Idle Air Control Actuator Market Report Scope & Overview:

The Idle Air Control Actuator Market size was valued at USD 1.04 billion in 2024 and is expected to reach USD 2.36 billion by 2032, growing at a CAGR of 9.13% during 2025-2032.

To Get more information on Idle Air Control Actuator Market - Request Free Sample Report

The global idle air control (IAC) actuators market is growing as the world is moving toward more efficient and eco-friendly vehicles and together with it, the rapid evolution of automotive technology drives the global market for idle air control actuators. Global light vehicle production is projected to reach around 89 million units by 2025 (OICA), which will in turn drive growth for advanced engine management components, such as IAC actuators. This trend is most evident in the Asia Pacific region, where China and India are bolstering their automotive manufacturing capacity through government programs and an expanding consumer market. Meanwhile, Europe leads the technological innovation with the successful launch of the high-precision idle control technology in the face of stringent standard for emissions.

The U.S. idle air control actuator market size was valued at approximately USD 220 million in 2024 and is projected to reach around USD 410 million by 2032, growing at a CAGR of 6.2% over 2025-2032.

In the U.S., IAC actuators are important due to the substantial environmental footprint of the transportation sector. As of 2022, the transportation sector generated 28% of total greenhouse gas emissions and light-duty vehicles accounted for 57% of transport-related emissions (EPA). This has emphasized the importance of technologies that improve fuel consumption and emissions at idle, and IAC actuators are an important part of this value proposition for new and existing vehicles alike. The situation has compounded the aging U.S. vehicle fleet, as an average car in the U.S. is now more than 12 years old (EIA), leading to robust demand in the aftermarket for replacement parts.

Simultaneously, the market is adapting to the electrification wave, as hybrid, plug-in hybrid, and battery electric vehicles made up 16.3% of new U.S. light-duty vehicle sales in 2023, up from 12.9% the previous year 2022 (IEA). Globally, the electric car sales soared to nearly 14 million in 2023 and are expected to reach 17 million by the end of 2024, potentially accounting for one-fifth of all car sales (IEA). These shifts are prompting the development of specialized idle control solutions for new powertrains, ensuring market remains relevant and poised for continued growth in the evolving automotive landscape.

Idle Air Control Actuator Market Dynamics:

Drivers:

-

A Major Driver for the Market is the Global Emphasis on Reducing Vehicle Emissions and Improving Fuel Efficiency

As electric vehicles take over the world due to emission laws, you can expect the next level of engine management technology to be developed by car manufacturers to meet the latest -stricter emission compliance. In the U.S., the transportation sector was the largest source of greenhouse gas emissions, accounting for 28 % of total emissions in 2022, of which 57 % came from light-duty vehicles (EPA). This pressure from regulations forces manufacturers to implement idling with high levels of accuracy, which has caused increasing demand for IAC actuators. Furthermore, the increasing production of light vehicles-estimated to exceed 88.5 million units worldwide by 2025 (OICA)-further increases the demand for these products in developing regions such as Asia-Pacific. These trends will fuel ongoing Idle Air Control Actuator Market Expansion.

Restraints:

-

Idle Air Control Actuator Market Faces Restraints from Accelerating Shift toward Fully Electric Vehicles (EVs)

Traditional internal combustion engine (ICE) vehicles have idle air control like the AC100, however, most EVs do not, as electric motors behave differently and do not idle in the traditional sense. According to IEA, electric and hybrid-electric cars accounted for 16.3 % of new light duty vehicle sales in the United States in 2023. Given the anticipated global electric car sales of 17 million by 2024 (IEA), the market for traditional IAC actuators may shrink particularly in regions with stringently electrification implementation plan. This shift poses a long-term challenge to companies operating in the traditional Actuator market space, which may result in having to adapt to this new reality or risk becoming irrelevant in the new idle air control actuator market landscape.

Opportunities:

-

Growing Aftermarket Segment and Rising Average Age of Vehicles, Especially in Developed Markets Propel Growth

Average vehicle age in the US has exceeded 12 years (EIA), resulting in stronger demand for replacement components as older vehicles require more frequent servicing. The trend is also reinforced by the fact that the large fleet of internal combustion engine vehicles remain, despite the proliferation of electrification. Moreover, the vehicle ownership and manufacture in Asia-Pacific emerging markets are growing at the fastest pace, leading to significant prospects for sales of IAC actuators in both OEM and aftermarket.

With global automotive production expected to reach 89 million vehicles by 2025 (OICA), suppliers able to serve the needs of growing and maturing vehicle populations have a significant opportunity to enhance their position within this increasingly competitive market environment.

Challenges

-

Key Challenge is the Need to Adapt Evolving Automotive Technologies and Consumer Preferences

Hybrid, electric further powertrains also require new idle control solutions that distinctly differentiate from conventional concepts. The market also has to deal with changing raw material prices, and the potential disruption of supply chains, which can affect production costs and margins. As the industry continues its transition to electric vehicles, now reaching almost 14 million in 2023 and predicted to grow to 17 million in 2024 (IEA), manufactures will need to invest in R&D to develop actuator technologies suitable for next generation vehicles. Lack of adaptation to such rapidly changing market trends and technology outlook can become a major barrier to the growth of the market, affecting the Idle Air Control Actuator Market size and share.

Idle Air Control Actuator Market Segmentation Analysis:

By Product Type

The market is dominated by stepper motor actuators, accounting for an estimated 48% of the global market. Since automakers have begun integrating complex engine management systems to meet ever-tightening emissions requirements, they have increasingly turned to them for their accuracy and dependability in controlling idle speed on passenger and commercial vehicles. Their widespread use in OEM applications, and their ability to interface with the latest modular electronic control units only reinforces this dominance.

Rotary actuator is the fastest growing product segment, expected to register a CAGR of nearly 13.9% between 2025-2032. Their smaller size, continued improvement in durability, and excellent compatibility with high technology engine concepts, such as variable valve timing and direct injection combustion is causing their rapid adoption now especially in regions of the world that are introducing very significant vehicle technology changes.

By Vehicle Type

The passenger cars segment dominates the market, occupying around 54% of overall market share. This supremacy results from the regular volumes at which automobiles are actually manufactured globally, along with the intensified regulatory attention on improving fuel economy and leading to emission reductions in this segment. In addition, increasing disposable income levels, growing urbanization and uptake of advanced engine technologies in passenger vehicles, particularly in Europe and Asia Pacific regions, is further fueling the demand for high-tech idle control solutions.

Heavy-duty vehicles are the most rapidly-growing vehicle type with a CAGR of more than 9% until 2032. In addition, the global demand for large engines with durable idle control systems is expected to witness an increase as the logistics, construction, and industrial sectors continue to expand their activities across the world, especially in developing economies and this segment is anticipated to be a major growth engine for IAC actuator manufactures, contributing to higher idle air control actuator market size.

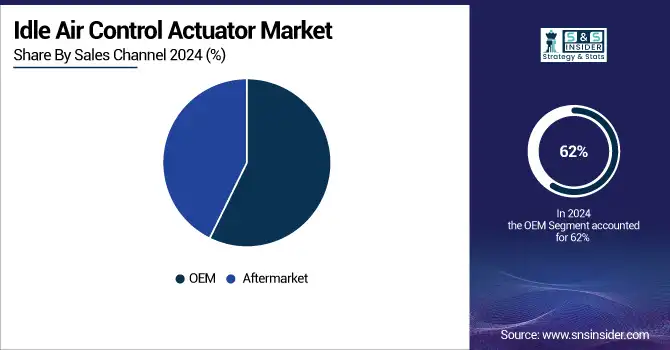

By Sales Channel

OEM accounts for almost 62% share of the market in terms of sales channel segment. That is because during assembly, IAC actuators are incorporated into the vehicle for emissions compliance and the engine to perform well from the beginning. Third, OEMs are reaping the benefits of investments in advanced engine management systems by automakers and pressures for cleaner vehicles, especially in the developed regions.

On the other hand, the aftermarket sector is the fastest growing, expected to maintain a compound annual growth rate of 10.5% between 2025 to 2032. Fueled by an increase in the average age of vehicles, now more than 12 years in the U.S., and the growing necessity for replacement parts, the aftermarket is expanding quickly, especially in areas with a high volume of older vehicles and consumers with increasing awareness of vehicle efficiency and emissions. Such trends are anticipated to have a strong impact on overall idle air control actuator market growth and identify key idle air control actuator market trends.

Idle Air Control Actuator Market Regional Outlook:

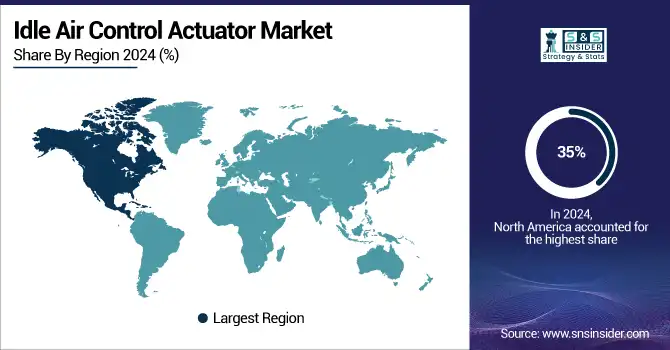

North America holds approximately 35% of the global market share reflecting the region's advanced automotive manufacturing infrastructure, high vehicle ownership rates, and strong demand for both OEM and aftermarket idle air control solutions.

The U.S. is the primary contributor within North America, supported by a large and aging vehicle fleet and ongoing technological advancements in engine management systems. The average vehicle age in the U.S. has surpassed 12 years, fueling aftermarket demand, while the region’s automotive actuators market is projected to grow at a CAGR of 6.9% through 2030.

Europe stands out for its advanced automotive manufacturing, with Germany dominating the region due to its robust OEM presence and technological leadership. Germany’s automotive sector accounts for nearly 20% of the country’s industrial revenue, and Europe’s push for electrification and emission reduction continues to drive adoption of high-precision IAC actuators.

Asia Pacific is the fastest-growing region, propelled by surging vehicle production, urbanization, and rising incomes. China leads the regional market, historically accounting for over 50% of Asia Pacific’s actuator sales, and is home to more than 500 actuator manufacturers. China’s vehicle production exceeded 27 million units in 2023, making it the largest automotive market globally.

Meanwhile, Latin America and the Middle East & Africa (LATAM & MEA) are emerging markets, with growth supported by increasing vehicle sales in Brazil, Mexico, and GCC countries, and a gradual shift toward stricter emission standards. Although LATAM & MEA collectively account for a smaller share, their automotive markets are expected to expand steadily as regulations tighten and infrastructure develops, presenting new frontiers for the idle air control actuator market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players Listed in the Idle Air Control Actuator Market are:

Some of the major idle air control actuators companies in the market are Robert Bosch GmbH, BorgWarner Inc., Continental AG, DENSO CORPORATION, Hitachi Automotive Systems Ltd., Valeo SA, Mikuni Corporation, ACDelco, Standard Motor Products, Walker Products Inc, and others.

Recent Developments:

-

In April 2025, BorgWarner showcased its latest electric commercial vehicle (eCV) solutions at the Advanced Clean Transportation Expo 2025, including the innovative iM-575 integrated inverter-motor drive module. This technology delivers industry-leading power and efficiency for heavy-duty electric vehicles, supporting the shift toward cleaner transportation and highlighting BorgWarner’s continued investment in advanced actuator and power module solutions.

-

In February 2025, Bosch released its ADS Software Update Version 6.5, expanding coverage for model year 2025 vehicles and adding new special tests and system applications. The update includes enhanced adjustment and actuation functions for various brands, supporting advanced diagnostics and calibration for idle control and engine management systems in the latest vehicles.

-

In 2025, Continental has advanced its engine actuator portfolio by introducing digital linear actuators and electric actuators with integrated position sensors. These innovations provide more precise airflow control and rapid response to idle speed variations, enabling automakers to meet stricter emission standards and improve overall engine efficiency.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.04 Billion |

| Market Size by 2032 | USD 2.36 Billion |

| CAGR | CAGR of 9.13% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • Product Type (Stepper Motor Actuators, Solenoid Actuators, Rotary Actuators) • Vehicle Type (Passenger Cars, Commercial Vehicles, Heavy-Duty Vehicles) • Sales Channel (OEM, Aftermarket) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Robert Bosch GmbH, BorgWarner Inc., Continental AG, DENSO CORPORATION, Hitachi Automotive Systems Ltd., Valeo SA, Mikuni Corporation, ACDelco, Standard Motor Products, Walker Products Inc. |

Frequently Asked Questions

North America dominated the market and holds approximately 35% of the global market share

The passenger cars segment dominates the market, occupying around 54% of overall market share

The Idle Air Control Actuator Market is dominated by stepper motor actuators, accounting for an estimated 48% of the global market .

The United States Idle Air Control Actuator Market size was valued at approximately USD 220 million in 2024 and is projected to reach around USD 410 million by 2032, growing at a CAGR of 6.2% from 2025 to 2032.

Idle Air Control Actuator Market size was valued at USD 1.04 billion in 2024 and is expected to reach USD 2.36 billion by 2032, growing at a CAGR of 9.13% from 2025-2032.

Get in Touch