Electric Vehicle Motor Market Report Scope & Overview:

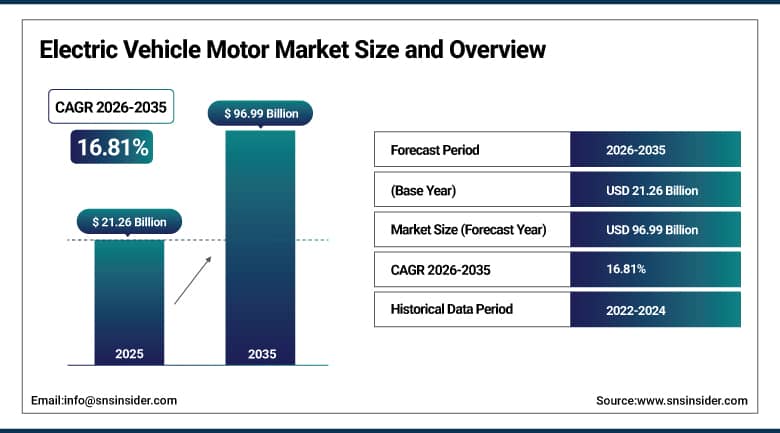

The Electric Vehicle Motor Market was valued at USD 21.26 billion in 2025 and is expected to reach USD 96.99 billion by 2035, growing at a CAGR of 16.81% from 2026–2035.

The electric vehicle motor market size is expected to rise significantly owing to the rising adoption of electric vehicles, the requirement for a more efficient method of propulsion, and the development of various types of motors such as PMSM, axial flux, and switched reluctance motors. Some of the key factors leading to the expansion of the market include integrated e-axles, AWD dual-motor technology, and reduced use of rare earth metals. Investment in the production of electric motors in ecosystems such as Asia-Pacific, Europe, and North America has also played an important role.

In 2025, major EV OEMs and Tier-1 suppliers expanded investments in next-generation motor platforms, with several manufacturers scaling up production of high-efficiency axial flux and switched reluctance motor prototypes aimed at reducing dependency on rare-earth materials.

Market Size and Forecast

-

Market Size 2026E: USD 23.95 Billion

-

Market Size 2035: USD 96.99 Billion

-

CAGR (2026 - 2035): 16.81%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Electric Vehicle Motor Market - Request Free Sample Report

Electric Vehicle Motor Market Trends

-

Rising adoption of PMSM motors is improving EV efficiency and performance globally.

-

Increasing e-axle integration is enabling compact and lightweight EV powertrain designs.

-

Growing use of SiC inverter-compatible motors is enhancing thermal efficiency and power density.

-

Shift toward SRM and rare-earth-free motors is improving cost and supply chain stability.

-

Rising AWD and dual-motor EV adoption is boosting high-performance vehicle demand.

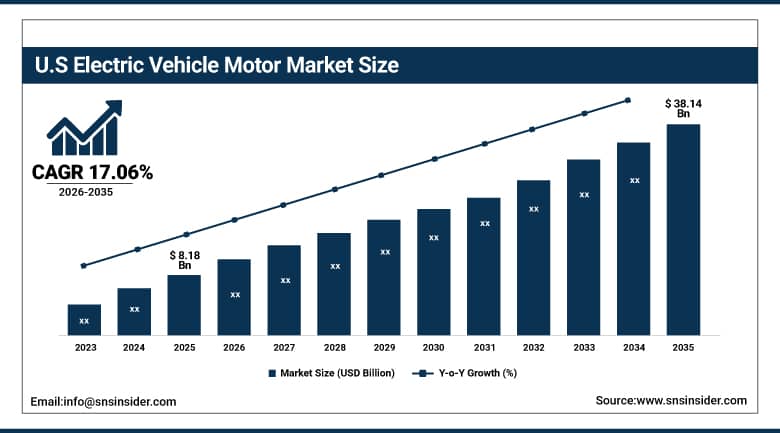

The US Electric Vehicle Motor Market Size Outlook

The Electric Vehicle Motor Market was valued at USD 8.18 billion in 2025 and is expected to reach USD 38.14 billion by 2035, growing at a CAGR of 17.06% from 2026–2035.

The market for electric vehicle motors is experiencing considerable growth as a result of the increasing popularity of EVs, the need for efficient propulsion mechanisms, and innovations in motor types including PMSM, axial flux, and switched reluctance motors. The growth of integrated e-axle solutions, the use of AWD dual-motor systems, and the efforts to decrease the usage of rare earth elements are some of the factors contributing to the development of the global market. Investment in the production of electric motors in ecosystems such as Asia-Pacific, Europe, and North America has also played an important role.

In 2025, major EV drivetrain manufacturers such as Nidec, Bosch, and ZF expanded production of next-generation high-efficiency e-drive systems, including compact integrated motor-inverter units designed for premium EV platforms and commercial electric vehicle fleets across North America and Europe.

Electric Vehicle Motor Market Segment Analysis

-

By Motor Type, permanent magnet synchronous motor (PMSM) dominated the market with 68.74% share in 2025; axial flux Motor is the fastest-growing segment with the highest CAGR.

-

By Power Output, 100–250 kW segment dominated the market with 55.29% share in 2025; below 100 kW is the fastest-growing segment with the highest CAGR.

-

By Vehicle Type, passenger electric vehicles dominated the market with 56.41% share in 2025; commercial electric vehicles is the fastest-growing segment with the highest CAGR.

-

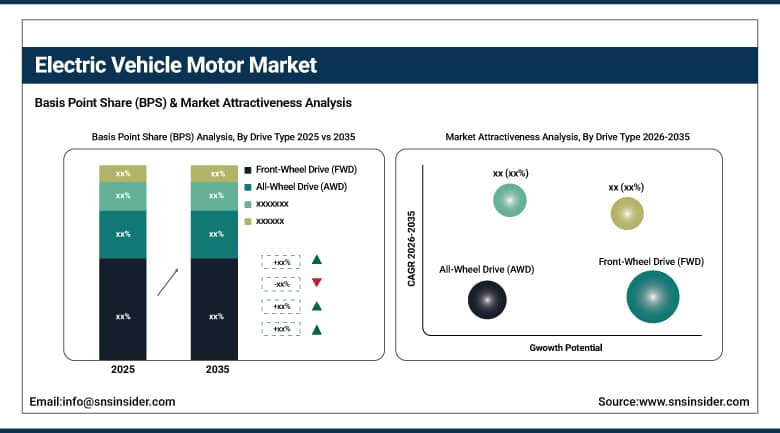

By Drive Type, front-wheel drive (FWD) dominated the market with 46.15% share in 2025; all-wheel drive (AWD) is the fastest-growing segment with the highest CAGR.

By Drive Type, front-wheel drive (FWD) dominates the electric vehicle motor market, while all-wheel drive (AWD) is the fastest-growing segment.

Front-wheel drive (FWD) was the biggest market segment in 2025 accounting for a market share of nearly 46.15%. This segment has enjoyed the leading market share position due to its economical design, mechanical simplicity, and suitability for smaller and mid-size vehicles. Moreover, the FWD system is cost-efficient to manufacture and assemble, making it easier to produce EVs in large volumes. FWD also offers adequate performance in typical city driving situations where most of the electric vehicle usage takes place.

All-wheel drive (AWD) is expected to record the highest CAGR between 2026 and 2035 due to rising consumer preference for high-performance SUVs and luxury cars. All-wheel drive increases traction, stability, and driving safety, especially under unfavorable road and weather conditions. The rise in the popularity of dual and multi-motor electric car platforms is driving the development of all-wheel drive systems among performance-oriented vehicles from the leading brands in electric cars.

By Motor Type, permanent magnet synchronous motor (PMSM) dominates the electric vehicle motor market, while axial flux motor is the fastest-growing segment.

The PMSM segment dominated the market with the highest revenue share of about 68.74% in 2025, mainly owing to its efficient operation, higher torque density, compact construction, and overall high performance over varied driving conditions. The PMSM technology finds extensive use in electric passenger cars and particularly in mid and high-end electric vehicles, which is mainly due to the high efficiency and increased driving range provided by the technology.

The axial flux motor segment is projected to register the fastest CAGR during 2026–2035 owing to the fact that it is built on the architecture of the future that allows for much greater power density within an even smaller form factor. Contrary to traditional radial-flux type motors, axial-flux motors offer more torque, less weight, and increased integration capabilities. Higher requirements for powerful electric vehicles (EVs), sport EVs, and small EVs are driving adoption rates.

By Power Output, the 100–250 kW segment dominates the electric vehicle motor market, while the below 100 kW segment is the fastest-growing segment.

The segment of 100 – 250 kW dominated the market with the highest market share of around 55.29% owing to the wide-scale deployment of this power range in passenger electric vehicles, such as sedans, sport utility vehicles, and crossovers. The ideal combination of acceleration capabilities, range, and cost-effectiveness of this power range makes it a popular choice as the global standard for electric vehicles. Moreover, the modular designs for EVs developed by manufacturers are based on this power range.

The Below 100 kW segment is expected to witness the highest CAGR during 2026–2035 because of the exponential rise in demand for electric two-wheelers, small urban electric vehicles, micro mobility options, and passenger electric vehicles at an entry level. Newer markets especially in the Asia-Pacific region have a high demand for cheap electric transport solutions where low power engines are favored.

By Vehicle Type, passenger electric vehicles dominate the electric vehicle motor market, while commercial electric vehicles are the fastest-growing segment.

Passenger EVs accounted for the highest revenue share of about 56.41% in 2025, it will be backed by mass adoption of the consumer, aggressive approaches to electrification from global OEMs, and a fast-growing EV charging infrastructure. The industry will gain from innovations in the technology of batteries, motors, and car software integration that result in improved ranges and driving experience.

It is expected that Commercial Electric Vehicles will have the highest CAGR between 2026 and 2035 due to increasing electrification in logistics, public transport, and industrial fleet sectors. The increasing need for logistics, last-mile delivery services, higher fuel prices, and the need to cut down on emissions via the use of electric vehicles have made it necessary for fleets to embrace electric mobility.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

86.54% |

|

Europe |

Germany |

26.29% |

|

Asia Pacific |

China |

45.35% |

|

Middle East & Africa |

UAE |

28.96% |

|

Latin America |

Brazil |

37.71% |

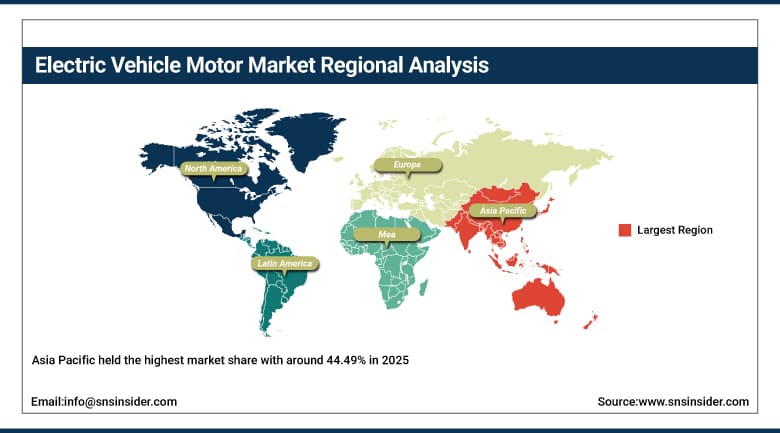

Asia Pacific Electric Vehicle Motor Market Insights

In terms of revenue generation, Asia Pacific held the highest market share with around 44.49% in 2025 and would witness the highest growth rate in terms of CAGR with a valuation of about 17.18% over 2026-2035 due to the presence of large-scale volume of electric vehicles, strong integration of supply chain management processes, and the dominance of electric two wheeler and passenger electric vehicle motors manufacture in the region. Countries like China, Japan, South Korea, and India dominate the manufacture of electric motors across the globe, especially China owing to their dominance in the rare earth metals industry and manufacturing prowess. This region will be witnessing a rapid increase in demand for compact electric vehicle motors which can be used in mainstream electric vehicles. Investment on manufacture of locally manufactured electric vehicles will be boosting the demand for efficient traction motors.

BYD surpassing annual EV production of over 3.0 million units, significantly scaling internal electric motor integration across its vehicle platforms, while Nidec expanded its EV traction motor production capacity in China and Southeast Asia by more than 25% to meet rising global OEM demand.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Electric Vehicle Motor Market Insights

North America, propelled by efficient manufacturing of EVs, high premium EV market penetration, and high deployment of high-efficiency drive trains, is another key market for drivetrain systems in passenger and commercial vehicles. This market enjoys a favorable environment because of the presence of major OEMs and Tier 1 companies that specialize in producing highly efficient motors like PMSM and dual motors used for AWD systems, mostly for SUVs and pickups and high-end luxury EV models. Investments in local EV components manufacturing and federal incentive policies promoting the manufacture of clean mobility vehicles in North America are boosting regional demand for drivetrain systems. Moreover, innovations in e-axle technology and high power density motors are making it possible for manufacturers to make cars lighter and more powerful.

General Motors allocating over USD 10 billion toward its Ultium-based EV and drivetrain expansion program, strengthening next-generation motor production capacity across North America, while Tesla reported that its dual-motor AWD systems improved energy efficiency by nearly 18% across updated Model 3 and Model Y platforms through enhanced motor and inverter optimization.

Europe Electric Vehicle Motor Market Insights

Europe continues to be among the important innovative regions in the electric vehicle motor market due to stringent regulations concerning emissions, extensive use of electric cars, and expertise in the field of automotive engineering. The main countries driving the trend include Germany, France, and the United Kingdom that concentrate on designing extremely efficient motors, light-weight drivetrains, and eco-friendly components. There is heavy expenditure on innovations in the field of motor designs with axial flow motors, rare-earth metal-free PMSMs receiving the most attention. OEMs in collaboration with tier-1 suppliers ensure design of energy efficient electric vehicle drive systems.

Volkswagen investing over EUR 180 billion in its electrification and software-driven mobility strategy through 2027, including large-scale deployment of standardized high-efficiency EV motor systems across its ID-series platforms, while BMW reported up to 20% improvement in drivetrain efficiency in its next-generation electric platforms through optimized motor and inverter integration.

LAMEA Electric Vehicle Motor Market Insights

Countries of the LAMEA region present a promising emerging market for electric motors, owing to the growing adoption of electric vehicles, the initiatives taken by the governments for electrification, and the usage of electric mobility in fleet transportation. There have been investments made by Brazil, UAE, Saudi Arabia, and South Africa in the electric vehicle fleets as well as urban mass transport and logistics. Collaborations with Original Equipment Manufacturers (OEMs) have also helped improve electric vehicle penetration, while more investments in charging infrastructure are driving the demand for electric motors.

Saudi Arabia investing over USD 50 billion in its NEOM smart city project, integrating electric mobility systems and high-efficiency EV drivetrain technologies, while Brazil expanded its electric bus deployment programs by more than 1,500 units in major cities such as São Paulo and Rio de Janeiro, directly increasing demand for high-torque commercial EV motors.

Market Dynamics:

Growth Drivers: Rapid global electrification of transportation and increasing demand for high-efficiency propulsion systems are accelerating the electric vehicle motor market.

There is an increased utilization of electric vehicles (EVs) not only in passenger cars but also in commercial vehicles and even motorcycles. The result has been increased requirements for motors, which include efficient motors such as PMSMs and induction motors. Continued innovations in relation to the efficiency, power density, and thermal performance of electric traction motors have improved their range and performance in automobiles. Emission standards as well as incentives from governments to produce zero-emission vehicles have made Original Equipment Manufacturers (OEMs) manufacture EVs. Integration of motors in association with e-axles and inverters has helped improve their performance and efficiency.

Restraints: High dependence on rare-earth materials and complex motor supply chains is limiting the scalability of ev motor production globally.

Machines using permanent magnets have reliance on materials such as neodymium and dysprosium; therefore, there is cost unpredictability associated with the geographical location of extraction and refining of the raw materials. Also, capital cost constraints for manufacturing motors using technologies such as axial flux and power dense make them costly and hard to use. Challenges in heat dissipation for motors with high power affect their durability. Finally, the lack of a standard motor design in the manufacture of electric cars, where each company uses its unique design, adds to research and development costs.

Opportunities: Development of rare-earth-free motors and next-generation axial flux technologies is creating significant growth opportunities in the EV motor market.

The advancement in motor technology in terms of switched reluctance motors and ferrite PMSM motors is helping in reducing the dependence on rare earth materials and improving cost efficiency. The growing adoption of electric vehicles in commercial sectors, electric buses, and heavy-duty electric trucks will create other segments for demanding torque motors. Implementation of advanced motor controls through artificial intelligence-based predictive maintenance and intelligent axles will enhance operational efficiency. There are ample business opportunities in the manufacturing of motors due to increasing electrification in emerging economies.

Recent Developments

-

2026: Tesla expanded its next-generation electric drive unit manufacturing capacity in North America and Asia, scaling integrated PMSM-based motor production for AWD platforms, with improved inverter-motor integration targeting higher energy efficiency and reduced drivetrain losses across updated EV models.

-

2026: Nidec Corporation increased its global traction motor production footprint, adding new high-efficiency EV motor lines in China and Southeast Asia, focusing on compact PMSM and induction motor systems to support rising demand from global passenger EV and electric two-wheeler manufacturers.

-

2025: BYD strengthened its vertically integrated EV motor ecosystem by scaling in-house production of high-efficiency electric traction motors across its Ocean and Dynasty series platforms, supporting over 3 million annual EV unit production with improved cost efficiency and power density optimization.

-

2025: Volkswagen Group advanced its unified electric drive platform strategy by expanding standardized EV motor and e-axle integration across its MEB-based vehicles, improving drivetrain efficiency and reducing component complexity across its global electric vehicle lineup.

Electric Vehicle Motor Market Key Players are:

-

BYD

-

Tesla

-

Nidec Corporation

-

Bosch Mobility

-

Continental AG

-

ZF Friedrichshafen AG

-

Siemens AG

-

Denso Corporation

-

Hitachi Astemo

-

Magna International

-

BorgWarner Inc.

-

GKN Automotive (Dana Incorporated)

-

Schaeffler AG

-

Valeo SA

-

Mitsubishi Electric Corporation

-

Toshiba Corporation

-

Hyundai Mobis

-

LG Magna e-Powertrain

-

UQM Technologies (Cummins Inc.)

-

Dana TM4 (Dana Incorporated)

Electric Vehicle Motor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 21.26 Billion |

| Market Size by 2035 | USD 96.99 Billion |

| CAGR | CAGR of 16.81% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Motor Type (Permanent Magnet Synchronous Motor (PMSM), Induction Motor (IM), Switched Reluctance Motor (SRM), Axial Flux Motor, Others) • By Power Output (100–250 kW,Below 100 kW, Above 250 kW) • By Vehicle Type (Passenger Electric Vehicles, Commercial Electric Vehicles, Electric Two-Wheelers, Electric Buses, Electric Trucks) • By Drive Type (Front-Wheel Drive (FWD), Rear-Wheel Drive (RWD), All-Wheel Drive (AWD)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BYD, Tesla, Nidec Corporation, Bosch Mobility, Continental AG, ZF Friedrichshafen AG, Siemens AG, Denso Corporation, Hitachi Astemo, Magna International, BorgWarner Inc., GKN Automotive (Dana Incorporated), Schaeffler AG, Valeo SA, Mitsubishi Electric Corporation, Toshiba Corporation, Hyundai Mobis, LG Magna e-Powertrain, UQM Technologies (Cummins Inc.), Dana TM4 (Dana Incorporated) |

Frequently Asked Questions

The electric vehicle motor market is expected to grow at a CAGR of 16.81% from 2026 to 2035.

The electric vehicle motor market was valued at USD 21.26 billion in 2025.

Rising demand from electric mobility expansion, rapid electrification of passenger and commercial fleets, increasing adoption of high-performance drivetrains, and growing investments in next-generation vehicle platforms is driving demand for electric vehicle motors globally.

The Permanent Magnet Synchronous Motor (PMSM) segment dominated the Electric Vehicle Motor market in 2025.

Asia Pacific dominated the Electric Vehicle Motor Market in 2025.

Get in Touch