Buses and Coaches Market Report Scope & Overview:

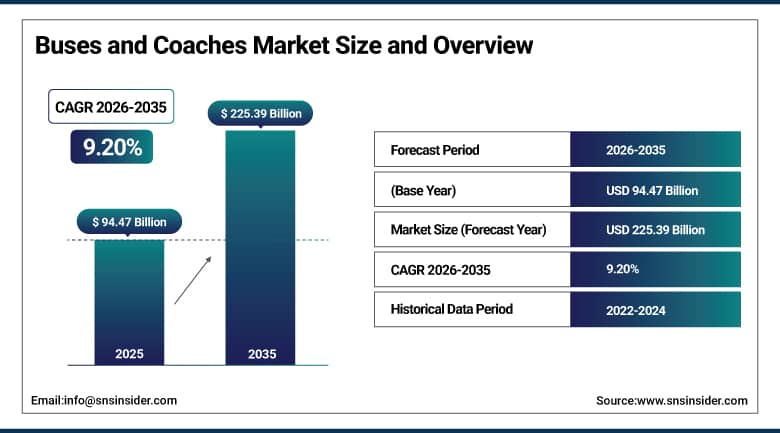

The Buses and Coaches Market was valued at USD 94.47 Billion in 2025 and is expected to reach USD 225.39 Billion by 2035, growing at a CAGR of 9.20% from 2026 to 2035.

The buses and coaches market is witnessing strong transformation driven by electrification, digitalization, and rising urban mobility demand across global transportation networks. Governments are increasingly investing in zero-emission public transit fleets, accelerating the adoption of electric and hybrid buses in major cities. Advancements in connected vehicle technologies, AI-based fleet management, and predictive maintenance systems are improving operational efficiency and service reliability. Meanwhile, demand for high-capacity articulated buses and premium intercity coaches is expanding due to rising urban density and passenger comfort expectations. Additionally, alternative fuels such as hydrogen are emerging as long-term solutions for sustainable long-distance and regional transportation applications.

The global buses and coaches market is undergoing rapid transformation driven by large-scale electrification programs, government funding initiatives, and fleet modernization strategies. In 2025, worldwide deployment of electric and hydrogen buses exceeded 60,000 units, supported by over USD 25 billion in public and private investments. Key government initiatives include China’s NEV subsidy program, the European Union’s Clean Vehicles Directive, the Germany Electromobility Funding Guideline (BMDV Programs), Brazil’s Proconve P8 Emission Standards Program, the UK Zero Emission Bus Regional Areas (ZEBRA) program, and Canada’s iZEV Program (Integrated Zero Emission Vehicle Strategy support for fleets). These initiatives are accelerating adoption across major markets.

Market Size and Forecast

-

Market Size in 2026E: USD 102.07 Billion

-

Market Size by 2035: USD 225.39 Billion

-

CAGR: 9.20% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Buses and Coaches Market - Request Free Sample Report

Buses and Coaches Market Trends

-

Accelerating electrification of urban transit fleets, driven by zero-emission mandate is rapidly expanding the electric bus share of new municipal fleet procurement.

-

Rising adoption of articulated and bi-articulated buses in high-density urban corridors increase passenger capacity per route.

-

Growing deployment of connected vehicle telematics, real-time passenger information systems improving operational efficiency and predictive maintenance.

-

Expanding demand for premium specification intercity coaches equipped with advanced passenger comfort features including reclining seats, onboard Wi-Fi.

-

Progressive integration of hydrogen fuel cell propulsion technology in regional and long-distance coach applications is emerging as a high-potential pathway for decarbonizing routes.

The U.S. Buses and Coaches Market Outlook

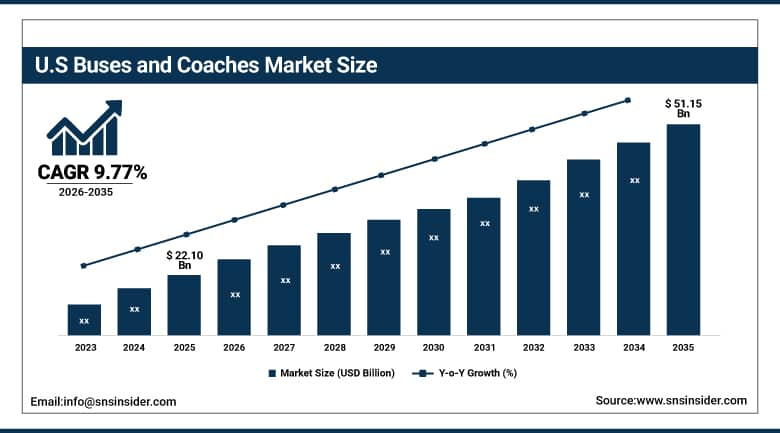

The U.S. Buses and Coaches Market was valued at approximately USD 22.10 Billion in 2025 and is expected to reach approximately USD 51.15 Billion by 2035, growing at a CAGR of approximately 9.77%.

The United States buses and coaches market is a highly structured and policy-driven ecosystem supported by large-scale public transit systems, extensive school transportation networks, and mature intercity coach operations that collectively drive steady fleet demand and replacement cycles. Federal funding initiatives such as the Infrastructure Investment and Jobs Act and the Low and No Emission Bus Program are accelerating fleet electrification by supporting the adoption of battery-electric and hydrogen fuel cell buses across municipal transit agencies. In addition, the country’s vast school bus fleet, the largest globally, represents a major replacement opportunity, with growing state-level mandates promoting the shift toward electric school buses. These factors are reshaping procurement patterns and advancing sustainable mobility adoption nationwide.

The U.S. Federal Transit Administration’s Low and No Emission Vehicle Program is playing a pivotal role in accelerating fleet electrification, with approximately USD 1.7 billion investment allocated in fiscal year 2025 to support zero-emission transit bus procurement and related charging infrastructure across 46 transit agencies in 29 states. A notable example is the Los Angeles County Metropolitan Transportation Authority’s collaboration with Proterra, which introduced 120 battery-electric 40-foot buses operating at an average range of 218 miles per charge under mixed urban conditions. The deployment has achieved around 31% lower per-mile energy costs versus diesel equivalents and reduced annual CO₂ emissions by approximately 6,400 metric tons, reinforcing the agency’s roadmap toward a fully zero-emission bus fleet by 2030.

Buses and Coaches Market Segment Analysis

-

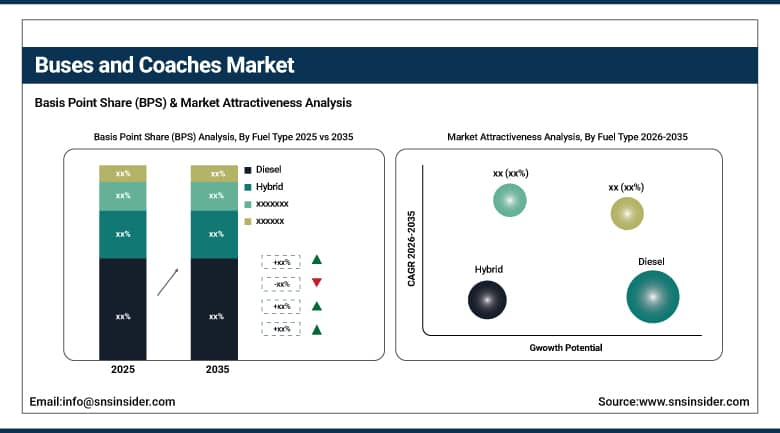

By Fuel Type, the diesel segment dominated the buses and coaches market with 47.36% share in 2025, while the hybrid segment is the fastest growing fuel type with the highest CAGR of 10.75% from 2026 to 2035.

-

By Type, the single deck segment dominated the buses and coaches market with 41.66% share in 2025, while the articulated bus segment is the fastest growing type with the highest CAGR of 10.28% from 2026 to 2035.

-

By Application, the public transit segment dominated the buses and coaches market with 44.78% share in 2025, while the it is also the fastest growing application with the highest CAGR of 9.68% from 2026 to 2035.

-

By Seating Capacity, the 31–50 seats segment dominated the buses and coaches market with 38.69% share in 2025, while the above 70 seats segment is the fastest growing capacity category with the highest CAGR of 11.28% from 2026 to 2035.

By Fuel Type, diesel segment dominates, hybrid segment grows fastest

Diesel-powered vehicles segment dominated by 47.36% of buses and coaches market revenue in 2025, maintaining their dominant position across urban transit, intercity, school transportation, and rural mobility applications due to their high energy density, established fueling infrastructure, and proven operational reliability across diverse conditions. Despite increasing regulatory pressure and rapid electrification in developed markets, diesel continues to remain the preferred drivetrain in cost-sensitive and infrastructure-limited regions. In developing economies across Asia, Africa, and Latin America, diesel buses dominate fleet procurement due to lower upfront costs and limited charging infrastructure. However, gradual market share erosion is expected as hybrid and electric bus adoption accelerates globally.

Hybrid powertrains represent the fastest-growing fuel type segment in the buses and coaches market, driven by increasing adoption from transit operators seeking a transitional solution between conventional diesel and fully electric buses. These systems offer a balanced combination of reduced fuel consumption, lower emissions, and operational flexibility without the infrastructure limitations associated with battery-electric fleets. Parallel and series hybrid configurations, especially those equipped with regenerative braking systems, deliver fuel efficiency improvements of 20–40% in stop-start urban conditions compared to diesel buses. This results in significant operating cost savings and improved route efficiency, making hybrid buses particularly attractive for city transit networks with high-frequency stops and variable passenger demand.

By Type, single deck buses segment dominate, articulated buses segment grow fastest

Single deck buses segment dominated by 41.66% of buses and coaches market revenue in 2025, reflecting their position as the most widely deployed vehicle configuration across global mobility networks. This segment supports a wide range of applications, including urban transit, suburban feeder services, school transportation, intercity routes, and rural connectivity, due to its operational flexibility and adaptability to diverse infrastructure conditions. The design enables efficient passenger boarding and alighting, standardized maintenance practices, and simplified driver training, making it the preferred choice for large-scale fleet procurement. Additionally, single deck buses are compatible with all major propulsion technologies, enabling smooth transition toward electric, hybrid, and alternative fuel systems.

Articulated buses segment represent the fastest-growing type segment in the buses and coaches market, driven by increasing demand for high-capacity urban mobility solutions in densely populated cities. Transit authorities are adopting these vehicles to improve passenger throughput per route while managing rising ridership and limited fleet expansion budgets. Featuring a flexible joint between two sections, articulated buses can carry around 150–200 passengers, significantly higher than standard single-deck buses. This capacity advantage makes them ideal for bus rapid transit corridors and high-frequency urban routes. Their integration with dedicated lanes enhances operational efficiency, schedule reliability, and overall transport system productivity, supporting large-scale urban transit optimization strategies.

By Application, public transit segment dominates, while it also grows fastest

Public transit segment dominated by 44.78% of buses and coaches application revenue in 2025, making it the dominant application segment in the global market. This reflects the large-scale role of municipal transport systems in vehicle procurement and fleet modernization across major regions including China, Europe, India, Southeast Asia, and Latin America. Public transit authorities manage the world’s largest organized bus fleets, generating steady demand through scheduled replacement cycles, capacity expansion, and technology upgrades. Government support in the form of subsidies, concessional financing, and zero-emission mandates is further accelerating adoption of electric and hybrid buses, strengthening procurement momentum and reinforcing long-term market growth in this segment.

Public transit segment also represents the fastest-growing application segment in the buses and coaches market, driven by large-scale municipal fleet electrification programs, rapid urbanization, and increasing government investments in sustainable mass mobility systems. Accounting for a significant share of global revenue in 2025, this segment continues to expand as cities across China, Europe, India, Southeast Asia, and Latin America prioritize high-capacity, low-emission transport solutions. Strong policy support through subsidies, concessional financing, and zero-emission mandates is accelerating procurement of electric and hybrid buses. Continuous fleet replacement cycles, network expansion, and smart city integration initiatives are further reinforcing sustained growth momentum in public transit applications globally.

By Seating Capacity, 31–50 seat buses segment dominates, above-70-seat segment grow fastest

The 31–50 seat capacity segment dominated market for 38.69% of buses and coaches market revenue in 2025. This segment encompasses the standard full-size single deck urban transit bus and intercity coach configurations that constitute the core procurement volume across global public transport and private coach operator markets, reflecting the widespread alignment between the 31–50 seat capacity envelope and the operational requirements of urban trunk route services, suburban express routes, school transportation programs, and regional intercity coach services where vehicle capacity is sized to match typical peak-hour load factors without the operational complexity or infrastructure requirements of higher-capacity articulated or double-deck alternatives.

The above-70-seat category represents the fastest-growing capacity segment in the buses and coaches market, driven by increasing deployment of high-capacity articulated buses, bi-articulated buses, and premium double-deck coach platforms across high-density urban transit corridors, intercity trunk routes, and airport shuttle networks. Growing urban populations, rising peak-hour congestion, and the need to maximize passenger throughput per vehicle are encouraging transit authorities to adopt higher-capacity configurations. These vehicles enable improved operational efficiency by reducing fleet requirements while increasing per-trip passenger movement. Additionally, investments in bus rapid transit systems and long-distance express services in emerging and developed markets are further accelerating demand for above-70-seat capacity buses globally.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.41% |

|

Europe |

Germany |

34.16% |

|

Asia Pacific |

China |

37.75% |

|

Middle East & Africa |

UAE |

19.68% |

|

Latin America |

Brazil |

25.61% |

Asia Pacific Buses and Coaches Market Insights

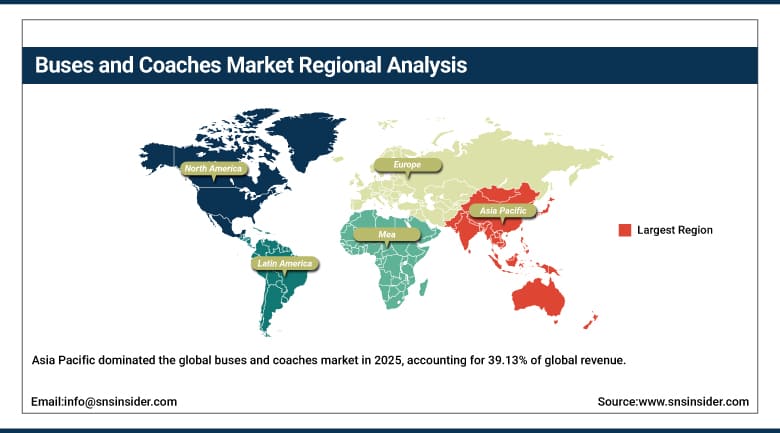

Asia Pacific dominated the global buses and coaches market in 2025, accounting for 39.13% of global revenue, with China contributing 37.75% of regional demand. This leadership is driven by large-scale urbanization, strong public transport dependency, and sustained government investment in bus fleet expansion and electrification. China leads global electric bus adoption through national subsidy programs and municipal mandates, supported by major manufacturers such as Yutong, BYD, CRRC, and King Long, with cities like Shenzhen and Beijing operating near fully electrified fleets. Meanwhile, India is emerging as a high-growth market, supported by metro feeder expansion, intercity connectivity projects, and the PM e-Bus Sewa scheme targeting 10,000 electric buses across multiple cities.

China's Ministry of Transport, under its 14th Five-Year Transportation Development Plan allocating USD 1.6 Trillion toward integrated transportation infrastructure, directly accelerated CRRC and BYD's joint development of a next-generation 18-meter articulated battery-electric bus platform for high-frequency BRT deployments in Tier 1 and Tier 2 Chinese cities, with field deployment across 28 qualifying routes in Shenzhen and Chengdu demonstrating a 26% improvement in energy consumption efficiency per passenger-kilometer compared with the preceding generation platform, and a 19% reduction in total fleet operating cost per route per annum compared with legacy CNG articulated bus configurations.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Buses and Coaches Market Insights

North America accounted for 28.48% of global buses and coaches revenue in 2025, with the United States contributing around 82.14% of regional demand. The market is driven by transit fleet modernization, large-scale school bus replacement cycles, and a strong policy push toward zero-emission mobility. Federal programs such as FTA funding initiatives, along with state-level incentives and EPA emissions regulations, are accelerating the shift toward battery-electric and hydrogen fuel cell buses. School transportation electrification is gaining momentum across multiple states. Canada also contributes steadily, with cities like Toronto, Vancouver, and Montreal actively investing in electric bus fleets supported by climate-focused transit policies and funding programs.

Canada and the United States are witnessing strong momentum in public transit electrification supported by large-scale government funding and municipal procurement programs. In 2025, the U.S. Infrastructure Investment and Jobs Act and Federal Transit Administration grants collectively supported over USD 1.7 billion in zero-emission bus investments, enabling deployment pipelines exceeding 5,500 electric and hydrogen fuel cell buses across major transit agencies. Leading cities such as Los Angeles, New York, and San Francisco are achieving 30–40% reductions in energy cost per mile with electrified fleets. In Canada, federal ZEB (Zero Emission Bus) initiatives have supported over 3,000 buses across Toronto, Vancouver, and Montreal, reinforcing national net-zero mobility targets.

Europe Buses and Coaches Market Insights

Europe accounted for 22.73% of global buses and coaches revenue in 2025. The region is driven by a strong regulatory framework, with the European Union’s Clean Vehicles Directive enforcing minimum procurement requirements for zero-emission and low-emission buses across public sector fleets, accelerating the shift away from diesel. Key markets such as Germany, the UK, France, the Netherlands, and Nordic countries are leading adoption of electric and hydrogen buses, supported by subsidies, low-emission zones, and city-level electrification targets. At the same time, the intercity coach segment is recovering strongly, with operators upgrading fleets to premium, comfort-focused coaches to meet rising demand for affordable long-distance travel across Europe.

The European Commission's Sustainable and Smart Mobility Strategy, targeting a 90% reduction in transport emissions by 2050, prompted Daimler Buses and Solaris Bus & Coach to jointly qualify a new hydrogen fuel cell articulated bus platform in 2025 through a structured pilot deployment program across Hamburg and Warsaw municipal transit networks, demonstrating zero-emission operation, competitive range performance, and passenger capacity equivalent to diesel articulated alternatives, with results submitted to EU regulatory authorities in support of the expanded hydrogen bus infrastructure funding framework under the Connecting Europe Facility.

Middle East & Africa and Latin America Buses and Coaches Market Insights

Middle East & Africa and Latin America are among the fastest-growing regions in the buses and coaches market, driven by rapid urbanization, population growth, and increasing investment in organized public transport systems. Middle East & Africa accounted for 3.19% of global revenue in 2025 and is projected to grow at a CAGR of 9.65%, supported by major transit projects in GCC countries such as Saudi Arabia’s Vision 2030 and the UAE’s smart mobility initiatives, along with expanding bus networks in African cities. Latin America contributed about 6.47% of global revenue, with Brazil representing nearly 46% of regional demand through fleet modernization and BRT expansion in key metropolitan areas.

Saudi Arabia's Public Transport Authority, under the Kingdom's Vision 2030 Mobility Program, partnered with Yutong Bus to deploy a 500-vehicle battery-electric and hybrid bus fleet across the Riyadh public transit network in 2025, representing the largest single zero-emission bus procurement program in GCC history. The deployment demonstrated average fuel cost savings of 44% compared with the legacy diesel fleet, supported the Kingdom's national carbon neutrality target, and established a replicable procurement and operational framework subsequently adopted by transit authorities in Abu Dhabi and Doha for their parallel fleet electrification programs.

Market Dynamics:

Growth Drivers: Urbanization-driven public transit demand and zero-emission fleet electrification policies are the primary structural growth catalysts

The structural acceleration of global urbanization is driving strong demand for organized public transport systems, with the United Nations projecting that 68% of the global population will live in urban areas by 2050, up from 56% in 2025. This rapid shift is increasing the need for efficient, high-capacity, and cost-effective mobility solutions in densely populated cities. Buses and coaches remain the most widely used surface transport mode due to their flexibility and low infrastructure requirements compared to rail systems. Additionally, global decarbonization policies are accelerating fleet renewal, as governments in Europe, the United States, and China support zero-emission bus adoption through regulations, subsidies, and electrification targets.

India's Ministry of Housing and Urban Affairs, under the PM e-Bus Sewa scheme allocation of USD 5,613 Crore for 10,000 electric bus procurement and operations support across 169 cities, awarded contracts in 2025 to Tata Motors and Olectra Greentech covering the supply of 3,200 and 1,800 electric buses respectively, with initial deployments across Bengaluru, Pune, Hyderabad, and Ahmedabad transit networks demonstrating a 38% reduction in operational energy cost per kilometer, zero-emission performance across all operating routes, and improved passenger satisfaction metrics attributable to enhanced vehicle interior specifications compared with the displaced diesel fleet units.

Restraints: High acquisition cost of zero-emission vehicles and inadequate charging infrastructure in emerging markets constrain transition pace

The higher upfront cost of battery-electric and hydrogen fuel cell buses compared to diesel vehicles remains a major barrier to rapid electrification, especially in regions with limited subsidies and constrained transit budgets. A standard 12-meter electric bus typically carries a USD 150,000–300,000 price premium depending on battery capacity, extending payback periods and complicating procurement planning for operators. In developing regions such as Sub-Saharan Africa, South Asia, and Southeast Asia, weak charging infrastructure, unreliable electricity supply, and limited depot networks further restrict adoption. Consequently, diesel buses continue to dominate fleet procurement in these markets, maintaining their strong presence in the global buses and coaches industry over the medium term.

Opportunities: Smart mobility integration and tourism recovery-driven premium coach demand represent high-growth commercial frontiers

The convergence of connected vehicle technology, smart city infrastructure, and AI-driven mobility analytics is creating significant opportunities in intelligent bus fleet management systems. These platforms integrate real-time tracking, passenger counting, predictive maintenance, energy optimization, and automated fare collection into unified solutions, enabling new recurring revenue streams beyond traditional vehicle sales. This shift strengthens long-term relationships between manufacturers and fleet operators while improving operational efficiency. At the same time, the recovery of global tourism, business travel, and leisure mobility is boosting demand for premium coach fleets. Operators in Europe, North America, and Southeast Asia are increasingly upgrading vehicles with advanced comfort, connectivity, and sustainability features to meet rising passenger expectations.

The European Commission, under the Clean Vehicles Directive, is accelerating the transition of public transport fleets toward zero-emission mobility across EU member states, mandating that at least 45% of new bus procurement in many regions be classified as clean vehicles. In 2025, Germany, France, the Netherlands, and the Nordic countries collectively deployed over 18,000 electric and hydrogen buses, supported by more than €6 billion in combined EU and national subsidies. Cities such as Berlin, Paris, Amsterdam, and Stockholm have expanded electric bus penetration to 35–60% of urban fleets, delivering up to 25–40% reductions in operational energy costs and significant improvements in urban air quality and noise levels.

Recent Developments:

-

2026: Volvo Bus launched its next-generation Volvo 9700 DD electric double-deck coach platform, featuring a 540 kWh battery system delivering a certified range exceeding 500 kilometers on a single charge, targeting European long-distance coach operators pursuing fleet electrification without compromising intercity range performance or passenger capacity relative to diesel alternatives.

-

2026: BYD expanded its electric bus manufacturing footprint with the commissioning of a new 50,000-unit annual capacity production facility in Łódź, Poland, establishing a European manufacturing base that reduces lead times for EU market fleet deliveries and satisfies local content requirements under European public procurement regulations applicable to municipal transit authority purchasing programs.

-

2025: Daimler Buses introduced the eCitaro G fuel cell articulated bus for series production delivery, combining a 98 kWh battery buffer system with a roof-mounted hydrogen fuel cell range extender to deliver an operational range exceeding 400 kilometers per refueling cycle, targeting high-frequency urban BRT routes where the range limitations of pure battery-electric articulated buses constrain full duty cycle coverage.

-

2025: Yutong Bus secured a framework supply agreement with the Saudi Public Transport Authority for the delivery of 1,200 battery-electric and hybrid buses across the Riyadh metropolitan transit network expansion program, representing the manufacturer's largest single contract in the Middle East market and establishing a regional service and maintenance infrastructure hub to support the deployment.

Buses and Coaches Market Key Players Are:

-

Yutong Bus Co., Ltd.

-

BYD Auto Co., Ltd.

-

Daimler Buses (Mercedes-Benz)

-

Volvo Bus Corporation

-

Solaris Bus & Coach S.A.

-

King Long United Automotive Industry Co., Ltd.

-

CRRC Corporation Limited

-

Tata Motors Limited

-

NFI Group Inc. (New Flyer)

-

Alexander Dennis Limited (ADL)

-

Scania AB

-

MAN Truck & Bus SE

-

Iveco Bus

-

Higer Bus Company Limited

-

Zhongtong Bus Holding Co., Ltd.

-

Proterra Inc.

-

CAF (Construcciones y Auxiliar de Ferrocarriles)

-

Van Hool N.V.

-

Olectra Greentech Limited

-

SML Isuzu Limited

Buses and Coaches Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 94.47 Billion |

| Market Size by 2035 | USD 225.39 Billion |

| CAGR | CAGR of 9.20% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Fuel Type (Diesel, Hybrid, Electric, Fuel Cell, Gasoline, Others), • By Bus Type (Single Deck, Double Deck, Articulated Bus, Mini Bus, Trolley Bus, Others), • By Application (Public Transit, Intercity Coach, School Transportation, Tourism & Charter Services, Corporate/Employee Transportation, Others), • By Seating Capacity (Up to 30 Seats, 31–50 Seats, 51–70 Seats, Above 70 Seats) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Daimler Buses, Volvo Group, BYD, Yutong, Tata Motors, Ashok Leyland, Scania, MAN Truck & Bus, Iveco Group, AB Volvo (Volvo Buses), Solaris Bus & Coach, Alexander Dennis, NFI Group (New Flyer), Proterra, Gillig, King Long, Zhongtong Bus, Higer Bus, Wrightbus, Isuzu Motors. |

Frequently Asked Questions

The buses and coaches market is expected to grow at a CAGR of 9.20% from 2026 to 2035.

The buses and coaches market was valued at USD 94.47 Billion in 2025.

The primary growth factors include accelerating urbanization driven public transit demand, government-mandated zero-emission fleet electrification programs, and sustained recovery in intercity coach and tourism travel demand.

The single deck segment dominated the buses and coaches market with 41.66% share in 2025.

Asia Pacific dominated the buses and coaches market in 2025, holding 39.13% of global revenues, driven by the scale of China's urban transit fleet electrification program and India's expanding electric bus procurement initiatives.

Get in Touch