Brachytherapy Market Report Scope & Overview:

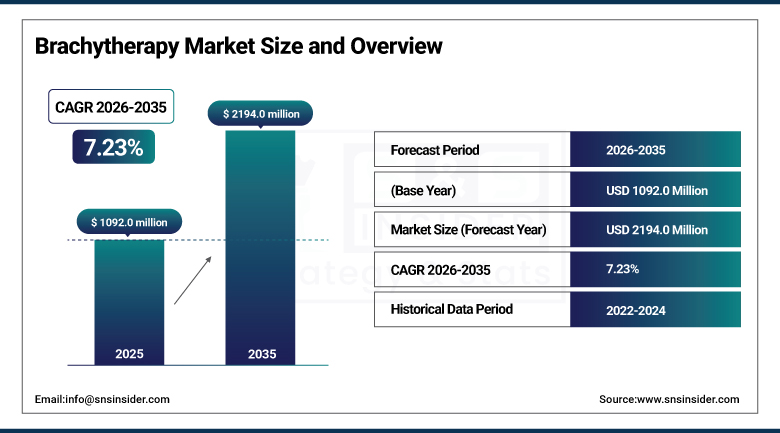

The Brachytherapy Market size was USD 1,092.0 Million in 2025 and is expected to reach USD 2,194.0 Million by 2035, growing at a CAGR of 7.23% from 2026–2035.

The brachytherapy market is growing at a stable pace due to factors such as the rise in the burden of cancer across the globe, advances made in radiation oncology, and increasing availability of minimally invasive techniques for treating cancer. The market is marked by the growing adoption of HDR and LDR brachytherapy procedures for various cancers such as prostate, breast, cervical, and others, owing to advancements in terms of improved efficacy, patient outcomes, and hospitalization rates. Increased spending on infrastructure development for oncology treatments, supportive reimbursement scenarios in advanced economies, and increasing awareness about targeted radiation therapy solutions are adding to the momentum of the market.

In December 2023, Perspective Therapeutics, earlier known as Isoray, sold its brachytherapy business, along with its radioactive Cesium-131 seeds, to GT Medical Technologies. This allowed Perspective Therapeutics to shift its focus on other therapy segments, while GT Medical Technologies can develop its brachytherapy products further. These three significant events in 2023 and 2024 have collectively formed the trends of consolidation, collaboration, and specialization in the brachytherapy industry.

Market Size and Forecast

-

Market Size in 2026E: USD 1,171 Million

-

Market Size by 2035: USD 2,194 Million

-

CAGR: 7.23% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Brachytherapy Market - Request Free Sample Report

Brachytherapy Market Trends

-

Electronic brachytherapy is gaining adoption for superficial skin cancers and non-melanoma indications as a lower-cost alternative.

-

Real-time imaging guidance integration with brachytherapy applicators is improving procedural precision across all indications.

-

Outpatient HDR brachytherapy protocols are reducing hospital stays and improving patient experience for prostate and breast cancers.

-

AI-driven treatment planning software is reducing planning time and improving dose optimization for brachytherapy procedures.

-

Emerging market oncology center expansion is creating new brachytherapy equipment procurement demand across Asia Pacific.

-

Research into non-oncological brachytherapy applications including cardiac arrhythmias and keloid scars is broadening addressable indications.

The U.S. Brachytherapy Market Outlook

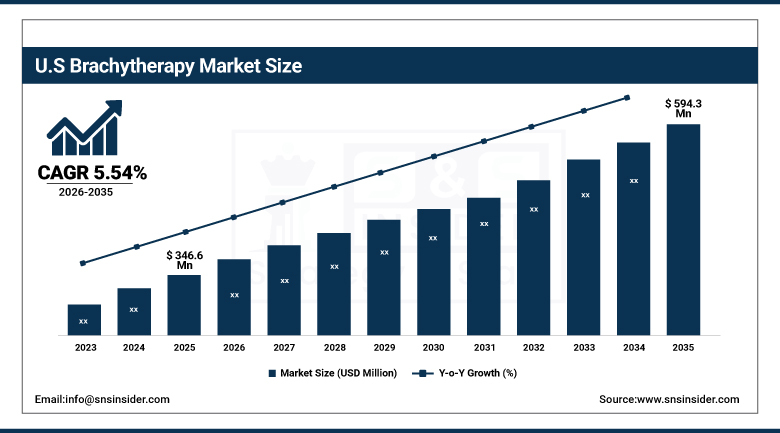

The U.S. Brachytherapy Market was valued at approximately USD 346.6 Million in 2025. It is expected to reach approximately USD 594.3 Million by 2035, growing at a CAGR of approximately 5.54%.

In North America brachytherapy market, the United States has maintained a leadership role due to its sophisticated oncology infrastructure, adoption of HDR and LDR methods, and its sharp emphasis on cancer detection and treatment at an early stage. In addition to this, the country’s favorable reimbursement policies and investment in radiotherapy technologies have ensured its leadership position in the market. The NCCN guidelines continue to strongly recommend the use of brachytherapy for prostate, cervical, and early stage breast cancers.

In October 2023, Elekta announced its agreement with iCAD Inc.'s acquisition of Xoft to get its Xoft Axxent Electronic Brachytherapy (eBx) System so that Elekta could expand its range of cancer therapy offerings through electronic brachytherapy to treat breast cancer, non-melanoma skin cancer, and gynecological cancer. In September 2024, Varian, which is a Siemens Healthineers Company, forged a strategic alliance with Sun Nuclear to develop quality assurance solutions using the Sun Nuclear's SunCHECK quality management system and Varian's radiotherapy systems.

Brachytherapy Market Segment Analysis

-

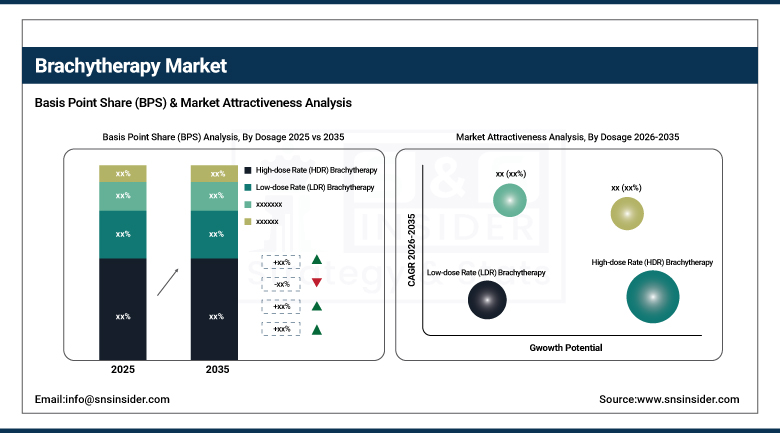

By Dosage, the high-dose rate (HDR) brachytherapy segment dominated the brachytherapy market with approximately 73.40% share in 2025. Low-Dose Rate (LDR) Brachytherapy represents the other key dosage category, primarily used in permanent prostate seed implants.

-

By Product, the Applicators & Afterloaders segment dominated the brachytherapy market with approximately 45.20% share in 2025. Seeds and electronic brachytherapy represent meaningful alternative product categories and is fastest growing.

-

By Application, the prostate cancer segment dominated the brachytherapy market with approximately 33.15% share in 2025. The breast cancer segment is expected to register the fastest growth, at an explicit CAGR of approximately 7.73%.

By Dosage, HDR dominates on clinical efficiency and precision

High Dose Rate (HDR) Brachytherapy has taken lead in terms of dosage with about 73.40% market share in 2025 due to high efficiency of treatment, which allows providing high doses of radiation within short time spans in outpatients clinics. HDR brachytherapy is characterized by reduction of hospital stays and increased patient convenience. It allows for great precision since the radiation dose is delivered to tumors in a more accurate way and healthy tissues are not affected, thus reducing the number of side effects and increasing safety of treatment. Wide treatment scope (prostate, cervical and breast cancers), along with high effectiveness and affordability of the therapy made it popular choice of medical professionals.

Low Dose Rate (LDR) Brachytherapy is the fastest growing and consists mainly of prostate seed implants using Iodine-125 or Palladium-103 sources. It allows providing continuous low level radiation for several weeks instead of high-intensity fractionated doses. Permanent seed implant is the standard treatment for certain cases of localized prostate cancer patients with low and medium risks. Due to its safety and efficacy of this procedure, it is considered as an established standard in treatment of low-risk prostate cancer.

By Product, applicators & afterloaders dominate on precision delivery

Applicators & Afterloaders held the dominant position in terms of market share in the product category in 2025 with an estimate of 45.20%. The importance of the function served by these companies in delivering radiation precisely to cancer cells without harming the healthy tissues around them contributes significantly to their dominance in the market. Applicators help in placing radioactive substances near or in the tumor to ensure a minimally invasive process for better comfort for the patients and reduced recovery time. The Afterloader ensures that the radiation is delivered to the desired location with the use of HDR brachytherapy.

Seeds represent a meaningful alternative product category, particularly for LDR prostate brachytherapy using Iodine-125 (I-125) and Palladium-103 (Pd-103) permanent implants. Electronic Brachytherapy (eBx) represents a growing alternative product segment, using miniaturized X-ray tubes rather than radioactive isotopes, reducing radiation safety requirements and potentially lowering infrastructure costs. As outpatient brachytherapy keeps expanding and electronic systems gain FDA clearances for new indications, the electronic brachytherapy segment should keep growing within the overall product mix.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Brachytherapy Market Insights

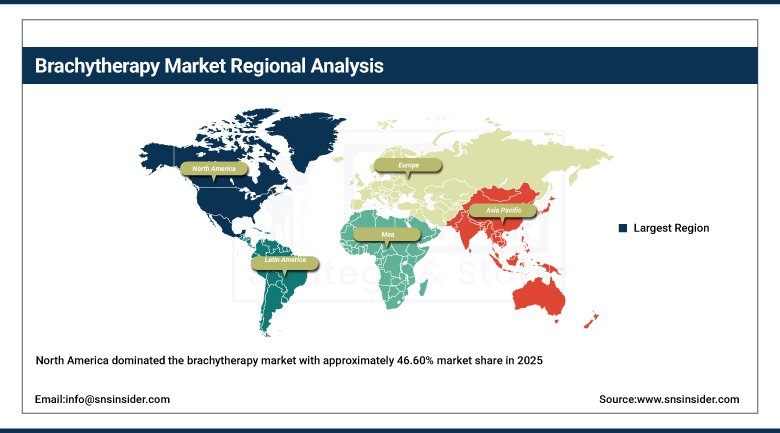

North America dominated the brachytherapy market with approximately 46.60% market share in 2025. Its established healthcare infrastructure, early adoption of innovative radiotherapy technologies, and high incidence of cancer cases most notably prostate and breast cancers drive this leadership. The region is favored by huge government and private investments in cancer research and supportive reimbursement policies that enable access to brachytherapy treatments. The presence of key market participants, strategic acquisitions, and intense clinical study activity contribute to the region's dominance across multiple brachytherapy modalities.

The United States accounts for approximately 82.5% of North American revenue. NCCN guideline endorsement of brachytherapy for key indications and favorable Medicare/Medicaid reimbursement for both HDR and LDR procedures keep reinforcing domestic market leadership. This combination of clinical guidelines, reimbursement support, and oncology infrastructure keeps North America firmly in the lead.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Brachytherapy Market Insights

Europe represents a meaningful brachytherapy market, supported by well-established radiation oncology infrastructure and strong national cancer screening programs. Germany leads the regional market, backed by strong academic medical centers and radiation oncology investment. France and the UK contribute meaningful demand through their own extensive cancer treatment networks.

Germany accounts for approximately 24.6% of European revenue. European Society for Radiotherapy & Oncology (ESTRO) clinical guidelines continue endorsing brachytherapy for cervical, prostate, and breast cancer indications across the region. This guideline support should keep reinforcing steady European brachytherapy demand.

Asia Pacific Brachytherapy Market Insights

Asia Pacific is expected to be the fastest-growing brachytherapy market with approximately 7.95% CAGR through the forecast period. Rising cancer incidence, growing healthcare infrastructure, and higher awareness of radiotherapy options drive this expansion. China, India, and Japan are experiencing rapid growth of oncology centers and state-sponsored programs promoting increased accessibility for cancer treatment. Increasing demand for affordable therapies, rising medical tourism, and expansion by global players into emerging markets are driving penetration of brachytherapy in the region.

China accounts for approximately 40.6% of Asia Pacific revenue. India's rapidly growing oncology center network and improving training and technical knowledge are also contributing meaningfully. As regional oncology investment keeps expanding and brachytherapy awareness grows, this growth trajectory should continue strengthening.

MEA & Latin America Brachytherapy Market Insights

The UAE leads MEA revenue, growing cancer incidence and improving oncology infrastructure both support regional brachytherapy adoption. Saudi Arabia is also investing in radiation oncology capacity as part of broader healthcare modernization.

Brazil leads Latin American revenue, expanding oncology center networks and growing cancer incidence drive regional brachytherapy demand. Mexico and Argentina contribute secondary demand through their own expanding cancer care infrastructure.

Market Dynamics

Growth Drivers: Rising global cancer burden boosting demand for localized radiotherapy

The increasing global incidences of various types of cancers, especially of prostate, breast, cervical, and skin cancers, continue to fuel interest in various targeted and less invasive treatments, such as brachytherapy. According to GLOBOCAN 2023, there were 20 million new cases of cancer reported around the world, with the most common cancers being prostate and breast cancers. Brachytherapy provides radiation that is very localized without affecting the surrounding tissues, thus making it suitable for cancers located in sensitive areas.

With high-dose rate brachytherapy increasingly becoming the preferred procedure carried out in an outpatient setting, the experience of patients has been significantly improved, and there have been few cases of hospital admissions. Improvements, such as real-time image guidance and applicators, have increased accuracy and success of the procedure. Electronic brachytherapy devices are embracing the concept of personalized treatment of cancer, which is efficient and less damaging to organs.

Restraints: Limited availability of skilled professionals and infrastructure

One of the major obstacle hindering the expansion of brachytherapy technology is the inadequacy of professionals who would be able to carry out brachytherapy procedures accurately. Unlike radiotherapy, brachytherapy consists of a rather complicated process of planning and source insertion and demands adherence to safety protocols that require highly skilled professionals. It should be noted that most hospitals, especially those located in low- and middle-income countries, lack the infrastructure for conducting brachytherapy procedures, such as HDR afterloaders and real-time imaging systems.

According to the International Atomic Energy Agency (IAEA) report from 2023, more than 70% of low-income countries do not possess any dedicated brachytherapy facilities. This obstacle leads to significant shortages of therapy opportunities for patients who could benefit from brachytherapy because its clinical efficacy is proven to be very high.

Opportunities: Expansion of brachytherapy beyond oncology

Although brachytherapy has traditionally been utilized in the treatment of diseases such as prostate, cervical, and breast cancers, recent studies have opened up new possibilities through the use of brachytherapy for non-cancerous disorders such as cardiac arrhythmias and keloid scarring. This widening of the scope of application allows for the inclusion of new patient groups and fields of therapy. Additionally, advancements in the field of electronic and image guided brachytherapy devices have increased accuracy of treatments.

The FDA has granted permission for the usage of brachytherapy electronic equipment in cases of superficial skin cancers and non-melanoma. The increasing acceptability of minimally invasive procedures has made the medical fraternity more receptive towards adopting brachytherapy for purposes other than cancer treatments.

Recent Developments:

-

2023: Elekta agreed in October 2023 to acquire iCAD Inc.'s Xoft business, including the Xoft Axxent Electronic Brachytherapy (eBx) System, strengthening Elekta's cancer treatment portfolio for breast, skin, and gynecological cancers.

-

2024: Varian (a Siemens Healthineers company) formed a strategic partnership with Sun Nuclear in September 2024 to integrate Sun Nuclear's SunCHECK quality management system with Varian's radiotherapy systems for improved brachytherapy quality assurance.

-

2023: Perspective Therapeutics (formerly Isoray) announced the sale of its Cesium-131 brachytherapy seed assets to GT Medical Technologies in December 2023, enabling GT Medical to further develop brachytherapy solutions while Perspective Therapeutics focused on alpha therapy.

Brachytherapy Market Key Players are:

-

Elekta AB

-

Varian Medical Systems, Inc.

-

Isoray Inc.

-

Becton, Dickinson and Company (BD)

-

Eckert & Ziegler BEBIG

-

CIVCO Radiotherapy

-

Boston Scientific Corporation

-

Theragenics Corporation

-

iCAD, Inc.

-

GT Medical Technologies

-

Huiheng Medical, Inc.

-

Panacea Medical Technologies Pvt. Ltd.

-

Sensus Healthcare, Inc.

-

Oncura, Inc.

-

Nucletron B.V. (An Elekta Company)

-

C4 Imaging LLC

-

Radiation Products Design, Inc.

-

BEBIG Medical GmbH

-

IsoAid LLC

-

K&S Associates, Inc.

Brachytherapy Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1,092.0 Million |

| Market Size by 2035 | USD 2,194.0 Million |

| CAGR | CAGR of 7.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Dosage (High-dose Rate (HDR) Brachytherapy, Low-dose Rate (LDR) Brachytherapy) • By Product (Seeds, Applicators & Afterloaders, Electronic Brachytherapy) • By Application (Prostate Cancer, Gynecological Cancer, Breast Cancer, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Elekta AB, Varian Medical Systems, Inc., Isoray Inc., Becton, Dickinson and Company (BD), Eckert & Ziegler BEBIG, CIVCO Radiotherapy, Boston Scientific Corporation, Theragenics Corporation, iCAD, Inc., GT Medical Technologies, Huiheng Medical, Inc., Panacea Medical Technologies Pvt. Ltd., Sensus Healthcare, Inc., Oncura, Inc., Nucletron B.V. (An Elekta Company), C4 Imaging LLC, Radiation Products Design, Inc., BEBIG Medical GmbH, IsoAid LLC, and K&S Associates, Inc. |

Frequently Asked Questions

The Brachytherapy Market is expected to grow at a CAGR of 7.23% from 2026 to 2035.

The Brachytherapy Market was valued at USD 1,092 Million in 2025.

The Prostate Cancer segment dominated with approximately 33.15% share in 2025.

North America dominated the Brachytherapy Market with approximately 46.60% revenue share in 2025.

Rising global cancer burden, increasing adoption of HDR brachytherapy in outpatient settings, and technological advances in delivery systems and treatment planning are the primary growth factors.

Get in Touch