Central Venous Catheter Market Report Scope & Overview:

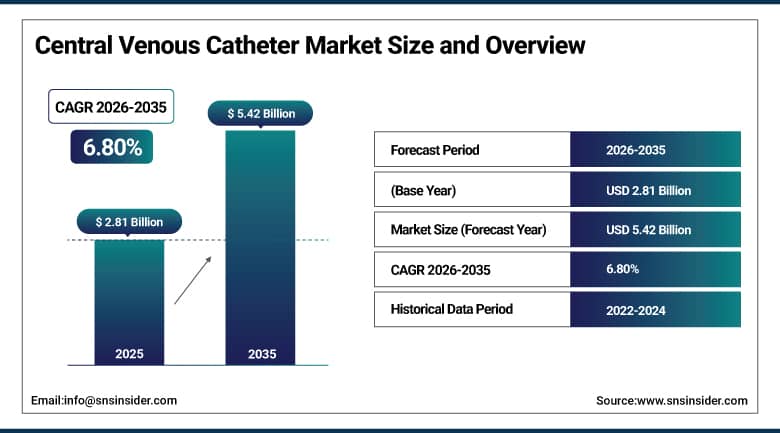

The Central Venous Catheter Market was valued at USD 2.81 billion in 2025 and is expected to reach USD 5.42 billion by 2035, growing at a CAGR of 6.80% from 2026-2035.

The central venous catheter market is expanding owing to the increasing incidences of chronic diseases like cancer, kidney failure, and heart diseases that need continuous intravenous medication. The increase in the number of patients admitted to ICUs and surgeries has increased the demand for a reliable vascular access device. The increasing application of central venous catheters in chemotherapy, dialysis, and critical care centers adds to the growth of the central venous catheter market.

In 2024, Teleflex introduced the Arrow ErgoPack Complete System with an antimicrobial technology for central lines, proving itself to be an innovator of infection prevention.

In 2023, Medtronic and an outpatient surgery center teamed up to deploy AI-driven catheter placement tools to bring down misplacement rates, showcasing tech adoption in the central venous catheter market share.

Central Venous Catheter Market Size and Forecast

-

Central Venous Catheter Market Size in 2025: USD 2.81 Billion

-

Central Venous Catheter Market Size by 2035: USD 5.42 Billion

-

CAGR: 6.80% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Central Venous Catheter Market - Request Free Sample Report

Central Venous Catheter Market Trends

-

Rising prevalence of chronic diseases and critical care admissions is driving the central venous catheter market.

-

Growing number of surgical procedures and long-term intravenous therapies is boosting market growth.

-

Expansion of hospital infrastructure, intensive care units (ICUs), and emergency care services is fueling device adoption.

-

Increasing focus on efficient drug delivery, hemodynamic monitoring, and patient safety is shaping adoption trends.

-

Advancements in antimicrobial coatings, catheter materials, and insertion techniques are enhancing safety and reducing infection risks.

-

Rising demand for minimally invasive and long-term vascular access solutions is supporting market expansion.

-

Collaborations between medical device manufacturers, hospitals, and research institutions are accelerating innovation and global adoption.

U.S. Central Venous Catheter Market Size Outlook:

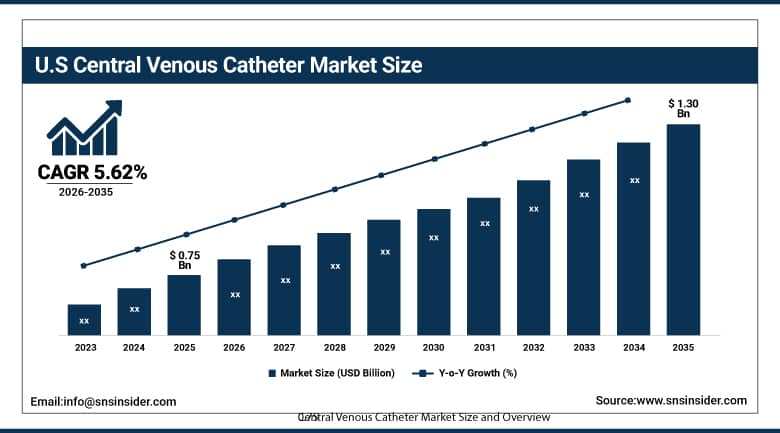

The U.S. Central Venous Catheter Market was valued at USD 0.75 billion in 2025 and is expected to reach USD 1.30 billion by 2035, growing at a CAGR of 5.62% from 2026-2035.

Central venous catheters market is witnessing growth owing to the rise in the incidence of chronic diseases, increased number of patients admitted to ICUs, and the need for chemotherapy and dialysis. The advanced infrastructure of the healthcare sector along with the high adoption rate of minimally invasive treatments is aiding the market growth.

Central Venous Catheter Market Segment Highlights

-

By Product Type, Double Lumen Central Venous Catheters segment dominated the Market in 2025 with around 38% share; Triple Lumen Central Venous Catheters segment is the fastest growing during the forecast period.

-

By Placement Site, Internal Jugular Vein segment dominated the Market in 2025 with around 45% share; Femoral Vein segment is the fastest growing during the forecast period.

-

By Application, Drugs and Fluid Administration segment dominated the Market in 2025 with around 41% share; Chemotherapy segment is the fastest growing during the forecast period.

-

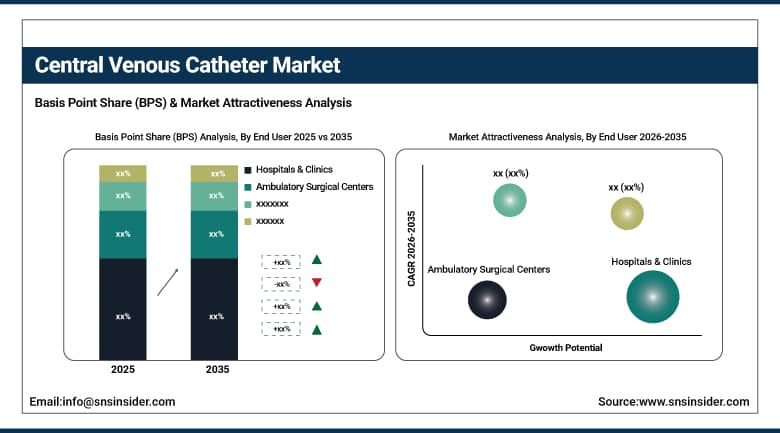

By End User, Hospitals & Clinics segment dominated the Market in 2025 with around 68% share; Ambulatory Surgical Centers segment is the fastest growing during the forecast period.

By End User, Hospitals & Clinics segment dominates the Market, Ambulatory Surgical Centers segment expected to grow fastest.

The Hospitals & Clinics segment led the Central Venous Catheter Market throughout 2025 owing to the high volume of procedures undertaken at such establishments including critical care treatments, surgeries, and emergencies. Being the main entry point for the use of catheters, hospitals had the best medical professionals and infrastructure facilities available to assist them. The influx of patients coupled with the rise in the number of chronic and acute cases was another factor that boosted the Hospitals & Clinics segment's position.

The Ambulatory Surgical Centers segment was expected to exhibit the highest growth rates for the entire forecast period owing to an increase in the number of minimally invasive operations and cost-saving measures. These centers have increasingly turned to central venous catheters as a means of treatment and recovery process post-surgery. Increasing trends towards same-day discharges and advances in catheter technologies are some factors boosting their usage at such establishments.

By Product Type, Double Lumen Central Venous Catheters segment dominates the Market, Triple Lumen Central Venous Catheters segment expected to grow fastest.

The Double Lumen Central Venous Catheters segment accounted for the largest market share in the Central Venous Catheter Market in 2025 owing to its prevalent use in critical care scenarios that involve administering multiple therapies simultaneously. The ability of the Double Lumen Central Venous Catheters to provide adequate functionality while being easy to insert and posing fewer risks than higher lumen alternatives made it dominant within the market. Their extensive use in emergencies and chronic disease therapies further strengthened their dominance.

The Triple Lumen Central Venous Catheters segment is anticipated to exhibit the highest growth rate in the forecast period owing to the rising requirement in sophisticated clinical scenarios that require multiple infusions simultaneously. The high incidence of chronic diseases, rising ICU admissions, and increasing oncological treatments have increased the demand for more functional devices. The capacity of these devices to handle various therapies such as vasopressors, parenteral nutrition, and antibiotics at once is increasing their adoption.

By Placement Site, Internal Jugular Vein segment dominates the Market, Femoral Vein segment expected to grow fastest.

In 2025, the Internal Jugular Vein segment was dominant in the Central Venous Catheter market owing to the easy accessibility of the segment and low complication rate. In addition, the anatomically accurate positioning of the catheter was an added advantage, which contributed to its dominance. Moreover, the clinical preference by health-care practitioners along with established procedural guidelines also contributed significantly to the dominant position of this segment.

Femoral Vein segment is expected to witness the fastest growth during the forecast period due to its increasing use in emergency situations and patients where upper body access is limited. It offers quick insertion with minimal interference in airway management, making it suitable for trauma and intensive care cases. Growing adoption in urgent care settings and advancements in infection control techniques are further supporting its rising utilization.

By Application, Drugs and Fluid Administration segment dominates the Market, Chemotherapy segment expected to grow fastest.

Drugs and Fluid Administration Application accounted for the largest market share in the Central Venous Catheter market in 2025 owing to its wide application in the delivery of drugs, IV fluids, and nutrition in critically ill patients. The increasing frequency of hospitalizations and surgical interventions where there was a need to infuse drugs in patients at a controlled rate played a vital role in the segment’s market dominance.

The chemotherapy segment is projected to record the highest growth over the forecast period on account of the increasing global incidence of cancer and higher adoption rates for chronic venous access devices for cancer patients. The central venous catheters play a major role in the administration of chemotherapy drugs and help to increase the efficiency of the process while ensuring minimum discomfort to the patient.

Central Venous Catheter Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

91.8% |

|

Europe |

United Kingdom |

22.9% |

|

Asia Pacific |

Australia |

7.6% |

|

Middle East & Africa |

UAE |

13.1% |

|

Latin America |

Brazil |

49.4% |

North America Central Venous Catheter Market Insights

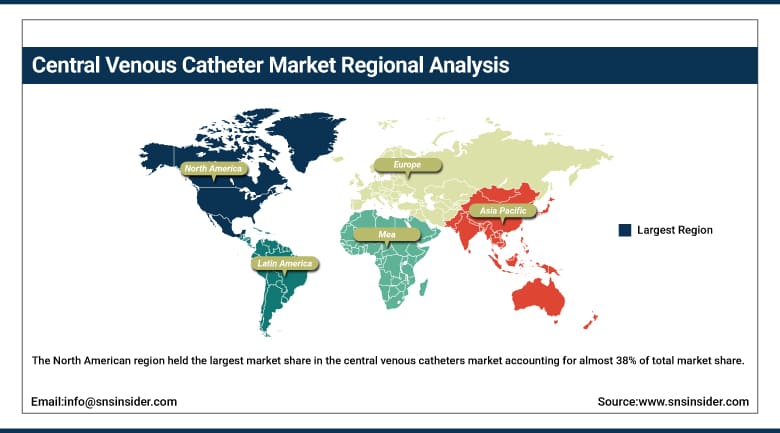

The North American region held the largest market share in the central venous catheters market accounting for almost 38% of total market share. The factors contributing to the dominance of the region include the high prevalence rate of chronic diseases, the presence of advanced medical infrastructure in the region, and the adoption of critical care. Other reasons include the growing prevalence of cancer and its treatment through the administration of chemo therapy, dialysis, and IV infusions.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Central Venous Catheter Market Insights

The Asia-Pacific region is experiencing the fastest CAGR in the global market for central venous catheters because of fast development in health infrastructure and an increase in patient numbers. The rise in the number of chronic conditions, availability of better treatment facilities, and investments in hospitals are boosting the demand. An increase in the implementation of intensive care practices, oncological treatment, and surgeries is also supporting market growth. Improvements in healthcare awareness, medical tourism, and government initiatives in providing healthcare services are propelling market growth in the region.

Europe Central Venous Catheter Market Insights

The European region ranks second in terms of size in the central venous catheter market. The growth drivers are a sophisticated healthcare infrastructure, increased occurrence of chronic conditions, and demand for sophisticated critical care procedures. Europe demonstrates high acceptance of infection control catheters and highly sophisticated medical equipment. Increasing cancer therapies, an aging population, and increasing surgery rates are additional factors that favor the use of catheters. Besides, reimbursement policies and stringent healthcare regulations help maintain sustained growth in the European markets.

Middle East & Africa and Latin America Central Venous Catheter Market Insights

The Middle East and Africa along with Latin American markets for CVCs are witnessing steady growth on account of increased healthcare spending and incidence of chronic diseases. Growing hospital infrastructure, coupled with an increasing adoption of advanced critical care techniques, is also contributing to this positive growth trend. Increased use of oncology treatments, dialysis, and emergency care treatments is driving the demand for CVCs. Nevertheless, limited availability of advanced healthcare facilities in some regions is hindering the growth prospects.

Central Venous Catheter Market Growth Drivers:

-

Rising critical care admissions and increasing need for long-term intravenous therapies driving strong central venous catheter adoption globally

Increasing instances of chronic ailments including cancer, kidney failure, and heart-related complications have increased hospitalizations that require prolonged IV therapy. The use of central venous catheters is crucial for the administration of chemotherapy drugs, nutritional support, and vital medicines. This is important because the central venous catheter helps to deliver medicines directly to patients who require immediate treatment. Increasing instances of surgeries and emergencies are likely to drive the market for vascular access devices even higher. Increased health facilities and ICU beds in developing and developed countries are also driving the market for vascular access devices.

Central Venous Catheter Market Restraints:

-

Catheter-related bloodstream infections and procedural complications limiting adoption and increasing clinical risk concerns in healthcare facilities

There are also various health hazards that are linked with the use of central venous catheters, including bloodstream infections caused by catheters, thrombosis, and mechanical problems, and these issues have been a constant cause for worry among health care practitioners. Incorrect insertion methods and lengthy catheterization can result in increased infection cases, causing higher incidences of illness, extended patient hospitalizations, and escalating expenses. The presence of strict regulatory laws and protocols makes the clinical use even more complicated. Moreover, the requirement for specialized and competent staff for both insertion and catheter management reduces access in small hospitals.

Central Venous Catheter Market Opportunities:

-

Technological advancements in antimicrobial coatings and catheter design innovations improving safety and expanding clinical acceptance worldwide

The continuous development of catheter materials and design has greatly improved the performance of the products. The production of catheters that have antimicrobial coatings and catheters bonded with heparin is lowering the chances of infections occurring to patients. Biocompatibility of catheters together with the introduction of flexible multi-lumen catheters makes their insertion easier. Ultrasound technology that can be used during the catheterization process improves accuracy of catheterization processes while minimizing associated risks. More research on the products by companies will result into more innovative catheters with higher dwell periods.

Recent Developments:

-

2026: Teleflex continued innovation in Arrow vascular access systems, enhancing catheter navigation technologies and supporting improved central venous catheter placement accuracy in acute care and emergency medicine settings.

-

2026: BD launched its next-generation central venous catheter insertion platform, designed to simplify central line placement and improve safety in high-pressure clinical environments. The system integrates multiple steps into a unified CVC insertion workflow.

-

2025: B. Braun launched new catheter securement and vascular access innovations including Clik-FIX epidural and PNB catheter systems. The company also expanded IV and infusion-related catheter safety solutions improving clinical workflow efficiency.

-

2025: ICU Medical expanded its infusion therapy and catheter-based delivery systems, focusing on improving closed system drug transfer and vascular access safety. The company emphasized reducing bloodstream infection risks in hospital CVC use.

-

2024: Teleflex introduced next-generation Arrow VPS Rhythm DLX technologies supporting improved catheter tip navigation during vascular access procedures. The system enhanced precision in central line and PICC placement using real-time guidance tools.

Key Players:

-

ICU Medical

-

B. Braun SE

-

BD Becton Dickinson and Company

-

Teleflex Incorporated

-

Medtronic plc

-

Smiths Medical

-

Poly Medicure Limited

-

Lepu Medical Technology

-

AngioDynamics Inc

-

Vygon SA

-

Edwards Lifesciences Corporation

-

Cook Medical

-

Terumo Corporation

-

Nipro Corporation

-

Asahi Kasei Corporation

-

Merit Medical Systems Inc

-

Bactiguard Holding AB

-

Halyard Health Owens and Minor

-

Argon Medical Devices

-

Fresenius Kabi AG

Central Venous Catheter Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.81 Billion |

| Market Size by 2035 | USD 5.42 Billion |

| CAGR | CAGR of 6.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Single Lumen Central Venous Catheters, Double Lumen Central Venous Catheters, Triple Lumen Central Venous Catheter, and Quadruple Lumen Central Venous Catheters) • By Placement Site (Internal Jugular Vein, Femoral Vein, and Subclavian Vein) • By Application (Chemotherapy, Drugs and Fluid Administration, Blood Transfusions, and Others) • By End User (Hospitals & Clinics, Ambulatory Surgical Centers, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ICU Medical, B. Braun SE, BD Becton Dickinson and Company, Teleflex Incorporated, Medtronic plc, Smiths Medical, Poly Medicure Limited, Lepu Medical Technology, AngioDynamics Inc, Vygon SA, Edwards Lifesciences Corporation, Cook Medical, Terumo Corporation, Nipro Corporation, Asahi Kasei Corporation, Merit Medical Systems Inc, Bactiguard Holding AB, Halyard Health Owens and Minor, Argon Medical Devices, Fresenius Kabi AG |

Frequently Asked Questions

Ans: The Central Venous Catheter Market is expected to grow at a CAGR of 6.80% from 2026 to 2035.

Ans: The Central Venous Catheter Market was valued at USD 2.81 billion in 2025.

Ans: Rising critical care admissions and increasing need for long-term intravenous therapies driving strong central venous catheter adoption globally.

Ans: The Double Lumen Central Venous Catheters segment dominated the Central Venous Catheter Market in 2025.

Ans: North America dominated the Central Venous Catheter Market in 2025.

Get in Touch