Orthopedic Software Market Report Scope & Overview:

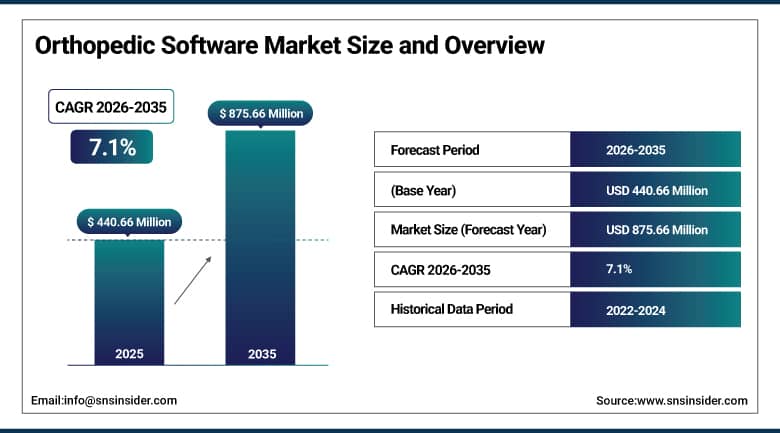

The Orthopedic Software Market size was USD 440.66 Million in 2025 and is expected to reach USD 875.66 Million by 2035, growing at a CAGR of 7.1% from 2026–2035.

Orthopedic software assists providers in managing image management, surgical planning, and patient records. The need for this type of software will continue to increase as the global disease burden associated with musculoskeletal diseases increases. Currently, over 1.71 billion individuals are suffering from musculoskeletal diseases such as osteoarthritis and lower back pain. Lower back pain is suffered by about 570 million individuals globally and is considered the most common reason for disability. The prevalence rate of osteoarthritis in the knee range is estimated to be between 22% and 39% in adults over 50 years old. Patients who require joint replacement surgery are becoming increasingly younger, as there has been an increase in joint replacement surgery in people aged in their 40s. Orthopedic injuries due to sports participation in older adults are anticipated to rise by 123% in 2040.

NHS Scotland launched an AI virtual physiotherapist called Kirsty to help patients with back pain. The service lets nearly one million Lothian residents book same-day appointments instead of waiting weeks. Built by Flok Health, the tool runs therapy sessions through a phone app. Early feedback shows meaningful improvement compared to conventional physiotherapy approaches. This kind of AI-driven care delivery reflects where orthopedic software is heading next. Similar virtual care models are likely to expand across other public health systems.

Market Size and Forecast:

-

Market Size in 2026E: USD 472.06 Million

-

Market Size by 2035: USD 875.66 Million

-

CAGR: 7.1% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Orthopedic Software Market - Request Free Sample Report

Orthopedic Software Market Trends:

-

AI-driven diagnostics and predictive analytics are becoming standard features across orthopedic software platforms.

-

Cloud-based orthopedic systems are gaining ground due to lower upfront costs and easier IT maintenance.

-

Interoperability requirements are pushing vendors toward standardized data exchange across care settings.

-

Patient engagement apps syncing rehab milestones are closing the feedback loop for bundled-payment compliance.

-

3D-printed bone regeneration research is expanding the potential applications for orthopedic planning software.

-

Value-based care models are increasing demand for holistic, integrated patient data management tools.

-

Growing telehealth integration is expanding orthopedic software's role beyond traditional clinical settings.

U.S. Orthopedic Software Market Outlook:

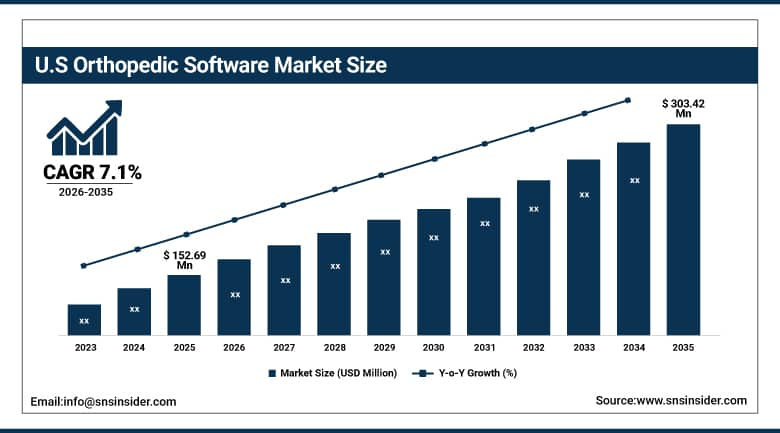

The U.S. Orthopedic Software Market is estimated at approximately USD 152.69 Million in 2025. It is projected to reach approximately USD 303.42 Million by 2035, growing at a CAGR of approximately 7.1%. These figures are estimated from North America's regional share, since the source report does not provide a separate U.S. dollar value.

Over seven million orthopedic procedures are conducted each year in the United States. Healthcare expenditure in the U.S. in 2023 amounted to USD 4.3 trillion, which accounts for 18.3% of GDP in the country. Over 95% of eligible hospitals in the U.S. utilize certified health information technology solutions. Such a high level of digitization of the health care industry continues to positively impact the widespread adoption of orthopedic software solutions across the country.

Radiologists in Minden, Germany use AI technologies offered by Siemens Healthineers to analyze their X-ray pictures. The system managed to discover some cancerous tumors, which could not be seen by human analysts before. Such applications of AI help accelerate the diagnostics and intervention processes. On the other hand, researchers at the University of Illinois Urbana-Champaign are developing bone healing methods based on AI technologies. They use 3D microstructures resembling termite mounds in the study.

Orthopedic Software Market Segment Analysis:

-

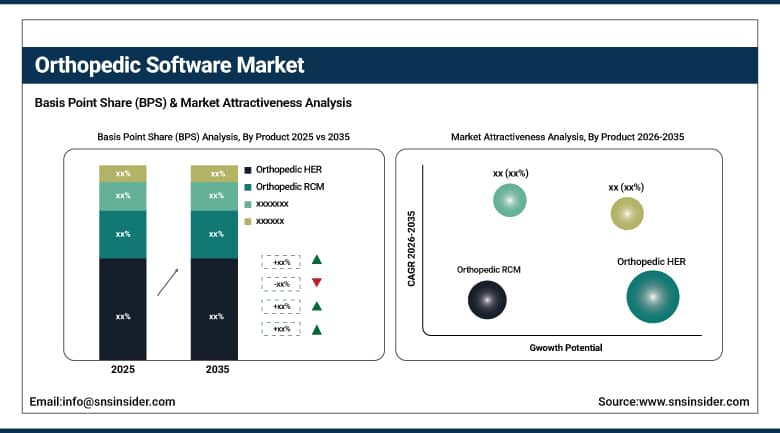

By Product, the orthopedic EHR segment dominated the orthopedic software market with approximately 26% share in 2025. The digital templating/preoperative planning software segment is seeing the fastest adoption growth.

-

By Mode of Delivery, the web/cloud-based segment dominated the orthopedic software market share in 2025. On-premise deployment is expected to grow progressively.

-

By Application, the orthopedic surgeries segment dominated the orthopedic software market with approximately 55% share in 2025. The fracture management segment is seeing rising adoption.

-

By End Users, the hospitals segment dominated the orthopedic software market with approximately 55% share in 2025. The ambulatory care centers segment is seeing rising adoption.

By Product, orthopedic EHR dominates, digital templating gains fastest ground

Orthopedic EHR emerged as the most successful product category due to the compliance of the government mandates concerning health IT. Over 95% of all eligible American hospitals have already integrated their certified health IT systems. They greatly enhance coordination of care, clinical decision-making, and workflow management for doctors and other hospital staff. Orthopedic physicians depend on EHR software to store information about patients' health and the progress of the therapy. With each passing year, AI and machine learning become more widely used in EHR software. The importance of value-based care models increases the need for comprehensive EHR solutions. Governmental actions to promote interoperability (ONC Interoperability Standards Advisory), among other things, boost the demand for EHR solutions.

Digital templating and preoperative planning software is seeing the fastest adoption growth. Surgeons use these tools for 3D modeling, virtual surgical planning, and real-time navigation. Rising demand for minimally invasive surgery is accelerating adoption of these planning tools. Robotic-assisted surgical device clearances have climbed sharply over the past decade. Software that integrates with robotic systems gives surgeons better visualization and procedural control. Surgeons increasingly expect these tools to reduce both planning time and intraoperative risk. This combination of precision and efficiency keeps driving rapid adoption of templating software.

By Mode of Delivery, web/cloud-based platforms lead by a wide margin

Web and cloud-based solutions accounted for an estimated 85% of the total revenue share in 2025. Both scalability and deployment ease contribute to the appeal of cloud-based solutions. Over 75% of American hospitals had implemented cloud-based health information technology infrastructure by 2023. With cloud platforms, healthcare specialists can get access to patients' records in various locations at once. It facilitates cooperation between different specialists and improves patients' services significantly. Also, cloud solutions are cheaper due to low initial costs and lack of the need for maintaining expensive IT infrastructure. In this way, small companies do not require spending too much money in advance. Thus, cloud-based delivery remains the dominant choice.

On-premises implementation is relevant when an organization has strong restrictions on accessing sensitive data internally. Some hospital chains still opt for an on-premises solution for specific purposes of security or compliance. It accounts only for a small fraction in terms of current market leaders, mostly for enterprises with pre-existing investments in hardware. As security standards continue improving, however, the market share of on-premises is likely to fall further.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Orthopedic Software Market Insights

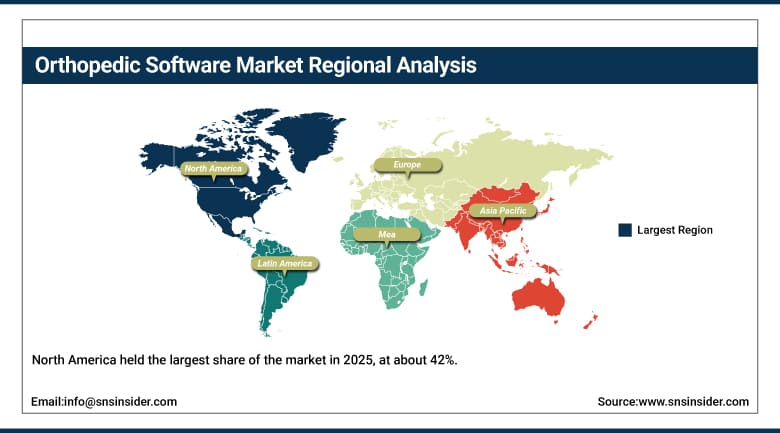

North America held the largest share of the market in 2025, at about 42%. Well-established healthcare infrastructure and early digital health adoption both support this lead. High healthcare expenditure further reinforces this regional position significantly. U.S. healthcare spending reached USD 4.3 trillion in 2023, representing 18.3% of national GDP.

The United States accounts for approximately 82.5% of North American revenue. The region's leadership in medical research and innovation keeps reinforcing this position. Numerous orthopedic software companies are headquartered across North America, further strengthening this advantage.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Orthopedic Software Market Insights

Europe represents a steady, mature market for orthopedic software across hospitals and clinics. Germany leads the regional market, supported by federal grants subsidizing healthcare digitization. Strict GDPR compliance requirements keep shaping how vendors design data-handling features.

Germany accounts for approximately 24.6% of European revenue. The UK's NHS interoperability program gives vendors with proven data-exchange capabilities a real advantage. France continues channeling innovation budgets toward coordinated, image-enabled orthopedic care networks.

Asia Pacific Orthopedic Software Market Insights

Asia Pacific is growing fastest in this market, supported by rising healthcare digitization. India's National Digital Health Mission is expanding orthopedic software penetration across the country. The WHO estimates that by 2050, one in four people across Asia Pacific will be over 60.

China accounts for approximately 40.6% of Asia Pacific revenue. Large population bases combined with rising orthopedic disorder incidence keep driving regional demand higher. Government healthcare modernization initiatives across the region should keep reinforcing this growth trajectory.

MEA & Latin America Orthopedic Software Market Insights

The UAE leads MEA revenue, growing healthcare digitization investment and rising specialist hospital capacity both support this position. Saudi Arabia is also expanding its digital health infrastructure across major medical centers. Government-led digital transformation programs across the Gulf region continue reinforcing this momentum.

Brazil leads Latin American revenue, expanding healthcare access and rising adoption of digital health tools both drive this regional lead. Mexico and Argentina contribute secondary demand through their own expanding healthcare systems.

Market Dynamics:

Growth Drivers: Rising orthopedic disorder burden accelerating demand for management software

The increasing number of cases of orthopedic diseases is one of the important drivers of this market. More than 1.71 billion people suffer from musculoskeletal diseases at present. Low back pain afflicts nearly 570 million individuals, accounting for being the top reason for global disability. Between 0.5% and 1% of adults are affected by rheumatoid arthritis, with females being more affected than males. The prevalence of osteoarthritis in the knees of the population aged above 50 is between 22% and 39%. Joint replacements among younger people are becoming common, with a lot of people in their 40s undergoing joint surgery operations. Such trends are the result of increasing life expectancies and demands for remaining active during middle ages. The issue of musculoskeletal diseases represents an especially significant burden in India.

Injuries from sports in elderly adults are predicted to increase 123% until 2040. It indicates a definite requirement for efficient injury management and treatment solutions. Orthopedic solutions can facilitate the organization of patients' information, treatment programs, and outcomes evaluation. The increasing use of data-driven decision-making tools by physicians adds value to this driver. Since musculoskeletal diseases are constantly increasing around the world, the forecasted driver will persist over the prediction period.

Restraints: High deployment costs limiting broader orthopedic software adoption

Expensive implementation of software in the orthopedic field is preventing some institutions from adopting such systems. Expenses related to licensing costs, upgrading equipment and training personnel increase the overall cost. On average, the cost of implementing an EHR system in a hospital is about USD 15 million. High costs are creating a significant hindrance to smaller medical organizations.

Additional costs arising from maintenance of the system will only increase expenditure. It becomes difficult to provide tangible returns on investment because the impact might not be clear in the short run. Providers who have a tough time making profits become hesitant to invest in such systems. Such high costs are hindering rapid adoption of the software in smaller practices.

Opportunities: AI and machine learning integration creating new orthopedic software growth potential

AI and machine learning implementation can help unlock substantial growth potential for this market. Such technologies allow precise assessment of large amounts of patient cases for proper diagnosis. Personalized patient treatment plans will become a possibility due to AI-enabled clinical decision support. Tools such as virtual physiotherapy systems, which include, among others, the Kirsty tool developed by NHS Scotland, are creating new opportunities for remote treatment.

AI-based tools already help diagnose tumors overlooked by radiologists during visual examination. The development of AI-based biomaterials to regenerate bones is promising for future prosthetic implants. Early investments in such technological capabilities will give companies significant competitive advantages in the future. Collaboration between software developers and research laboratories can accelerate the innovation process. AI adoption is increasing in healthcare, and this market opportunity should remain stable throughout the forecast period.

Recent Developments:

-

2024: Formus Labs received FDA 510(k) clearance for Formus Hip, the first fully automated 3D surgical planning software for hip replacement.

-

2024: Exactech released updated ExactechGPS software, improving tibia and femur resection planning for total knee replacement procedures.

-

2023: Stryker launched the Ortho Q Guidance System, offering advanced surgical guidance for knee and hip procedures controllable from the sterile field.

Orthopedic Software Market Key Players are:

-

Brainlab AG

-

Materialise N.V.

-

Stryker

-

eClinicalWorks

-

NextGen Healthcare

-

Allscripts Healthcare Solutions

-

athenahealth

-

CureMD Healthcare

-

DrChrono Inc.

-

GreenWay Health LLC

-

IBM Corporation (Merge Healthcare)

-

Medstrat Inc.

-

Exactech, Inc.

-

OPIE Software

-

Siemens Healthineers AG

-

Koninklijke Philips

-

Zimmer Biomet

-

Johnson & Johnson

-

GE HealthCare

-

Medtronic

Orthopedic Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 440.66 Million |

| Market Size by 2035 | USD 875.66 Million |

| CAGR | CAGR of 7.1% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Digital Templating/Preoperative Planning Software, Orthopedic EHR, Orthopedic RCM, Orthopedic Practice Management, Orthopedic PACS, and Others) • By Application (Orthopedic Surgeries, Fracture Management, and Others) • By Mode of Delivery (Web/Cloud-Based and On-premise) • By End Users (Hospitals, Ambulatory Care Centers, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Brainlab AG, Materialise N.V., Stryker, eClinicalWorks, NextGen Healthcare, Allscripts Healthcare Solutions, athenahealth, CureMD Healthcare, DrChrono Inc., Greenway Health LLC, IBM Corporation (Merge Healthcare), Medstrat Inc., Exactech, Inc., OPIE Software, Siemens Healthineers AG, Koninklijke Philips, Zimmer Biomet, Johnson & Johnson, GE HealthCare, and Medtronic. |

Frequently Asked Questions

The Orthopedic Software Market is expected to grow at a CAGR of 7.1% from 2026 to 2035.

The Orthopedic Software Market was valued at USD 440.66 Million in 2025.

Rising musculoskeletal disorder prevalence, growing AI integration, and increasing demand for minimally invasive surgical planning are the primary growth factors.

The Orthopedic EHR segment dominated the Orthopedic Software Market with approximately 26% share in 2025.

North America dominated the Orthopedic Software Market with approximately 42% revenue share in 2025.

Get in Touch