Skin Cancer Treatment Market Size & Trends:

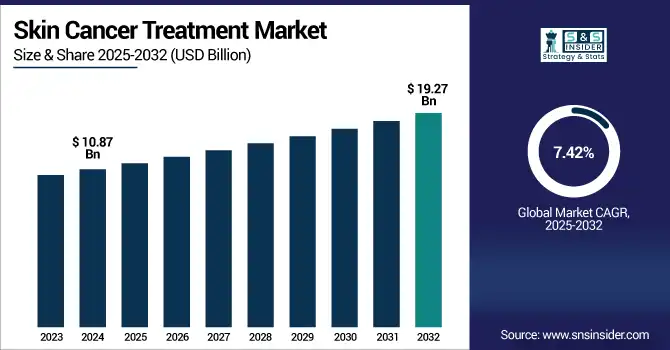

The Skin Cancer Treatment Market size was valued at USD 10.87 billion in 2024 and is expected to reach USD 19.27 billion by 2032, growing at a CAGR of 7.42% over the forecast period of 2025-2032.

The skin cancer treatment market is growing significantly due to the increasing incidence of melanoma and non-melanoma skin cancers, growing awareness of early detection, and the development of targeted and combination therapies. As the population increases and aging continues, the need for the treatment of skin disorders increases. Furthermore, widened health infrastructure facilities and encouraging reimbursement policies in developed countries have resulted in better access to treatment. Advanced treatment methods are also being implemented in emerging economies, which is expected to enable the market to grow considerably during the forecast period.

To Get more information on Skin Cancer Treatment Market - Request Free Sample Report

The U.S. skin cancer treatment market size was valued at USD 3.24 billion in 2024 and is expected to reach USD 5.57 billion by 2032, growing at a CAGR of 7.06% over the forecast period of 2025-2032.

The global market is currently dominated by North America, due to the high incidence of melanoma and nonmelanoma skin cancers in the U.S. The U.S. also has established healthcare infrastructure, robust adoption of advanced therapies such as immunotherapy and targeted therapies, and broad access to specialized dermatological care.

Skin Cancer Treatment Market Dynamics:

Drivers

-

The Increasing Prevalence of Skin Cancer is Driving the Market Growth

The increasing number of cases of melanoma and non-melanoma skin cancer across the globe is one of the key factors driving demand. Rising levels of ambient ultraviolet (UV) radiation, derived from sun exposure or from tanning beds, lack of an ozone layer, and outdoor occupational exposures increase that risk. Moreover, changes in lifestyles and an aging profile increase the vulnerability. Skin cancer is an increasingly common disease, and there is a growing need to diagnose and treat skin cancer early, fostering market growth.

Public health programmes are increasingly aimed at early detection and prevention. This increasing burden of disease is driving healthcare systems to expand dermato-oncological services.

The Cancer Atlas states that 70–90% of melanoma burden and nearly all keratinocyte cancers (non‐melanoma) are owing to excessive exposure to ultraviolet (UV) radiation.

According to PMC (2021), there were an estimated 6.64 million skin cancer cases worldwide (melanoma and non-melanoma; combined), leading to over 2.89 million DALYs.

But even so, non-melanoma skin cancer cases in the U.S. rose by 77% between 1994 and 2014, and the annual melanoma death total will surpass 8,000 by 2025, per the Skin Cancer Foundation.

A Herald Sun article (May 2025) stated that there was a 10% increase in melanoma diagnoses in Victoria, Australia, between 2022 and 2023, attributed to decreased sun protective behaviour among young people and tanning fashions that were popularised on social media.

-

Development in the Treatment Modalities Driving the Market Growth

The development and technological advantages provide new opportunities for the management of skin cancers. Immunotherapies (e.g. checkpoint inhibitors), targeted therapies, and minimally invasive surgeries have introduced new therapeutic practices that have led to better survival of the patients. These breakthroughs provide more targeted and individualized strategies that tend to have fewer deleterious side effects than traditional treatments. This is driving the market as healthcare providers switch over to these superior therapies.

The number of novel therapies and accessibility continue to grow through ongoing clinical trials and approval from regulatory authorities. Moreover, pharmaceutical companies are already making huge investments in R&D for the development of next-generation treatment options, which are more effective and safer.

Tumor-infiltrating lymphocyte (TIL) therapies such as lifileucel (AMTAGVI), for instance, demonstrated “remarkably durable” responses in previously treated metastatic melanoma and a five-year progression-free survival benefit, Melanoma Research Foundation reported.

Lifileucel was granted U.S. Food and Drug Administration accelerated approval as the first TIL therapy for metastatic or unresectable melanoma following PD-1 inhibitor progression.

The DREAMseq trial (review of A Cure Today) confirms that immunotherapy is the standard of care for metastatic melanoma and provides better results compared to targeted BRAF/MEK inhibitor therapies.

Skin Cancer Treatment Market Segmentation Insights:

By Cancer Type

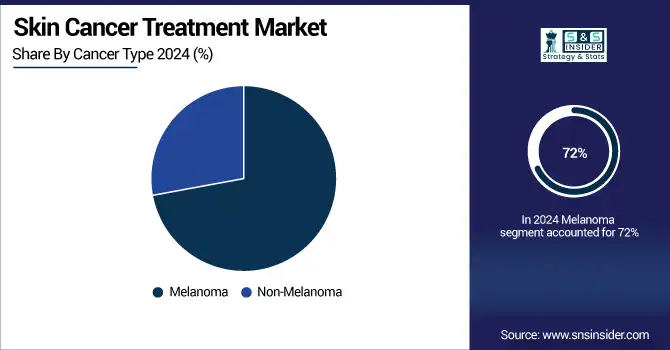

The melanoma segment dominated the skin cancer treatment market share in 2024, with around 72% due to aggressiveness with poor prognosis, and has an increasing prevalence globally, especially among fair individuals, as they are profoundly exposed to intense UV rays. Melanoma more frequently demands more aggressive treatments, such as the use of immunotherapies, targeted therapies, and additional check-ins, which leads to additional health care expenditures. In addition, strong R&D pipelines and a stronger clinical focus on melanoma by pharmaceutical companies have enabled the early approval and uptake of new treatment strategies, cementing their leadership position in the market.

The non-melanoma segment is expected to grow at the fastest pace during the forecast years due to the growing incidence of basal cell carcinoma and squamous cell carcinoma, which are the most common types of skin cancer across the globe. Greater awareness, better screening efforts, and the proliferation of local, minimally invasive treatments such as cryotherapy and photodynamic therapy are driving adoption. Furthermore, the trend toward early outpatient treatments and the increasing geriatric population will also enhance the rapid expansion of this segment shortly.

By Therapy Type

The immunotherapy segment occupied the highest share in the skin cancer treatment market in 2024 due to most effective treatment for advanced and metastatic melanoma, for which other standard therapies have limited results. Immunotherapies, including nivolumab and pembrolizumab, are emerging as first‐line therapies with potential for prolonged survival. The increase in FDA and EMA approvals, along with increasing clinical trials and physicians’ preference for personalized cancer care, has sent immunotherapy to the forefront of managing skin cancer in all major healthcare markets.

The radiation therapy segment is anticipated to witness the fastest growth during the years that are to follow due to its rising use in the treatment of NMSCs with advanced non-melanoma skin cancers, mainly in elderly and inoperable patients. Technical innovations in radiotherapy, including the application of stereotactic body radiotherapy (SBRT) and image-guided radiation therapy (IGRT), have enhanced treatment accuracy and minimized adverse effects. Furthermore, increasing cases of skin cancers across an ageing population and increasing availability of radiation technology in developing countries are stoking the uptake of the segment.

By Route of Administration

The topical segment dominated the skin cancer treatment market share in 2024 with around 33.25%, as it is commonly used for the treatment of superficial and early-stage non-melanoma skin cancers such as basal cell carcinoma and actinic keratosis. In contrast to other invasive and/or costly treatments, topical agents, such as imiquimod and 5-fluorouracil, are less expensive and patient-friendly due to low systemic side effects. This segment accounts for the largest share due to easy application, especially in home care settings, and growing preference for outpatient treatment options.

The intravenous (IV) segment is expected to witness the fastest growth over the forecast period on account of the increasing use of immunotherapies and targeted biologics that are administered through IV. These treatments, including checkpoint inhibitors and monoclonal antibodies, are largely for advanced and metastatic melanomas. Increasing clinical indications of IV-drugs, creation of new infusion regimens with expanded usage of IV-drugs, and growing accessibility at oncologic outposts are propelling the segment of IV-drugs, particularly in developed healthcare industries.

By End User

The hospitals segment dominated the skin cancer treatment market in 2024 with around 41.52% market share, owing to the availability of a full range of cancer care services (such as surgery, chemotherapy, immunotherapy, and radiotherapy) under one roof. Hospitals are usually the first to be measured for the diagnosis and treatment of skin cancer, especially for less common or more advanced skin cancers. In addition to having multidisciplinary care teams, strong medical infrastructure, and established reimbursement environments, other factors to help hospitals become the market leader are their capacity to treat a larger patient volume.

The cancer research & treatment centers market is projected to have a significant CAGR during the forecast period, with the rising availability of state-of-the-art treatment options, clinical trials, tailor-made treatment options, and network-supported oncological expertise in these specialized centers. As precision medicine and immuno-oncology have become more prevalent, patients are increasingly being referred to special cancer centers that offer cutting-edge, personalized, research-based treatments. These centres are also at the forefront of implementing new technologies and treatments, and they will be crucial to changes in the landscape in the management of skin cancer.

Skin Cancer Treatment Market Regional Analysis:

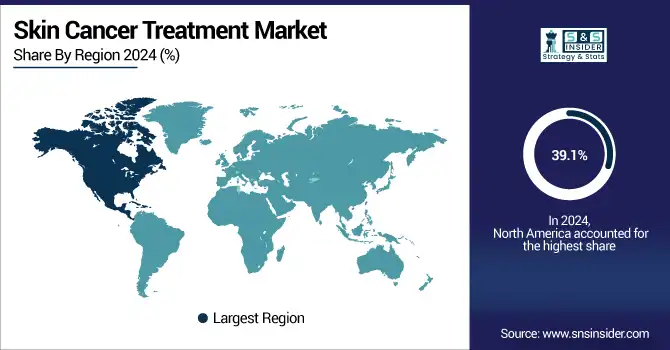

North America is the leading region in the skin cancer treatment market analysis, with around 39.1% market share in 2024 due to the high occurrence of melanoma, non-melanoma skin cancers, due to higher UV exposure, fair-skinned population distribution, and tanning beds usage. In addition, advanced healthcare infrastructures, well-developed reimbursement schemes, and early use of new therapies such as immunotherapy, targeted therapy, and Mohs micrographic surgery are implemented in the area as well. Deep investment in cancer research, a large presence of major pharmaceutical companies, and a high level of awareness with regard to skin cancer screening also contribute to the dominance of North America in the market.

Asia Pacific is the fastest-growing region in the skin cancer treatment market with 7.96% CAGR over the forecast period due to awareness of the disease, increasing the frequency of diagnosis, and increasing expenses on health care in emerging economies such as China, India, and Southeast Asia. Increased prevalence of skin cancer is due to the ageing of the population and outdoor occupations. The public and private sectors are making significant investments in healthcare facilities, which are increasing access to dermatology and oncology services. The brand plays a crucial role in the advancement of therapeutics and clinical trials, which is driving the treatment adoption and market expansion.

Europe is witnessing substantial growth in the skin cancer treatment market trends due to an increase in the burden of the disease, healthcare advances, and a flourishing clinical research landscape. Melanoma cases have increased by 1/3 in the past 10 years, particularly amongst those aged 80 and above, with a 57% increase in cases, adding to the need for new treatment options and early diagnosis initiatives, while cancer types such as lung and breast are falling.

The UK's NHS Cancer Vaccine Launch Pad, in collaboration with Scancell and BioNTech, is speeding up trials for new DNA and mRNA-based melanoma vaccines and increasing patient access by 2030.

Moreover, with the advent of fast, new immunotherapy formulations, such as the injectable version of nivolumab, the admin time is shrinking and economies of scale for the hospitals are improving, driving more of this into European oncology care. Such development has come in line with the overall growth of Europe’s skin cancer pharmacotherapy sector, as a result of increased access to precision medications, immunotherapy, and clinical trials in forerunning nations such as the UK, Germany, and France.

Latin America and the Middle East & Africa (MEA) are witnessing the moderate growth of the skin cancer treatment market due to awareness, improving healthcare access, and rising availability of diagnosis and treatments. In Latin America, countries such as Brazil and Mexico are developing national public screening programs and are investing in oncology infrastructure, which is allowing for increased early detection and access to treatment of skin cancer.

Growth in the MEA region is driven by an increase in skin cancer cases caused by climate exposure and lifestyle changes, and successful government-led health initiatives. Nations including the United Arab Emirates (UAE), Saudi Arabia, and South Africa are strengthening their dermatological services and collaborating with international healthcare organizations. Meanwhile, with persistent problems of resource access in rural areas, there are some moderate gains in such areas due to some improvement in diagnostic capabilities and specialist care.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players in the Skin Cancer Treatment Market:

The skin cancer treatment market companies are Roche Holding AG, Merck & Co., Inc., Bristol-Myers Squibb Company, Novartis AG, Pfizer Inc., Amgen Inc., Sanofi S.A., AstraZeneca PLC, Eli Lilly and Company, Regeneron Pharmaceuticals, Inc., Sun Pharmaceutical Industries Ltd., Leo Pharma A/S, Galderma S.A., F. Hoffmann-La Roche Ltd., Bausch Health Companies Inc. (formerly Valeant), Glenmark Pharmaceuticals Ltd., DermTech, Inc., Castle Biosciences, Inc., Allergan (AbbVie Inc.), 3M Company, and other players.

Recent Developments in the Skin Cancer Treatment Industry:

-

May 2025 – Merck & Co., Inc. (MSD overseas and in Canada) disclosed that new data in more than 25 cancer types across a range of treatment environments will be shared at the American Society of Clinical Oncology (ASCO) Annual Meeting, which will take place from May 30 through June 3. The findings highlight Merck's focus on accelerating cancer research and strengthening its portfolio of mature oncology medicines.

-

February 2025 – Bristol Myers Squibb announced findings from its Phase 3 RELATIVITY-098 trial of Opdualag (nivolumab and relatlimab-rmbw combination) as an adjuvant treatment for patients with completely resected stage III–IV melanoma. The study failed to achieve its first primary endpoint, recurrence-free survival (RFS).

-

January 2024 – Pfizer Inc. has announced that SGN-TGT, a candidate drug in development for skin cancer, is at Phase I clinical trials. Phase I drugs addressing skin cancer have an overall 75% phase transition success rate (PTSR) to progress to Phase II, as per GlobalData.

Skin Cancer Treatment Market Report Scope:

Report Attributes Details Market Size in 2024 USD 10.87 Billion Market Size by 2032 USD 19.27 Billion CAGR CAGR of 7.42% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Cancer Type (Melanoma, Non-Melanoma)

• By Therapy Type (Surgical Procedures, Radiation Therapy, Chemotherapy, Targeted Therapy, Immunotherapy, Photodynamic Therapy (PDT), Topical Treatments)

• By Route of Administration (Topical, Oral, Injectable, Intravenous (IV), Others e.g., Intralesional)

• By End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers (ASCs), Cancer Research and Treatment Centers, Homecare Settings)

Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles The skin cancer treatment market companies are Roche Holding AG, Merck & Co., Inc., Bristol-Myers Squibb Company, Novartis AG, Pfizer Inc., Amgen Inc., Sanofi S.A., AstraZeneca PLC, Eli Lilly and Company, Regeneron Pharmaceuticals, Inc., Sun Pharmaceutical Industries Ltd., Leo Pharma A/S, Galderma S.A., F. Hoffmann-La Roche Ltd., Bausch Health Companies Inc. (formerly Valeant), Glenmark Pharmaceuticals Ltd., DermTech, Inc., Castle Biosciences, Inc., Allergan (AbbVie Inc.), 3M Company, and other players.

Frequently Asked Questions

Ans: North America dominated the Skin Cancer Treatment Market in 2024.

Ans: The “Melanoma” segment dominated the Skin Cancer Treatment Market.

Ans: The Increasing Prevalence of Skin Cancer is Driving the Market Growth.

Ans: The Skin Cancer Treatment Market was USD 10.87 billion in 2024 and is expected to reach USD 19.21 billion by 2032.

Ans: The Skin Cancer Treatment Market is expected to grow at a CAGR of 7.42% from 2025 to 2032.

Get in Touch