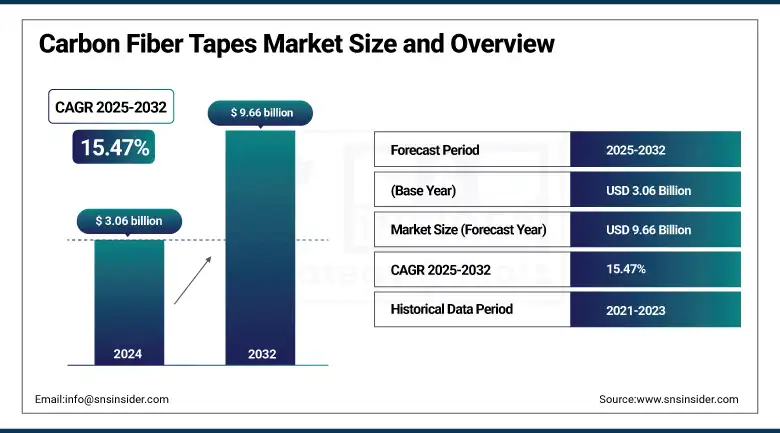

Carbon Fiber Tapes Market Size Analysis:

The Carbon Fiber Tapes Market size was valued at USD 3.06 billion in 2024 and is expected to reach USD 9.66 billion by 2032, growing at a CAGR of 15.47% over the forecast period of 2025-2032.

The Carbon Fiber Tapes Market is witnessing strong growth, driven by increasing demand in aerospace and defense sectors. These industries require high strength-to-weight, temperature resistance, and durability, making carbon fiber tapes ideal for aircraft fuselage, wings, and structural components through automated fiber placement (AFP) and tape laying (ATL). In defense, applications include lightweight armor, drones, and missile systems. Rising defense budgets and fleet modernization further boost adoption. Notably, NASA’s HiCAM project, with USD 184 million funding and USD 136 million industry contribution, aims to advance high-rate composites for full-scale fuselage and wing demonstrations by 2028, significantly supporting market expansion.

To Get more information On Carbon Fiber Tapes Market - Request Free Sample Report

Carbon Fiber Tapes Market Trends

-

Rising adoption of carbon fiber tapes in electric vehicles for lightweight structural components is accelerating market growth.

-

Increasing use of thermoplastic carbon fiber tapes is enhancing recyclability and reducing production cycle times.

-

Expansion of wind energy sector is driving demand for carbon fiber tapes in turbine blades for improved efficiency.

-

Integration of automated manufacturing systems is boosting production consistency and reducing labor costs.

-

Development of hybrid composites combining carbon fiber tapes with other materials is enabling tailored mechanical properties.

-

Growth in sporting goods and high-performance equipment is creating new application avenues for lightweight, strong tapes.

-

Rising focus on reducing carbon emissions is encouraging adoption of lightweight materials in transportation and industrial sectors.

-

Advances in resin systems compatible with carbon fiber tapes are improving thermal and chemical resistance for harsh environments.

Carbon Fiber Tapes Market Growth Drivers

-

Increasing Adoption of Electric Vehicles (EVs) Drives the Market Growth

The drive to electric mobility is adding significantly to demand for lightweight, high-strength materials that can help to make batteries more efficient and give vehicles a longer range. Carbon fiber tapes, especially prepreg tapes, are particularly well-suited to EV applications, such as battery enclosures, structural reinforcement, and underbody protection, as a result of their high stiffness-to-weight ratio. With increasing EV scale, these tapes provide a competitive edge in performance and efficiency for automakers.

For instance, in 2023, Teijin Automotive Technologies grew its Ohio composite plant to produce carbon-fiber-based EV components for automotive OEMs in the coming years, as growing demand.

Carbon Fiber Tapes Market Restraints

-

High Production and Material Costs May Hamper the Market Growth

High raw material prices and processing technologies are among the key factors deterring the evolution of the carbon fiber tapes market. Carbon fiber preparation for the manufacturing of carbon fiber these are energy-demanding process, including oxidation, carbonization, and surface treatment, which involve special equipment and qualified personnel. Prepreg tapes require particular control of resin impregnation and storage, and the manufacturing process is made complicated.

This makes the cost of carbon fiber tapes much higher than traditional materials, such as aluminum, steel, or even fiberglass. Consequently, their use is restricted to very-high-end industries, such as aerospace, military, and high-performance luxury automotive.

Carbon Fiber Tapes Market Opportunities

-

Infrastructure Retrofitting and Seismic Strengthening Create an Opportunity in the Market

Decrepit infrastructure in North America, Europe, and parts of Asia is opening up a big opportunity for advanced composite materials, such as carbon fiber tapes. These tapes are also particularly well suited for structural strengthening because of their high tensile strength, fatigue resistance, and corrosion resistance. As carbon fiber tapes do not corrode and have less added mass, they are ideal for use in applications ranging from bridge strengthening, seismic reinforcement, and pipeline and column wrap located within ocean environments, which drive the carbon fiber tapes market trends.

In earthquake-threatened parts globally, for instance, in California, Japan, and Turkey, carbon fiber tapes are being marketed to retrofit ageing buildings and structures. These application areas are also funded by the government and public-private partnerships, and hence the civil sector emerges as a promising field beyond aerospace and automotive.

For instance, in 2023, the U.S. Department of Transportation (DOT) awarded more than USD 1.2 billion in funding to bridge rehabilitation projects under the Infrastructure Investment and Jobs Act, including a pilot program.

Carbon Fiber Tapes Market Segment Highlights

By Form

Prepreg carbon fiber tape leads the market with over 62% share due to superior strength, uniform resin distribution, and ease of use in automated fiber placement, making it ideal for aerospace and defense applications with high performance and reduced processing time. Dry tapes are the fastest-growing segment, favored for cost-effective resin infusion and customization flexibility. Their scalability and affordability are driving adoption in wind energy, sports equipment, and other industries. The combination of high-performance prepregs and versatile dry tapes is shaping the carbon fiber tapes market, balancing efficiency, cost, and application-specific requirements.

By Resin Type

Epoxy resins dominate the carbon fiber tapes market with over 40% share due to their excellent mechanical strength, durability, and adhesion, making them ideal for structural aerospace components requiring long-term performance under extreme conditions. Thermoplastic resins are the fastest-growing segment, driven by demand for recyclable, impact-resistant materials in automotive and defense sectors. Their rapid processing, weldability, and suitability for high-volume production, especially in electric vehicle components, are boosting adoption. The combined use of high-performance epoxy and versatile thermoplastic resins is shaping the market, offering a balance of durability, sustainability, and production efficiency across industries.

By Grade

PAN-based carbon fibers lead the market due to their superior strength-to-weight ratio, widespread availability, and established production technology, making them ideal for commercial aviation, high-performance automotive, and sporting goods applications. High-modulus grades are the fastest-growing segment, offering exceptional stiffness for space and advanced aerospace structures. Their adoption is increasing in satellite panels and aircraft frames where minimal deflection is critical. The combination of versatile PAN-based fibers and specialized high-modulus grades enables the carbon fiber tapes market to address diverse performance requirements, from general industrial use to highly demanding aerospace and space applications.

By Manufacturing Process

The hot melt process dominates the carbon fiber tapes market with over 45% share, offering precise resin control, fast cure cycles, and environmental benefits, making it ideal for aerospace and automotive applications requiring consistency and speed. Pultrusion is the fastest-growing process, valued for high automation, cost efficiency, and continuous profile production. Its adoption is rising in civil infrastructure and marine components, enabling large-scale production with minimal labor. Together, these processes balance high-performance manufacturing with scalability, supporting diverse industry demands and driving growth in the carbon fiber tapes market across aerospace, automotive, infrastructure, and marine sectors.

By End-Use Industry

Aerospace & defense dominates the carbon fiber tapes market with over 55% share, driven by the demand for ultra-lightweight, high-strength components in aircraft, spacecraft, and defense systems, where stringent safety and performance standards make these materials indispensable. Automotive is the fastest-growing segment, fueled by vehicle electrification and strict fuel efficiency regulations. Carbon fiber tapes are increasingly used in battery enclosures, body-in-white structures, and crash safety components to reduce weight and improve range. The combined growth of aerospace and automotive applications underscores the market’s expansion, highlighting carbon fiber tapes’ critical role in high-performance, lightweight, and efficiency-focused industries.

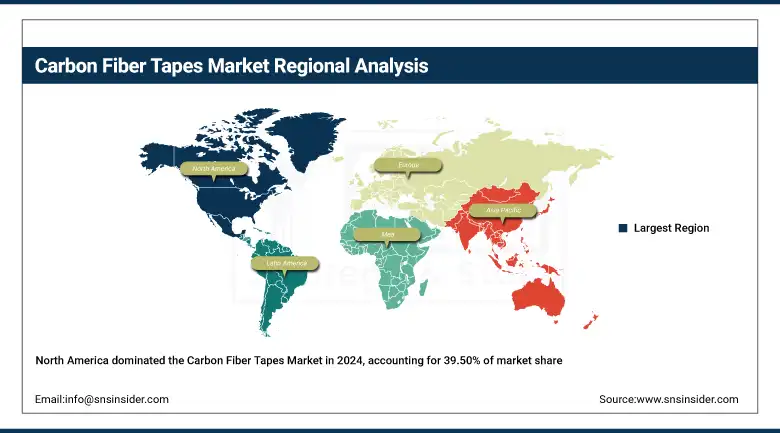

Carbon Fiber Tapes Market Regional Analysis

North America Carbon Fiber Tapes Market Insights

North America Carbon Fiber Tapes market held the largest market share, around 39.50%, in 2024. It is driven primarily by the presence of a highly-integrated aerospace & defense industry, a robust R&D infrastructure, and high demand for aircraft OEMs. The high product availability, and the presence of well-established companies such as Hexcel and Toray Composite Materials (America), ensures the high quality of the composite.

In July 2023, Toray Composite Materials America revealed a 30,000 sq. ft. expansion to its Spartanburg, SC plant, for 3,000 metric tons/year of carbon fiber for clean‑energy and aerospace applications, available in 2025. Toray Composite Materials America, Inc.+10Toray Composite Materials America, Inc.+10Textile World+10.

Get Customized Report as per Your Business Requirement - Enquiry Now

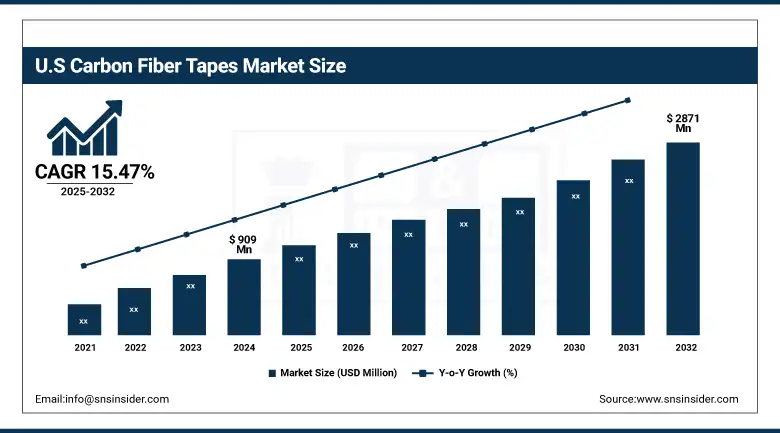

U.S. Carbon Fiber Tapes Market Insights

The U.S Carbon Fiber Tapes market size was USD 909 million in 2024 and is expected to reach USD 2871 million by 2032 and grow at a CAGR of 15.47% over the forecast period of 2025-2032. It is owing to the development of industries, such as military, aviation, clean energy structural materials. The U.S. defense and aerospace OEMs frequently require a domestic carbon fiber supply for strategic security. The sale of the company's assets was completed in November 2024, and Toray Advanced Composites has added 4,366m² of R&D and manufacturing floor space dedicated to thermoplastic carbon tape innovation and supply for defense and industrial customers in Englewood, Colorado.

Asia Pacific Carbon Fiber Tapes Market Insights

Asia Pacific is the fastest growing market in the carbon fiber tapes market as its aerospace, automotive, lightweight materials, and clean energy industries are growing substantially. Nations including China, Japan, South Korea, and India are investing considerably in in-country production of carbon composites in order to reduce dependence on imported carbon composite and to achieve green sustainability targets. Toray Industries, the biggest carbon fiber maker globally, has been increasingly seeking to expand its business operations in the region. Most recently, Toray has heightened its South Korea-based plant in Gumi in 2023 to meet pressure vessel and hydrogen storage tank demand for electric and fuel-cell vehicles.

Europe Carbon Fiber Tapes Market Insights

Europe has a significant contribution towards the carbon fiber tapes market as there are well-established automotive, aerospace, and wind energy sectors that look up to lightweight as well as high-performance materials to cut down on emissions and increase efficiency. R&D investment and collaboration with major composite companies in Germany, France, and the U.K. are the dominant markets. In the dominant industry is key domination or 10 years. One recent development is the Teijin Carbon Europe (formerly Toho Tenax) site in Heinsberg-Oberbruch, Germany, with one of the largest carbon fiber production plants in Europe, producing 5100 t/year. This established infrastructure enables high-volume supply to leading European OEMs, such as Airbus and BMW, which use carbon fiber tapes in aircraft and EV manufacturing.

Latin America Carbon Fiber Tapes Market Insights

The Latin America carbon fiber tapes market is gradually expanding, supported by the region’s growing aerospace, automotive, and renewable energy industries. Brazil and Mexico are at the forefront, driven by rising aircraft manufacturing partnerships, defense modernization, and the adoption of lightweight materials in vehicles. The wind energy sector is also boosting demand as carbon fiber tapes enhance turbine blade efficiency. Although adoption is at an early stage compared to North America and Europe, increasing investments in advanced composites manufacturing, coupled with sustainability initiatives, are expected to position Latin America as a promising growth hub for carbon fiber tapes.

Middle East & Africa Carbon Fiber Tapes Market Insights

The Middle East & Africa carbon fiber tapes market is witnessing steady growth, fueled by infrastructure development, aerospace investments, and defense sector modernization. The UAE and Saudi Arabia are leading markets, with rising demand for lightweight composites in aircraft, drones, and military applications. Additionally, the push toward renewable energy projects, including wind power installations, is opening new opportunities. In Africa, South Africa is emerging as a key market due to its automotive and industrial applications. While the market is still developing, government-backed industrial diversification and technological collaborations are expected to accelerate adoption across the region.

Competitive Landscape for Carbon Fiber Tapes Market

Hexcel Corporation, founded in 1948, is headquartered in Stamford, Connecticut, USA. It is a leading advanced composites company serving aerospace, defense, and industrial markets. Hexcel produces carbon fiber, reinforcement fabrics, prepregs, and resin systems, with carbon fiber tapes widely used in aerospace structures, wind energy, and automotive lightweighting. Its expertise in automated fiber placement materials positions it as a key player in high-performance composites.

-

In April 2024, Hexcel opened a new Center of Research & Technology Excellence in Salt Lake City, enhancing innovation in next-generation carbon fiber prepregs and tapes for aerospace and industrial applications.

Toray Industries Inc., established in 1926 and headquartered in Tokyo, Japan, is a global leader in advanced materials. The company operates across fibers & textiles, plastics, chemicals, environment, and life sciences. In carbon fiber tapes, Toray provides thermoset and thermoplastic solutions for aerospace, defense, and automotive applications. Its materials are critical for structural components, offering lightweight, high-strength performance.

-

In September 2023, Toray launched a new thermoplastic carbon fiber tape optimized for hydrogen storage tanks and electric vehicle components, supporting lightweight structures and expanding applications in sustainable mobility.

Teijin Limited, founded in 1918, is headquartered in Tokyo, Japan, with business segments spanning advanced fibers, composites, healthcare, and IT. In composites, Teijin develops high-performance carbon fiber tapes for aerospace, automotive, and industrial markets. Its offerings support fuel efficiency, structural integrity, and sustainable manufacturing.

-

In January 2024, Teijin announced the development of a new high-heat-resistant carbon fiber tape designed for next-generation aircraft engines, enabling components to withstand higher operating temperatures while improving overall engine efficiency.

Carbon Fiber Tapes Market Companies are:

-

Toray Industries Inc.

-

Teijin Limited

-

Mitsubishi Chemical Group

-

SGL Carbon

-

Gurit Holding AG

-

Park Aerospace Corp.

-

Royal DSM

-

Solvay S.A.

-

Celanese Corporation

-

Rhein Composite GmbH

-

TCR Composites

-

SHD Composite Materials Ltd.

-

North Thin Ply Technology (NTPT)

-

ATC Manufacturing

-

Cytec Engineered Materials

-

Cristex Composite Materials

-

PRF Composite Materials

-

TenCate Advanced Composites

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.06 Billion |

| Market Size by 2032 | USD 9.66 Billion |

| CAGR | CAGR of 15.47% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Form: Prepreg Tape, Dry Tape, Others (Woven Tape, Multi-axial Tape) •By Resin Type: Epoxy, Thermoplastic, Polyamide, Bismaleimide, Others (Vinyl Ester, Phenolic, Polyimide) •By Grade: PAN-based Carbon Fiber, Pitch-based Carbon Fiber, High-Strength Grade, High-Modulus Grade, Others (Intermediate Modulus Grade, Ultra-High Modulus, Recycled Carbon Fiber) •By Manufacturing Process: Hot Melt, Solvent Dip, Wet Layup, Pultrusion, Others (Dry Winding, Braiding) •By End-Use Industry: Aerospace & Defense, Automotive, Sports & Leisure, Marine, Others (Pipe & Tank, Construction & Infrastructure, Wind Energy, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | Hexcel Corporation, Toray Industries Inc., Teijin Limited, Mitsubishi Chemical Group, SGL Carbon, Zoltek Corporation, Gurit Holding AG, Park Aerospace Corp., Royal DSM, Solvay S.A., Celanese Corporation, RheinComposite GmbH, TCR Composites, SHD Composite Materials Ltd., North Thin Ply Technology (NTPT), ATC Manufacturing, Cytec Engineered Materials, Cristex Composite Materials, PRF Composite Materials, TenCate Advanced Composites |

Frequently Asked Questions

Ans. Policies supporting lightweight materials, defense modernization, EV incentives, and green energy mandates are driving demand and investments, especially in the U.S., EU, China, and Japan.

Ans Asia Pacific is the fastest-growing region, with strong investments in aerospace (e.g., COMAC in China), EVs, and infrastructure, along with growing domestic carbon fiber production capabilities.

Ans High production costs, limited recyclability, and complex processing techniques hinder wider adoption, especially in cost-sensitive industries like automotive and construction.

Ans Innovations include automated fiber placement (AFP), thermoplastic tape integration, dry tape for out-of-autoclave (OOA) processing, and improved resin infusion systems for faster, more sustainable production.

Ans. Asia Pacific and North America are the major growth hubs, driven by surging demand in aerospace, automotive, and renewable energy sectors, especially in China, India, Japan, and the U.S.

Get in Touch