Clinical Trial Equipment & Ancillary Solutions Market Report Scope & Overview:

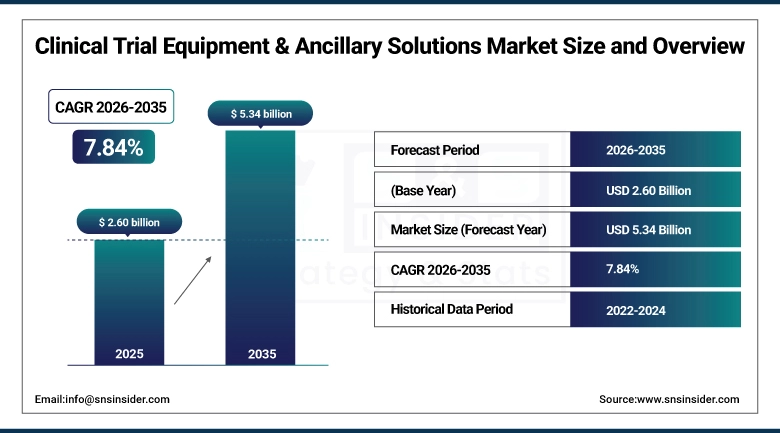

The Clinical Trial Equipment & Ancillary Solutions Market was valued at USD 2.60 billion in 2025 and is expected to reach USD 5.34 billion by 2035, growing at a CAGR of 7.84% from 2026-2035.

The logistical infrastructure that makes clinical trials possible the investigational product storage freezers, temperature monitoring systems, centrifuges, specimen shipping containers, trial-specific supplies, and the supply chain management services that procure and distribute them — is an under-recognized but commercially essential component of the clinical research enterprise. Every clinical trial must provision each investigative site with the specific equipment and supplies that the protocol requires: if the protocol calls for blood samples centrifuged within 30 minutes of collection and stored at -80°C before central laboratory processing, every participating site needs access to a centrifuge with appropriate specifications and an ultra-low temperature freezer and someone must source, procure, calibrate, maintain, and at trial completion, return or dispose of these assets across potentially dozens of sites on multiple continents. This is the work of the clinical trial equipment and ancillary solutions industry a specialized supply chain whose participants provide trial-specific procurement, equipment rental and maintenance, cold chain shipping, specimen transport, and ancillary supply management that CROs and pharmaceutical sponsors outsource to specialists. Precision medicine, cell and gene therapy, and biologic trials each requiring more specialized equipment and more careful handling than conventional pharmaceutical trials historically demanded.

ClinicalTrials.gov registry data documents that actively recruiting clinical trials globally exceeded 65,000 in 2024 — a record — with oncology representing the largest therapeutic area and precision medicine trials the fastest-growing category. PhRMA's annual report documents that U.S. pharmaceutical and biotech companies invested a record USD 102 billion in R&D in 2023, with clinical development representing 55-60% of total R&D spend — creating the trial activity that sustains clinical trial equipment and ancillary solutions market demand.

Clinical Trial Equipment & Ancillary Solutions Market Size and Forecast

-

Market Size in 2025: USD 2.60 Billion

-

Market Size by 2035: USD 5.34 Billion

-

CAGR: 7.84% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Clinical Trial Equipment & Ancillary Solutions Market - Request Free Sample Report

Clinical Trial Equipment & Ancillary Solutions Market Trends

-

Decentralized clinical trial (DCT) adoption is expanding the equipment and supply chain requirements from traditional investigative site provisioning to include patient home-visit kits, wearable biosensor devices, and direct-to-patient supply shipments whose logistics complexity requires specialized ancillary solution providers.

-

Cell and gene therapy clinical trial proliferation is creating ultra-specialized cryogenic equipment requirements — including liquid nitrogen dry shippers, controlled-rate freezers, and cryogenic sample management systems — whose supply is limited and whose demand growth is outpacing existing equipment provider capacity.

-

Digital supply chain platforms integrating investigational product tracking, equipment status monitoring, and ancillary supply inventory management are enabling sponsor and CRO visibility across complex multi-site global trial equipment networks that manual management cannot provide at adequate quality.

-

Single-use clinical equipment solutions — providing trial-specific single-use diagnostic and sample collection equipment that eliminates cleaning validation requirements between patient uses — are growing as trial protocols for infectious disease and immunocompromised patient populations require infection control standards that reusable equipment cannot consistently meet.

-

Clinical equipment asset tracking using RFID and IoT sensors is enabling real-time location and condition monitoring of expensive portable equipment — centrifuges, infusion pumps, portable monitoring devices — distributed across investigative site networks, reducing equipment loss and enabling proactive maintenance scheduling.

-

Sustainable trial supply chains — using recyclable shipping containers, optimizing shipment consolidation to reduce carbon footprint, and right-sizing cold chain packaging to minimize refrigerant waste — are becoming sponsor requirements driven by pharmaceutical company ESG commitments that extend through their clinical trial supply chain.

-

International investigational product import-export regulatory complexity — where country-specific customs documentation, import permit requirements, and regulatory approval conditions for investigational products vary substantially across the 50+ countries that global Phase III trials span — sustains demand for regulatory specialists within ancillary solution providers.

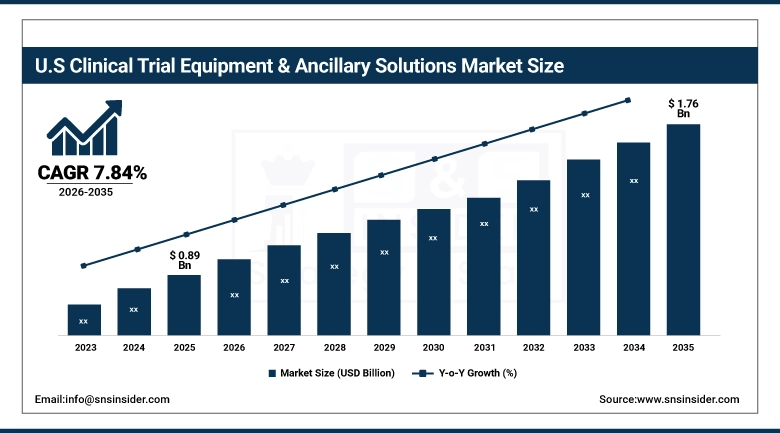

U.S. Clinical Trial Equipment & Ancillary Solutions Market was valued at USD 0.89 billion in 2025 and is expected to reach USD 1.76 billion by 2035, growing at a CAGR of 7.84% from 2026-2035.

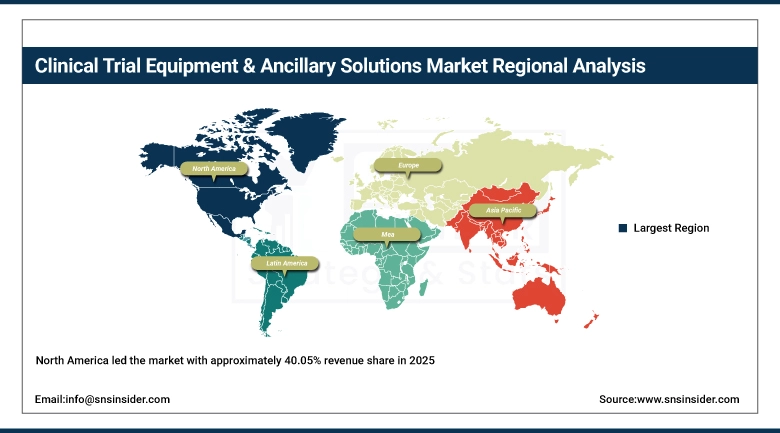

North America led the Clinical Trial Equipment & Ancillary Solutions Market with approximately 40.05% revenue share in 2025, driven by the United States' combination of the world's most active clinical trial ecosystem where approximately 34% of all globally registered clinical trial sites are located in the U.S. and the most developed clinical trial support industry whose specialized service providers include Almac Group, World Courier (AmerisourceBergen), Marken (UPS Healthcare), Myonex (Catalent), and Fisher Clinical Services. The U.S. market's clinical trial activity concentration where major pharmaceutical and biotech company headquarters are clustered in Boston, San Francisco, New Jersey, and New York — sustains the demand for trial equipment and ancillary solutions that the world's largest pharmaceutical R&D market generates. FDA's clinical trial regulatory requirements — including the 21 CFR Part 11 electronic records and signatures compliance for equipment calibration documentation, and the ICH guidelines governing clinical supplies management — sustain quality system demands for equipment providers that create differentiated capability barriers supporting premium pricing.

The Association of Clinical Research Organizations documents that U.S. contract research organizations managed clinical trials with aggregate value exceeding USD 25 billion in 2023, with each trial generating proportional equipment and ancillary solution procurement requirements across its investigative site network. Catalent's fiscal 2024 clinical supply services revenue — which encompasses investigational product manufacturing, labeling, packaging, and distribution alongside equipment and ancillary solutions exceeded USD 1 billion, demonstrating the commercial scale of the integrated clinical trial supply chain market.

Clinical Trial Equipment & Ancillary Solutions Market Segment Analysis

-

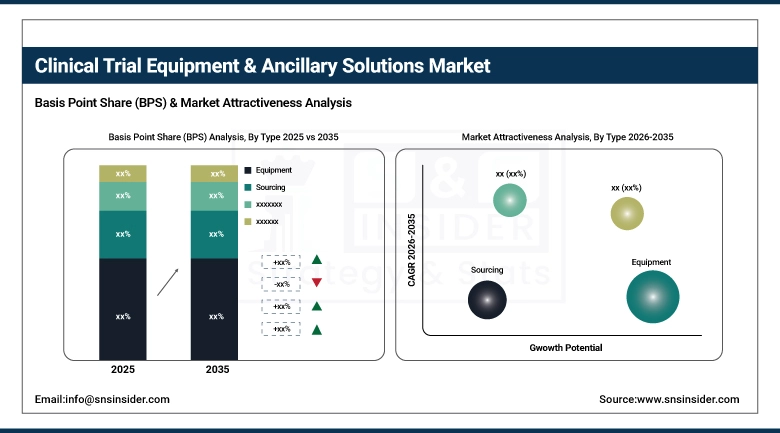

By Type, Equipment dominated the Clinical Trial Equipment & Ancillary Solutions Market in 2025; Sourcing segment growing at the fastest CAGR driven by outsourcing and single-vendor supply models.

-

By Phase, Phase III dominated with the largest share in 2025; Phase I growing at the fastest CAGR driven by early-stage precision medicine and gene therapy trials.

By Type: Equipment dominates, Sourcing growing fastest

Equipment held the dominant type position in the Clinical Trial Equipment & Ancillary Solutions Market in 2025, reflecting the capital-intensive nature of the specialized laboratory and clinical equipment that each trial protocol requires at investigative sites. Trial equipment encompasses a wide range: ultra-low temperature freezers for biological sample storage, ambient temperature refrigerators for less sensitive specimens, centrifuges for sample processing, spirometers for respiratory function measurement, holter monitors for cardiac monitoring, infusion pumps for drug administration, wearable biosensor systems for continuous monitoring, and specialized diagnostic equipment for protocol-specific assessments. Each protocol creates a distinct equipment list whose items may be sourced, rented, or deployed from equipment provider inventory — creating the procurement challenge that specialized clinical equipment companies address more efficiently than trial sponsors managing hundreds of equipment items across dozens of investigative sites.

The Sourcing segment is projected to grow at the fastest CAGR, supported by increased outsourcing of clinical trial procurement functions and the shift toward single-vendor supply models where one ancillary solutions provider manages the complete procurement, vendor qualification, distribution, and returns logistics for an entire trial's non-IP supply requirements. Single-vendor ancillary sourcing — where a sponsor entrusts one provider with procurement responsibility for everything from syringes and lab consumables through equipment rental and ancillary medication supply — provides sponsors with simplified vendor management, consolidated quality oversight, and supply chain risk management that multi-vendor alternative procurement cannot match at equivalent quality control confidence.

By Phase: Phase III dominates, Phase I growing fastest

Phase III trials held the dominant phase position in the Clinical Trial Equipment & Ancillary Solutions Market in 2025, reflecting the resource intensity of pivotal registration trials whose patient enrollment scale, multi-site geographic distribution, and protocol complexity create the largest single-trial equipment and ancillary solution budgets in the clinical development program. A global Phase III oncology trial enrolling 500 patients across 100 sites in 30 countries requires equipment provisioning at each site — centrifuges, freezers, sample collection supplies alongside international cold chain logistics for specimen transport, ancillary medication supply chains for concomitant medications, and patient kit distribution for at-home assessments. Each of these elements creates equipment and ancillary solution procurement demand that sustains Phase III segment revenue dominance.

Phase I is growing at the fastest CAGR, driven by the expanding number of first-in-human clinical trials particularly in precision medicine, cell and gene therapy, and biologic modalities whose early-phase programs require specialized equipment and cold chain handling that conventional Phase I trials historically did not demand. Cell therapy Phase I trials require cryogenic chain management from the leukapheresis collection at the investigative site through manufacturing processing to finished product release and administration a cold chain complexity that Phase I oncology conventional drug trials never required and whose specialized equipment and logistics demands create premium revenue opportunities for providers with established cell therapy logistics capabilities. The FDA's record IND filing volumes 1,756 in FY2025 create a growing pipeline of Phase I programs whose equipment and supply needs sustain Phase I market growth above Phase III's large but more stable patient population base.

Clinical Trial Equipment & Ancillary Solutions Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Europe |

United Kingdom |

27% |

|

Asia Pacific |

China |

38% |

|

Middle East & Africa |

Israel |

42% |

|

Latin America |

Brazil |

50% |

North America Clinical Trial Equipment & Ancillary Solutions Market Insights

North America led the market with approximately 40.05% revenue share in 2025, driven by the United States' exceptional clinical trial concentration and the presence of leading clinical trial equipment and ancillary solution companies. Almac Group, Marken (UPS Healthcare), World Courier (AmerisourceBergen), Fisher Clinical Services (Thermo Fisher), Myonex (Catalent), and Yourway Transport collectively represent a sophisticated U.S. clinical trial support industry whose capabilities span investigational product distribution, equipment rental, specimen logistics, and ancillary sourcing. The U.S. market's clinical supply chain infrastructure particularly the temperature-controlled warehousing and transport networks that pharmaceutical clinical logistics require sustains quality standards whose ICH compliant documentation creates differentiated service capability barriers that international competitors seeking U.S. market entry must establish before competing for major pharmaceutical sponsor contracts.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Clinical Trial Equipment & Ancillary Solutions Market Insights

Asia Pacific is the fastest-growing regional Clinical Trial Equipment & Ancillary Solutions Market, driven by the global pharmaceutical industry's progressive migration of clinical trial activity toward Asian investigative sites where patient recruitment speed, cost efficiency, and disease prevalence align with trial sponsor commercial objectives. China's NMPA regulatory alignment with ICH standards has made China-based investigative sites viable for global multi-regional trials, creating growing equipment and ancillary solution demand from China's rapidly expanding clinical research infrastructure. India's large patient population, English-language scientific community, and GCP-compliant clinical site ecosystem are attracting clinical trial outsourcing from major pharmaceutical companies whose speed-to-enrollment objectives make India a strategically important clinical geography.

Europe Clinical Trial Equipment & Ancillary Solutions Market Insights

Europe's Clinical Trial Equipment & Ancillary Solutions Market holds a substantial position driven by the UK, Germany, France, Spain, and the Netherlands as primary clinical trial markets. The EU Clinical Trials Regulation (EU CTR No 536/2014) harmonization which simplified multi-country trial authorization across EU member states has sustained European clinical trial activity that would otherwise have migrated to less regulated geographies. European clinical trial logistics providers including Almac (UK), Kuehne+Nagel (Switzerland), and World Courier serve major pharmaceutical companies' European clinical supply chain requirements whose regulatory complexity including GDP-compliant temperature-monitored transport documentation sustains premium service pricing above commodity pharmaceutical logistics.

MEA and Latin America Clinical Trial Equipment & Ancillary Solutions Market Insights

Israel's Clinical Trial Equipment & Ancillary Solutions Market is active relative to its size, reflecting the country's dense clinical trial activity Israel has one of the world's highest per-capita clinical trial participation rates whose multinational pharmaceutical company presence and sophisticated clinical research infrastructure creates proportional equipment and ancillary solution demand. Latin America's market is growing in Brazil and Mexico, where pharmaceutical companies are conducting increasing clinical trial activity attracted by large patient populations, diverse disease profiles, and improving GCP regulatory frameworks that enable data inclusion in global regulatory submissions.

Clinical Trial Equipment & Ancillary Solutions Market Growth Drivers:

Rising clinical trial volume and cell & gene therapy complexity driving sustained clinical trial equipment market growth globally

The Clinical Trial Equipment & Ancillary Solutions Market's 7.84% CAGR is driven by the compound effect of growing global clinical trial volume driven by pharmaceutical R&D investment records and the expanding precision medicine and biologic pipeline and increasing per-trial equipment and ancillary complexity driven by advanced therapy modalities. The global clinical trial pipeline's shift toward precision medicine, cell therapy, gene therapy, and bispecific antibody modalities each requiring more specialized equipment handling, more carefully managed cold chains, and more protocol-specific supply sourcing than conventional small molecule trials creates per-trial equipment and ancillary solution spending that substantially exceeds historical averages. Each cell therapy trial requiring centralized manufacturing and decentralized administration adds a cryogenic cold chain round-trip to the equipment and logistics budget that traditional injectable drug trials never included.

Clinical Trial Equipment & Ancillary Solutions Market Restraints:

Regulatory complexity and supply chain disruptions creating clinical trial equipment market challenges globally

The Clinical Trial Equipment & Ancillary Solutions Market faces supply chain reliability challenges that pharmaceutical sponsors and patients ultimately bear: equipment delivery delays at trial startup, cold chain excursion events during specimen shipping, and ancillary supply shortages during global disruptions each create trial delays that cost pharmaceutical companies hundreds of thousands of dollars per day of protocol execution delay. The COVID-19 pandemic's disruption of global logistics networks causing delays in equipment deployment, specimen transport failures, and investigational product supply chain disruptions demonstrated the clinical trial supply chain's vulnerability to macro logistical events, motivating sponsors to diversify supplier relationships and build supply chain redundancy that increases operating costs but improves resilience.

Clinical Trial Equipment & Ancillary Solutions Market Opportunities:

Decentralized trial equipment supply and digital supply chain management creating clinical trial ancillary solutions market growth opportunities

Decentralized clinical trial equipment supply where patients participating in home-based trial assessments receive trial-specific equipment kits and sample collection supplies shipped directly to their homes represents the market's most significant growth opportunity, because DCT adoption by pharmaceutical sponsors is expanding the equipment distribution scope from investigative sites to patient homes at scale. Each DCT patient interaction requiring a blood draw generates a patient home kit containing requisite supplies for sample collection, processing, and shipment whose kit assembly, distribution, and returns logistics sustain ancillary solution provider revenue per patient above equivalent site-based trial interactions. Digital supply chain management platforms real-time inventory visibility, automated reorder triggers, temperature monitoring integration, and regulatory document management create differentiated value for equipment and ancillary providers whose digital capabilities enable more efficient, compliant, and transparent supply chain management than legacy manual processes.

Recent Developments:

-

2026: Marken (UPS Healthcare) launched its CelliRx cryogenic cell therapy logistics platform combining liquid nitrogen dry shipper management, cryogenic monitoring with 15-minute temperature alert response, chain of custody documentation, and regulatory import-export coordination in 35 countries providing pharmaceutical companies developing CAR-T and stem cell therapies with a purpose-built logistics network that addresses the specific cryogenic chain integrity, tracking, and documentation requirements that cell therapy clinical trial logistics demand beyond conventional clinical supply chain capabilities.

-

2025: Almac Group opened its Singapore clinical supply center its first Asia Pacific cold chain clinical logistics facility providing -20°C and -80°C storage, GMP-compliant packaging, regional distribution across Southeast Asia, and ancillary sourcing services to pharmaceutical companies conducting clinical trials in Singapore, Malaysia, and the broader ASEAN region, addressing the supply chain gap that limited clinical trial activity in Southeast Asia when investigational products required transshipment through European or North American hubs.

-

2025: Thermo Fisher Scientific launched its Evidex clinical supply management platform integrating investigational product tracking, equipment calibration management, ancillary inventory monitoring, and cold chain excursion reporting in a single cloud-based dashboard providing pharmaceutical sponsors with real-time visibility into their global clinical supply chain status that previously required manual consolidation of reports from multiple supply chain vendor systems.

Clinical Trial Equipment & Ancillary Solutions Market Key Players

Some of the Clinical Trial Equipment & Ancillary Solutions Market Companies

-

Almac Group Ltd.

-

Marken Ltd. (UPS Healthcare)

-

World Courier Inc. (AmerisourceBergen)

-

Fisher Clinical Services (Thermo Fisher Scientific)

-

Myonex Inc. (Catalent)

-

Yourway Transport Inc.

-

Biocair Ltd.

-

Woodley Equipment Company Ltd.

-

Imperial CRS Inc.

-

Emsere SAS

-

Quipment SAS

-

MNX Global Logistics

-

Parexel International Corporation

-

IQVIA Holdings Inc.

-

Ancillare LP

-

IRM (International Resource Management)

-

ClinSupplies Ltd.

-

Eurofins CDMO

-

Catalent Inc. (Clinical Supply Services)

-

PCI Pharma Services

Clinical Trial Equipment & Ancillary Solutions Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.60 Billion |

| Market Size by 2035 | USD 5.34 Billion |

| CAGR | CAGR of 7.84% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product [Sourcing (Procurement, Rental), Supply/Logistics (Transportation, Packaging, Others), Service (Calibrations, Equipment servicing, Others), Others] • By Phase [Phase I, Phase II, Phase III, Phase IV] |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Almac Group Ltd., Marken Ltd. (UPS Healthcare), World Courier Inc. (AmerisourceBergen), Fisher Clinical Services (Thermo Fisher Scientific), Myonex Inc. (Catalent), Yourway Transport Inc., Biocair Ltd., Woodley Equipment Company Ltd., Imperial CRS Inc., Emsere SAS, Quipment SAS, MNX Global Logistics, Parexel International Corporation, IQVIA Holdings Inc., Ancillare LP, IRM (International Resource Management), ClinSupplies Ltd., Eurofins CDMO, Catalent Inc. (Clinical Supply Services), PCI Pharma Services |

Frequently Asked Questions

The market was valued at USD 2.60 billion in 2025.

North America dominated with approximately 40.05% share; Asia Pacific is the fastest growing.

Sourcing is growing at the fastest CAGR driven by outsourcing and single-vendor supply model adoption.

Phase III dominated with the largest share; Phase I is growing at the fastest CAGR.

The market is expected to grow at a CAGR of 7.84% from 2026 to 2035.

Get in Touch