Border Security Technologies Market Report Scope & Overview:

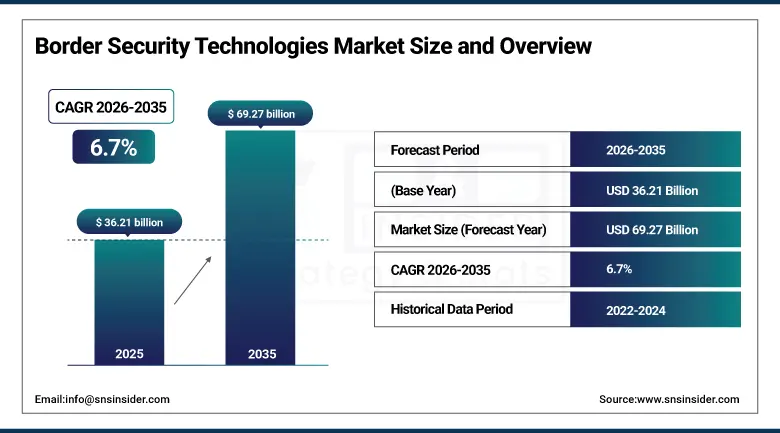

The Border Security Technologies Market was valued at USD 36.21 billion in 2025 and is expected to reach USD 69.27 billion by 2035, growing at a CAGR of 6.7% from 2026-2035

Market growth within border security technologies is increasing rapidly because of the backing received from the defense agencies on issues regarding national security, migration, and terrorism at border crossings. The real-time surveillance and detection of threats in land, air, and water borders has increased significantly with the implementation of artificial intelligence, unmanned aerial vehicles, biometrics, radar technology, and thermal imaging technology. There have been several innovations in smart borders through the process of digital transformation within the border security industry due to the advancements brought about by the need for sophisticated solutions from the defense sector through public-private collaboration. The year 2023 saw over 200 cyberattacks aimed at energy infrastructures while in the same period, the utility sector suffered around 1,728 attacks per week.

As per statistics in the industry, the surveillance technology segment occupied about 34.53% of the border security technologies market share in 2025, with radar systems, night vision cameras, thermal cameras, and biometrics being the basic component of border intelligence, although unmanned technologies are forecast to grow at the highest rate of 9.80%, owing to the increasing significance of drones and robots in border monitoring applications.

Market Size and Forecast

• Market Size in 2025: USD 36.21 Billion

• Market Size by 2035: USD 69.27 Billion

• CAGR: 6.7% from 2026 to 2035

• Base Year: 2025

• Forecast Period: 2026-2035

• Historical Data: 2022-2024

To Get more information on Border Security Technologies Market - Request Free Sample Report

Border Security Technologies Market Trends

• Rapid integration of AI and machine learning into border surveillance platforms enabling real-time behavioral pattern recognition, predictive threat detection, anomaly flagging, and automated alert generation across vast border perimeters.

• Growing deployment of autonomous UAV and UGV systems for 24/7 border patrol in remote, dangerous, and environmentally challenging terrain where manned surveillance is costly, dangerous, or logistically impractical.

• Increasing adoption of biometric identification systems including facial recognition, iris scanning, and fingerprint identification at border checkpoints, ports of entry, and airport terminals for rapid, accurate identity verification.

• Rising investment in integrated command and control platforms that aggregate data from multiple border surveillance systems — including satellite imagery, radar, UAV feeds, and sensor networks — into a single operational intelligence picture.

• The rising implementation of smart border management solutions including the use of X-rays on vehicles, cargo scanning, and artificial intelligence for risk assessment in order to optimize trade corridor management.

• The growing creation of maritime domain awareness solutions featuring radar on naval ships, Automatic Identification System for vessel tracking, autonomous vessels, and submarine sonar in order to monitor the borders effectively.

• The rising expenditure on border cybersecurity solutions that will protect the critical information systems used by border management agencies from sophisticated cyber attacks from rival states.

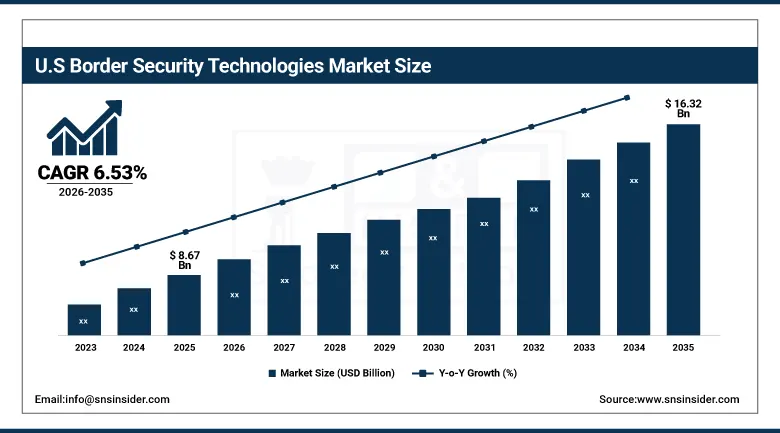

U.S. Border Security Technologies Market was valued at USD 8.67 billion in 2025 and is expected to reach USD 16.32 billion by 2035, registering a CAGR of 6.53% during 2026-2035.

The United States is the leader in the global market and continues to remain at the top because of large international borders, huge expenditure on defense, and the early use of modern surveillance and detection technologies. Key drivers behind this are increasing rates of illegal immigration, smuggling of drugs, weapons, and other security-related issues that require smart border technology. There have been substantial investments made by the U.S. government on AI systems, UAVs, drones, biometrics, and cameras equipped with AI. Recently, in February 2024, the United States DHS signed a deal worth USD 450 million with Anduril industries.

Lockheed Martin previewed its 2025 AI-enhanced surveillance platform featuring real-time threat detection, advanced radar integration, and autonomous monitoring capabilities for complex border environments — while Raytheon launched next-generation thermal drones and integrated border monitoring systems reflecting the accelerating premium technology investment driving the U.S. border security market.

Border Security Technologies Market Segment Insights

-

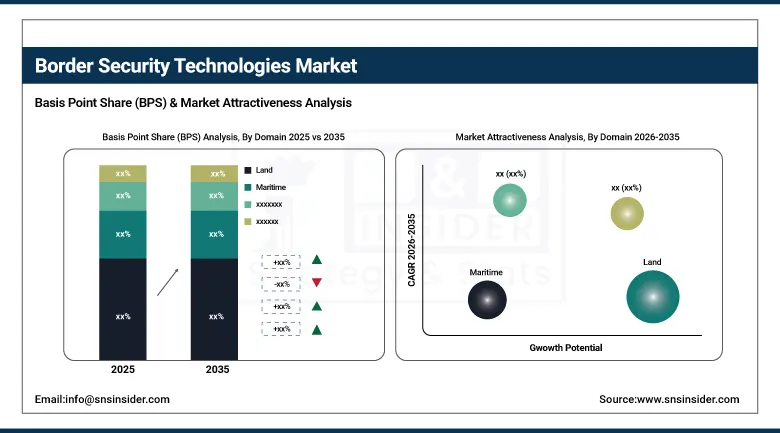

Based on Domain, Land accounted for the largest market share (~66.67%) in 2025; Maritime expected to be the fastest-growing segment (CAGR of 8.96%).

-

Based on System, Surveillance Systems accounted for the largest market share (~34.53%) in 2025; Unmanned Systems expected to be the fastest-growing segment (CAGR of 9.80%).

-

Based on End-User, Military accounted for the largest market share (~52.4%) in 2025; Homeland Security expected to be the fastest-growing segment (CAGR of 8.25%).

Border Security Technologies Market Segment Analysis

By Domain, Land dominates, Maritime expected to grow fastest

The land domain captured the largest revenue share of approximately 66.67% in 2025, driven by the vast scale of global land borders and the growing threats of illegal crossings, smuggling, and terrorism. The scope of land border security includes security surveillance cameras, radar, physical barriers, unmanned aerial vehicle patrols, ground sensors, and biometric controls spread over thousands of kilometers of perimeter security on land. It is the volume and number of applications of land border security on such a massive scale that helps maintain its large market share.

Maritime sector has been expected to hold the fastest CAGR of 8.96% during 2026-2035 because of increasing threats around the coast and rising need for maritime security services. Governments are spending on modern technology like smart buoys, naval radars, unmanned surface vehicles, and satellite based maritime domain awareness solutions to regulate illegal trafficking and unauthorized activities at sea. Thales and BAE Systems have extended their range of maritime surveillance solutions to meet growing demands of naval defense organizations across the globe.

By System, Surveillance Systems dominate, Unmanned Systems expected to grow fastest

In terms of market share by revenue, surveillance systems held the highest percentage of about 34.53% in 2025. These include radar systems, night vision cameras, thermal imaging devices, acoustic sensors, and biometric scanners which together constitute the basis of intelligence gathering in modern border security infrastructure. The increasing emphasis on real-time situation assessment and threat prediction is resulting in more funding for advanced AI-based surveillance technologies with greater coverage areas per capita.

Unmanned systems are expected to have the highest CAGR of 9.80%, owing to the increasing significance of unmanned aerial vehicles (UAVs), unmanned ground vehicles (UGVs), and unmanned surface vehicles (USVs) as critical means for efficient border surveillance during all hours of the day on tough terrains. The attributes of endurance, flexible payloads, and less risk of operation make unmanned solutions a top choice for border surveillance, emergency support, and intelligence gathering operations.

By End-User, Military dominates, Homeland Security expected to grow fastest

The military category accounted for about 52.4% of the total revenue share in 2025 due to the application of sophisticated drones, radars, and command-and-control centers in the military's defense of its national border security through the deployment of unmanned aerial vehicles. The military is at the forefront of developing some of the most sophisticated border monitoring solutions, which utilize all domains.

The homeland security market is anticipated to have the highest CAGR of 8.25% because of rising focus on civil border security, immigration, and anti-terrorism activities. Homeland security government bodies have adopted smart border solutions such as behavioral screening using artificial intelligence, vehicle examination systems, biometric identity management, and intelligence information sharing to fight border challenges from multiple fronts.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

41% |

|

Europe |

Germany |

30% |

|

Asia Pacific |

China |

43% |

|

Middle East & Africa |

Saudi Arabia |

35% |

|

Latin America |

Brazil |

44% |

North America Border Security Technologies Market Insights

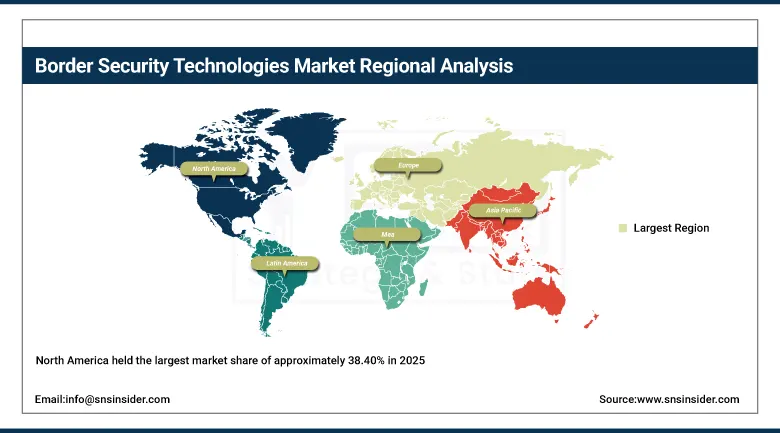

North America held the largest market share of approximately 38.40% in 2025, driven by high defense spending, advanced technological infrastructure, and ongoing cross-border security challenges. The U.S. DHS and CBP are the primary procurement drivers, continuously investing in next-generation UAV systems, AI-powered surveillance, biometric entry-exit systems, and integrated border management infrastructure across its extensive international borders.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Border Security Technologies Market Insights

The Asia Pacific region is projected to grow at the highest CAGR of 8.86% between 2026 and 2035 owing to rising geopolitical tensions, border modernization efforts in China, India, South Korea, and Japan, and large borders on both land and water that are highly vulnerable to cross-border illegal activities. Large-scale investments for border security in India and border surveillance modernization in China fuel high regional growth.

Europe Border Security Technologies Market Insights

The continent is experiencing robust expansion due to migratory pressures, geopolitical issues like the Russia-Ukraine crisis, and the EU’s smart borders program encompassing ETIAS and the Schengen Border Code. The EU-Africa Sahel Shield Initiative introduced a USD 1.8 billion fund for AI drones and biometric checkpoints in countries within the Sahel region in March 2025. Germany is at the forefront, investing in border management systems and surveillance technology.

Middle East & Africa and Latin America Border Security Technologies Market Insights

The market for border security technologies in the Middle East region is expanding due to large investments by GCC countries in defense budgets towards intelligent border technologies, maritime domain awareness, and advanced surveillance technologies for securing energy infrastructures. Latin America is witnessing increasing investments in border security technologies owing to drug trafficking threats and criminal activities along borders.

Border Security Technologies Market Growth Drivers:

Rising cross-border security threats and increasing adoption of AI-driven surveillance technologies accelerating market growth: The market is witnessing strong growth in 2025 due to increasing concerns related to illegal immigration, terrorism, drug trafficking, human smuggling, and cross-border criminal activities. There has been considerable growth in investments made by governments globally in sophisticated border security infrastructure, command-and-control mechanisms, and defense technologies that would help them enhance their national security capacity.

Increasing usage of artificial intelligence, biometrics, unmanned aerial vehicles, thermal imagery, radars, and predictive threat analysis has helped transform border security from merely being a defensive process into an intelligent one. Apart from this, increasing global defense expenditure, along with modernization initiatives undertaken by countries, are leading to an enhanced deployment of smart border management solutions incorporating cyber-physical security, situational awareness, and intelligent threat detection technologies.

Border Security Technologies Market Restraints:

High deployment costs, privacy concerns, and interoperability challenges limiting large-scale adoption: The following represents a number of problems that the market will face during 2025 owing to the high cost of implementing, integrating, and maintaining surveillance technology and border security monitoring technologies. The introduction of AI-powered analysis, biometrics identification, unmanned aerial vehicles, radars, and control-and-command systems will require considerable government funding.

Moreover, increasing problems relating to data privacy, biometrics surveillance, and civil rights issues are also posing obstacles in regard to the use of border monitoring techniques on a large scale. In many cases, difficulties are also faced with regard to the integration of the old system of border monitoring and new AI-based surveillance systems owing to their non-interoperability. Such issues have kept several advanced border security solutions from being adopted in many regions around the globe.

Border Security Technologies Market Opportunities

Expanding maritime security investments and autonomous surveillance adoption creating new growth opportunities: The market is expected to witness significant growth opportunities through 2035 due to rising investments in maritime border protection, autonomous surveillance infrastructure, and advanced biometric verification systems. In this regard, governments are increasingly using drone aircraft equipped with artificial intelligence, autonomous surveillance systems, thermal cameras, and smart surveillance towers to enhance border security on land, coasts, and seas.

There is also an increasing trend of using biometric identification tools at airports, port authorities, and immigration stations. Furthermore, ongoing modernization efforts by armed forces of countries in Asia-Pacific and the Middle East are leading to greater procurement of innovative border surveillance, cybersecurity, and command-and-control platforms. This bodes well for the future growth prospects of border security solutions suppliers globally.

Recent Developments:

-

2026: Anduril Industries expanded deployment of its AI-enabled Lattice surveillance and command platform for border monitoring, autonomous threat detection, and counter-drone operations across U.S. defense and homeland security programs.

-

2026: Palantir Technologies strengthened its role in border and homeland security through expanded AI-powered analytics, biometric identification, and real-time intelligence management contracts with U.S. government agencies.

-

2026: The U.S. Department of Homeland Security initiated advanced autonomous drone and 5G surveillance trials along the U.S.-Canada border to improve reconnaissance, ISR operations, and cross-border situational awareness capabilities.

Border Security Technologies Market Key Players

• Lockheed Martin Corporation

• Raytheon Technologies

• Northrop Grumman Corporation

• BAE Systems plc

• Thales Group

• Leonardo S.p.A.

• Elbit Systems Ltd.

• Airbus SE

• General Dynamics Corporation

• L3Harris Technologies

• Teledyne FLIR

• DRS Technologies

• Anduril Industries

• Palantir Technologies

• QinetiQ Group plc

• ASIS Guard

• Leidos Holdings, Inc.

• SAIC

• Bosch Security Systems

• Honeywell International Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 36.21 Billion |

| Market Size by 2035 | USD 69.27 Billion |

| CAGR | CAGR of 6.7% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Domain (Land, Maritime, Aerial) • By System (Surveillance Systems, Unmanned Systems, Biometric Systems, Radar Systems, Command & Control, Others) • By End-User (Military, Homeland Security) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, Raytheon Technologies, Northrop Grumman Corporation, BAE Systems plc, Thales Group, Leonardo S.p.A., Elbit Systems Ltd., Airbus SE, General Dynamics Corporation, L3Harris Technologies, Teledyne FLIR, DRS Technologies, Anduril Industries, Palantir Technologies, QinetiQ Group plc, ASIS Guard, Leidos Holdings, Inc., SAIC, Bosch Security Systems, Honeywell International Inc. |

Frequently Asked Questions

North America dominated the market in 2025, accounting for approximately 38.40% of global market revenue, driven by high defense spending and persistent cross-border security challenges requiring continuous investment in surveillance and detection systems.

The Surveillance Systems segment dominated the market in 2025 with approximately 34.53% revenue share, encompassing radar networks, thermal cameras, biometric scanners, and night vision systems.

The Land domain segment dominated the market in 2025 with approximately 66.67% revenue share, driven by the massive scale of global land border surveillance requirements.

The integration of AI and autonomous systems enhancing real-time border surveillance and threat detection — combined with growing geopolitical tensions, rising cross-border threats from terrorism and trafficking, and government investments in smart border modernization programs — is the primary driver of sustained market growth through 2035.

The market was valued at USD 36.21 billion in 2025.

The market is expected to grow at a CAGR of 6.7% from 2026 to 2035.

Get in Touch