Circular Packaging Market Report Scope And Overview:

The circular packaging market is gaining momentum as industries embrace more sustainable practices, aligning with global initiatives to cut down on waste and promote recycling. This market revolves around the creation and utilization of packaging solutions explicitly designed to be reusable, recyclable, or compostable, aiming to minimize environmental harm. The central concept is to establish a "circular" lifecycle for packaging materials, ensuring that the end of one product's life marks the beginning of another, thereby reducing the reliance on raw materials and lessening carbon footprints.

Get More Information on Circular Packaging Market - Request Sample Report

The pivotal driver behind the growth of this market is the increasing recognition of the environmental repercussions associated with plastic and other non-degradable packaging materials. With plastic pollution emerging as a critical environmental challenge, especially in contributing to ocean waste, various industries, notably the consumer goods sector, are prioritizing the adoption of circular packaging strategies to strike a balance between business objectives and sustainability goals. Utilizing recycled materials in manufacturing can help limit landfill expansion and alleviate other environmental pressures.

MARKET DYNAMICS

KEY DRIVERS:

-

Consumer Demand for Eco-Friendly Packaging

Increasing consumer consciousness regarding environmental issues is driving demand for eco-friendly packaging. Consumers are actively seeking products with minimal environmental impact, leading businesses to adopt circular packaging to meet these preferences.

-

Growing awareness of environmental issues and a global shift towards sustainable practices are driving industries to adopt circular packaging solutions

RESTRAIN:

-

The availability of high-quality recycled materials suitable for circular packaging may be limited.

OPPORTUNITY:

-

Ongoing advancements in materials and technologies offer opportunities for the development of more sustainable and efficient circular packaging solutions.

-

The rising use of recycled plastic is expected to create a self-reinforcing cycle, increased demand boosts raw material prices, making recycling more economically viable.

CHALLENGES:

-

Circular packaging may have different weight, volume, or transportation requirements compared to traditional packaging.

-

Packaging companies face the challenge of ensuring widespread recyclability of their products while introducing new materials at scale to avoid potential consumer backlash and regulation.

Impact of Russia Ukraine War

The packaging industry worldwide, including the circular packaging sector, is facing significant challenges due to the Russia-Ukraine crisis. Supply chain disruptions, escalating raw material costs, and operational difficulties are putting strain on the industry. Major players like Ukraine's Karpatneftekhim, the largest petrochemical plant, and Vetropack, owners of the largest glass factory, have halted operations due to martial law declarations and damage caused by military actions. This cessation not only affects the supply of essential materials such as plastic granulate but also raises concerns about the industry's long-term prospects if the conflict continues.

The conflict has severely impacted Ukrainian enterprises like Re-Leaf Technology, halting operations due to logistical challenges and infrastructure damage. The aftermath includes potential long-term damage to Ukraine's infrastructure, significant financial losses, and a labour shortage post-war. The anticipated economic downturn in Ukraine and global companies exiting the Russian market due to reputational risks are altering market dynamics. While Ukrainian firms may have a small market share, the conflict's broader implications are shaping the circular packaging market's trajectory globally.

Impact of Economic Slowdown

Amidst an economic slowdown, the circular packaging market faces changes driven by consumer behaviour shifts, ongoing innovations, and regulatory shifts. Despite challenges, the packaging sector stays dedicated to sustainability, adjusting to market and regulatory changes. Sustainable packaging innovations are addressing environmental concerns by prioritizing recyclability, reusability, and composability. This aligns with growing consumer demand for eco-friendly products and the industry's commitment to reducing non-renewable materials. Collaboration across the value chain is crucial for advancing the circular economy in packaging, aiming to improve recycling systems and introduce new sustainable technologies.

Regulatory changes, particularly in regions like the European Union, are driving the industry towards sustainability. The EU's Packaging and Packaging Waste Regulation mandates recycled content targets, promoting recyclability and composability. Challenges remain, such as securing enough recycled materials and navigating global recycling systems. The industry is responding with innovations like bio-based materials and digital technologies to improve recycling processes and promote circularity in packaging.

KEY MARKET SEGMENTS

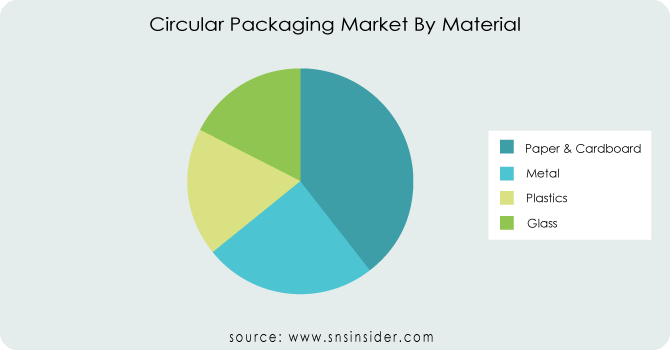

By Material

-

Paper & Cardboard

-

Metal

-

Plastics

-

Glass

Get Customized Report as per Your Business Requirement - Request For Customized Report

By Product Type

-

Bottles & Jars

-

Bags and Pouches

-

Containers and Tubs

-

Boxes and Cartons

By End Use

-

Boxes and Cartons

-

Food and Beverage

-

Pharmaceuticals

-

Others

REGIONAL ANALYSIS

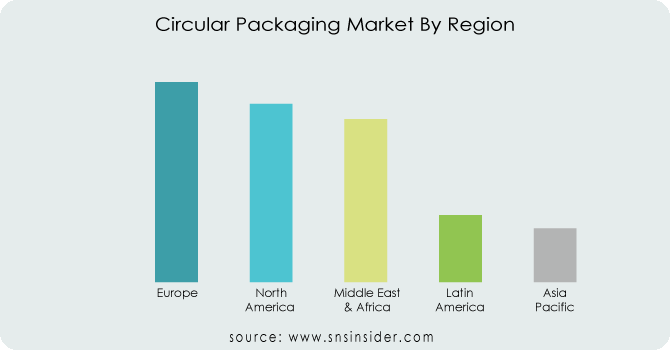

Europe has been a dominant force in the adoption of circular packaging due to stringent regulations, particularly within the European Union (EU). The EU's commitment to sustainability and circular economy principles has driven significant advancements in recyclable and compostable packaging solutions. North America, particularly the United States and Canada, has also been a major player in the circular packaging market. The region has seen increased consumer awareness and regulatory initiatives promoting eco-friendly packaging practices.

Asia-Pacific has been identified as one of the fastest-growing regions in the circular packaging market. Rapid industrialization, urbanization, and a growing middle class have led to increased consumption. As awareness of environmental issues rises, there is a notable shift towards sustainable and circular packaging solutions. Latin America is showing potential for significant growth in the adoption of circular packaging. Increasing awareness of sustainability, coupled with regulatory developments in certain countries, is driving the demand for eco-friendly packaging options.

REGIONAL COVERAGE:

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

Key players

Some of the major players in the Circular Packaging Market are Amcor plc, Sonoco Products Company, Berry Global Group, Inc, Sealed Air Corporation, Mondi plc, WestRock Company, Graphic Packaging Holding Company, International Paper Company, Huhtamäki Oyj, DS Smith Plc. and other players.

Amcor plc - Company Financial Analysis

RECENT TRENDS

-

Diageo has revealed a worldwide partnership with EcoSpirits, a circular economy technology firm, to create a flexible framework for testing and expanding circular packaging initiatives in approximately 18 markets within the next three years.

-

Manufacturer of high-performance packaging films Südpack together with dairy producer Arla Foods are testing a new process to ensure the circularity of mozzarella cheese packaging.

| Report Attributes | Details |

|---|---|

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Paper & Cardboard, Metal, Plastics, Glass) • By Product Type (Bottles & Jars, Bags And Pouches, Containers And Tubs, Boxes And Cartons) • By End Use (Boxes And Cartons, Food And Beverage, Pharmaceuticals, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Amcor plc, Sonoco Products Company, Berry Global Group, Inc, Sealed Air Corporation, Mondi plc, WestRock Company, Graphic Packaging Holding Company, International Paper Company, Huhtamäki Oyj, DS Smith Plc. |

| Key Drivers | • Consumer Demand for Eco-Friendly Packaging • Growing awareness of environmental issues and a global shift towards sustainable practices are driving industries to adopt circular packaging solutions |

| Restraints | • The availability of high-quality recycled materials suitable for circular packaging may be limited. |

Frequently Asked Questions

The Europe region held the largest market share and will continue to dominate the market.

Ongoing advancements in materials and technologies offer opportunities for the development of more sustainable and efficient circular packaging solutions.

The availability of high-quality recycled materials suitable for circular packaging may be limited.

The major players in the Circular Packaging Market are Amcor plc, Sonoco Products Company, Berry Global Group, Inc, Sealed Air Corporation, Mondi plc, WestRock Company, Graphic Packaging Holding Company, International Paper Company, Huhtamäki Oyj, DS Smith Plc. and other players.

The Key driver is consumer Demand for Eco-Friendly Packaging.

Get in Touch