Cell & Gene Therapy Manufacturing Services Market Report Scope & Overview:

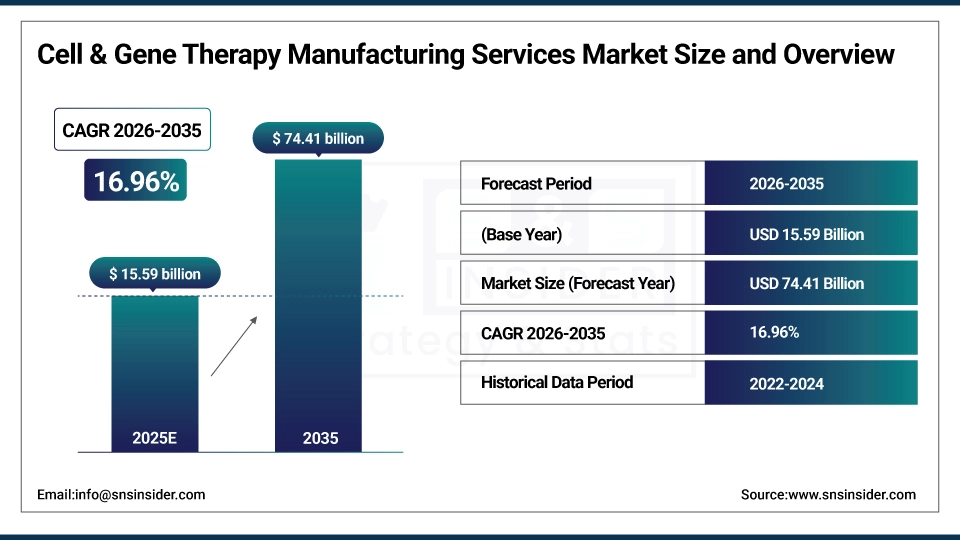

The Cell & Gene Therapy Manufacturing Services Market size is estimated at USD 15.59 billion in 2025 and is expected to reach USD 74.41 billion by 2035, growing at a CAGR of 16.96% over the forecast period of 2026-2035.

The global cell & gene therapy manufacturing services market trend is a growing demand for advanced therapeutic manufacturing solutions such as viral vector production, cell processing platforms, and gene editing technologies. The growth of the market is driven by increasing clinical trial activities, regulatory approvals for cell and gene therapies, and pharmaceutical industry investment in personalized medicine. Also driven by a growing adoption of contract manufacturing models and the growing focus on scalable manufacturing infrastructure as biotechnology companies become more focused on accelerating therapy commercialization and are more willing to invest in specialized manufacturing technologies, resulting in growth in the domestic and international market for pre-commercial and commercial-scale manufacturing services.

Cell & Gene Therapy Manufacturing Services Market Size and Forecast:

-

Market Size in 2025: USD 15.59 billion

-

Market Size by 2035: USD 74.41 billion

-

CAGR: 16.96% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Cell & Gene Therapy Manufacturing Services Market - Request Free Sample Report

Cell & Gene Therapy Manufacturing Services Market Trends

-

Cell & gene therapy manufacturing services are being adopted because biotechnology companies demand specialized manufacturing expertise, regulatory compliance support, and scalable production infrastructure.

-

Customized manufacturing platforms based on therapy modality, target indication, and production scale to improve therapy development outcomes.

-

The development of automated cell processing systems, closed manufacturing platforms, and real-time analytics to improve the manufacturing efficiency and reduce contamination risks.

-

Integrated workflow solutions, end-to-end manufacturing services, and technology transfer support are all available to ensure continuous production capability and regulatory submission readiness.

-

Increased demand for single-use manufacturing systems, modular cleanroom facilities and flexible production capacity to help reduce capital expenditure and improve operational efficiency.

-

Collaboration between pharmaceutical companies, contract development manufacturing organizations and technology providers to develop standardized manufacturing processes and improve therapy accessibility.

-

FDA, EMA and regulatory agencies promoting standards for manufacturing quality, GMP compliance, potency testing requirements, and chemistry manufacturing controls documentation.

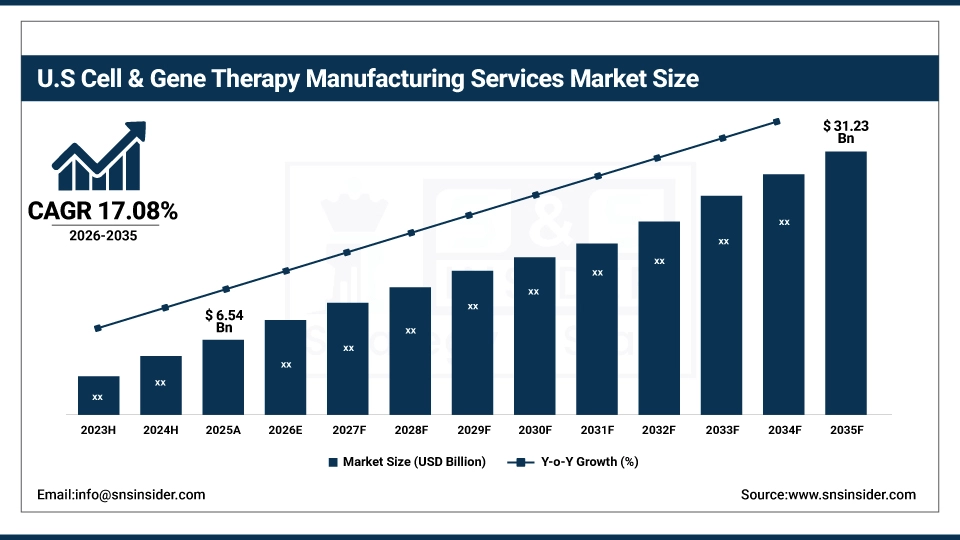

The U.S. Cell & Gene Therapy Manufacturing Services Market is estimated at USD 6.54 billion in 2025 and is expected to reach USD 31.23 billion by 2035, growing at a CAGR of 17.08% from 2026-2035. The United States represents the largest market for cell & gene therapy manufacturing services, primarily driven by the extensive biotechnology sector presence, federal support for regenerative medicine, and well-developed contract manufacturing infrastructure. Government funding programs, high levels of venture capital investment and increased pharmaceutical company spending on advanced therapy development help to drive growth in the market.

Cell & Gene Therapy Manufacturing Services Market Growth Drivers:

-

Increasing Regulatory Approvals and Clinical Pipeline Expansion are Driving the Cell & Gene Therapy Manufacturing Services Market Growth

Increasing regulatory approvals and clinical pipeline expansion take the center stage as a growth driver for the cell & gene therapy manufacturing services market share, and are driven by the implementation of expedited regulatory pathways, breakthrough therapy designations, and regenerative medicine advanced therapy standards for accelerated therapy development and commercial manufacturing readiness. These solutions for advanced therapeutic manufacturing and quality assurance are driving the base of the market, the penetration of contract manufacturing & in-house markets, and adding to the overall market share globally.

For instance, in June 2024, commercial-scale and integrated manufacturing solutions accounted for ~59% of the total global cell & gene therapy production investments, reflecting growing institutional preference and expanding market share.

Cell & Gene Therapy Manufacturing Services Market Restraints:

-

High Manufacturing Costs and Technical Complexity are Hampering the Cell & Gene Therapy Manufacturing Services Market Growth

High manufacturing costs & technical complexity of cell & gene therapy production also restrict the cell & gene therapy manufacturing services market growth, as a large number of emerging biotechnology companies face difficulties establishing specialized manufacturing capabilities and maintaining stringent quality control standards. This might lead to production bottlenecks, limited therapy accessibility, and reduced return on investment for therapy developers. As a result, therapy commercialization timelines suffer, and market growth is stunted in regions where manufacturing infrastructure is limited and specialized workforce availability is scarce.

Cell & Gene Therapy Manufacturing Services Market Opportunities:

-

Automation and Process Innovation Drive Future Growth Opportunities for the Cell & Gene Therapy Manufacturing Services Market

The opportunity in the automation and process innovation in cell & gene therapy manufacturing services market is in the form of robotic cell processing, artificial intelligence-driven quality control, and continuous manufacturing systems. These solutions provide for reduced manual intervention, individualized therapy production optimization, and real-time process monitoring. Through enhanced manufacturing consistency, reduced production timelines, and improved cost efficiency, particularly in areas with high therapy demand, these technologies may improve patient access, decrease manufacturing costs, and expand the market.

For instance, in April 2024, the FDA reported that 76% of approved cell & gene therapies utilized advanced manufacturing platforms with automated processing capabilities, highlighting rising technology adoption and increasing demand for innovative manufacturing solutions.

Cell & Gene Therapy Manufacturing Services Market Segment Analysis

-

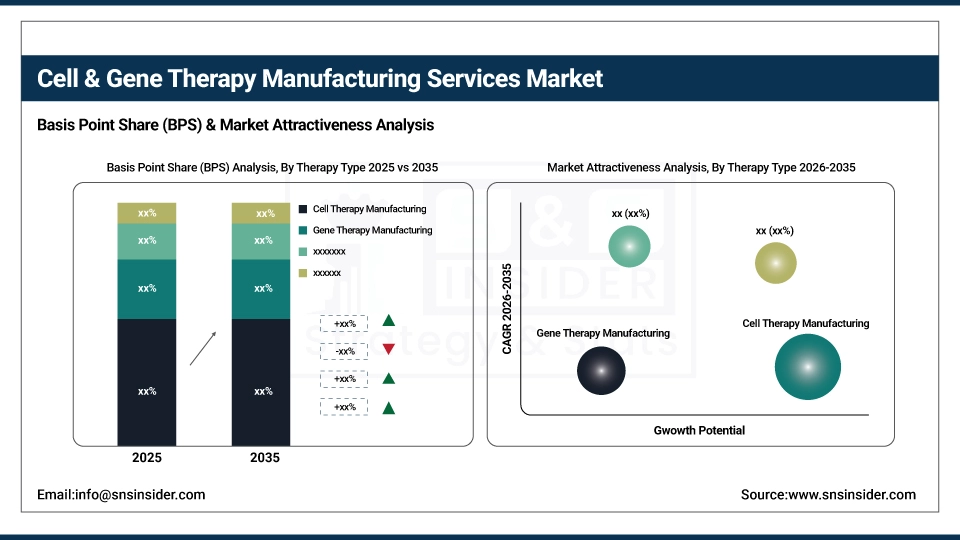

By therapy type, cell therapy manufacturing held the largest share of around 56.72% in 2025E, and the gene therapy manufacturing segment is expected to register the highest growth with a CAGR of 18.34%.

-

By manufacturing scale, the commercial scale manufacturing segment dominated the market with approximately 58.16% share in 2025E, while the pre-commercial/R&D scale manufacturing is expected to register the highest growth with a CAGR of 17.45%.

-

By manufacturing mode, contract manufacturing accounted for the leading share of nearly 64.89% in 2025E, and is expected to register the highest growth with a CAGR of 17.23%.

By Therapy Type, Cell Therapy Manufacturing Leads the Market, While Gene Therapy Manufacturing Registers Fastest Growth

The cell therapy manufacturing segment accounted for the highest revenue share of approximately 56.72% in 2025, owing to established manufacturing protocols for CAR-T cell therapies, extensive clinical experience with stem cell processing, and regulatory pathway clarity for autologous cell products. Emerging trends, including increasing adoption of allogeneic cell therapy approaches and growing investment in cell banking infrastructure.

The gene therapy manufacturing segment is anticipated to achieve the highest CAGR of nearly 18.34% during the 2026–2035 period, driven by the increasing number of gene therapy clinical trials, advancements in viral vector production technologies, and growing approval of gene editing therapeutics. Drivers include rising adoption of AAV vector manufacturing, the preference for lentiviral and retroviral production capabilities.

By Manufacturing Scale, the Commercial Scale Manufacturing Segment dominates, while the Pre-Commercial/R&D Scale Manufacturing Segment Shows Rapid Growth

By 2025, the commercial scale manufacturing segment contributed the largest revenue share of 58.16% due to increasing therapy commercialization, revenue generation from marketed products and established manufacturing process validation. Growing adoption of large-scale bioreactor systems coupled with automated filling operations, companies are increasingly investing in commercial manufacturing capacity.

The pre-commercial/R&D scale manufacturing segment is projected to grow at the highest CAGR of about 17.45% between 2026 and 2035 due to the growing number of clinical trial initiations and demand for flexible manufacturing platforms. Some of the reasons include enhanced process development needs, better technology optimization requirements, and biotechnology startups' preference for outsourced development services.

By Manufacturing Mode, Contract Manufacturing Leads, and Registers Fastest Growth

The contract manufacturing segment accounted for the largest share of the cell & gene therapy manufacturing services market with about 64.89%, owing to capital efficiency advantages, access to specialized manufacturing expertise, and risk mitigation for therapy developers. Reasons driving the contract manufacturing segment include increasing outsourcing preferences and regulatory compliance support needs, also grow at the fastest rate with a CAGR of around 17.23% throughout the forecast period of 2026–2035, as biotechnology companies seek comprehensive manufacturing partnerships, technology transfer capabilities, and global manufacturing network access. Increased focus on core competency development and reduced time to market contribute to their adoption, while improved manufacturing flexibility and cost optimization drive continued investment.

Cell & Gene Therapy Manufacturing Services Market Regional Highlights:

North America Cell & Gene Therapy Manufacturing Services Market Insights:

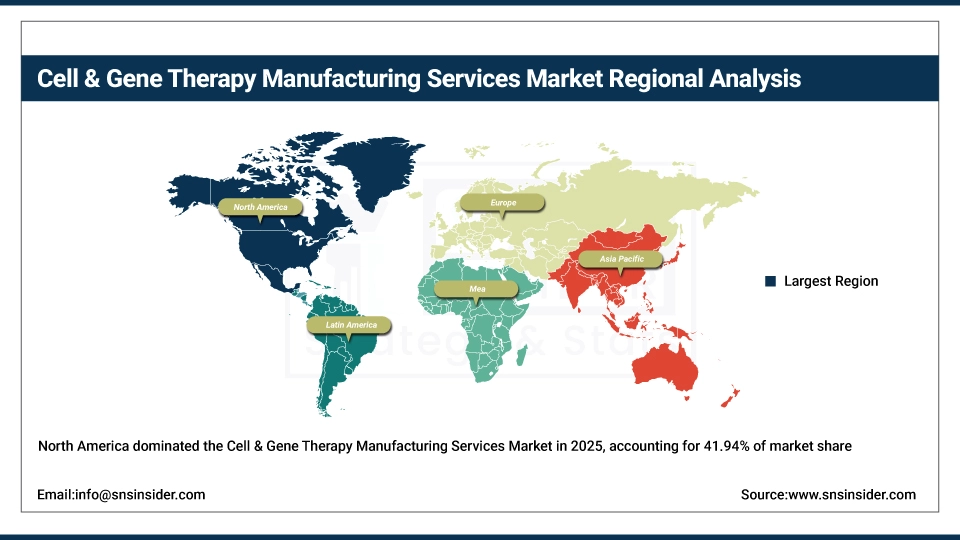

North America held the largest revenue share of over 41.94% in 2025 of the cell & gene therapy manufacturing services market due to an established biotechnology industry infrastructure, strong venture capital funding ecosystem, and increased pharmaceutical company investment in regenerative medicine. Include ubiquitous presence of contract development manufacturing organizations, an advanced regulatory environment, growing academic medical center collaboration and greater acceptance of autologous and allogeneic therapy manufacturing stemming from clinical success rates. At the same time, various government initiatives, FDA regenerative medicine programs and enormous investments in manufacturing technology from biotechnology companies are anchoring cell & gene therapy manufacturing services in the market, and ensuring multibillion dollar revenues around the world.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Cell & Gene Therapy Manufacturing Services Market Insights:

Asia Pacific is the fastest-growing segment in the cell & gene therapy manufacturing services market with a CAGR of 19.27%, as the awareness about advanced therapy benefits, government biotechnology development initiatives, and manufacturing infrastructure investment in developing nations is growing. Factors including rapid clinical research expansion, rising pharmaceutical company presence with manufacturing facility establishment, and growing adoption of international manufacturing standards are stimulating the market growth. Contract manufacturing organization growth and skilled workforce availability have been instrumental in improving manufacturing capacity, especially in countries with emerging biotechnology sectors. Public-private partnerships and regulatory harmonization efforts also help in advancing therapy development and commercial manufacturing capabilities. Increase in demand in Asia Pacific region owing to rising healthcare expenditure against historical spending levels and growing cost competitiveness and accessibility of specialized manufacturing services.

Europe Cell & Gene Therapy Manufacturing Services Market Insights:

The cell & gene therapy manufacturing services market in Europe is the second-dominating region after North America on account of an increase in the adoption of advanced therapy medicinal product regulations, robust pharmaceutical manufacturing infrastructure, and increasing therapy development initiatives across healthcare systems. Rising implementation of EMA regulatory frameworks, advanced cell processing facilities, favorable government funding for regenerative medicine research, and cross-border manufacturing network development are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Cell & Gene Therapy Manufacturing Services Market Insights:

In Latin America, and Middle East & Africa, the growing biotechnology sector development and increase in clinical research activity with manufacturing partnership formation support the cell & gene therapy manufacturing services market growth. The rising popularity of technology transfer programs and regional manufacturing capability building, along with international pharmaceutical company collaboration, will aid therapy accessibility and manufacturing capacity expansion. The increasing healthcare infrastructure investment and improving regulatory framework maturity in these regions are continuing to encourage market growth.

Cell & Gene Therapy Manufacturing Services Market Competitive Landscape:

Lonza Group AG (est. 1897) is a leading contract development and manufacturing organization that focuses on integrated biotechnology production solutions for pharmaceutical and healthcare industries. It uses its comprehensive manufacturing network and advanced production capabilities to produce cutting-edge cell & gene therapy manufacturing services with seamless process development and commercial scale production integration.

-

In February 2025, it expanded its cell & gene therapy manufacturing capacity with a new automated processing facility in Switzerland, aiming to improve viral vector production efficiency and autologous therapy manufacturing capabilities across its global client network.

Thermo Fisher Scientific Inc. (est. 1956) is a well-known global life sciences company focused on analytical instruments, laboratory equipment, and bioproduction services. It invests in modular cleanroom systems and single-use manufacturing platforms with the hopes of revolutionizing advanced therapy production with secure, scalable, and technology-enabled manufacturing solutions.

-

In May 2024, launched an enhanced cell processing platform featuring closed-system manufacturing and integrated quality analytics across global pharmaceutical markets, enhancing production consistency, regulatory compliance automation, and manufacturing throughput optimization.

Catalent Biologics (est. 1933) is a leading contract development and manufacturing organization in the fields of gene therapy vector production, cell therapy processing, and clinical trial material manufacturing. The company's manufacturing service portfolio focuses on end-to-end development support and flexible production capacity, and features a strong commitment to regulatory excellence and continuous innovation to complement the strong market presence in both clinical and commercial manufacturing settings.

-

In September 2024, introduced advanced viral vector production capabilities and expanded gene therapy manufacturing capacity for its global facility network, strengthening AAV production capabilities and expanding adoption among biotechnology companies developing gene editing therapeutics.

Cell & Gene Therapy Manufacturing Services Market Key Players:

-

Lonza Group AG

-

Catalent Biologics

-

WuXi AppTec

-

Samsung Biologics

-

Fujifilm Diosynth Biotechnologies

-

Charles River Laboratories

-

MilliporeSigma

-

Oxford Biomedica

-

Cobra Biologics

-

Cognate BioServices

-

MaxCyte Inc.

-

Minaris Regenerative Medicine

-

Cell and Gene Therapy Catapult

-

Cytiva

-

Waisman Biomanufacturing

-

Paragon Bioservices

-

RoosterBio Inc.

-

Andelyn Biosciences

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.59 Billion |

| Market Size by 2035 | USD 74.41 Billion |

| CAGR | CAGR of 16.96% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Therapy Type [Cell therapy manufacturing (Stem cell therapy, Non stem cell therapy), Gene therapy manufacturing] • By Manufacturing Scale [Pre-commercial/R&D scale manufacturing, Commercial scale manufacturing] • By Manufacturing Mode [Contract manufacturing, In-house manufacturing] • By Workflow [Cell processing, Cell banking, Process development, Fill & finish operations, Analytical and quality testing, Raw material testing, Vector production, Others] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Lonza Group AG; Thermo Fisher Scientific Inc.; Catalent Biologics; WuXi AppTec; Samsung Biologics; Fujifilm Diosynth Biotechnologies; Charles River Laboratories; MilliporeSigma; AGC Biologics; Oxford Biomedica; Cobra Biologics; Cognate BioServices; MaxCyte Inc.; Minaris Regenerative Medicine; Cell and Gene Therapy Catapult; Cytiva; Waisman Biomanufacturing; Paragon Bioservices; RoosterBio Inc.; Andelyn Biosciences |

Frequently Asked Questions

Ans: North America dominated the Cell & Gene Therapy Manufacturing Services Market in 2025.

Ans: The Cell Therapy Manufacturing segment dominated the Cell & Gene Therapy Manufacturing Services Market in 2025.

Ans: Increasing Regulatory Approvals and Clinical Pipeline Expansion are Driving the Cell & Gene Therapy Manufacturing Services Market Growth.

Ans: The Cell & Gene Therapy Manufacturing Services Market size was estimated at USD 15.59 billion in 2025 and is expected to reach USD 74.41 billion by 2035.

Ans: The Cell & Gene Therapy Manufacturing Services Market is expected to grow at a CAGR of 16.96% over the forecast period.

Get in Touch