Prostate Cancer Diagnostics Market Report Scope & Overview:

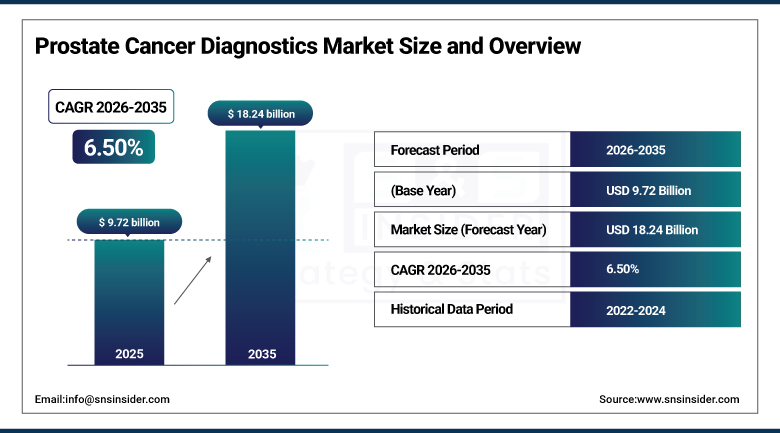

The Prostate Cancer Diagnostics Market was valued at USD 9.72 billion in 2025 and is expected to reach USD 18.24 billion by 2035, growing at a CAGR of 6.50% from 2026-2035.

The growth of the Prostate Cancer Diagnostics Market is fueled by the increasing incidence of prostate cancer and the rise in awareness regarding its early detection. The development of screening initiatives and the adoption of modern diagnostic techniques including molecular diagnostics and imaging techniques are contributing to the growth of the market. Moreover, the growing geriatric population, improved healthcare infrastructure, and increased funding for cancer research are propelling the growth of the market.

The World Cancer Research Fund reports over 1.4 million new prostate cancer cases diagnosed globally in 2023, making it the second most prevalent cancer in men. The American Cancer Society estimates that early detection of prostate cancer when it remains localized produces a 5-year relative survival rate exceeding 99%, creating strong clinical justification for prostate-specific diagnostic investment.

Prostate Cancer Diagnostics Market Size and Forecast

-

Market Size in 2025: USD 9.72 Billion

-

Market Size by 2035: USD 18.24 Billion

-

CAGR: 6.50% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Prostate Cancer Diagnostics Market - Request Free Sample Report

Prostate Cancer Diagnostics Market Trends

-

Rising prevalence of prostate cancer and increasing aging male population are driving the prostate cancer diagnostics market.

-

Growing demand for early detection and accurate screening methods is boosting market growth.

-

Expansion of healthcare infrastructure and awareness programs is fueling diagnostic adoption.

-

Increasing focus on non-invasive and minimally invasive testing methods is shaping adoption trends.

-

Advancements in biomarker-based tests, imaging technologies, and molecular diagnostics are enhancing accuracy and reliability.

-

Rising investments in oncology research and personalized medicine are supporting market expansion.

-

Collaborations between diagnostic companies, hospitals, and research institutions are accelerating innovation and global adoption.

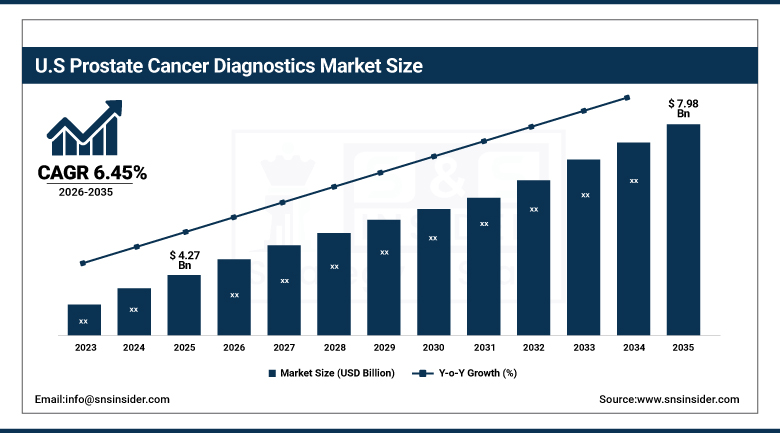

U.S. Prostate Cancer Diagnostics Market was valued at USD 4.27 billion in 2025 and is expected to reach USD 7.98 billion by 2035, growing at a CAGR of 6.45% from 2026-2035.

U.S. Prostate Cancer Diagnostics Market Growth is propelled by high prevalence rates of prostate cancer and a focus on early diagnosis and screening programs. The development of sophisticated healthcare facilities and the use of technologies like molecular diagnostics and imaging contribute to higher demand. Growing funding for cancer research and rising awareness levels are contributing to market expansion.

The American Urological Association's 2023 prostate cancer early detection guidelines recommend PSA screening discussion for men aged 40-54 at elevated risk and for all men aged 55-69, creating clinical practice framework that sustains U.S. PSA testing volumes. CMS has approved reimbursement for multiple prostate cancer genomic tests including Prolaris, Oncotype DX Genomic Prostate Score, and Decipher under Medicare Part B coverage for appropriate clinical indications.

Prostate Cancer Diagnostics Market Segment Analysis

-

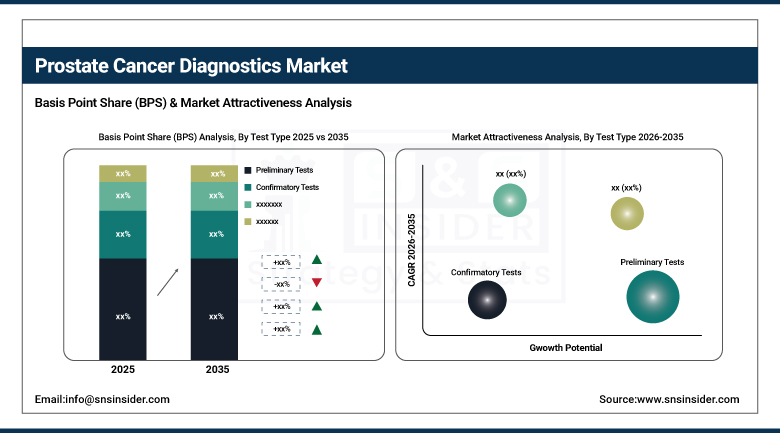

By Test Type, Preliminary Tests segment dominated the Prostate Cancer Diagnostics Market in 2025 with 61% share; Confirmatory Tests segment fastest growing (CAGR).

-

By Type, Adenocarcinoma segment dominated the Prostate Cancer Diagnostics Market in 2025 with 79% share; Interstitial Cell Carcinoma segment fastest growing (CAGR).

-

By End User, Hospitals segment dominated the Prostate Cancer Diagnostics Market in 2025 with 54% share; Outpatient Facilities segment fastest growing (CAGR).

By Test Type, Preliminary Tests segment dominates the Prostate Cancer Diagnostics Market, Confirmatory Tests segment expected to grow fastest.

Preliminary Tests held a dominant position in the Prostate Cancer Diagnostics Market in terms of maximum market revenue share of around 61% in 2025 owing to their extensive use in screening processes involving PSA tests and digital rectal examinations. They remain popular among healthcare organizations because of easy availability, affordability, and wide use in mass-screening programs.

Confirmatory Tests are projected to record a faster CAGR during the forecast period between 2026 and 2035 due to an increase in demands for further diagnoses following preliminary tests. There have been rising trends in using advanced imaging studies, biopsy techniques, and molecular diagnostics, which have gained popularity owing to technological advances and better disease characterization.

By Type, Adenocarcinoma segment dominates the Prostate Cancer Diagnostics Market, Interstitial Cell Carcinoma segment expected to grow fastest.

Adenocarcinoma segment captured the largest market share of Prostate Cancer Diagnostics in 2025 with almost 79%, being the most prevalent form of prostate cancer among people around the world. The rising cases and screenings for adenocarcinoma will increase the need for procedures aimed at diagnosing such condition, thus ensuring the steady use of diagnostics in hospitals, labs, and other medical facilities.

The Interstitial Cell Carcinoma segment will showcase the highest growth rate (CAGR) during 2026-2035. This is attributed to the rising awareness and advancements made regarding the diagnostic technologies, which have enabled clinicians and scientists to detect rarer forms of prostate cancer, including interstitial cell carcinoma.

By End User, Hospitals segment dominates the Prostate Cancer Diagnostics Market, Outpatient Facilities segment expected to grow fastest.

The hospitals segment was the leading market in terms of revenue, holding the largest share of around 54% in 2025 due to their role in providing cancer screening and diagnosis services. The presence of advanced diagnostic machinery and qualified healthcare staff makes the facility popular among the patients seeking prostate cancer tests, ensuring consistent revenue generation for the segment through regular patient inflow.

The outpatient facilities segment is anticipated to witness the fastest CAGR in the market from 2026 to 2035 owing to the rising popularity of economical and convenient diagnostic solutions. The growing acceptance of minimally invasive tests, reduced waiting time, and availability of specialized diagnostic centers are contributing to the adoption of the facility for conducting prostate cancer tests.

Prostate Cancer Diagnostics Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Europe |

Germany |

25% |

|

Asia Pacific |

Japan |

38% |

|

Middle East & Africa |

Saudi Arabia |

38% |

|

Latin America |

Brazil |

50% |

North America Prostate Cancer Diagnostics Market

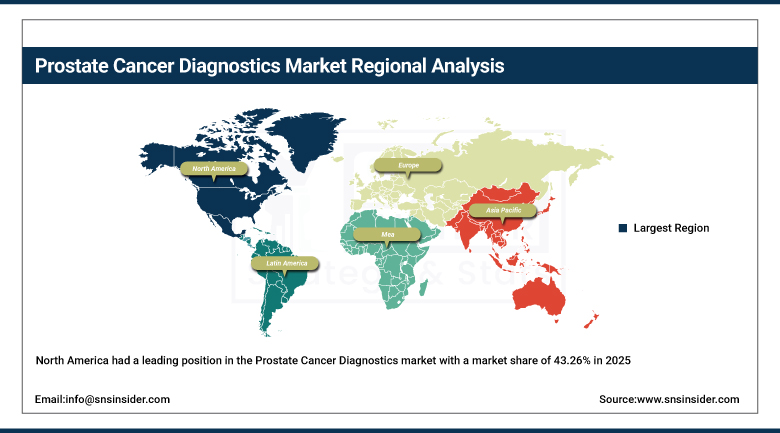

North America had a leading position in the Prostate Cancer Diagnostics market with a market share of 43.26% in 2025 due to its advanced healthcare facilities, increased levels of awareness, and quick adoption of innovative diagnostic methods. North America has the second highest number of reported cases of prostate cancer in the world. In 2023 alone, there were an estimated 288,300 prostate cancer patients in the United States according to the American Cancer Society. Further, the presence of prominent firms in the market such as Abbott Laboratories, Roche Diagnostics, and Siemens Healthineers promotes innovation and provision of advanced diagnostic techniques such as PSA tests, targeted MRI biopsies, and liquid biopsy tests.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Prostate Cancer Diagnostics Market

Asia Pacific will emerge as the fastest-growing market, registering a CAGR of 7.59% during the forecast period due to increasing incidences of cancer, rising expenditure on healthcare, and improved diagnostic infrastructure. The incidence rate of prostate cancer in Asia, according to WHO, is increasing due to increasing aged population, changes in lifestyle, and cancer screening programs. Countries like China, India, and Japan are seeing increasing use of PSA tests, biomarker diagnostics, and AI-driven imaging techniques. Increasing government initiatives to raise cancer awareness and screening programs, along with better access to healthcare, are adding to the growth potential. Additionally, increasing investments by foreign diagnostic companies and collaborations for clinical research are also boosting technology advancements.

Europe Prostate Cancer Diagnostics Market

Europe Prostate Cancer Diagnostics Market is influenced by rising incidences of prostate cancer and early detection efforts. Efficient screening and diagnosis facilities along with high awareness rate will fuel the uptake of tests. The area has good support of funds in health care sector as well as innovations like molecular diagnostics and imaging technology. Moreover, government support, growing aged populace, and continuous research activities in the field of oncology will boost market growth in European countries.

Middle East & Africa and Latin America Prostate Cancer Diagnostics Market

The Middle East & Africa and Latin America Prostate Cancer Diagnostics Market is growing at a steady pace due to increased awareness regarding prostate cancer as well as improvements in the availability of healthcare services. The construction of diagnostic centers, an increase in the number of initiatives taken by governments to detect cancer at an early stage, and investments in healthcare infrastructure are aiding in the adoption of diagnostics. Furthermore, urbanization along with the availability of good medical facilities is helping in early diagnosis.

Prostate Cancer Diagnostics Market Growth Drivers:

-

Rising prostate cancer prevalence and liquid biopsy innovation driving sustained global diagnostic market growth

The prostate cancer diagnostics market relies on a demographic platform that becomes stronger each year, in that more men are living long enough to be at the age when prostate cancer strikes, and the increasing elderly population around the world increases the at-risk population. Every man who reaches 55 years of age reaches the age where discussions about prostate cancer begin, and every man diagnosed with prostate cancer creates many additional diagnostic occasions initial screening, verification, staging, and follow-up monitoring. At the same time, liquid biopsy technology has created additional diagnostic opportunities that are not just for initial diagnosis monitoring response to hormone treatment, identifying resistance mutations which will indicate lack of response, and monitoring for biochemical recurrence following definitive therapy are examples of such applications.

The World Cancer Research Fund projects prostate cancer incidence will increase by 77% globally between 2020 and 2040 as the male population over 60 grows. The National Cancer Institute's SEER database documents a 1.5-2% annual increase in prostate cancer detection rates in the U.S. as PSA screening programs recover from the USPSTF's 2012 discouragement recommendation reversal.

Prostate Cancer Diagnostics Market Restraints:

-

High costs of advanced genomic and imaging tests limiting prostate cancer diagnostic access in cost-sensitive healthcare markets

High costs of sophisticated genomics and imaging tests continues to pose as a considerable limitation within the Prostate Cancer Diagnostics Market, especially in economically constrained healthcare settings. Molecular diagnostic techniques, MRI-based screening, and genetic testing are highly capital-intensive and necessitate the availability of advanced machinery, experienced personnel, and high-cost operations. Moreover, in most areas, insufficient financial incentives and poor health insurance coverage hinder the implementation of these tests by patients. Healthcare institutions with meager resources find it challenging to purchase expensive medical diagnostic equipment.

Prostate Cancer Diagnostics Market Opportunities:

-

AI-powered diagnostic integration and liquid biopsy innovation creating new prostate cancer diagnostic growth opportunities

The incorporation of AI into the diagnostic workflows for prostate cancer provides a real value add that is facilitating adoption as opposed to simply displacing current methods of analysis. AI pathology software solutions, which can provide standardized Gleason scoring and identify nuanced patterns within prostate biopsies that a human pathologist would potentially overlook, have been shown in clinical trials to enhance inter-reader agreement and identify clinically significant prostate cancer at higher rates in difficult cases. In prostate MRI image analysis, the use of AI is enabling community radiologists to attain PI-RADS levels of accuracy in their reporting, comparable to those achieved by specialized prostate radiologists.

Recent Developments:

-

2025: Myriad Genetics launched Precise MRD for prostate cancer monitoring, enabling detection of biochemical recurrence through circulating tumor DNA analysis at PSA levels below conventional PSA assay detection thresholds, providing earlier recurrence detection that allows more timely salvage therapy initiation.

-

2025: Exact Sciences received FDA clearance for its Oncotype DX GPS genomic prostate score test update incorporating a larger gene panel with improved prediction of 10-year metastasis risk, providing urologists and patients with stronger prognostic evidence for active surveillance versus immediate treatment decisions in low-to-intermediate risk prostate cancer.

-

2026: Lantheus Holdings launched PYLARIFY AI, an AI-powered automated quantitative analysis platform for its PSMA PET imaging agent, providing standardized prostate cancer staging measurement and treatment response assessment without the variability of manual nuclear medicine physician interpretation.

Prostate Cancer Diagnostics Market Key Players

Some of the Prostate Cancer Diagnostics Market Companies

-

Abbott Laboratories

-

Roche Holdings AG

-

Siemens Healthineers AG

-

Beckman Coulter Inc. (Danaher)

-

OPKO Health Inc.

-

MDxHealth SA

-

Myriad Genetics Inc.

-

GenomeDx Biosciences (Veracyte)

-

Genomic Health Inc. (Exact Sciences)

-

Lantheus Holdings Inc.

-

Hologic Inc.

-

bioMerieux SA

-

Qiagen NV

-

Illumina Inc.

-

BD Biosciences (Becton Dickinson)

-

Agilent Technologies Inc.

-

DiaSorin S.p.A.

-

Sysmex Corporation

-

Ortho Clinical Diagnostics

-

Fujirebio Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.72 billion |

| Market Size by 2035 | USD 18.24 billion |

| CAGR | CAGR of 6.50% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Test Type (Preliminary Tests, Confirmatory Tests) • By Type (Adenocarcinoma, Interstitial Cell Carcinoma, Other) • By End Use (Hospitals, Outpatient Facilities, Home Care, Research & Manufacturing) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories, Siemens Healthineers, Roche Diagnostics, Hologic, Inc., Myriad Genetics, Inc., OPKO Health, Inc., Genomic Health (Exact Sciences Corporation), MDxHealth, Beckman Coulter, Inc., Thermo Fisher Scientific Inc., EDX Medical Group, BioMérieux SA, DiaSorin S.p.A., QuidelOrtho Corporation, Becton, Dickinson and Company (BD), AstraZeneca plc, Pfizer Inc., Novartis AG, EDAP TMS, Hitachi, Ltd., and other players. |

Frequently Asked Questions

North America dominated the Prostate Cancer Diagnostics Market in 2025.

The Confirmatory Tests segment is expected to register the fastest CAGR through 2035.

The Rising Prevalence of Prostate Cancer and the Growing Geriatric Population Accelerating the Prostate Cancer Diagnostics Market.

The Prostate Cancer Diagnostics Market was valued at USD 9.72 billion in 2025.

The Prostate Cancer Diagnostics Market is expected to grow at a CAGR of 6.50% from 2026 to 2035.

Get in Touch