Content Analytics Market Report Scope & Overview:

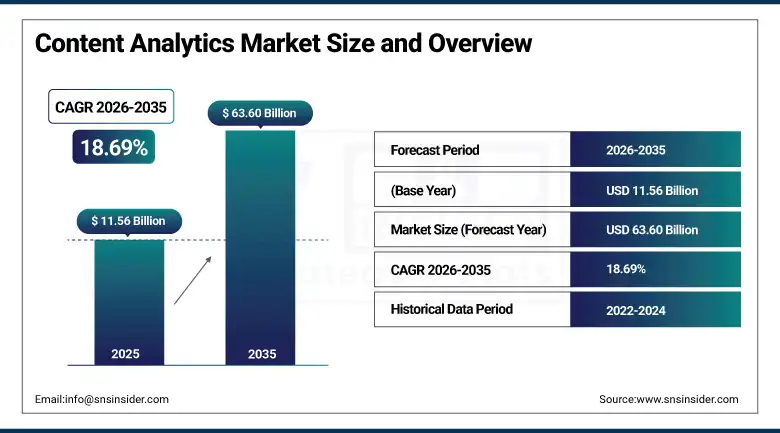

The Content Analytics Market was valued at USD 11.56 Billion in 2025 and is expected to reach USD 63.60 Billion by 2035, growing at a CAGR of 18.69% from 2026–2035.

The worldwide content analytics market is developing at an incredible rate. Content analytics refers to the study of using complex analytic tools, which include natural language processing, machine learning, and artificial intelligence, for obtaining valuable, structured information from unstructured data sources such as texts, web pages, social media updates, emails, audio transcripts, and other multimedia data sources. Organizations have started using AI-based content analytics in order to get meaningful insights from their unstructured data in various industry segments, including BFSI, retail, healthcare, and media.

The market is fueled by rising demand for analytics solutions, growing amount of unstructured enterprise data, and gradual incorporation of generative AI into content analytics platforms. The threat of data breaches within content analytics processes has necessitated greater emphasis on cybersecurity and compliance in order to safeguard sensitive data managed through content analytics.

In the year 2024, IBM Watson improved its ability to perform analytics on documents by adding new NLP models which were built for analyzing contracts and regulatory documents in order to be able to automatically extract the obligations and timelines contained within at an unprecedented speed. The expansion reflects the commercial recognition that the BFSI sector's extraordinary contract and regulatory document volume creates the most commercially valuable enterprise content analytics application whose automation ROI directly funds premium solution investment.

Market Size and Forecast

-

Market Size in 2026E: USD 13.72 Billion

-

Market Size by 2035: USD 63.60 Billion

-

CAGR: 18.69% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Content Analytics Market - Request Free Sample Report

Content Analytics Market Trends

-

Generative AI integration with content analytics platforms is enabling automated content summarization, insight extraction, and report generation from unstructured document collections.

-

Multimodal content analytics processing audio, video, images, and text within unified analytical frameworks is enabling new application categories for retail customer behavior analysis.

-

Real-time content analytics for social media sentiment monitoring, news event tracking, and competitive intelligence is creating demand for low-latency streaming analytics infrastructure.

-

Regulatory compliance content analytics for GDPR, CCPA, and sector-specific financial and healthcare regulation is creating structured institutional procurement.

-

Edge content analytics processing enabling local on-device content analysis without cloud data transmission is creating deployment capability for privacy-sensitive healthcare, financial, and government content analytics applications.

The U.S. Content Analytics Market Outlook

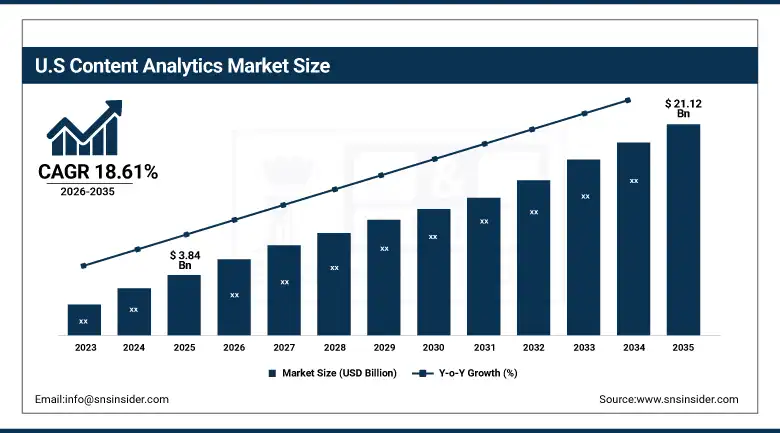

The U.S. content analytics market was valued at approximately USD 3.84 Billion in 2025 and is expected to reach approximately USD 21.12 Billion by 2035, growing at a CAGR of approximately 18.61%.

The U.S. is the world's most commercially sophisticated content analytics market within North America's dominant revenue position. IBM, Microsoft, SAP, SAS Institute, and OpenText's U.S. operations collectively define the commercial content analytics technology frontier. The extraordinary volume of enterprise unstructured data across financial contracts, healthcare clinical notes, legal documents, and customer communications creates the most commercially compelling content analytics ROI environment of any national market. FINRA and SEC's regulatory surveillance requirements, HIPAA's clinical documentation analysis mandate, and the legal sector's e-discovery content analytics adoption collectively create structured institutional content analytics procurement across high-value industry verticals.

For instance, Microsoft’s Azure AI Content Understanding service received a boost in 2025 with improved multimodal document intelligence, which allows companies to analyze complicated documents such as invoices, contracts, and regulatory statements and pull out relevant information. The company’s business model entails integration of the content analysis functionality within its cloud computing platform, where enterprises have established connections with Azure that facilitate natural consumption of the AI-powered content analysis services.

Content Analytics Market Segment Analysis

-

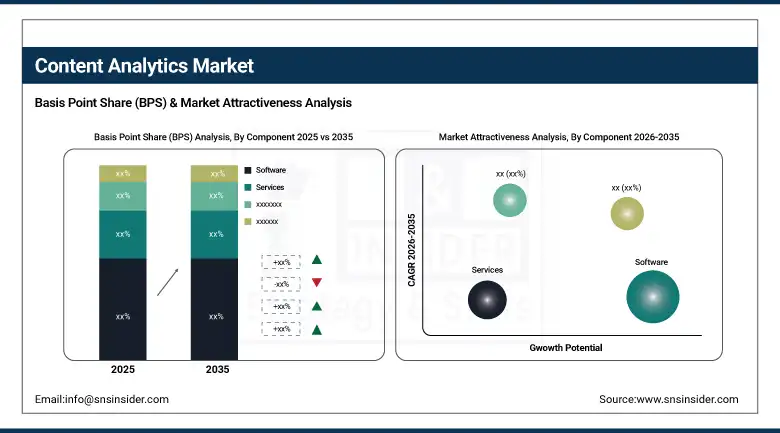

By Component, the software segment dominated the market with approximately 63% share in 2025, while the services segment is the fastest growing.

-

By Deployment Mode, the cloud-based segment dominated the market with approximately 58% share in 2025, while the on-premise segment is the fastest growing.

-

By Organization Size, the large enterprises segment dominated the market with approximately 65% share in 2025, while the small & medium enterprises segment is the fastest growing.

-

By End User, the BFSI segment dominated the market with approximately 28% share in 2025, while the healthcare & life sciences segment is the fastest growing.

By Component, software dominates, services grow fastest

Software retained the dominant component position with approximately 63% of the content analytics market in 2025. Content analytics software platforms encompassing NLP engines, text mining tools, and content intelligence dashboards collectively constitute the solution portfolio whose deployed technology creates the commercial infrastructure for enterprise content analytics capability. The software segment's dominance reflects the foundational requirement for deployed analytical technology whose configuration to specific enterprise content types, industry vocabularies, and analytical objectives creates the commercial relationships that sustain consistent procurement.

Services are the fastest-growing component because content analytics implementation's technical complexity creates consulting, integration, and managed service demand that substantially exceeds many enterprise analytics teams' internal capability. Each new content analytics programme deployment requires domain-specific model training, workflow integration with existing enterprise content management systems, and stakeholder training. Managed content analytics services that operate NLP models, monitor analytical quality, and deliver insight reports create recurring service revenue whose commercial momentum compounds with the enterprise market's growing outsourcing preference.

By End User, BFSI dominates, healthcare & life sciences grow fastest

BFSI retained the dominant end-user position with 28% of the content analytics market in 2025. The financial services industry's document volume, encompassing mortgage contracts, insurance policies, customer communications, and fraud investigations, creates the commercially compelling content analytics investment case of any industry vertical. Each financial institution's contract review automation ROI, calculated in analyst time saved across thousands of annual contract reviews, creates quantifiable payback. Regulatory surveillance of communication content for market abuse detection, GDPR compliance monitoring of customer data processing records, and AML transaction narrative analysis collectively create structured institutional content analytics procurement.

Healthcare and life sciences is the fastest-growing end user because the convergence of EHR clinical note analysis for disease progression research, medical literature mining for drug discovery intelligence, regulatory submission document review automation, and adverse event signal detection in pharmacovigilance databases creates multiple growth vectors in a single industry vertical. Each healthcare system that deploys NLP for clinical note coding automation creates content analytics procurement whose ROI is measured in reduced manual coding effort and improved billing accuracy.

By Deployment, cloud dominates, on-premise grows for regulated sectors

Cloud-based deployment retained the dominant position with approximately 58% of the content analytics market in 2025. Content analytics platforms’ cloud delivery creates scalability advantages whose elastic compute access enables large-volume document batch processing that on-premise hardware capacity limitations would require capital investment to match. Cloud-delivered NLP model updates create continuous performance improvement that on-premise deployments whose update cycles are governed by IT change management cannot match equivalently. The SaaS content analytics model’s subscription economics eliminate capital software licensing investment that creates adoption accessibility for Organizations whose analytics investment cycle previously excluded premium content analytics solutions.

On-premise deployment is the fastest-growing for regulated industries because financial services regulators’ data residency requirements and government classified content's security clearance processing restrictions create mandatory on-premise processing requirements that cloud delivery cannot satisfy regardless of cloud provider security certification. Each financial institution that must process client PII in regulated jurisdictions and each healthcare system that must maintain clinical data within sovereign boundaries creates on-premise content analytics infrastructure procurement whose regulatory compliance motivation sustains investment independently of cloud alternative cost comparison.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Content Analytics Market Insights

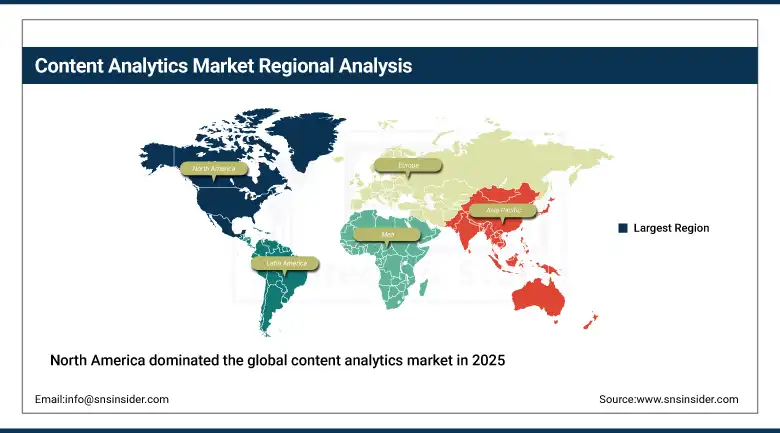

North America dominated the global content analytics market in 2025 as the most commercially advanced analytics adoption region. The United States accounts for approximately 87.4% of North American revenues through IBM, Microsoft, SAP, SAS Institute, and OpenText's commercial dominance, the financial services and healthcare sectors’ above-average content analytics ROI, and the extraordinarily large enterprise unstructured data volumes whose analysis creates the most commercially compelling content analytics investment cases globally.

Canada contributes approximately 12.6% of North American revenues through its financial services sector's analytics investment, the growing technology industry's AI content platform adoption, and the healthcare system's clinical documentation analysis programme.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Content Analytics Market Insights

Europe is a technically sophisticated content analytics market where GDPR's data governance requirements create both compliance use cases and data localization constraints that sustain on-premise and hybrid content analytics deployment. Germany accounts for approximately 22.3% of European revenues through its manufacturing sector's operational document analytics, the financial services industry's regulatory compliance content analysis, and SAP's domestic content analytics integration within enterprise platform deployments.

The United Kingdom and France are significant secondary markets where financial services regulatory surveillance requirements, legal sector e-discovery content analytics adoption, and the pharmaceutical industry's clinical document processing create consistent institutional content analytics procurement.

Asia Pacific Content Analytics Market Insights

Asia Pacific is the fastest-growing regional content analytics market, driven by China's extraordinary enterprise digital transformation investment, India's IT services sector's content analytics platform development for global clients, Japan's manufacturing sector's operational document analytics, and South Korea's technology industry's AI platform adoption. China accounts for approximately 44.8% of Asia Pacific revenues through its government digital economy programme, the financial services sector's regulatory compliance analytics, and the domestic technology company's content intelligence platform development.

India represents the most commercially dynamic emerging market within Asia Pacific where the IT services industry's content analytics platform service delivery for global clients creates above-average domestic capability development, and the rapidly growing domestic enterprise sector's analytics adoption creates expanding domestic content analytics procurement.

MEA & Latin America Content Analytics Market Insights

UAE leads MEA revenues at approximately 38.4% through its financial services sector's content analytics investment, the government's digital transformation initiative creating regulatory document analytics procurement, and the technology sector's AI platform adoption. Brazil leads Latin American revenues at approximately 44.2% through its financial services sector's LGPD compliance analytics, the large enterprise market's digital transformation investment, and the growing technology industry's content intelligence platform adoption.

Saudi Arabia's Vision 2030 digital economy investment and South Africa's financial services sector create significant MEA secondary markets whose content analytics procurement reflects the progressive enterprise AI adoption across both national markets.

Market Dynamics

Growth Drivers: Unstructured data explosion and gen AI integration creating systematic enterprise content analytics investment

The exponential growth of enterprise unstructured data is the content analytics market's most commercially certain structural growth driver. IDC projects that 80% of enterprise data will be unstructured by 2030, creating a data intelligence gap whose closing requires content analytics capability. Each new enterprise digital workflow that generates documents, emails, social content, and multimedia data creates proportional content analytics opportunity whose commercial scale grows with enterprise digitalization. The generative AI revolution's ability to process and extract structured insights from intractable unstructured content volumes is creating capability breakthroughs that substantially expand the addressable content analytics use case universe beyond what NLP-only approaches could previously serve.

Generative AI integration with content analytics platforms is creating the commercially transformative product capability advancement. Large language models whose ability to understand, and extract structured insights from complex enterprise documents creates analytical capability whose commercial value justifies premium platform investment. Each LLM-powered content analytics capability that replaces manual document review with automated insight extraction creates ROI whose quantification in analyst hours saved and error reduction sustains enterprise procurement momentum.

Restraints: Data privacy regulation constraining content analytics deployment and unstructured data quality variability

Data privacy regulation creates deployment constraints that limit content analytics reach across sensitive content categories. GDPR's purpose limitation principle restricts the repurposing of customer communication data for analytics that was not disclosed at collection, CCPA's opt-out requirements create data exclusion management complexity, and HIPAA's de-identification requirements for clinical text analytics create processing overhead that reduces analytical dataset completeness.

Unstructured data quality variability creates analytical accuracy challenges whose impact on content analytics output quality reduces business user confidence in automated insight recommendations. Each enterprise content analytics deployment that encounters inconsistent document formatting, multilingual content, domain-specific vocabulary creates accuracy reduction that moderates adoption momentum among business users whose performance expectations are calibrated to human analyst quality.

Opportunities: Generative AI content analytics platforms and regulated industry compliance automation

Generative AI content analytics platforms represent the commercially transformative near-term market development opportunity whose LLM-powered document understanding creates capabilities substantially beyond previous NLP-based approaches. Each enterprise that deploys GPT-4 or equivalent LLM-integrated content analytics for contract intelligence, regulatory monitoring, or customer communication analysis creates a commercial precedent whose demonstrated ROI sustains peer enterprise adoption at progressively faster adoption rates. The competitive pressure to automate content insight creates organizational motivation that sustains above-average AI content analytics investment.

Regulated industry compliance automation represents the most commercially certain near-term growth driver for content analytics premium solution specification. The regulatory environment's progressive increase in document volume and analytical sophistication requirement creates systematic compliance analytics investment that compounds with regulatory complexity growth.

Recent Developments:

-

2025: IBM expanded its watsonx AI-powered content analytics suite, focusing on enterprise document intelligence and automated knowledge extraction for regulated industries such as banking and healthcare.

-

2025: Microsoft expanded its Azure AI Content Understanding service in 2025 with enhanced multimodal document intelligence enabling enterprises to extract structured data from complex mixed-format documents including invoices, contracts, and regulatory filings at enterprise scale.

-

2025: SAS upgraded its SAS Viya platform, integrating generative AI for advanced text analytics, sentiment analysis, and content classification.

Content Analytics Market Key Players

-

IBM Corporation

-

Microsoft Corporation

-

SAP SE

-

SAS Institute Inc.

-

OpenText Corporation

-

Oracle Corporation

-

Google LLC (Google Cloud)

-

Amazon Web Services

-

Adobe Inc.

-

NICE Systems

-

Verint Systems

-

Clarabridge (Qualtrics)

-

Coveo Solutions Inc.

-

Sinequa

-

BA Insight

-

Elasticsearch (Elastic NV)

-

Attivio Inc.

-

Salesforce

-

Mindbreeze GmbH

-

Linguamatics (IQVIA)

Content Analytics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.56 Billion |

| Market Size by 2035 | USD 63.60 Billion |

| CAGR | CAGR of 18.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Deployment Mode (Cloud-Based, On-Premise, Hybrid) • By Organization Size (Large Enterprises, Small & Medium Enterprises) • By End User (BFSI, Retail & E-Commerce, Healthcare & Life Sciences, IT & Telecom, Media & Entertainment, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Microsoft Corporation, SAP SE, SAS Institute Inc., OpenText Corporation, Oracle Corporation, Google LLC (Google Cloud), Amazon Web Services, Adobe Inc., NICE Systems, Verint Systems, Clarabridge (Qualtrics), Coveo Solutions Inc., Sinequa, BA Insight, Elastic NV (Elasticsearch), Attivio Inc., Salesforce, Mindbreeze GmbH, Linguamatics (IQVIA) |

Frequently Asked Questions

The Content Analytics Market was valued at USD 11.56 Billion in 2025.

The Content Analytics Market is expected to grow at a CAGR of 18.69% from 2026 to 2035.

Exponential growth of enterprise unstructured data creating analytical intelligence gaps whose closing requires AI-powered content analytics, and generative AI integration.

Software dominated the Content Analytics Market.

North America dominated the Content Analytics Market in 2025.

Get in Touch