Cargo Insurance Market Report Scope & Overview:

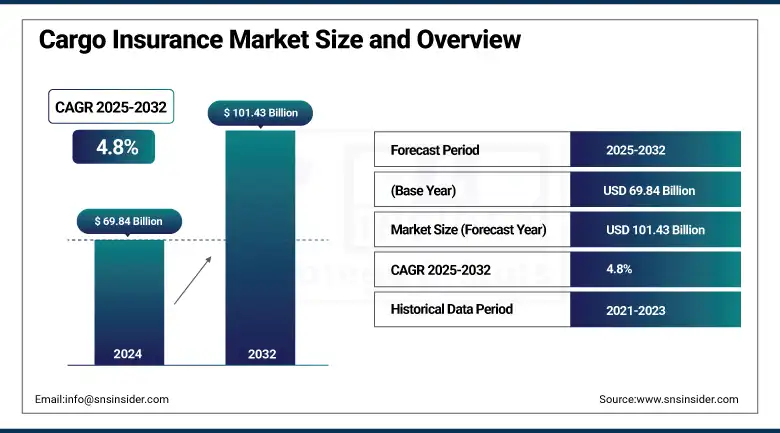

The Cargo Insurance Market size was valued at USD 69.84 billion in 2024 and is expected to reach USD 101.43 billion by 2032, expanding at a CAGR of 4.8% over the forecast period of 2025-2032.

The Cargo Insurance Market is part of the transportation and logistics sector that provides cover for goods that are carried and transported by air, land, and sea against risks such as theft, damage, and loss. Demand for different types of coverage, such as ocean, air, and land insurance, is driven primarily by increasing international trade and e-commerce. Flexible options such as single-trip, annual contract, and open cover policies are also suitable for businesses of all sizes. Furniture, manufacturing, retail, logistics, and other industries that transport high-value or perishable goods that are often lost and stolen benefit from cargo insurance, whether directly through shipping or indirectly during the collection of under-the-table pay. Asia Pacific leads the fastest growth region, while North America and Europe lead the value due to their advanced logistics network.

To Get more information On Cargo Insurance Market - Request Free Sample Report

According to research, AI-powered claims processing cuts settlement time from over 30 days to under 7, while blockchain-based digital policies reduce fraud risk by up to 25%.

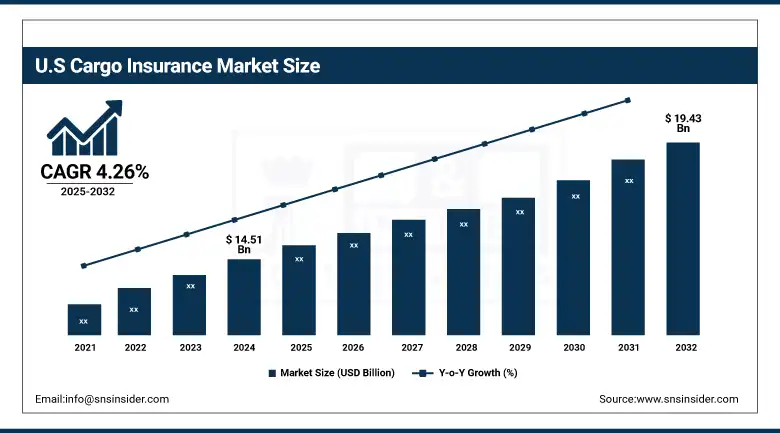

The U.S Cargo Insurance Market size reached USD 14.51 billion in 2024 and is expected to reach USD 19.43 billion in 2032 at a CAGR of 4.26% from 2025 to 2032.

The U.S. cargo insurance market leads the world, derived from its robust logistics infrastructure, large volume of trade, and rising risk management needs for cross-border cargoes. Expansion in e-commerce, increase in transportation of valuables and temperature-controlled freight, as well as rising inclination towards the use of digital platforms for real-time monitoring and claims processing are some of the key contributors to this growth. Moreover, the availability of major global insurers and rigorous regulatory requirements helps ensure full cargo coverage.

Market Dynamics:

Drivers:

-

Growing International Trade Volumes and E-Commerce Activities Drive the Demand for Comprehensive and Flexible Cargo Insurance Coverage Solutions

The growth of international trade and the explosion of e-commerce have led to a continuously rising demand for strong cargo insurance solutions. Businesses are shipping larger amounts of goods, often through multiple modes, thus requiring broader-based coverage that also needs to be more flexible. Insurance is used by e-commerce platforms behind their dream of speedy delivery for the customers since any sort of delay, damage, or loss causes risk problems. However, insurers began incorporating digital tools over the past few years, such as blockchain for transparent contracts and IoT for shipment tracking, thereby making risk management much more efficient.

According to the International Transport Forum, over 70% of global cargo now involves at least two modes of transport, increasing the need for flexible, multimodal insurance coverage.

Restraints:

-

High Insurance Premiums and Limited Awareness Among Small and Medium Enterprises Hinder Wider Adoption of Cargo Coverage Across Global Markets.

While cargo insurance is beneficial, many small and medium-sized enterprises still do not have it, mainly due to expensive premium rates and a lack of awareness of its usefulness. But a lot of SMEs either do not buy enough insurance for their goods or they go without insurance at all, putting themselves at risk for hefty payouts should the unfortunate happen. Complicated insurance nomenclature and relatively low ROI terms make for an uphill battle. However, cargo insurance market companies have begun to roll out accelerated, usage-based policies and awareness efforts for small and medium-sized enterprise businesses.

Opportunities:

-

Rising Integration of Artificial Intelligence and Blockchain Technology Creates Opportunities for Real-Time Risk Assessment and Faster Claims Management.

There are loads of opportunities waiting to be tapped in the cargo insurance sector, due to the opening up of some new fields by technological advancements such as the integration of AI and blockchain processes. It leverages AI for real-time risk modelling, predictive analytics, and automated decision-making, resulting in more accurate underwriting and timely claims settlement. It could guarantee concrete, transparent, real-time, and updated policy contracts for a trustworthy process along the entire logistics chain. This digital transformation not only increases efficiency but also caters to technology-minded clients who want their insurance to be faster and data-driven, in line with modern logistics and the complexities of global shipping.

Challenges:

-

Increasing Disruptions from Natural Disasters and Geopolitical Conflicts Pose Significant Challenges to Cargo Insurance Risk Management and Claim Payout Structures

More frequent natural disasters like floods and hurricanes, higher geopolitical tensions, are major headwinds for cargo grounds. These events make the risk assessment much harder and increase the loss ratios, but they are totally unpredictable. Incidents such as the Red Sea shipping crisis or European port strikes have brought up losses and costs in the insurance sector related to supply chain disruption. Companies are integrating climate modelling and geopolitical intelligence into their underwriting, but the volatility of global conditions is still overburdening risk frameworks and capital buffers.

Segment Analysis

By Type

In 2024, Ocean Cargo Insurance will dominate the market with a 52.31% share of the revenue. This places an emphasis on the dominance that these trade routes have, accounting for more than 80% of global trade by volume, although this is a myriad metric. This growth in the segment is due to increasing international trade and growing e-commerce, along with rising demand for imported goods. Since the Israel-Gaza conflict, brokers like Howden have introduced war risk cargo insurance for ships in high-risk zones like the Red Sea.

The Air Cargo Insurance segment is expected to grow at the fastest CAGR of 6.65%. The growth is driven by the rising need for quick delivery of high-value, time-sensitive goods, including electronics and pharmaceuticals. The segment benefits from an increase in air freight services and globalization of the supply chain. In this space, Parsyl is adding value by providing better tools around risk management by using sensors for temperature-sensitive shipments to lower their losses.

By Coverage

In 2024, Annual Contract Insurance will account for the largest revenue share, 40.54%. The segment holds a leading spot as it offers a cheaper and convenient option for businesses that ship regularly. With it, you will not have the related administrative burden and will get seamless protection coverage. This segment is driven by the growing complexity of supply chains and the need for continuous risk management solutions. This is making the segment more attractive to a wider variety of clients as insurers are creating specialized annual policies for specific industries.

Open Cover Insurance is anticipated to grow at the fastest CAGR of 6.06% during the forecast period. The increase comes from its ability to accommodate clients with ever-changing shipment amounts and shipment frequencies. This part of the segment is a better fit for businesses with less predictable shipping schedules and covers numerous shipments under one contract. Post-pandemic global trade recovery has contributed to a considerable increase in open cover policies as climbing cargo volumes lead to greater demand for all-in-one shipment coverage.

By Industry

The manufacturing industry segment leads the market with a revenue share of 34.38% in 2024. When manufacturers transport raw materials and finished goods, they are heavily reliant on cargo insurance policies to prevent the risk of financial loss. Driven by the increasing globalization of manufacturing operations and supply chains, the growth in the segment is significant. The provision of tailored insurance policies designed to mitigate sector-specific risks, such as equipment damage and production delays, is further strengthening the position of the segment in the global market.

The Retail segment is expected to have the strongest growth, with a CAGR of 6.77%. This expansion is driven by the rapid increase in e-commerce and the demand for logistics solutions to support people buying goods on the internet. With more losses being caused by the damage or the delay in the shipment, there is a growing demand from retailers for insured cargo. In response, insurers are crafting sector-specific policies, including immediate monitoring and fast claim procedures, which are then supporting the growth trajectory of the segment.

By Commodity

Bulk Cargo accounts for the fastest cargo insurance market share of 31.42% in 2024. Particularly bulk commodities, i.e., coal, grain, and minerals. It is primarily fueled by the continuous consumption of these basic commodities and the inherent danger of moving it across borders. To deal with challenges like spillage, contamination, and weather-related damages, insurers are coming up with tailored solutions to protect bulk cargo shipments.

The High-Value Goods segment is anticipated to witness the fastest CAGR of 6.48% over the forecast period. Such growth is propelled by the increase in cross-border transportation of high-value goods like luxury goods, electronics, pharmaceuticals, etc., which requires added service in-transit protection. With the help of IoT and Blockchain, insurers are providing real-time monitoring and high-value shipments documentation. These advancements play a significant role in reducing risks associated with theft and damage, thus bolstering the segment's growth.

By Scale

Large Enterprises account for 38.14% of the market revenue in 2024. Engaged in large amounts of international trade, they require all-risk cargo insurance products to protect their services. The growth is propelled by both the increasing complexity of large supply chains as well as the demand for tailored insurance policies. The tailored offerings, where integrated risk management services and focused support are being offered to fulfill the needs of large enterprises, further reinforce the leading position of this segment.

The SMEs segment is expected to grow at the fastest CAGR of 5.88%. The growth is also credited to the growing awareness of SMEs to participate in global trade and the need for them to realize the need for taking cargo insurance. The Indian government's subsidy scheme, launched in April 2024, is designed to stimulate marine cargo insurance among exporters, specifically SMEs, by minimizing the cost of insurance premiums and easing export risks.

Regional Analysis

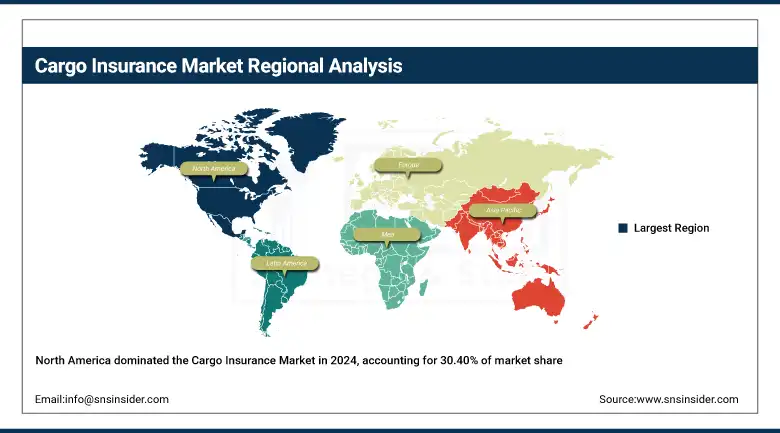

North America accounts for the largest market share of 30.40% due to its superior logistics network infrastructure, significant monetary value added to international trade, and a strong regulatory environment. Market growth is further fostered by the advancement of an ecosystem for a mature supply chain in the region and the penetration of digital insurance platforms. This growth is mainly driven by the surge in e-commerce shipments and the increasing demand for tailored insurance coverage solutions.

Get Customized Report as per Your Business Requirement - Enquiry Now

The United States dominates the North American market due to its massive trade volume, advanced transportation infrastructure, and widespread use of risk management solutions in freight and logistics.

Europe, being a major contributor to cross-border trade agreements, has the presence of established sea routes, the high uptake of risk management solutions, growing maritime tourism, and other factors for the European insurance market. Good oversight on insurance policies and international policyholders is provided by the top insurers who provide insurance across maritime, air, and land transport.

Germany ranks first in Europe due to its highly export-oriented economy, excellent connectivity, logistics hubs, and presence of various global cargo insurance providers.

The Asia Pacific is growing at the fastest rate, at a CAGR of 6.41%, due to the thriving of manufacturing, growing cross-border trade, and an increase in cargo movement through prominent shipping hubs. The ongoing market growth in the region is, thus, mainly attributed to the rapid infrastructure development and the growing awareness of the protection of cargo.

China dominates Asia Pacific due to its large export volume, extensive shipping networks, and increased demand for cargo coverage across manufacturing and e-commerce sectors.

The Middle East & Africa and Latin America are experiencing cargo insurance market growth due to various trade routes, infrastructural developments, and increasing export movements in the region, spearheaded by the UAE and Brazil as key hubs for logistics and trading activities, respectively.

Key Players

The major key players of the cargo insurance market are Allianz, Zurich Insurance Group, Generali, Liberty Mutual, Munich Re, AIG, Swiss Re, Tokio Marine, Lloyd’s of London, Chubb, and others.

Key Developments

-

In May 2024, Allianz Commercial expanded its project cargo insurance to cover high-value shipments, offering enhanced protection against transit damage, delays, and geopolitical risks for global infrastructure projects.

-

In February 2025, Helvetia Global Solutions partnered with insurtech Breeze to integrate advanced technology into cargo insurance, enhancing and streamlining international transport insurance solutions.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 69.84 Billion |

| Market Size by 2032 | USD 101.43 Billion |

| CAGR | CAGR of 4.8% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Ocean Cargo Insurance, Air Cargo Insurance, Land Cargo Insurance) •By Coverage (Single-Trip Insurance, Annual Contract Insurance, Open Cover Insurance) •By Industry (Manufacturing, Retail, Transportation, Logistics) •By Commodity (High-Value Goods, Bulk Cargo, Perishable Goods, Hazardous Cargo) •By Scale (Small and Medium Enterprises (SMEs), Large Enterprises) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Allianz, Zurich Insurance Group, Generali, Liberty Mutual, Munich Re, AIG, Swiss Re, Tokio Marine, Lloyd’s of London, Chubb. |

Frequently Asked Questions

North America dominated the Cargo Insurance Market in 2024, accounting for the largest market share of 30.40% due to its superior logistics infrastructure, significant trade value, and strong regulatory environment.

The Ocean Cargo Insurance segment dominated the market with a 52.31% revenue share in 2024, driven by its role in over 80% of global trade by volume.

The major growth factor is the growing international trade volumes and expansion of e-commerce activities, which increase demand for comprehensive and flexible cargo insurance coverage solutions.

The Cargo Insurance Market size was valued at USD 69.84 billion in 2024.

The expected CAGR of the Cargo Insurance Market is 4.8% over the forecast period from 2025 to 2032.

Get in Touch