Chiplet Market Report Scope & Overview:

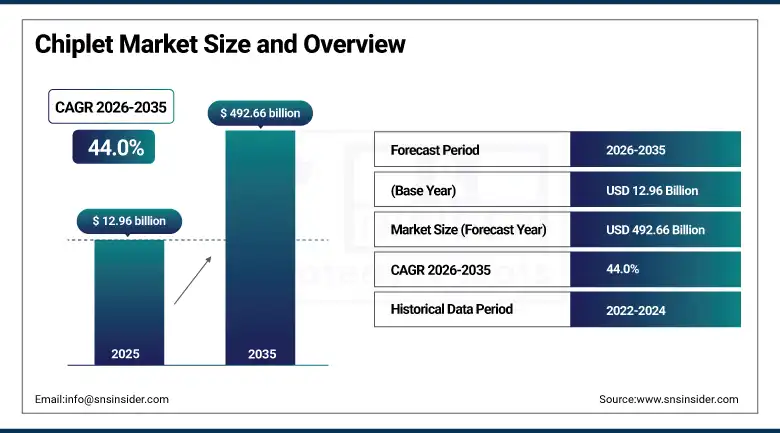

The Chiplet Market was valued at USD 12.96 billion in 2025 and is expected to reach USD 492.66 billion by 2035, growing at a CAGR of 44.0% from 2026–2035.

The Global chiplet market is revolutionizing the semiconductor industry through the development of modular chip design approaches that incorporate several small dies into a single superior package. In contrast to conventional monolithic system-on-chip approaches, the chiplet architecture allows semiconductor companies to combine processing capabilities, memory capabilities, artificial intelligence accelerators, graphic processing units, and input/output capabilities using distinct process nodes. The adoption of chiplets is expected to enhance the yield of production, scalability, flexibility of customization, and speed to the market for complex computers. There has been increased demand for high-performance computing, artificial intelligence, cloud data centers, 5G infrastructure, and automotive electronic solutions, which has driven the adoption of chiplet technologies across the globe. There has been substantial growth in the complexity of semiconductor design and the slowdown of monolithic scaling economics.

The UCIe Consortium introduced the UCIe 3.0 specification with support for up to 64 GT/s data rates to improve interoperability and performance for next-generation chiplet-based systems. Intel also unveiled advanced multi-chiplet packaging technologies capable of integrating massive AI processors with HBM5 memory stacks using its EMIB and Favero’s platforms.

Market Size and Forecast

-

Market Size 2026E: USD 18.62 Billion

-

Market Size 2035: USD 492.66 Billion

-

CAGR (2026-2035): 44.0%

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Chiplet Market - Request Free Sample Report

Chiplet Market Trends

-

Broad adoption of the UCIe standard is enabling interoperable multi-vendor chiplet ecosystems and accelerating development of open chiplet marketplaces.

-

Rising deployment of AI inference at the network edge is increasing demand for power-efficient chiplet-based AI accelerators in telecom, automotive, and industrial systems.

-

Expanding hyperscale AI infrastructure investments are driving adoption of chiplet-integrated GPUs, memory architectures, and high-performance accelerator platforms.

-

Semiconductor manufacturers are increasingly shifting from monolithic SoC designs toward heterogeneous chiplet architectures to improve scalability, yield, and cost efficiency.

-

Growing data center and networking infrastructure development across emerging economies is accelerating demand for chiplet-based server and networking silicon solutions.

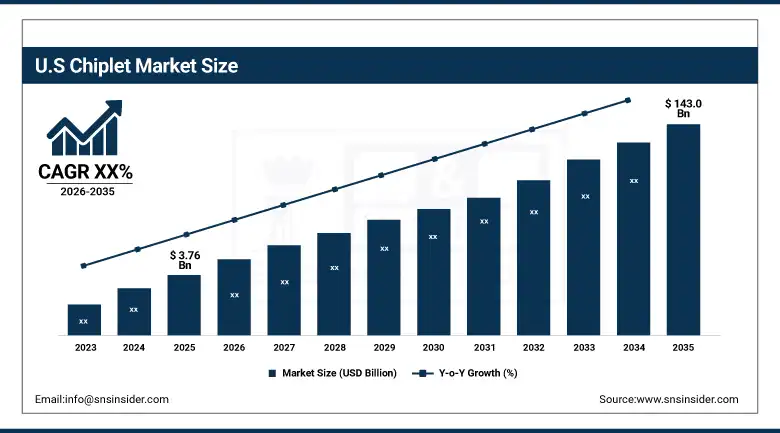

The U.S. Chiplet Market Size Outlook

The U.S. Chiplet Market was valued at approximately USD 3.76 billion in 2025 and is expected to reach approximately USD 143.0 billion by 2035, supported by strong demand from hyperscale AI data center, defense semiconductor, and advanced automotive sectors.

The United States is the world's hub of chiplet innovations, with Intel's Favero’s 3D stacking and EMIB 2.5D interconnection technologies, NVIDIA's multiple die GPU designs that enable training of trillion-parameter models in AI applications, and AMD's native chiplets for EPYC processors that have proven to be highly superior to their monolithic counterparts in terms of performance and efficiency in enterprise data centers. The procurement by the U.S. defense sector of advanced processing technologies using chiplets for the development of future radars, electronic warfare equipment, and autonomous systems generates a high-demand premium market that warrants the top tier of specifications.

Apple's collaboration with Broadcom to develop the custom AI chipset 'Baltra' launching in 2026 leveraging Broadcom's 3.5D packaging expertise, combined with Intel's UCIe-based power efficiency innovations reducing circuit frequencies for enhanced reliability in System-in-Package designs, exemplify the premium innovation at the U.S. market's technology frontier where validated chiplet integration performance and advanced packaging capabilities command the highest semiconductor product pricing globally.

Chiplet Market Segment Analysis

-

According to Processor, CPU dominated with approximately 44.00% market share in 2025; GPU is the fastest-growing processor type at a CAGR of approximately 46.20% from 2026 to 2035.

-

In terms of Packaging Technology, 2.5D/3D packaging dominated with approximately 38.5% market share in 2025; System-in-Package (SiP) is the fastest-growing packaging segment at approximately 45.8% CAGR, driven by IoT, wearable, and mobile device integration requirements.

-

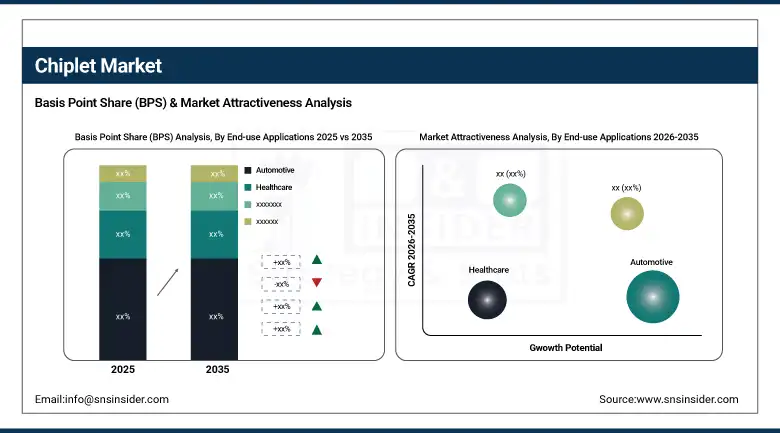

By End-use Application, Automotive dominated as the largest application segment with 32.00% share in 2025; Enterprise Electronics is the fastest-growing application segment at 46.10% CAGR driven by data center, cloud computing, and AI infrastructure chiplet adoption.

By Processor, CPU dominates, GPU grows fastest

CPU maintained its leadership in the Chiplet market in 2025 with approximately 44.00% revenue share, driven by the fundamental commercial imperative for general-purpose computing performance scaling that chiplet architectures uniquely enable by disaggregating monolithic processor dies into compute, I/O, and cache chiplets manufactured at optimized process nodes to achieve the highest core counts, cache capacities, and memory bandwidth within power and thermal constraints.

GPU chiplets are the fastest-growing processor segment at approximately 46.20% CAGR through 2035, driven by the extraordinary growth of AI training and inference workloads in hyperscale data centers where NVIDIA Blackwell multi-die GPU architectures, AMD RDNA-based compute GPUs, and custom AI ASIC chiplet designs are enabling transistor counts, memory bandwidth, and compute throughput that monolithic GPU designs cannot achieve within reticle size and yield constraints.

By Packaging Technology, 2.5D/3D dominates, SiP grows fastest

The 2.5D/3D packaging segment retained its leading position with approximately 38.5% market share in 2025 due to the adoption of TSMC CoWoS silicon interposer technology in AI accelerators and high-bandwidth memory integration that provides the highest die-to-die bandwidth density required for training large language models, combined with Intel Favero’s 3D stacking technology enabling logic-on-logic chiplet integration that maximizes performance-per-watt in premium processor designs.

System-in-Package technology experienced the most significant growth rate among other packaging approaches at approximately 45.8% CAGR until 2035, driven by the proliferation of IoT devices, smartwatches, wireless earbuds, and compact consumer electronics platforms requiring the highest levels of component miniaturization, where SiP integration of processor, memory, RF, and power management chiplets into a single compact package delivers the functional density and power efficiency that discrete component board designs cannot achieve.

By End-use Application, Automotive dominates, Enterprise Electronics grows fastest

The Automotive segment maintained its position as the leading application in the Chiplet Market in 2025 due to the accelerating global transition to electric vehicles and autonomous driving systems that require increasingly powerful, energy-efficient semiconductor solutions for battery management, motor control, sensor fusion, and autonomous driving compute platforms, where chiplet architectures enable automotive OEMs to combine specialized processing, connectivity, and safety chiplets into application-specific integrated solutions with faster development cycles and extended model life updates than monolithic SoC alternatives. Automotive chiplets must meet AEC-Q100 reliability qualification and ISO 26262 functional safety certification requirements for use in safety-critical vehicle control applications.

The Enterprise Electronics application is expected to be the most rapidly growing segment of the market until 2035 due to the extraordinary capital expenditure cycle in hyperscale data center AI infrastructure where cloud providers including AWS, Microsoft Azure, and Google Cloud are deploying chiplet-based AI accelerators, networking processors, and custom silicon at unprecedented scale to support large language model training and inference services, combined with the hyperscaler shift to custom silicon ASIC chiplet designs that deliver superior performance-per-watt efficiency relative to merchant GPU silicon for specific AI workload optimization.

Regional Analysis

|

Region |

Major Country |

Share within Region 2025 (%) |

|---|---|---|

|

North America |

United States |

68% |

|

Europe |

Germany |

30% |

|

Asia Pacific |

China / Taiwan |

42% |

|

Middle East & Africa |

UAE |

22% |

|

Latin America |

Brazil |

38% |

North America Chiplet Market Insights

North America is the fastest-growing chiplet market, anchored by the United States which accounted for approximately 68% of North American revenues in 2025, driven by the world's leading AI chip designers including NVIDIA, Intel, AMD, and Apple, combined with the CHIPS and Science Act's USD 52 billion in domestic semiconductor manufacturing and R&D funding that is building out a comprehensive chiplet ecosystem spanning design, foundry, and advanced packaging capabilities. IPC's confirmation that electronic semiconductor solution exports rose 4.7% in 2025 confirms the U.S. chiplet industry's growing global competitiveness in premium AI accelerator and defense semiconductor segments.

Europe Chiplet Market Insights

Europe is a significant and growing chiplet market, driven by Germany's world-leading automotive and industrial semiconductor demand for ADAS, EV powertrain, and industrial automation chiplet solutions, combined with ASML's critical EUV lithography equipment monopoly enabling the advanced node manufacturing that chiplet architectures require, and European semiconductor sovereignty initiatives supporting STMicroelectronics, Infineon, and NXP chiplet capability development. European chiplet demand is shaped by strict RoHS and REACH compliance requirements combined with automotive and industrial functional safety certification standards that have elevated the technical specification floor across all product categories.

Asia Pacific Chiplet Market Insights

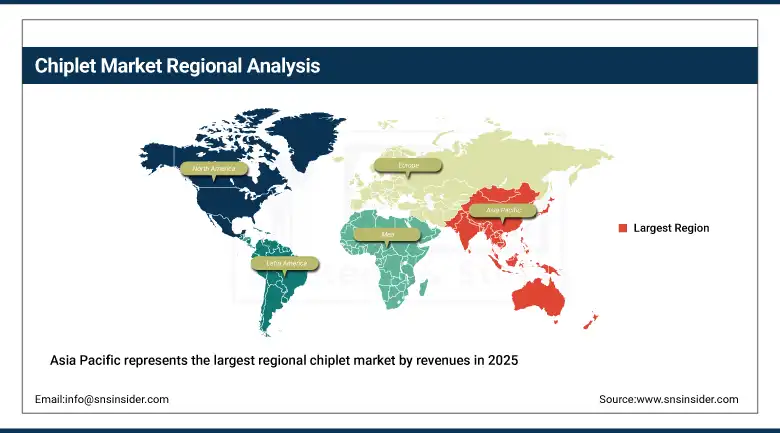

Asia Pacific represents the largest regional chiplet market by revenues in 2025, driven by TSMC's foundry leadership in advanced node chiplet manufacturing and CoWoS advanced packaging, Samsung's foundry and HBM memory chiplet capabilities, and the enormous consumer electronics and automotive semiconductor consumption of China, Japan, South Korea, and Taiwan that drives the highest regional chiplet integration volumes. China's dominant position as the world's largest producer of consumer electronics creates the highest regional chiplet consumption volume, while the manufacturing and design cost advantages of TSMC and Samsung are enabling competitive pricing that sustains Asia Pacific's revenue leadership through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Latin America and MEA Chiplet Market Insights

Latin America and MEA are growing chiplet markets driven by data center infrastructure investment, consumer electronics adoption, and telecommunications equipment upgrades requiring advanced chiplet-based processor and networking silicon for 5G deployment. Brazil leads Latin American revenues at approximately 38% through its consumer electronics, telecommunications, and industrial automation sectors that drive chiplet adoption. MEA adoption is anchored by UAE and Saudi Arabia's Vision 2030 technology infrastructure investments and growing data center construction programs, and South Africa's expanding fintech and telecommunications sectors that specify chiplet-based networking and computing silicon.

Market Dynamics

Growth Drivers: Expanding AI infrastructure investment, semiconductor complexity scaling, and cost-effective heterogeneous integration driving broad-based chiplet demand across global computing sectors

The primary structural growth drivers for the chiplet market are the continuing expansion of global AI training and inference infrastructure investment at hyperscale cloud providers that demands chiplet-based GPU and accelerator architectures capable of exceeding reticle-size transistor count limitations, the growing complexity of semiconductor system requirements that makes monolithic SoC designs at advanced nodes prohibitively expensive for all but the highest-volume applications, and the technology upgrade cycle across enterprise computing, automotive, and telecommunications infrastructure that replaces legacy monolithic processor designs with chiplet-based heterogeneous integration architectures offering superior performance-per-watt, customization flexibility, and total cost of ownership. The global AI transformation of data center operations is installing new accelerated computing systems across every hyperscale and enterprise category, each requiring chiplet-integrated GPU, memory, and networking silicon.

The CHIPS and Science Act's USD 52 billion allocation for domestic semiconductor manufacturing and R&D, combined with Intel's UCIe-based power efficiency innovations, AMD's chiplet-native EPYC processor leadership in enterprise data center deployments, and NVIDIA's Blackwell multi-die GPU architecture enabling trillion-parameter AI model training, confirm that the chiplet market's transformational technology base is simultaneously expanding into new premium applications through advanced packaging and materials innovation while sustaining its foundational automotive and computing application volumes through the global semiconductor investment cycle.

Restraints: Competition from mature monolithic SoC designs in cost-sensitive applications, complex advanced packaging supply chains, and thermal management challenges in high-density chiplet integration

A significant restraint on the market is the persistent cost premium of advanced chiplet packaging technologies relative to mature monolithic SoC production, where CoWoS, Favero’s, and SoIC assembly costs remain substantially higher than conventional flip-chip BGA packaging and constrain chiplet adoption in mid-range and cost-sensitive consumer electronics applications where total BOM cost determines technology selection. The complexity and limited capacity of advanced packaging technologies require specialized OSAT capabilities that constrain chiplet assembly supply during demand surges, creating lead time and supply security risks for OEM customers committing to chiplet-based product architectures. Thermal management of high-power-density chiplet assemblies where stacked dies and HBM memory generate concentrated heat loads requires sophisticated cooling solutions that add system cost and design complexity in edge computing, automotive, and industrial applications.

Opportunities: UCIe ecosystem standardization, AI edge chiplet deployment, and emerging market data center infrastructure expansion

The Universal Chiplet Interconnect Express (UCIe) standard's broad adoption by Intel, AMD, TSMC, Samsung, ARM, and Qualcomm represent the foundational industry standardization that will unlock multi-vendor chiplet marketplaces enabling fabless companies to source best-in-class memory, I/O, analog, and processing chiplets from specialized suppliers without proprietary integration constraints, creating a new chiplet IP licensing and commercialization market. AI inference deployment at the network edge in telecommunications base stations, automotive platforms, and industrial automation equipment creates growing demand for power-efficient chiplet-based AI accelerators delivering data center performance within edge power and thermal budgets, representing a high-volume market segment that extends chiplet adoption beyond premium hyperscale applications. The industrialization of data center infrastructure across Southeast Asia, Latin America, and Middle East economies is creating growing demand for chiplet-integrated server and networking silicon, expanding the addressable market for chiplet-based computing solutions.

Recent Developments:

-

2025: Intel expanded its chiplet portfolio with next-generation Foveros Direct copper-to-copper bonding technology achieving sub-1-micron interconnect pitch, enabling significantly higher die-to-die bandwidth density and reduced latency for AI accelerator and premium server processor chiplet integration than previous generation hybrid bonding approaches.

-

2026: Apple launched its 'Baltra' custom AI chipset developed in collaboration with Broadcom, leveraging 3.5D packaging technology to deliver cloud AI inference performance optimized for Apple's data center infrastructure, marking Apple's entry into hyperscale chiplet-based AI accelerator deployment.

-

2025: NVIDIA's Blackwell Ultra platform extended the multi-die GPU chiplet architecture with enhanced NVLink interconnect bandwidth and HBM3e memory integration, achieving 1.4 exaflops of AI compute in a single rack configuration for large language model training at hyperscale data center deployments.

Chiplet Market Key Players are:

-

Intel Corporation

-

Advanced Micro Devices, Inc. (AMD)

-

Apple Inc.

-

IBM

-

Marvell

-

MediaTek Inc.

-

NVIDIA Corporation

-

Achronix Semiconductor Corporation

-

Ranovus

-

Netronome

-

Cadence Design Systems, Inc.

-

SiFive, Inc.

-

ALPHAWAVE SEMI

-

Eliyan

-

Ayar Labs, Inc.

-

Tachyum

-

X-Celeprint

-

Kandou Bus SA

-

NHanced Semiconductors

-

Tenstorrent

Chiplet Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.96 Billion |

| Market Size by 2035 | USD 492.66 Billion |

| CAGR | CAGR of 44.0% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Processor (Field-Programmable Gate Array (FPGA), Graphics Processing Unit (GPU), Central Processing Unit (CPU), Application Processing Unit (APU), Artificial Intelligence Application-specific Integrated Circuit (AI ASIC) Coprocessor) • By Packaging Technology (System-in-Package (SiP), Flip Chip Chip Scale Package (FCCSP), Flip Chip Ball Grid Array (FCBGA), 2.5D/3D, Wafer-Level Chip Scale Package (WLCSP), Fan-Out (FO)) • By End-use Applications (Enterprise Electronics, Consumer Electronics, Automotive, Industrial Automation, Healthcare, Military & Aerospace, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intel Corporation, Advanced Micro Devices, Inc. (AMD), Apple Inc., IBM, Marvell Technology, Inc., MediaTek Inc., NVIDIA Corporation, Achronix Semiconductor Corporation, Ranovus Inc., Netronome Systems, Inc., Cadence Design Systems, Inc., SiFive, Inc., Alphawave Semi, Eliyan Corporation, Ayar Labs, Inc., Tachyum Inc., X-Celeprint Limited, Kandou Bus SA, NHanced Semiconductors, Inc., and Tenstorrent Inc. |

Frequently Asked Questions

System-in-Package (SiP) is the fastest-growing packaging technology segment at approximately 45.8% CAGR through 2035, driven by IoT, wearable, and compact consumer electronics integration requirements.

CPU dominated with approximately 44.00% of revenues in 2025.

The extraordinary expansion of AI training and inference infrastructure investment at hyperscale cloud providers demanding chiplet-based GPU and accelerator architectures capable of exceeding reticle-size transistor count limitations, combined with the CHIPS and Science Act's domestic semiconductor manufacturing investment and the cost-effectiveness of heterogeneous integration architectures that enable semiconductor companies to combine specialized chiplets manufactured at optimal process nodes while reusing proven chiplet IP across multiple product generations.

The Chiplet Market was valued at USD 12.96 billion in 2025.

The Chiplet Market is expected to grow at a CAGR of 44.0% from 2026 to 2035.

Get in Touch