Burn-In Test System for Semiconductor Market Size Analysis:

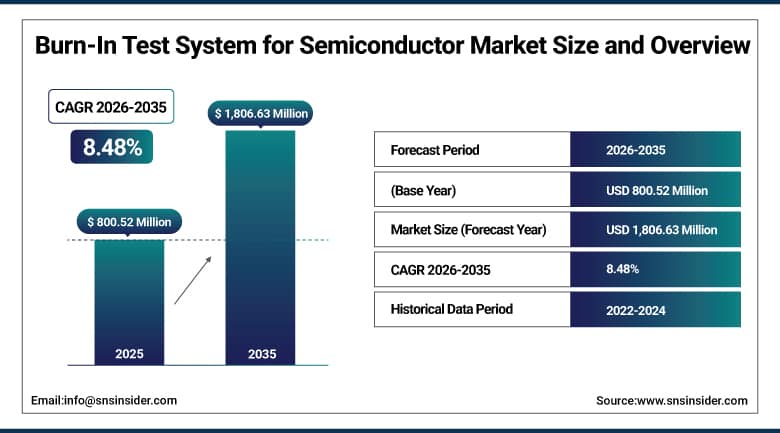

The Burn-In Test System for Semiconductor Market was valued at USD 800.52 Million in 2025 and is expected to reach USD 1,806.63 Million by 2035, growing at a CAGR of 8.48% from 2026 to 2035.

The Burn-In Test System for Semiconductor Market is growing due to increasing demand for high-reliability semiconductor devices across automotive, AI, data centers, and consumer electronics. Rising chip complexity, advanced nodes, and higher power densities require rigorous stress testing to detect early failures. Growth in fabless manufacturing and outsourcing to OSAT providers further boosts demand. Additionally, expanding electric vehicle production, industrial automation, and stricter quality and reliability standards are accelerating adoption of advanced burn-in testing systems.

Market Size and Forecast

-

Market Size in 2026E: USD 868.40 Million

-

Market Size by 2035: USD 1,806.63 Million

-

CAGR: 8.48% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Burn-In Test System for Semiconductor Market - Request Free Sample Report

Burn-In Test System for Semiconductor Market Trends

-

Increasing adoption of fully automated and digitally connected burn-in platforms for real-time monitoring, predictive analytics, and yield optimization.

-

Growing demand for application-specific and high-temperature burn-in solutions driven by AI accelerators, custom ASICs, and advanced memory technologies.

-

Expansion of semiconductor manufacturing capacity in Asia Pacific and renewed investments in North America and Europe fueling market growth.

-

Rising importance of high-reliability testing due to advanced process nodes, higher power densities, and heterogeneous integration in semiconductors.

-

Increasing R&D in advanced packaging, chiplets, and next-generation materials, prompting demand for flexible, scalable, and compact burn-in systems.

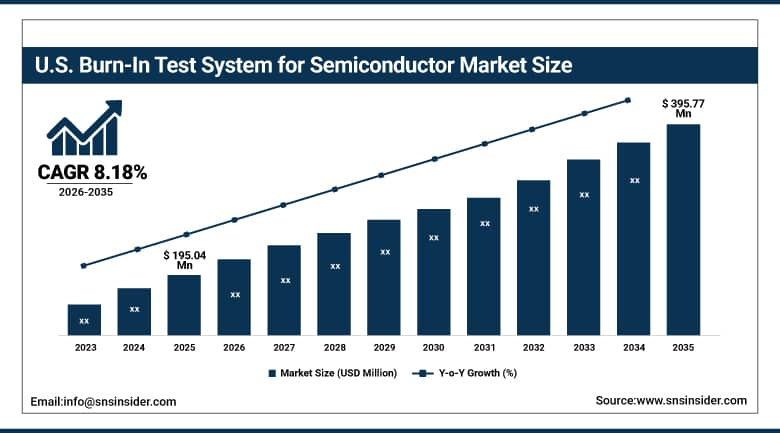

U.S. Burn-In Test System for Semiconductor Market Size Outlook:

The U.S. Burn-In Test System for Semiconductor Market was valued at approximately USD 195.04 Million in 2026 and is expected to reach approximately USD 395.77 Million by 2035, growing at a CAGR of approximately 8.18%.

The U.S. Burn-In Test System for Semiconductor Market is growing due to rising investments in advanced semiconductor manufacturing, increased demand for high-reliability chips in automotive, aerospace, defense, and data centers, and strong adoption of automated testing to meet stringent quality and reliability standards.

AEM Holdings launched a high-throughput, fully automated burn-in platform engineered specifically for AI processors and other high-performance compute devices, reflecting how quickly burn-in test system vendors are adapting their product lines to the surging demand for AI accelerator and data center chip validation.

Burn-In Test System for Semiconductor Market Segment Analysis

-

By Product Type, Integrated (Automated) Burn-In Test Systems dominated with a 37.75% share in 2025, while Portable/Compact Burn-In Systems is the fastest-growing product type at a CAGR of 9.25%.

-

By Application, DRAM & Memory Devices dominated with a 34.54% share in 2025, while ASICs & Custom ICs is the fastest-growing application at a CAGR of 9.21%.

-

By End User, Semiconductor Manufacturers dominated with a 38.86% share in 2025, while OSAT Providers is the fastest-growing end-user segment at a CAGR of 9.04%.

-

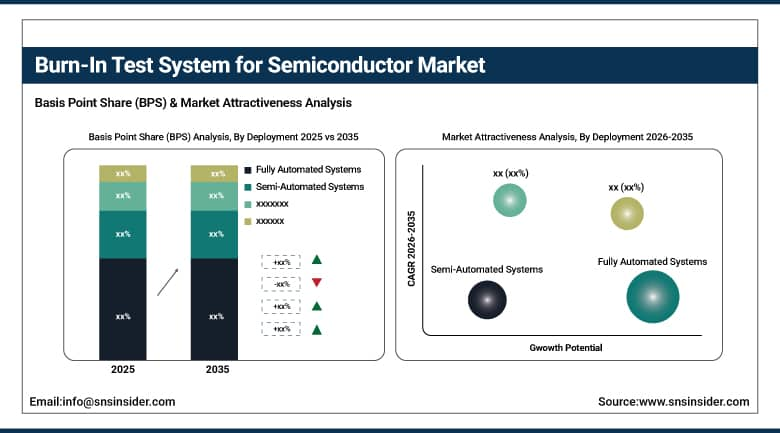

By Deployment/Operation Mode, Fully Automated Systems dominated with a 41.45% share in 2025, while Remote/Cloud-Enabled Burn-In Platforms is the fastest-growing deployment mode at a CAGR of 9.89%.

By Deployment/Operation Mode, Fully Automated Burn-In Systems Lead Market Remote Cloud-Enabled Platforms Drive Future Growth Opportunities

Fully Automated Systems are expected to dominate the Burn-In Test System for Semiconductor Market in 2025E due to their ability to deliver high throughput, consistent test conditions, and reduced human intervention in high-volume semiconductor manufacturing. These systems are widely adopted by large fabs and OSAT providers to meet stringent quality requirements. Meanwhile, Remote/Cloud-Enabled Burn-In Platforms are projected to grow at the fastest rate from 2026–2035, driven by Industry 4.0 adoption, real-time monitoring, predictive analytics, and increasing demand for connected, data-driven testing environments.

By Product Type, Integrated Automated Burn-In Systems Dominate Market Portable Compact Solutions Expected to Grow Fastest

Integrated (Automated) Burn-In Test Systems are expected to dominate the market in 2025E due to their high throughput, consistent test performance, and widespread adoption by large semiconductor manufacturers and OSAT providers. These systems support advanced process nodes and complex devices, making them essential for volume production. Meanwhile, Portable/Compact Burn-In Systems are projected to grow at the fastest rate from 2026–2035, driven by increasing use in R&D labs, pilot production lines, and smaller fabs seeking flexible, space-efficient, and scalable testing solutions.

By Application, DRAM and Memory Devices Lead Burn-In Market ASICs and Custom ICs Drive Fastest Growth

DRAM & Memory Devices are expected to dominate the Burn-In Test System for Semiconductor Market in 2025E due to high-volume production and the critical need for early-failure screening in memory chips used across data centers, consumer electronics, and enterprise storage. These devices require extensive reliability testing to ensure long-term performance. Meanwhile, ASICs & Custom ICs are projected to register the fastest growth from 2026–2035, driven by rising adoption of custom silicon for AI accelerator Chip, automotive electronics, and specialized computing applications requiring application-specific burn-in solutions.

By End User, Semiconductor Manufacturers Dominate Burn-In Market OSAT Providers Expected to Achieve Fastest Future Growth

Semiconductor Manufacturers are expected to dominate the Burn-In Test System for Semiconductor Market in 2025E due to their large-scale in-house production, stringent reliability requirements, and continuous investments in advanced testing infrastructure. These manufacturers rely heavily on burn-in systems to ensure product quality at high volumes. Meanwhile, Outsourced Semiconductor Assembly and Test (OSAT) Providers are projected to grow at the fastest rate from 2026–2035, driven by the expanding fabless model, increased test outsourcing, and rising demand for high-throughput, automated burn-in solutions.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

34.85% |

|

North America |

United States |

80.15% |

|

Europe |

Germany |

24.50% |

|

Latin America |

Brazil |

35.90% |

|

Middle East & Africa |

UAE |

24.75% |

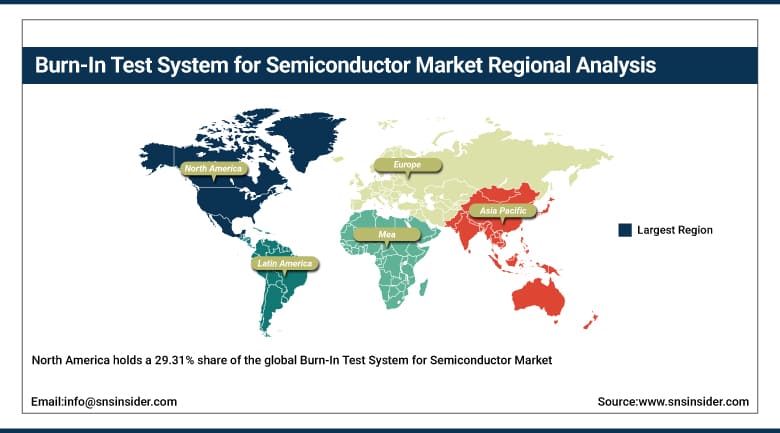

North America Burn-In Test System for Semiconductor Market Insights

North America holds a 29.31% share of the global Burn-In Test System for Semiconductor Market, driven by strong presence of advanced semiconductor manufacturers, leading fabless companies, and robust R&D infrastructure. The region benefits from high demand for reliable chips used in data centers, AI accelerators, aerospace, defense, and automotive electronics. Significant investments under government initiatives to strengthen domestic semiconductor manufacturing further support adoption of automated and high-performance burn-in testing systems to meet stringent quality and reliability standards.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Burn-In Test System for Semiconductor Market Insights

The United States dominates the North America Burn-In Test System for Semiconductor Market due to its leadership in advanced semiconductor design, strong presence of fabless and IDMs, major OSAT operations, and high investments in AI, defense, aerospace, and data center chips, all requiring stringent reliability and burn-in testing.

Europe Burn-In Test System for Semiconductor Market Insights

Europe accounts for 23.06% of the global Burn-In Test System for Semiconductor Market, supported by strong demand from automotive electronics, industrial automation, and power semiconductor manufacturing. The region is home to leading automotive OEMs and Tier-1 suppliers, driving stringent reliability and safety testing requirements. Growing adoption of electric vehicles, ADAS, and wide-bandgap semiconductors such as SiC and GaN, along with increasing investments in regional semiconductor manufacturing and R&D, continue to support steady demand for advanced burn-in test systems.

Germany Burn-In Test System for Semiconductor Market Insights

Germany dominates the European Burn-In Test System for Semiconductor Market due to its strong automotive manufacturing base, leadership in industrial electronics, and high demand for power semiconductors. The country’s focus on EVs, ADAS, Industry 4.0, and stringent quality standards drives sustained adoption of advanced burn-in testing systems.

Asia Pacific Burn-In Test System for Semiconductor Market Insights

Asia Pacific is expected to dominate the global Burn-In Test System for Semiconductor Market with a 41.22% share in 2025E, supported by strong semiconductor manufacturing bases in China, Taiwan, South Korea, and Japan. The region benefits from large-scale fab capacity, high memory and logic chip production, and a strong OSAT ecosystem. Additionally, Asia Pacific is projected to record the fastest CAGR of 8.75% from 2026–2035, driven by continued fab expansions, government support, rising AI and EV chip demand, and increasing adoption of automated burn-in testing systems.

China Burn-In Test System for Semiconductor Market Insights

China dominates the Asia Pacific Burn-In Test System for Semiconductor Market due to its extensive semiconductor manufacturing base, large OSAT ecosystem, and strong government support for domestic chip production. High volumes of memory, logic, and power semiconductor manufacturing drive substantial demand for automated and high-capacity burn-in testing systems across the country.

Latin America (LATAM) and Middle East & Africa (MEA) Burn-In Test System for Semiconductor Market Insights

Latin America and the Middle East & Africa represent smaller but emerging markets for burn-in test systems, driven by gradual expansion of electronics manufacturing, automotive assembly, and industrial infrastructure. Growth is supported by increasing semiconductor testing activities, rising adoption of reliable electronics in energy, telecom, and industrial applications, and growing interest in local assembly and testing capabilities. While limited fab presence restrains scale, investments in technology hubs, data centers, and industrial digitization are creating steady demand for advanced and reliable burn-in testing solutions.

Market Dynamics

Growth Drivers: Global Burn-In Test System Market Growth Driven by Rising Semiconductor Complexity High-Reliability Requirements and Expanding Automotive AI Data Center Applications

The global Burn-In Test System for Semiconductor Market is driven by the rising complexity and performance requirements of semiconductor devices across automotive, AI, data centers, 5G, and industrial electronics. Advanced process nodes, higher power densities, and heterogeneous integration increase the risk of early-life failures, making burn-in testing essential for ensuring long-term reliability. Rapid growth in electric vehicles, ADAS, and power electronics especially SiC and GaN devices has further intensified demand for rigorous stress testing. In addition, the expansion of fabless semiconductor companies and the increasing role of OSAT providers are accelerating investments in high-throughput, automated burn-in systems. Stricter quality standards, safety regulations, and zero-defect manufacturing goals across end-use industries continue to support sustained market growth.

5G deployment is widespread, with more than 70 % of U.S. cellular sites supporting 5G, increasing demand for reliable RF and base-station semiconductors that require thorough burn-in testing

Restraints:Burn-In Test System Market Faces Challenges from Long Testing Cycles High Energy Use Device Overstress and Limited Standardization

The Burn-In Test System for Semiconductor Market faces restraints from long testing cycles that can limit throughput, increasing energy consumption during high-temperature operation, and the risk of device overstress affecting yield if test parameters are not optimized. Limited standardization across device types, rapid technology transitions, and the need for specialized expertise to configure and manage advanced burn-in systems also constrain broader adoption.

Opportunities: Emerging Opportunities in Fully Automated Digitally Connected Burn-In Platforms Drive Growth Across Global Semiconductor Market

Significant opportunities exist in the adoption of fully automated and digitally connected burn-in platforms that enable real-time monitoring, predictive analytics, and improved yield optimization. Emerging applications such as AI accelerators, custom ASICs, and Next Generation memory technologies create demand for application-specific and high-temperature burn-in solutions. Growth in semiconductor manufacturing capacity across Asia Pacific and renewed investments in domestic chip production in North America and Europe further expand the addressable market. Additionally, increasing R&D activity in advanced packaging, chiplets, and next-generation materials presents opportunities for vendors to offer flexible, compact, and scalable burn-in systems tailored to evolving semiconductor architectures.

Automated burn-in systems are being introduced to meet advanced chip testing needs: AEM Holdings launched a high-throughput, fully automated burn-in platform engineered for AI processors and other high-performance compute devices.

Competitive Landscape for Burn-In Test System for Semiconductor Market:

Advantest Corporation is a leading global provider of semiconductor test equipment, specializing in advanced automated test systems, including burn-in and reliability testing solutions. The company supports high-volume production for memory, logic, automotive, and AI chips with innovative platforms and data-driven test infrastructure. With strong global presence and technology leadership, Advantest enables manufacturers to ensure performance, quality, and reliability across diverse semiconductor applications.

-

In October 2025, Advantest announced integration of NVIDIA’s machine learning technology into its Advantest Cloud Solutions Real-Time Data Infrastructure (ACS RTDI™) to bring real-time AI intelligence to semiconductor testing workflows, improving efficiency, yield, and adaptability for high-volume production.

Teradyne Inc. is a major global supplier of semiconductor test equipment, delivering high-performance automated test systems for logic, memory, wireless, and power devices. Its solutions support complex chip testing, advanced packaging, and system-level diagnostics. With a strong focus on innovation and partnerships, Teradyne helps semiconductor manufacturers and OSAT providers ensure device reliability, yield, and performance across diverse applications including AI, automotive, and communications.

-

In March 2025, Teradyne and ficonTEC launched a high-volume double-sided wafer probe test cell for silicon photonics, addressing growing co-packaged optics (CPO) testing demand.

Burn-In Test System for the Semiconductor Market Key Players:

-

Teradyne Inc.

-

Aehr Test Systems

-

Chroma ATE Inc.

-

Aetrium Incorporated

-

Texas Instruments Incorporated

-

Shenzhen EESTEST Electronic Co., Ltd.

-

Powertech Technology Inc.

-

CST (Chunghwa System Technology)

-

Incal Technology

-

Espec Corp.

-

Kyoritsu Test System Co., Ltd.

-

Accutronics Inc.

-

Dongguan Anritsu Electronics Co., Ltd.

-

Suzhou Xinyan Automation Technology Co., Ltd.

-

Shenzhen Hongzhun Technology Co., Ltd.

-

Shenzhen Sineva Intelligent Technology Co., Ltd.

-

Shenzhen Tongdewei Technology Co., Ltd.

-

Shenzhen Qipeng Technology Co., Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 800.52 Million |

| Market Size by 2035 | USD 1,806.63 Million |

| CAGR | CAGR of 8.48% From 2026 to 2035 |

| Base Year | 2025E |

| Forecast Period | 2026-2035 |

| Historical Data | 2021-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Stand-alone Burn-In Systems, Integrated (Automated) Burn-In Test Systems, Portable/Compact Burn-In Systems, and Specialized High-Temperature Burn-In Systems) • By Application (DRAM & Memory Devices, Microprocessors & CPUs, ASICs & Custom ICs, and Power Semiconductors & Discrete Devices) • By End User (Semiconductor Manufacturers, Outsourced Semiconductor Assembly and Test (OSAT) Providers, Electronics Original Equipment Manufacturers (OEMs) • By Research & Development (R&D) Laboratories), and Deployment/Operation Mode (Manual Operation, Semi-Automated Systems, Fully Automated Systems, and Remote/Cloud-Enabled Burn-In Platforms) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Advantest Corporation, Teradyne Inc., Aehr Test Systems, Chroma ATE Inc., Micro Control Company, Aetrium Incorporated, Texas Instruments Incorporated, Shenzhen EESTEST Electronic, Powertech Technology, Chunghwa System Technology, Incal Technology, Espec Corp., Kyoritsu Test System, Accutronics Inc., Dongguan Anritsu Electronics, Suzhou Xinyan Automation Technology, Shenzhen Hongzhun Technology, Shenzhen Sineva Intelligent Technology, Shenzhen Tongdewei Technology, Shenzhen Qipeng Technology. |

Frequently Asked Questions

Asia Pacific dominated the Burn-In Test System for Semiconductor Market in 20255.

Integrated (Automated) Burn-In Test Systems dominated the Burn-In Test System for Semiconductor Market.

The key drivers of the Burn-In Test System for Semiconductor Market are rising semiconductor complexity, high-reliability requirements, growing demand in automotive, AI, data centers, and increased adoption of automated testing systems.

The Burn-In Test System for Semiconductor Market size was USD 800.52 Million in 2025E and is expected to reach USD 1,806.63 Million by 2035.

The Burn-In Test System for Semiconductor Market is expected to grow at a CAGR of 8.48% from 2026-2033.

Get in Touch