Class 4 Truck Market Report Scope & Overview:

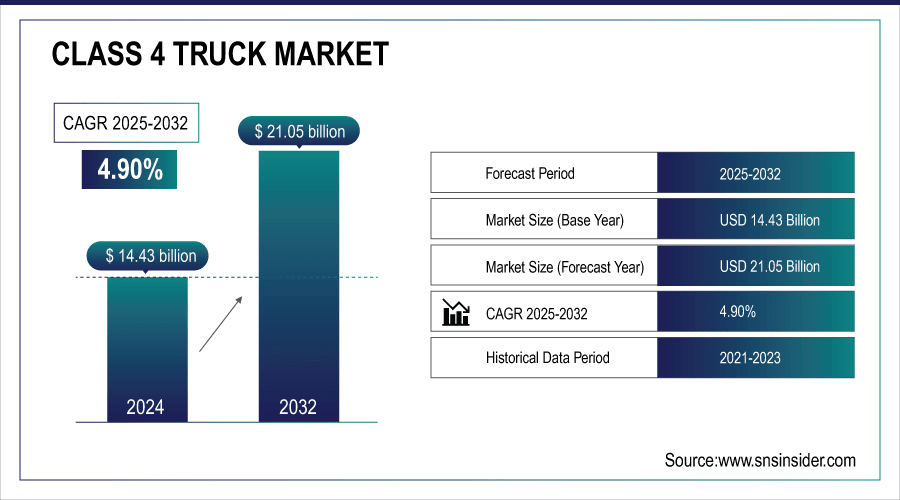

Class 4 Truck Market was valued at USD 15.14 billion in 2025 and is expected to reach USD 24.42 billion by 2035, growing at a CAGR of 4.90% from 2026-2035.

The Class 4 Truck Market is expanding owing to the increasing demand for efficient urban delivery solutions, the rise in e-commerce, and the increasing modernization of fleets. The adoption of electric and hybrid trucks owing to the increasing need for stricter emission standards and fuel efficiency enhancements also supports the market. Moreover, the development of infrastructure, advancements in telematics technology, and government support for eco-friendly commercial vehicles are encouraging the adoption of Class 4 trucks.

Government programs are also encouraging fleet owners to invest in Class 4 trucks. For example, the Inflation Reduction Act of 2022 provided USD 1 billion for the investment of clean, zero-emission heavy-duty vehicles. In addition, California’s Hybrid and Zero-Emission Truck and Bus Voucher Incentive Project (HVIP) provides point-of-sale rebates to consumers purchasing electric trucks.

To Get More Information On Class 4 Truck Market - Request Free Sample Report

Class 4 Truck Market Trends

-

Rising demand for medium-duty trucks in logistics, construction, and last-mile delivery is driving market growth.

-

Adoption of electric and hybrid Class 4 trucks is increasing due to emission regulations and sustainability goals.

-

Integration of telematics, fleet management, and safety technologies is enhancing operational efficiency.

-

Growth of e-commerce and urban delivery services is boosting demand for versatile medium-duty vehicles.

-

Government incentives and policies for clean transportation are supporting electric truck adoption.

-

Expansion of leasing and rental services is increasing market accessibility.

-

Collaborations between OEMs, technology providers, and fleet operators are accelerating innovation and deployment.

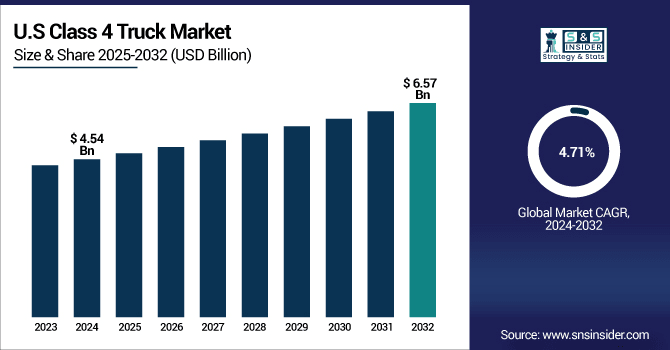

U.S. Class 4 Truck Market was valued at USD 4.75 billion in 2025 and is expected to reach USD 7.53 billion by 2035, growing at a CAGR of 4.71% from 2026-2035.

The U.S. Class 4 Truck Market is growing due to increasing e-commerce, demand for efficient last-mile delivery, fleet modernization, adoption of fuel-efficient and hybrid trucks, and supportive government incentives promoting eco-friendly commercial vehicles across urban and regional logistics.

Class 4 Truck Market Growth Drivers:

-

Adoption of Advanced Fuel-Efficient and Hybrid Technologies is Strengthening Class 4 Truck Market Demand Worldwide

Technological developments in fuel efficiency and emissions are encouraging fleet operators to choose Class 4 trucks with hybrid and electric propulsion systems. These trucks have operating costs that are substantially lower and comply with the toughest global emission standards. Government initiatives for environmentally responsible transportation are encouraging companies to develop technologically superior trucks. Companies that focus on research and development in light materials, aerodynamics, and telematics are enhancing the capabilities of trucks. Companies are increasingly adopting new trucks with advanced technology to cut costs and address the needs of city delivery. This relentless pursuit of technological innovation is a major driver for the market.

-

Under the EPA–DOT Heavy-Duty Phase 2 GHG standards (covering model years 2021–2027), advanced trucks are projected to reduce CO₂ emissions by up to 25%, save vehicle owners a total of USD 170 billion in fuel costs, and prevent up to 2 billion barrels of oil consumption yielding a net societal benefit of USD 230 billion.

-

The California Hybrid and Zero-Emission Truck and Bus Voucher Incentive Project (HVIP) administered by CARB is a primary example of how government incentives accelerate adoption of advanced Class 4-sized technologies.

-

As of December 2024, approximately 2,580 hybrid trucks and over 9,495 zero-emission trucks/buses have been supported via HVIP.

-

In total, around 15,100 clean vehicles have been deployed through the program, with estimated reductions of 1.357 million metric tons of CO₂e, 2,064 tons of NOₓ, 33.6 tons of hydrocarbons, and 80.5 tons of particulate matter.

-

In early 2025, over 5,000 HVIP-funded ZEVs were in production, accompanied by 16,327 charging and hydrogen fueling points installed statewide highlighting infrastructure growth alongside vehicle adoption.

Class 4 Truck Market Restraints:

-

High Purchase and Maintenance Costs of Class 4 Trucks are Limiting Market Expansion and Adoption

Class 4 trucks involve high initial purchase prices and significant maintenance costs, which can deter small and medium fleet operators. The price of spare parts, fuel, insurance, and repair is added to the overall cost of ownership, making it difficult for new entrants to adopt. Moreover, companies operating in developing areas have limited access to sources of funding, hindering the expansion of their fleet. Although there are long-term cost savings, the initial investment required for the development of advanced hybrid or electric Class 4 trucks may hinder the growth of the market.

Class 4 Truck Market Opportunities:

-

Growing E-Commerce and Urban Logistics Expansion Present Strong Opportunities for Class 4 Truck Market Growth

The increasing demand for e-commerce and the need for efficient delivery solutions in urban areas provide a massive opportunity for Class 4 trucks. Class 4 trucks are easier to maneuver in urban areas compared to heavy trucks because of their size, and their carrying capacity is also high. It is easy for businesses to extend their delivery areas with the help of Class 4 trucks. Additionally, businesses that are investing in electric and hybrid trucks can also capitalize on the increasing awareness of environmental issues. Collaborations between logistics companies and truck manufacturers to create solutions for urban delivery further improve market opportunities.

Class 4 Truck Market Segment Highlights

-

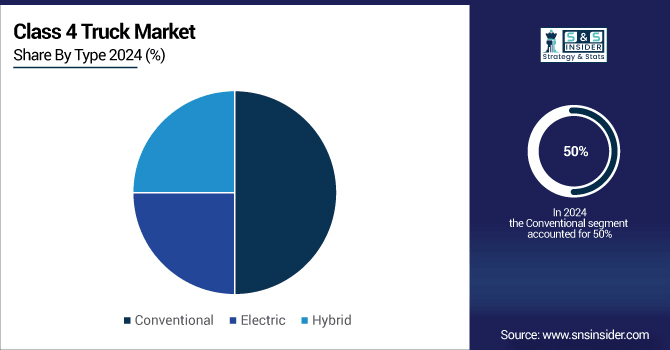

By Propulsion Type, Conventional dominated with 50% share in 2025; Hybrid fastest growing (CAGR).

-

By Application, General Delivery dominated with 41% share in 2025; Refrigerated Transportation fastest growing (CAGR).

-

By GVWR, 10,001 – 12,500 lbs dominated with 50% share in 2025; 14,501 – 16,500 lbs fastest growing (CAGR).

-

By Body Type, Dry Van dominated with 36% share in 2025; Refrigerated Van fastest growing (CAGR).

-

By Fuel Type, Diesel dominated with 56% share in 2025; Electric fastest growing (CAGR).

Class 4 Truck Market Segment Analysis

By Type, Conventional trucks dominated the Class 4 Truck Market in 2024, while Hybrid trucks are projected to grow fastest from 2026-2035.

Conventional trucks led the Class 4 Truck Market in 2025 because of their tested and trusted reliability, existing infrastructure, and relatively low purchase price. They are the most preferred type of truck by fleet operators for general delivery and commercial purposes, as they are rugged and easy to maintain.

Hybrid trucks are expected to register the highest growth rate between 2026 and 2035 as organizations continue to opt for fuel-efficient and eco-friendly trucks. Emission standards are increasing, and governments are offering incentives and technological advancements in battery and hybrid technology are promoting the adoption of new trucks.

By Application, General Delivery led in 2024, with Refrigerated Transportation expected to grow fastest due to rising cold chain logistics demand.

General Delivery was the largest in 2025 because of the rising e-commerce market, which requires efficient last-mile delivery. Class 4 trucks provide the best weight-carrying capacity and maneuverability to be used in urban areas, which helps in faster delivery, reduced operating costs, and improved performance, making them the most in-demand solution for logistics and courier services.

Refrigerated Transportation is expected to register the highest growth rate during the forecast period due to the growing demand for cold chain logistics. The increasing demand for online grocery, pharmaceutical, and perishable product delivery necessitates the use of refrigerated trucks. Organizations are adopting the latest refrigerated Class 4 trucks with energy-efficient cooling systems to cater to the demand for urban delivery and ensure product quality.

By Payload Capacity, the 10,001–12,500 lbs segment dominated in 2024, while 14,501–16,500 lbs is projected to grow fastest for heavier commercial loads.

The 10,001-12,500 lbs market was the largest in 2025 because these trucks are best suited for carrying payloads in urban areas while still being fuel-efficient. This market is preferred by fleet owners for general commercial use because it is a cost-effective solution for carrying moderate payloads in urban areas.

The 14,501-16,500 lbs market is expected to grow at the fastest rate from 2026 to 2035 because of the growing need for heavier payloads in commercial logistics. The payload capacity of the delivery trucks is being increased by companies to transport bulk materials, construction materials, and other specialized logistics. This is the perfect market for fleet owners who want to be more efficient without having to purchase more expensive trucks.

By Body Type, Dry Van trucks led in 2024, while Refrigerated Van trucks are expected to grow fastest for temperature-sensitive deliveries.

Dry Van trucks were the market leaders in 2025 because of their adaptability, easy maintenance, and ability to transport a variety of products. They are commonly used for general transport, retail transport, and e-commerce logistics. They provide secure cargo protection and are cost-effective, making them the most preferred vehicles for fleet owners in regional transportation.

The Refrigerated Van trucks are expected to have the highest growth rate from 2026 to 2035 due to the growing demand for the transportation of temperature-sensitive cargo. The rise in the e-commerce of pharmaceuticals, food, and perishable products is driving this demand. The latest cooling technology and energy-efficient solutions have made it possible to transport goods safely and on time, thus contributing to the growth of cold chain logistics and regional transportation services.

By Powertrain, Diesel trucks dominated in 2024, whereas Electric trucks are expected to grow fastest driven by environmental regulations and urban logistics adoption.

Diesel trucks were the most visible part of the market in 2025 due to the existing fuel infrastructure, lower purchase price, and high torque, which is optimal for various tasks. They are favored by fleet managers for their reliability and long-distance driving capabilities, which offer cost-effectiveness, durability, and easy maintenance for logistics tasks.

Electric trucks are expected to have the fastest growth rate from 2026 to 2035 because of environmental regulations, rising fuel costs, and government subsidies. Advances in battery technology, lower total cost of ownership, and urban logistics applications make electric Class 4 trucks an attractive solution, resulting in their rapid adoption for last-mile and commercial delivery logistics.

Class 4 Truck Market Regional Analysis

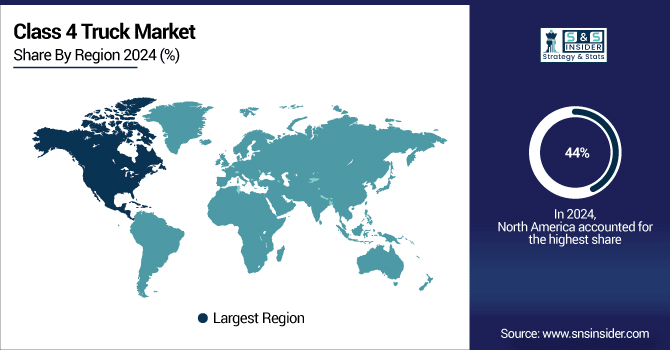

North America Class 4 Truck Market Insights

North America led the Class 4 Truck Market with the largest revenue share of approximately 44% in 2025 because of its established logistics network, high e-commerce adoption, and widespread truck modernization. The demand for last-mile delivery trucks, favorable government regulations, and the presence of major truck manufacturers further fueled the market adoption and revenue leadership in the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Class 4 Truck Market Insights

The Asia Pacific market is anticipated to register the fastest CAGR during the period 2026-2035, driven by the growing urbanization, rising e-commerce transactions, and developing logistics infrastructure. The increasing need for effective last-mile delivery solutions, government support for eco-friendly trucks, and growing industrialization are expected to fuel the growth of the Class 4 Truck Market in the Asia Pacific, making it the fastest-growing market during the forecast period.

Europe Class 4 Truck Market Insights

The Europe Class 4 Truck Market is a prominent market in the global Class 4 Truck Market, driven by the region's strict emission norms, well-developed transportation infrastructure, and the need for effective urban logistics solutions. The adoption of electric and hybrid trucks is increasing in the region, thanks to government support. The growing e-commerce business and the need for modernization of logistics infrastructure by logistics companies are also expected to fuel the growth of the Class 4 Truck Market in the Europe region.

Middle East & Africa and Latin America Class 4 Truck Market Insights

Middle East & Africa show moderate growth in the Class 4 Truck Market due to expanding urbanization, infrastructure development, and rising demand for commercial delivery vehicles. Latin America is experiencing a growing market due to the rise of e-commerce, the modernization of logistics, and government support for expanding the fleet. Both regions offer emerging opportunities for the development of the Class 4 truck market.

Class 4 Truck Market Competitive Landscape:

Ford Motor Company

Ford Motor Company is one of the major participants in the Class 4 Truck Market, as it provides dependable and fuel-efficient medium-duty trucks for commercial and urban delivery use. Its product offerings, such as the F-Series, are known for their ruggedness, sophisticated safety technologies, and low operating expenses. Innovation, its dealer network, and emphasis on electric and hybrid models improve its position in the market.

-

In 2025, Ford Motor Company Unveiled the Ranger Super Duty, a factory-built heavy-duty mid-size pickup offering 4,500 kg gross vehicle mass, robust towing (4,500 kg), and combined mass (8,000 kg), plus integrated smart features like onboard scales and device mounts.

-

In 2024, Ford Motor Company Revealed the Ranger Plug-In Hybrid, introducing electrified capability to mid-size truck segment. Equipped with Pro Power Onboard, it offers zero-emission driving and worksite power from a hybrid powertrain.

-

In 2023, Ford Motor Company Introduced advanced 4WD systems on the Ranger and Everest featuring electronic shift-on-the-fly and 4A (automatic) mode, enabling seamless off-road capability and adaptability for diverse work conditions.

General Motors

General Motors is one of the major players in the Class 4 Truck Market, as it offers flexible and dependable medium-duty trucks. The Chevrolet line of trucks is built to be tough, fuel-efficient, and versatile, making it ideal for use in urban delivery, construction, and other specialized applications. Chevrolet trucks benefit from excellent support services, advanced safety solutions, and innovations in truck design.

-

In 2025, General Motors (Chevrolet) Announced the all-new Chevrolet Low Cab Forward lineup, offering multiple GVWR options up to ~33,000 lbs, a wide 31.5-ft turning radius, extensive wheelbase choices, and upfit flexibility for diverse vocational needs.

Volvo Group

Volvo Group is a major competitor in the Class 4 Truck Market, providing long-lasting and technologically advanced medium-duty trucks. The trucks are designed to focus on fuel economy, safety, and driver comfort, which are suitable for a variety of applications including delivery, construction, and specialty carriers. Global market presence, innovation, and a focus on sustainable solutions make Volvo Group a more competitive player in the Class 4 truck market.

-

In 2024, Volvo Group Launched the second-generation Volvo VNL Class 8 truck in North America, with digital mirrors, full-digital dash, faster I-Shift transmission, aerodynamic upgrades, and trims tailored for efficiency and driver comfort.

Key Players

Some of the Class 4 Truck Market Companies

-

Ford Motor Company

-

General Motors

-

Stellantis

-

Isuzu Motors Ltd.

-

Hino Motors Ltd.

-

Daimler Trucks North America LLC

-

Volvo Group

-

Navistar International Corporation

-

Mitsubishi Fuso Truck and Bus Corporation

-

PACCAR Inc.

-

Iveco

-

MAN Truck & Bus AG

-

Scania AB

-

Tata Motors

-

Mahindra & Mahindra Ltd.

-

Freightliner

-

Chevrolet

-

Ram Trucks

-

International Trucks

-

Hercules Truck & Bus Co.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.14 Billion |

| Market Size by 2035 | USD 24.42 Billion |

| CAGR | CAGR of 4.90% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type(Conventional, Electric, Hybrid) • By Application(General Delivery, Construction, Hazardous Material Transportation, Refrigerated Transportation) • By Payload Capacity(10,001 - 12,500 lbs, 12,501 - 14,500 lbs, 14,501 - 16,500 lbs, 16,501 - 18,500 lbs) • By Body Type(Dry Van, Flatbed, Refrigerated Van, Dump Truck, Box Truck) • By Powertrain(Diesel, Gasoline, Electric) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Ford Motor Company, General Motors, Stellantis, Isuzu Motors Ltd., Hino Motors Ltd., Daimler Trucks North America LLC, Volvo Group, Navistar International Corporation, Mitsubishi Fuso Truck and Bus Corporation, PACCAR Inc., Iveco, MAN Truck & Bus AG, Scania AB, Tata Motors, Mahindra & Mahindra Ltd., Freightliner, Chevrolet, Ram Trucks, International Trucks, Hercules Truck & Bus Co. |

Frequently Asked Questions

North America dominated with about 44% revenue share in 2025, supported by advanced logistics infrastructure, e-commerce growth, and modernized truck fleets.

The Conventional segment dominated with the highest revenue share in 2025 due to proven reliability, lower costs, and widespread adoption in urban logistics.

Market growth is driven by rising e-commerce, urban delivery demand, fleet modernization, and adoption of fuel-efficient, electric, and hybrid Class 4 trucks globally.

The global Class 4 Truck Market was valued at USD 15.14 billion in 2025, with North America contributing approximately 44% of total revenue.

The Class 4 Truck Market is projected to grow at a CAGR of 4.90% from 2026 to 2035, reaching USD 24.42 billion.

Get in Touch