

South Africa |

32% |

|

Latin America |

Brazil |

51% |

North America Printed Circuit Board Market Insights:

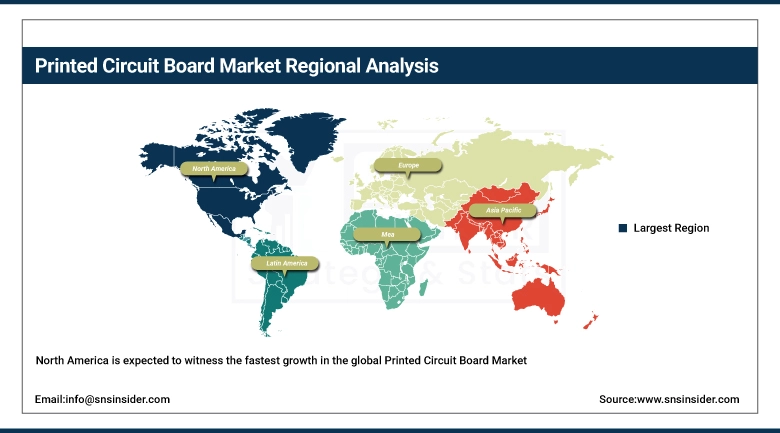

North America is expected to witness the fastest growth in the global Printed Circuit Board Market owing to rising investments in semiconductor manufacturing, increasing AI infrastructure deployment, and growing demand for advanced electronics across the United States and Canada. The United States dominates the regional market due to strong presence of aerospace & defense electronics manufacturers, cloud computing companies, automotive technology developers, and high-performance computing infrastructure providers. Growing investments under the CHIPS and Science Act during 2025 and 2026 are accelerating domestic PCB production and advanced semiconductor packaging capabilities. Increasing deployment of AI servers, data centers, electric vehicles, defense communication systems, and 5G networking infrastructure is further strengthening regional market growth. Rising focus on supply chain localization and high-reliability PCB manufacturing for military and industrial applications is also creating strong future growth opportunities across North America.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Printed Circuit Board Market Insights:

Europe maintains a significant position in the global Printed Circuit Board Market owing to the region’s strong automotive manufacturing industry, industrial automation infrastructure, and increasing investments in advanced electronics production. Germany, France, the UK, Italy, and the Netherlands are major regional markets driven by high demand for automotive PCBs, industrial control systems, medical electronics, and renewable energy applications. The region’s transition toward electric mobility and Industry 4.0 manufacturing is accelerating adoption of high-performance multilayer and HDI PCBs. Germany remains the leading market due to its dominant automotive electronics sector and growing semiconductor manufacturing initiatives. Increasing investments in EV charging infrastructure, smart factories, and advanced industrial robotics during 2025 and 2026 are further supporting PCB demand across Europe.

Asia Pacific Printed Circuit Board Market Insights:

Asia Pacific dominated the global Printed Circuit Board Market in 2025 owing to the region’s large-scale electronics manufacturing ecosystem, rapid semiconductor production expansion, and strong presence of consumer electronics and telecommunications industries across China, Japan, South Korea, Taiwan, and Southeast Asia. China continues to lead the regional market due to its massive electronics manufacturing base, strong PCB supply chain infrastructure, and growing investments in AI computing, EV production, and 5G deployment. Taiwan, South Korea, and Japan also play critical roles in advanced PCB manufacturing and semiconductor packaging technologies. Rising production of smartphones, laptops, automotive electronics, and data center hardware is significantly driving PCB demand throughout the region. Increasing investments in substrate-like PCBs, HDI boards, and advanced packaging technologies during 2025 and 2026 are further strengthening Asia Pacific’s market dominance.

Middle East & Africa Printed Circuit Board Market Insights:

The Middle East & Africa Printed Circuit Board Market is witnessing gradual growth supported by increasing investments in telecommunications infrastructure, industrial automation, renewable energy systems, and smart city development projects across the UAE, Saudi Arabia, and South Africa. Demand for PCBs is rising across industrial electronics, energy management systems, automotive applications, and consumer electronics assembly operations within the region. UAE and Saudi Arabia are leading regional adoption owing to growing investments in digital infrastructure, AI-enabled technologies, and industrial modernization programs. Expansion of electric infrastructure projects, cloud computing facilities, and smart manufacturing initiatives is expected to support long-term PCB demand across the region.

Latin America Printed Circuit Board Market Insights:

Latin America is emerging as a developing market for Printed Circuit Boards owing to growing electronics manufacturing activities, increasing automotive production, and rising adoption of industrial automation technologies across Brazil, Mexico, Argentina, and Chile. Brazil remains the dominant regional market supported by strong automotive manufacturing operations, consumer electronics demand, and industrial equipment production. Mexico is also witnessing increasing PCB demand due to expansion of electronics assembly facilities and automotive component manufacturing under nearshoring trends linked to North American supply chains. Growing investments in telecommunications infrastructure, renewable energy systems, and connected industrial technologies during 2025 and 2026 are expected to further support market growth across Latin America.

Market Growth Drivers: Rising demand for AI infrastructure, electric vehicles, and advanced consumer electronics driving PCB market growth

The fast-growing trend in artificial intelligence enabled computing, hyperscale data centers, electric cars, 5G technology, and consumer electronics has been majorly contributing to the growing global demand for advanced Printed Circuit Boards. Printed Circuit Boards play a key role in several applications including smartphones, computers, industrial automation equipment, automotive electronics, medical devices, and telecom gear because of their capability to enable dense, high speed, and compact electronic configurations. Investments being made in semiconductor fabrication plants, package assembly houses, and cloud infrastructure in North America, Europe, and Asia Pacific markets in 2025 and 2026 will continue to boost demand for PCBs.

Market Restraints: High manufacturing costs and semiconductor supply chain volatility limiting market expansion

The cost of producing PCBs is also high due to the use of highly sophisticated substrate material, copper lamination technology, and semi-conductor integration process. Volatility in the prices of raw materials used in the PCB manufacture such as copper foils, glass fibers, special resin and semiconductors can greatly affect the cost-effectiveness of manufacturing the product. The difficulties involved in the fabrication of PCBs, specifically those that are HDI boards, substrate like PCBs, and flexible circuits also pose significant production problems to manufacturers.

Market Opportunities: AI computing, advanced packaging, and EV electronics creating future growth opportunities

The fast-paced development of artificial intelligence servers, supercomputers, electric mobility systems, and advanced communication technology is resulting in significant prospects for companies producing innovative printed circuit boards around the world. The increased need for substrate-like PCBs, HDI PCBs, flexible PCBs, and high-frequency PCBs in AI accelerators, self-driving cars, and 5G network equipment is projected to contribute to future growth in the market. In addition, the growing investments in semiconductor packaging solutions, chiplet solutions, and electronics miniaturization processes are contributing to innovations within the industry.

Recent Developments

-

2026: TTM Technologies announced expansion of advanced PCB manufacturing capabilities in North America to support growing demand from aerospace, defense, AI infrastructure, and high-performance computing applications.

-

2025: AT&S Austria Technologie & Systemtechnik AG expanded production of high-end substrate-like PCBs and advanced packaging substrates to address increasing semiconductor and AI server demand across Asia Pacific and Europe.

Printed Circuit Board (PCB) Companies are:

• Zhen Ding Technology

• DSBJ

• Nippon Mektron

• Compeq

• Tripod Technology

• SCC

• Ibiden

• Hannstar Board

• AT&S

• Rhyming Technology

• Sanmina Corporation

• Wurth Elektronik Group

• Becker & Muller Schaltungsdruck GmbH

• Advanced Circuits Inc.

• Sumitomo Corporation

• Murrietta Circuits

• Shennan Circuits Co., Ltd.

• Meiko Electronics Co., Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 83.61 Billion |

| Market Size by 2035 | USD 136.02 Billion |

| CAGR | CAGR of 4.99% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Rigid Board (Single Layer Board, Double Layer Board, Others (Multilayer)), HDI Board, Flexible Board, Others) • By Application (Automotive, Consumer Electronics, Telecommunication, Healthcare, Energy & Power, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Zhen Ding Technology, Unimicron Technology, DSBJ, Nippon Mektron, Compeq, Tripod Technology, TTM Technologies, SCC, Ibiden, Hannstar Board, AT&S, Rhyming Technology, Sanmina Corporation, Wurth Elektronik Group, Becker & Muller Schaltungsdruck GmbH, Advanced Circuits Inc., Sumitomo Corporation, Murrietta Circuits, Shennan Circuits Co., Ltd., Meiko Electronics Co., Ltd. |

Frequently Asked Questions

Asia Pacific leads the Printed Circuit Board Market, owing to the strong manufacturing capabilities of the region, particularly in China, Japan, South Korea, and Taiwan, which are leading producers of PCBs.

Automotive is growing fastest, driven by greater integration of advanced electronic systems into vehicles.

Rigid Board dominates with over 40% market share.

The Printed Circuit Board Market was valued at USD 83.61 billion in 2025.

The Printed Circuit Board Market is expected to grow at a CAGR of 4.99% from 2026 to 2035.

Get in Touch