Carotenoids Market Report Scope & Overview:

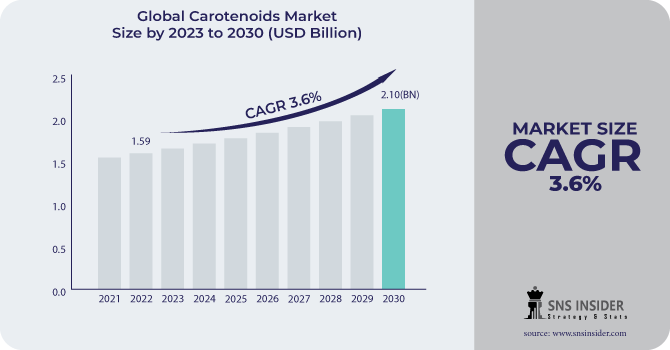

The Carotenoids Market size was USD 1.59 billion in 2022 and is expected to Reach USD 2.10 billion by 2030 and grow at a CAGR of 3.6 % over the forecast period of 2023-2030.

Carotenoids are a class of natural pigments that are produced by plants, algae, and some bacteria. They are responsible for the yellow, orange, and red colors of many fruits, vegetables, and flowers. Carotenoids are also found in some animals, such as salmon and shrimp.

The Carotenoids Market is segmented based on Type as Annatto, Canthaxanthin, Astaxanthin, Beta-carotene, Lutein, Zeaxanthin, Lycopene, and Others. Beta-carotene and Astaxanthin are the largest growing segment due to high utilization in end-user industries. These segments are two naturally occurring carotenoids that can be employed in a number of food and beverage applications. Consumers want more natural food and colorants. The industry is driven by the potential involvement of the aforementioned pigments in enhancing immunity, enhancing health, reducing diabetes, and providing several important health advantages.

By application, the animal feed segment is predicted to account for the largest market. The demand for nutrient-rich animal feed for domestic animals and cattle is rising. Due to their coloring abilities, carotenoids are widely employed in animal nutrition products and are included in the coloration of fish, crustaceans, egg yolks, and broiler skin.

MARKET DYNAMICS

KEY DRIVERS

-

Increase demand for personal care and cosmetic products

-

Increasing Demand for Natural Colorant

As consumers seek more transparency in their food and beverages and as marketers tout the usage of natural colors, the buyer's purchasing interest rises. When the label specifies fruit and vegetable juices and concentrates as colorings included in the ingredient declaration, consumers have a favorable perception of the brand. Anthocyanins, such as grape skin extract, give fruits and vegetables their red, blue, and purple colors. Carotenoids, including lycopene in tomatoes and beta-carotene in carrots, provide a variety of colors from yellow to red. The carotenoid market is being driven by a growing awareness of and use of naturally occurring colors from sources like tomatoes and carrots.

RESTRAIN

-

High prices of carotenoids

Synthetic carotenoids are produced by chemical synthesis. The production of synthetic carotenoids process is less complex and less expensive, which makes it more affordable than natural carotenoids. Carotenoids are a group of natural pigments that are extracted from algae, plants, and bacteria. This process involves using solvents and other chemicals, which can add to the cost of the carotenoids.

OPPORTUNITY

-

Potential benefits of carotenoids

It is believed that dietary carotenoids have health benefits by lowering the risk of disease, especially some malignancies and eye conditions. Beta-carotene, lycopene, lutein, and zeaxanthin are the carotenoids that have been most extensively researched in this regard. Carotenoids' antioxidant properties are thought to contribute in some measure to their positive benefits. Due to its capacity to be transformed into vitamin A, beta-carotene may offer additional advantages. Additionally, because lutein and zeaxanthin absorb harmful blue light that enters the eye, they may be preventive against eye illness. While a variety of fruits and vegetables contain these chemicals, tomatoes and tomato-related products are the main food sources of lycopene. Additionally, lutein and zeaxanthin can be found in egg yolks and are highly bioavailable. There are supplements that include these carotenoids.

CHALLENGES

-

Availability of synthetic carotenoids

Synthetic carotenoids are cheaper than natural carotenoids and they act as the best substitute, and they are often used in food and beverage products. This can pose a challenge to the natural carotenoids market.

IMPACT OF RUSSIA UKRAINE WAR

Russia and Ukraine are major producers of carotenoids, accounting for a combined share of 15% of the global market. The war has disrupted production and exports of carotenoids from Russia and Ukraine, leading to shortages in the global market. This is notably true for astaxanthin, a carotenoid used in dietary supplements, cosmetics, and aquaculture, among other uses. Prices for these goods have increased as a result of the scarcity of carotenoids. Astaxanthin, lutein, and zeaxanthin are produced in a BASF facility in Russia. War has caused Kemin Industries Inc. (Ukraine) and other important players to delay production.

IMPACT OF ONGOING RECESSION

The recession has impacted the global market of carotenoids. Food coloring used in the food sector is a significant source of carotenoids. Through 2022, the US market for food and beverage natural colors is anticipated to grow by 7.9% yearly. But the manufacture has been delayed because to carotenoid price increases. Natural carotenoid prices range from USD 350/kg to USD 7,500/kg, while synthetic carotenoid prices range from USD 250/kg to USD 2,000/kg. This difference in the prices is also the major reason for the manufacturers to choose synthetic carotenoids.

MARKET SEGMENTATION

By Type

-

Annatto

-

Astaxanthin

-

Beta-carotene

-

Canthaxanthin

-

Lutein

-

Lycopene

-

Zeaxanthin

-

Others

By Source

-

Natural

-

Synthetic

By Application

-

Animal Feed

-

Food & Beverages

-

Dietary Supplements

-

Cosmetics

-

Pharmaceuticals

.png)

REGIONAL ANALYSIS

Europe was the largest market, with revenue predicted to expand at a CAGR of 4.0% from 2022 to 2025 due to rising demand for health supplements and animal feed. The presence of prominent manufacturers such as Unilever, L'Oréal, Henkel, and Beiersdorf in the region is expected to be a major factor affecting growth in the region. Furthermore, rising food safety concerns in the United Kingdom are driving manufacturers to adopt clean labeling, fueling demand for carotenoids.

Asia-Pacific is the fastest-growing region, with an increasing number of customers opting for illness-prevention methods such as health supplements. Consumer-changing lifestyles and food consumption patterns have also contributed to the growth of the Asia-Pacific carotenoid market. Furthermore, economic expansion, technical developments, industrial growth, and low manufacturing costs in nations like as China, Japan, and India are expected to fuel the industry.

North America has the largest carotenoid market, owing to the growing demand for clean-label foods and health awareness. This market's expansion can be attributed to expanding awareness of the health advantages of carotenoids, rising demand for natural food colors, and rising demand for dietary supplements.

South America has grown significantly as the pharmaceutical and energy industries have expanded. These chemicals are increasingly being used in feed, food, supplements, cosmetic, and medicinal applications.

REGIONAL COVERAGE

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

KEY PLAYERS

Some major key players in the Carotenoids Market are NovoNutrients, Kemin Industries, BASF SE, Allied Biotech, Brenntag, Cyanotech Corp., Chr. Hansen, D.D. Williamson, Divis Laboratories, DSM Nutritional Products, Naturex SA, Lycored., and other key players.

NovoNutrients-Company Financial Analysis

RECENT DEVELOPMENTS

In 2023, NovoNutrients announced an advancement in carotenoid manufacturing technology. For every ton of protein-rich component, the company's overall carbon capture technique upcycles nearly two tons of carbon dioxide.

In 2023, LifeMeter, a portable, non-invasive instrument proven to assess the amount of important antioxidants known as carotenoids, is being introduced by MacuHealth, the leader in novel eye supplements. At the 2023 Vision Source Exchange in San Antonio, Texas, a device demonstration is taking place.

| Report Attributes | Details |

| Market Size in 2022 | US$ 1.59 Billion |

| Market Size by 2030 | US$ 2.10 Billion |

| CAGR | CAGR of 3.6 % From 2023 to 2030 |

| Base Year | 2022 |

| Forecast Period | 2023-2030 |

| Historical Data | 2019-2021 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Annatto, Canthaxanthin, Astaxanthin, Beta-carotene, Lutein, Zeaxanthin, Lycopene, and Others) • By Source (Natural and Synthetic) • By Application (Animal Feed, Dietary Supplements, Food & Beverages, Cosmetics, and Pharmaceuticals) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | NovoNutrients, Kemin Industries, BASF SE, Allied Biotech, Brenntag, Cyanotech Corp., Chr. Hansen, D.D. Williamson, Divis Laboratories, DSM Nutritional Products, Naturex SA, Lycored. |

| Key Drivers | • Increase demand for personal care and cosmetic products • Increasing Demand for Natural Colorant |

| Market Restrain | • High prices of carotenoids |

Frequently Asked Questions

Ans: Challenges are availability of synthetic carotenoids.

Ans: Asia Pacific region is the fastest-growing in the Carotenoids Market.

Ans: USD 2.10 billion is expected to grow by 2030.

Ans: Drivers are increasing demand for personal care and cosmetic products and increasing Demand for Natural colorants.

Ans: Carotenoids Market is anticipated to expand by 3.6 % from 2023 to 2030.

Get in Touch