Circuit Breaker Market Report Scope & Overview:

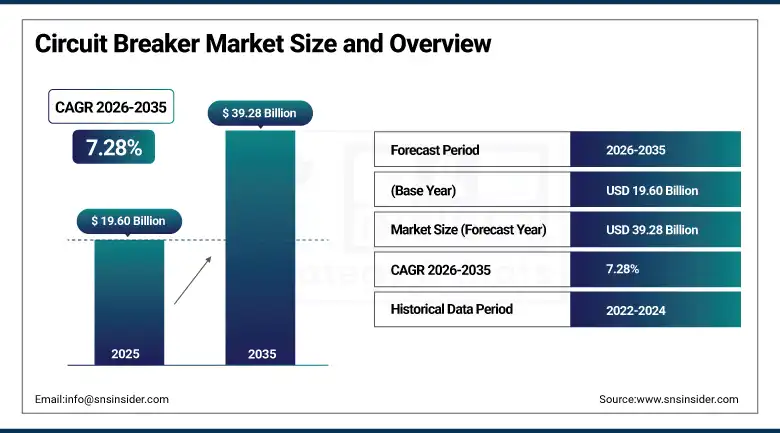

The Circuit Breaker Market was valued at USD 19.60 Billion in 2025 and is expected to reach USD 39.28 Billion by 2035, growing at a CAGR of 7.28% from 2026–2035.

The market for circuit breakers is experiencing a steady rate of growth that is commercially diverse in nature. Circuit breakers are critical safety devices that serve the purpose of cutting off the flow of electricity during faulty operations, thus protecting equipment from damage and ensuring that fires do not occur. This market is being spurred on by the need for increased infrastructure spending within grids, the rising number of renewable energy sources and their protection coordination, automation in industry, and increasing electric vehicle (EV) charging infrastructure installations.

In 2024, the Emax 2 Air Circuit Breaker was introduced by ABB, which comes with superior digital connectivity and IEC 61850 communication protocol capability, allowing power companies and other organizations to include monitoring and control of their circuit breakers within the digital platform for the management of the electrical grids. This product introduction is indicative of the commercial trend in circuit breaker technology towards intelligent circuit breakers whose safety and operational advantages are not available in the conventional circuit breakers.

Market Size and Forecast

-

Market Size in 2026E: USD 21.03 Billion

-

Market Size by 2035: USD 39.28 Billion

-

CAGR: 7.28% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Circuit Breaker Market - Request Free Sample Report

Circuit Breaker Market Trends

-

Smart circuit breaker adoption is increasing as utilities and industrial operators seek real-time monitoring and remote-control capabilities.

-

Renewable energy integration is creating new protection requirements across electricity grids. Bidirectional power flows from solar and wind installations require advanced circuit breakers capable of handling complex fault conditions.

-

Expansion of EV charging infrastructure is driving demand for residential and commercial circuit breakers. Dedicated protection systems are required to support the unique electrical loads associated with EV charging equipment.

-

Development of SF6-free circuit breakers is gaining momentum due to stricter environmental regulations. Manufacturers are increasingly investing in vacuum and clean-air technologies as alternatives to SF6-based switchgear.

-

Data centre construction is generating strong demand for high-performance circuit breakers. Large-scale facilities require reliable power distribution and protection systems to ensure uninterrupted operations and equipment safety.

U.S. Circuit Breaker Market Outlook

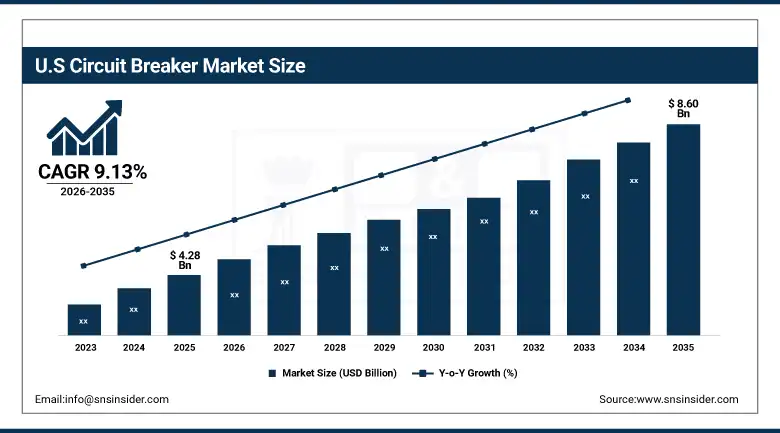

The U.S. Circuit Breaker Market was valued at approximately USD 4.28 Billion in 2025 and is expected to reach approximately USD 8.60 Billion by 2035, growing at a CAGR of approximately 9.13%.

The U.S. is the most commercially dynamic national circuit breaker market within the fastest-growing North American region. Bipartisan Infrastructure Law investment in grid modernisation, IRA incentives for clean energy infrastructure, and the manufacturing sector's reshoring investment are creating structured institutional and commercial circuit breaker procurement. The residential construction market's growth and EV charging infrastructure's distribution panel upgrade requirement are simultaneously creating consumer-facing circuit breaker demand that compounds with industrial and utility sector procurement.

Eaton Corporation launched its next-generation BR Arc Fault Circuit Interrupter in 2024, incorporating enhanced nuisance trip reduction algorithms that maintain required arc fault detection sensitivity while substantially reducing false trips from normal household appliances. The improved AFCI technology addresses the primary adoption barrier that has historically limited residential AFCI acceptance among electricians, creating commercial momentum for the broader residential circuit protection upgrade cycle driven by NEC code requirements.

Circuit Breaker Market Segment Analysis

-

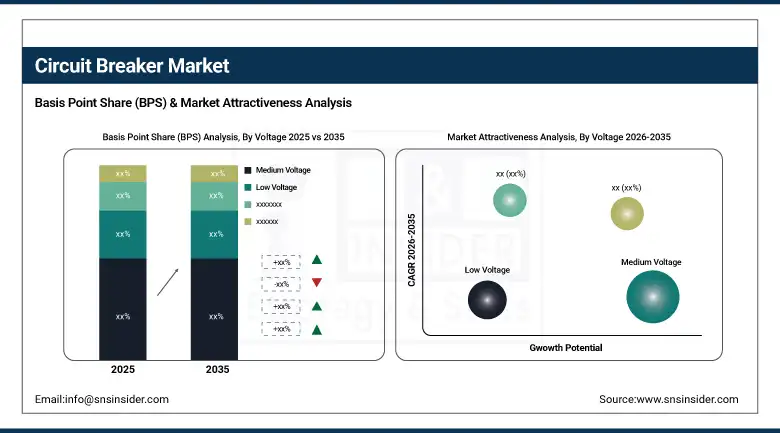

By Voltage, the Medium Voltage segment dominated the Circuit Breaker Market with approximately 52% share in 2025, while the High Voltage segment is the fastest growing.

-

By Type, the Gas/SF6 Circuit Breaker segment dominated the Circuit Breaker Market with approximately 44% share in 2025, while the Vacuum Circuit Breaker segment is the fastest growing.

-

By End User, the Utilities/T&D segment dominated the Circuit Breaker Market in 2025, while the Industrial segment is the fastest growing with a CAGR of approximately 8.68%.

-

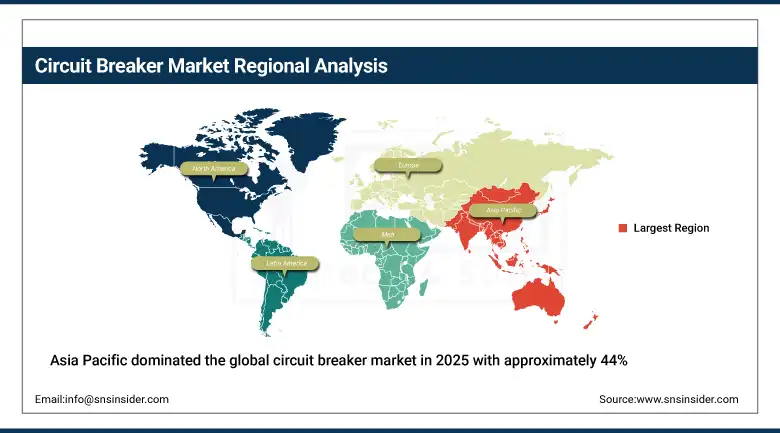

By Region, Asia Pacific dominated the Circuit Breaker Market with approximately 44% share in 2025, while North America is the fastest growing with a projected CAGR of approximately 9.13%.

By Voltage, medium voltage dominates, high voltage grows fastest

Medium voltage circuit breakers retained the dominant voltage position with approximately 52% of the circuit breaker market in 2025. MV circuit breakers serving the 1 kV to 36 kV voltage range define the distribution network protection infrastructure whose commercial scale reflects the extraordinary density of MV switchgear in the global power system. Each electrical substation, industrial facility main incoming panel, and commercial building primary distribution system requires MV circuit breakers whose aggregate global installed base creates consistent replacement, upgrade, and new installation procurement. Power grid modernisation programmes worldwide are creating the most commercially significant MV circuit breaker upgrade cycle in the market's history as digital protection relay integration and smart grid compatibility requirements motivate installed base replacement.

High voltage circuit breakers are the fastest-growing segment because transmission grid investment for renewable energy integration, interconnection infrastructure, and grid reliability improvement is creating new HV circuit breaker procurement whose per-unit commercial value substantially exceeds MV alternatives. Each new transmission substation, HVDC converter station, and grid interconnection project creates HV circuit breaker procurement whose individual contract value can reach millions of dollars per installation. The energy transition's requirement for new transmission capacity to connect remote renewable energy resources with population centres creates HV circuit breaker demand that is growing faster than any other voltage category.

By Type, gas/SF6 dominates, vacuum grows fastest

Gas and SF6 circuit breakers retained the dominant type position with approximately 44% of the circuit breaker market in 2025. SF6's extraordinary arc quenching capability, whose dielectric strength 2-3 times that of air at the same pressure enables compact switchgear designs that air-insulated alternatives cannot achieve, created the dominant market position that SF6 circuit breakers have maintained since their introduction in the 1960s. The global installed base of SF6-insulated switchgear and circuit breakers, representing decades of utility and industrial investment, creates replacement procurement that sustains SF6 circuit breaker commercial volume even as new installation specification progressively migrates toward SF6 alternatives.

Vacuum circuit breakers are the fastest-growing type because their maintenance-free sealed vacuum interrupter construction, absence of SF6 environmental liability, and compact design create compelling technical and regulatory advantages for medium voltage applications where SF6 phase-down regulation creates mandatory specification migration motivation. Each EU member state implementation of F-Gas Regulation SF6 restrictions creates new procurement pressure toward vacuum alternatives whose operational performance in MV applications has been thoroughly validated across decades of industrial and utility deployment.

By End User, utilities dominate, industrial grows fastest

Utilities and T&D retained the dominant end user position in the circuit breaker market in 2025. Electricity transmission and distribution utilities' systematic grid investment, whose scale is defined by the extraordinary capital expenditure of the global power sector, creates the most commercially concentrated and highest-volume circuit breaker customer segment. Each new substation, distribution feeder expansion, and transmission network upgrade creates circuit breaker procurement whose project scale and institutional procurement processes create predictable commercial relationships that circuit breaker manufacturers prioritise in product development and sales infrastructure investment.

Industrial is the fastest-growing end user at approximately 8.68% CAGR because the convergence of manufacturing reshoring, data centre expansion, mining electrification, and oil and gas facility automation is creating above-average industrial sector circuit breaker demand growth. Each new semiconductor fab, EV battery gigafactory, hyperscale data centre, and automated mining facility creates electrical distribution infrastructure requiring circuit breakers at quantities and specifications that sustain above-average per-project commercial value. The industrial sector's progressive electrification, replacing diesel-powered process equipment with electric alternatives, creates new circuit breaker demand categories that compound with industrial capital investment growth.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Circuit Breaker Market Insights

Asia Pacific dominated the global circuit breaker market in 2025 with approximately 44% of global revenues. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary power grid infrastructure investment, the State Grid Corporation and China Southern Power Grid's systematic capital expenditure programmes, and the rapid expansion of industrial and commercial electrical infrastructure. India's power sector investment under the RDSS programme and Southeast Asia's urbanisation-driven grid expansion create significant secondary market demand that reinforces Asia Pacific's commercial dominance.

Japan and South Korea represent technically sophisticated secondary markets whose advanced grid modernisation, renewable energy integration, and industrial automation create above-average per-unit circuit breaker specification. Mitsubishi Electric and Fuji Electric's Japanese operations contribute both domestic procurement and export-oriented product development whose global competitive position sustains Asia Pacific's circuit breaker manufacturing leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Circuit Breaker Market Insights

North America is the fastest-growing regional circuit breaker market at approximately 9.13% CAGR, driven by U.S. grid modernisation investment, IRA clean energy infrastructure incentives, and the manufacturing sector's reshoring programme. The United States accounts for approximately 87.4% of North American revenues through Eaton, ABB, Siemens, and Schneider Electric's commercial operations whose combined portfolio defines the North American intelligent circuit breaker standard. The residential construction market's NEC code-driven AFCI and GFCI requirement expansion creates consistent consumer-facing circuit breaker procurement that compounds with commercial and industrial sector investment.

Canada contributes approximately 12.6% of North American revenues through its utility sector's grid modernisation, the mining industry's electrical infrastructure, and the federal government's clean energy infrastructure investment that creates structured public sector circuit breaker procurement.

Europe Circuit Breaker Market Insights

Europe is a technically sophisticated circuit breaker market where EU F-Gas Regulation’s SF6 phase-down creates the most commercially transformative circuit breaker technology transition in the market's recent history. Germany accounts for approximately 22.3% of European revenues through Siemens’ domestic market leadership, the utility sector's energy transition grid investment, and the industrial sector's automation creating consistent procurement. ABB's Swiss headquarters and Schneider Electric's French operations sustain European circuit breaker supply from established regional commercial presences.

The United Kingdom, France, and Nordic markets are significant secondary European markets where grid modernisation, offshore wind connection, and industrial electrification create structured circuit breaker demand. The UK's National Grid Electricity System Operator's transmission investment and France's RTE grid modernisation programme create institutional-scale procurement that sustains European market growth.

MEA & Latin America Circuit Breaker Market Insights

The Middle East and Africa and Latin America are growing circuit breaker markets where power infrastructure development, industrial investment, and grid modernisation create structured demand. Saudi Arabia leads MEA revenues at approximately 31.2% through Saudi Electricity Company's grid investment, ARAMCO's industrial electrical infrastructure, and Vision 2030's industrial development creating new facility electrical distribution requirements.

Brazil leads Latin American revenues at approximately 44.2% through its power utility sector's distribution grid investment, the large industrial sector's electrical infrastructure, and the residential construction market's circuit breaker demand whose combined procurement sustains consistent commercial engagement with major circuit breaker suppliers.

Market Dynamics

Growth Drivers: Grid modernisation investment and renewable energy connection creating structured circuit breaker procurement

Grid modernisation investment is the circuit breaker market's most commercially certain structural growth driver. Utility capital expenditure programmes worldwide are systematically replacing ageing circuit breaker installed bases with modern digital-communication-enabled protection devices whose smart grid compatibility creates replacement demand beyond normal equipment lifecycle replacement timing. The Bipartisan Infrastructure Law, EU energy infrastructure investment, and China's grid capital expenditure programmes collectively define a multi-trillion-dollar procurement environment whose circuit breaker component creates the most commercially consistent demand in the electrical equipment market.

Renewable energy grid connection creates new circuit breaker procurement requirements beyond conventional grid expansion because solar and wind generation's bidirectional power flow creates protection coordination challenges that require circuit breakers capable of interrupting fault currents from generation sources as well as the supply network. Each new solar farm, wind park, and battery energy storage system grid connection creates circuit breaker procurement at both the generation facility and the grid interconnection point whose combined procurement scales with renewable energy capacity growth.

Restraints: SF6 phase-down regulatory timeline creating uncertainty and supply chain component shortage risk

EU F-Gas Regulation's SF6 phase-down timeline creates commercial uncertainty for utilities and industrial operators whose circuit breaker procurement planning must accommodate technology transition from SF6-insulated to vacuum or clean air alternatives. Each utility whose existing SF6 circuit breaker fleet requires replacement faces capital planning uncertainty as SF6-free alternatives' pricing and availability evolve during the technology transition period. The investment required to convert production from SF6 to vacuum and clean air circuit breakers creates capital allocation pressure for manufacturers whose product line transition timelines must align with customer procurement readiness.

Power semiconductor and electronic component supply chain disruptions create delivery uncertainty for smart circuit breakers whose digital communication modules, protection relay electronics, and IoT connectivity hardware require semiconductor components whose supply chain concentration in Asia Pacific creates geopolitical procurement risk. Each supply disruption episode that delays smart circuit breaker delivery extends project commissioning timelines and creates customer satisfaction risk that conventional mechanical circuit breakers do not face equivalently.

Opportunities: Smart circuit breaker market expansion and SF6-free technology premium market creation

Smart circuit breaker expansion represents the most commercially value-accretive near-term market development direction. Circuit breakers integrating digital protection relays, IEC 61850 communication, real-time fault data logging, and remote operation capability create premium product categories whose commercial value per unit substantially exceeds conventional mechanical circuit breakers. Utilities' systematic grid digitalisation investment is creating institutional procurement for smart circuit breakers whose intelligent protection coordination improves grid reliability metrics whose regulatory reporting creates financial motivation for above-average capital investment.

SF6-free circuit breaker technology creates a new premium product category whose environmental credentials create commercial differentiation in regulated markets where SF6 restrictions create mandatory technology specification migration. Vacuum circuit breakers and clean air (g3 fluoronitrile) circuit breakers whose environmental profile satisfies EU F-Gas Regulation requirements without the SF6 phase-down timeline uncertainty create structured procurement from utilities and industrial operators whose regulatory compliance programmes specify SF6-free alternatives in new installations before regulatory deadline requirements.

Recent Developments:

-

2024: ABB launched the Emax 2 Air Circuit Breaker with enhanced digital connectivity and IEC 61850 communication protocol support in 2024, enabling utilities and industrial operators to integrate circuit breaker monitoring and remote control directly into digital grid management platforms.

-

2024: Eaton Corporation launched its next-generation BR Arc Fault Circuit Interrupter in 2024 with improved nuisance trip reduction algorithms, addressing the primary adoption barrier for residential AFCI acceptance and creating commercial momentum for the NEC code-driven residential circuit protection upgrade market.

-

2024: Siemens Energy announced expanded production of SF6-free high-voltage circuit breakers using clean air technology in 2024, targeting utilities facing EU F-Gas Regulation SF6 phase-down requirements with viable HV circuit breaker alternatives whose environmental credentials satisfy regulatory mandates.

Circuit Breaker Market Key Players

-

ABB Ltd.

-

Siemens AG

-

Eaton Corporation

-

Schneider Electric

-

Mitsubishi Electric Corporation

-

General Electric (GE Vernova)

-

Fuji Electric Co., Ltd.

-

Legrand S.A.

-

Rockwell Automation

-

CHINT Group

-

Larsen & Toubro

-

Powell Industries

-

Kirloskar Electric

-

Mersen S.A.

-

Havells India

-

Lucy Electric

-

Toshiba Corporation

-

Hyundai Electric

-

LS Electric Co., Ltd.

-

CG Power & Industrial Solutions

Circuit Breaker Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 19.60 Billion |

| Market Size by 2035 | USD 39.28 Billion |

| CAGR | CAGR of 7.28% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Function (Anti-Corrosion, Self-Healing, Anti-Microbial, Anti-Fouling, Thermal Responsive, Others) • by Technology (Nanocoatings, Microencapsulation, Self-Assembling, Others) • by Substrate (Metal, Polymer, Glass, Ceramic, Others) • by End Use (Automotive, Aerospace & Defence, Healthcare & Medical, Construction, Marine, Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ABB Ltd., Siemens AG, Eaton Corporation, Schneider Electric, Mitsubishi Electric Corporation, General Electric (GE Vernova), Fuji Electric Co., Ltd., Legrand S.A., Rockwell Automation, CHINT Group, Larsen & Toubro, Powell Industries, Kirloskar Electric, Mersen S.A., Havells India, Lucy Electric, Toshiba Corporation, Hyundai Electric, LS Electric Co., Ltd., CG Power & Industrial Solutions |

Frequently Asked Questions

The Circuit Breaker Market is expected to grow at a CAGR of 7.28% from 2026 to 2035.

The Circuit Breaker Market was valued at USD 19.60 Billion in 2025.

Grid modernisation investment by utilities globally creating systematic circuit breaker procurement, and renewable energy grid connection creating new protection coordination requirements whose bidirectional power flow demands circuit breakers capable of interrupting fault currents from both utility and generation sources.

Medium Voltage dominated the Circuit Breaker Market with approximately 52% share in 2025, while High Voltage is the fastest growing segment.

Asia Pacific dominated the Circuit Breaker Market in 2025 with approximately 44% of global revenues, while North America is the fastest-growing region with a projected CAGR of approximately 9.13%.

Get in Touch