Cloud Communication Platform Market Report Scope & Overview:

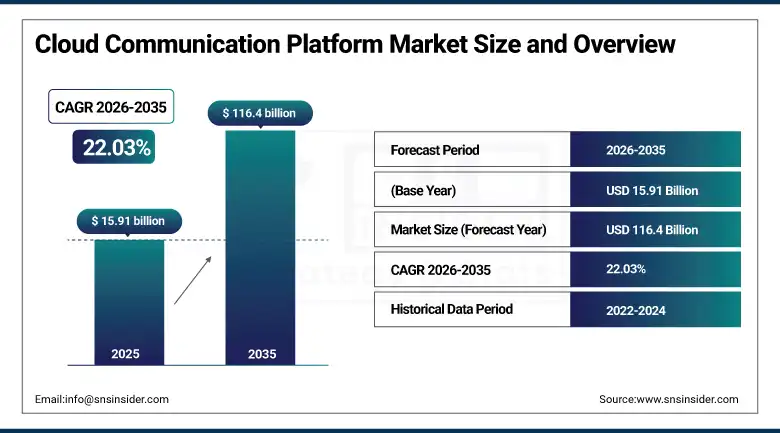

The Cloud Communication Platform Market was valued at USD 15.91 Billion in 2025 and is expected to reach USD 116.4 Billion by 2035, growing at a CAGR of 22.03% from 2026–2035.

Cloud communication platforms have evolved to become essential components of modern business operations worldwide. There was a far quicker shift away from traditional telephone-based premises to the cloud-based unified communications system due to and since the pandemic than many predicted. All organizations now expect seamless interaction of voice, video, messaging, and collaboration services within a single solution. On-premise PBX systems are becoming obsolete at an increasing pace. Cloud-based solutions are cheaper to manage, easier to scale, and update automatically with no need for IT departments to be responsible for the refresh cycle of equipment. Efficiency improvements are immediate and quantifiable. There are basically two products that define this space currently. The UC&C product category offers integration of voice, video, chat services, and file sharing into a single solution. CPaaS involves providing programmable communications APIs to developers, allowing them to integrate communications functionality directly into applications and workflow. The application of AI is changing both categories dramatically today. Features like real-time transcription, sentiment detection, intelligent call routing, and automated note-taking are becoming common across the leaders in this market segment. More than 70 percent of cloud communication platforms had already embedded AI functionality by 2025.

In 2025, over 70% of new cloud communication platforms deployed AI features including real-time transcription, sentiment analysis, and intelligent call routing. These capabilities have fundamentally changed how businesses manage internal operations and customer communications.

Market Size and Forecast

-

Market Size in 2026E: USD 19.41 Billion

-

Market Size by 2035: USD 116.4 Billion

-

CAGR: 22.03% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Cloud Communication Platform Market - Request Free Sample Report

Cloud Communication Platform Market Trends

-

AI-powered features including real-time transcription, automated meeting summaries, and intelligent call routing have become standard expectations rather than premium additions on enterprise cloud communication platforms globally.

-

CPaaS adoption is growing as developers embed communications into customer-facing applications, automating appointment reminders, payment confirmations, and support workflows without routing customers through separate channels.

-

Hybrid cloud deployment is growing in regulated industries that need cloud-scale flexibility for most workloads while retaining specific on-premise control over compliance-sensitive communication functions and data.

-

The permanent shift to remote and hybrid work has expanded the addressable market for cloud communication platforms well beyond large enterprises into mid-market and small business segments previously dependent on traditional phone systems.

-

Healthcare, financial services, and government sectors are adopting cloud communication platforms at accelerating rates as clinical, client advisory, and citizen service delivery benefits become operationally proven.

The U.S. Cloud Communication Platform Market Outlook

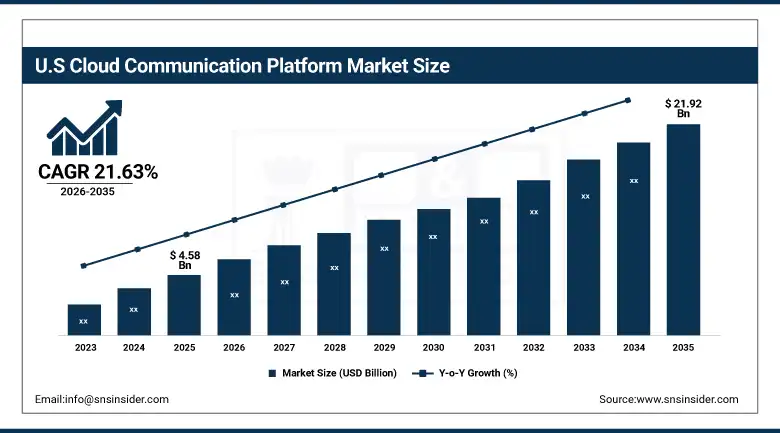

The U.S. Cloud Communication Platform Market was valued at approximately USD 4.58 Billion in 2025 and is expected to reach approximately USD 21.92 Billion by 2035, growing at a CAGR of 21.63%.

The United States is the biggest market for cloud communication platforms in terms of a country. Its dominance can be explained through the presence of the major technology platform providers in the world such as Twilio, RingCentral, Microsoft, Zoom, and Cisco. These companies produce some of the most popular cloud platforms in the world. American businesses pioneered the adoption of unified communications platforms. In addition, cloud-first policies within the federal government have resulted in huge platform adoptions in the government sector. Healthcare facilities invested in cloud communications to cope with telecommunication needs that became permanent due to the pandemic. Financial service providers are now using CPaaS in order to automate their customer communication across several million customer relationships at once. Another characteristic of the market in the U.S. is platform consolidation. Microsoft Teams and Zoom platforms have both increased their market share by absorbing competitors' market share from point solutions and standalone videoconferencing offerings. Independent CPaaS vendors such as Twilio, Vonage, and Bandwidth have gained market share by creating the underlying communication infrastructure used by developers.

Microsoft Teams crossed 320 million monthly active users in 2025, making it the single largest cloud communication platform by active user count and cementing Microsoft's position as the dominant enterprise unified communications vendor worldwide.

Cloud Communication Platform Market Segment Analysis

-

By Type, Unified Communication and Collaboration led the market with approximately 60.20% share in 2025; CPaaS is the fastest-growing type driven by API-based communications embedding across customer-facing applications and business workflows.

-

By Deployment Model, Public Cloud led with approximately 52.50% share in 2025; Hybrid Cloud is the fastest-growing deployment model at a CAGR of 12.80% as regulated industries balance cloud functionality with data control requirements.

-

By Application, IT & Telecom dominated with approximately 28.10% share in 2025; Healthcare is the fastest-growing application at a CAGR of 11.50%, driven by telehealth integration and patient engagement platform investments.

-

By Enterprise Size, Large Enterprises held the largest share in 2025; SMEs are growing faster as SaaS delivery makes enterprise-grade platforms accessible at affordable per-seat pricing.

By Type, unified communication and collaboration dominates, CPaaS grows fastest

The Unified Communication and Collaboration platforms accounted for about 60.20% of the cloud communication platform market in 2025. The reason for this high percentage is the almost ubiquitous implementation of unified cloud solutions instead of traditional communication infrastructure solutions at the enterprise level. UCC integrates voice calling, video conferencing, collaboration and teamwork, file exchange, and presence information all in one application. It can work on any device in any place. Microsoft Teams, Zoom, Cisco Webex, and Google Meet are some of the UCC companies that succeeded by resolving issues with existing technologies that the previous generation was unable to solve.

CPaaS is currently the fastest growing category of cloud communication platform market. CPaaS includes APIs that developers utilize to create voice, messaging, video functionalities, and other types of communication within their applications and business processes. Twilio, Vonage, Bandwidth, Sinch are the major providers in this space. CPaaS allows creating valuable communication experiences by building it right into your workflow. No need for customers to leave what they are doing now.

By Deployment Model, public cloud dominates, hybrid cloud grows fastest

Public cloud accounted for around 52.50% of revenues from deployment models in 2025. Commercial benefits offered by this model have been thoroughly studied. No upfront investments for hardware costs, automatic updates for software, pay-as-you-go billing structure that adjusts according to growing business, and access from any location or device. This list of attributes makes public cloud a top choice for most companies deploying cloud communication systems for the first time. Companies like Microsoft, Zoom, and RingCentral have fully embraced the technology based on public cloud.

Hybrid cloud represents the fastest growing deployment model with a compound annual growth rate of 12.80% up to 2033. Growth potential stems from regulation-heavy industries such as healthcare, financial services, and government bodies. Companies within these industries require scalability and power offered by cloud computing technology for the bulk of operations but keep on-premises control over certain kinds of data and functionalities. Healthcare providers dealing with HIPPA regulations, financial organizations with SEC rules for record keeping, and government bodies concerned with data sovereignty represent examples.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

76.4% |

|

Europe |

United Kingdom |

27.8% |

|

Asia Pacific |

China |

42.5% |

|

Middle East & Africa |

UAE |

28.6% |

|

Latin America |

Brazil |

41.3% |

North America Cloud Communication Platform Market Insights

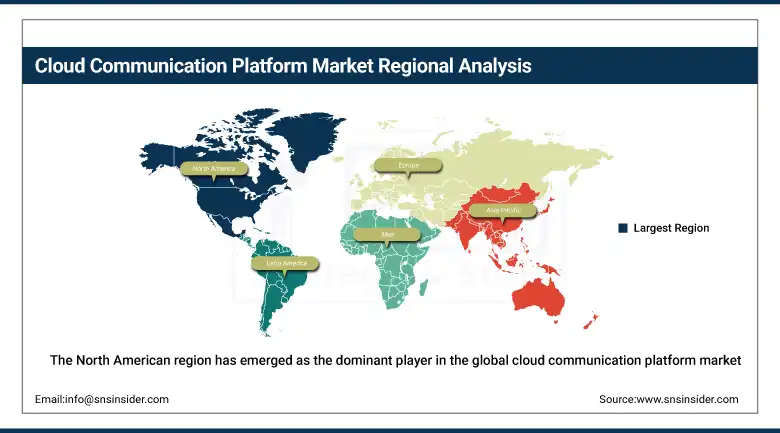

The North American region has emerged as the dominant player in the global cloud communication platform market for 2025. North America's dominance is attributed to the presence of the highest number of cloud communication platform vendors in the world, leading enterprise cloud adoption rates, and the highest level of CPaaS developer community engagement globally. U.S. companies have been amongst the earliest adopters of integrated cloud communication solutions to replace outdated PBX and email systems. This early adoption has enabled the creation of a sizeable user base of cloud platforms who contribute to the sustainability of the market through subscription spending. The Canadian market is rapidly developing as one of the leading markets for cloud communications in the region. The rapid adoption of cloud communication platforms by federal and provincial governments through government programmes and incentives has led to increased uptake in the public sector. Similar rates of adoption can be witnessed in the financial and healthcare sectors in Canada when compared to the U.S. Enterprise-grade security and data residency needs have influenced the purchase of platforms by organizations located in Canada.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cloud Communication Platform Market Insights

The European cloud communication platform market is a sizeable one, influenced by GDPR data residency regulations and high levels of enterprise unified communications deployments. The UK contributes about 27.8% of the revenue generated from the continent as its largest market for technology products. Microsoft Teams has an extremely high market penetration rate in European enterprises. There has been a lot of investment by vendors in European data centers due to GDPR. Germany, France, the Netherlands, and Scandinavia are notable countries within Europe that account for sizable national markets with high enterprise adoption rates. Procurement of cloud communication platforms has been heavily impacted by GDPR compliance within Europe. European customer data has to be stored in the EU under data residency laws. Companies which have set up cloud infrastructures in the EU have won big deals from large enterprises because of this reason. There has been rapid growth of the CPaaS market in Europe as digital companies such as retailers, financial institutions, and the healthcare industry incorporate communications into their customer journeys.

Asia Pacific Cloud Communication Platform Market Insights

Asia Pacific is the fastest-growing region for cloud communication platforms. China accounts for approximately 42.5% of Asia Pacific revenues. Alibaba Cloud, Tencent, and ByteDance operate the dominant domestic platforms within China. India, Japan, South Korea, and Southeast Asia represent some of the fastest-growing national markets globally. Digital transformation investment is accelerating the shift from legacy communication infrastructure across the region. Government digital economy programmes in Singapore, India, and South Korea are directly supporting enterprise cloud adoption at the national policy level.

MEA & Latin America Cloud Communication Platform Market Insights

The Middle East and Africa and Latin America are growing cloud communication markets where digital infrastructure investment and enterprise digitization are creating sustained demand. The UAE leads MEA revenues at approximately 28.6% of the regional share. Smart city investment in Dubai and Abu Dhabi has created a digitally advanced enterprise environment where cloud communication adoption is high among financial services, government, and hospitality sectors. Brazil leads Latin American revenues at approximately 41.3% through its large enterprise market and active fintech and digital retail sectors. CPaaS adoption is accelerating in both regions among companies automating customer communications.

Market Dynamics

Growth Drivers: Rising enterprise cloud adoption, AI integration into communication workflows, and the permanent shift to hybrid work are driving cloud communication platform market growth.

Cloud computing in the enterprise world is rapidly catching up. Enterprises that delayed their investments in cloud communication solutions are now dealing with costs associated with maintaining systems that were long since replaced by peers years ago. Shifting from on-premise PBX solutions to cloud solutions can be viewed not only as a means of releasing funds but also as an operational improvement. Enterprises are shifting funds from maintenance of hardware and IT staff to cloud subscriptions that offer greater functionality while costing less than the previous solution. Artificial Intelligence is creating new economic value in cloud communication systems. The ability to transcribe live meetings, extract action items, analyze sentiments, and trigger workflows automatically are commercially available today in 2025. All these functions create tangible productivity gains which justify premium-tiered subscription models. Enterprises selecting cloud communication solutions featuring superior AI capabilities have succeeded in closing large deals due to those capabilities.

Restraints: Data security concerns, regulatory compliance complexity, and network reliability dependency are the primary restraints on cloud communication platform market growth.

The greatest concern that keeps enterprises from using cloud communication is that of data security. The worries about possible data interception, hacking, and unauthorized use by the service providers are justified. There are many cases where such security breaches happened on cloud networks over the past decade. As a countermeasure, vendors now employ end-to-end encryption and zero-trust security architecture, and even offer private cloud versions of their products. Still, for the most security conscious enterprises, the risks are too high to use the technologies widely despite all measures taken. Certain compliance issues appear when deploying cloud solutions within some industries. HIPAA, GDPR, and regulations related to the recording of financial communication affect the deployment costs, because they must be considered in each case separately. In addition, smaller service providers often fail to deploy their solutions to regulated industries due to insufficient infrastructure.

Opportunities: CPaaS integration into AI-powered customer experience platforms and cloud adoption across emerging market enterprises represent the strongest cloud communication platform market growth opportunities.

CPaaS will drive the future growth of the cloud communication space. Communications functionality is being integrated into virtually all types of business software. The capability to place a voice call off of a CRM record, send an SMS from an ERP process flow, or enable video consultations on a healthcare app opens up an expansive, and ever-growing, market of programmable communication APIs. Every additional software product created by a company is another potential client for CPaaS with its own steady stream of API usage fees. Digitization in emerging market businesses provides a significant growth opportunity in the form of low-penetration rates. Companies operating in countries such as India, Southeast Asia, Africa, and Latin America are now deploying cloud communication solutions without having first to deploy a legacy PBX system, something that took decades for Western companies to overcome. This means that companies are adopting cloud systems with a clean slate of no technical debt at all.

Recent Developments:

-

2025: Twilio launched its Segment AI platform integrating customer data with real-time communication personalization, enabling enterprises to trigger context-aware voice, SMS, and email messages based on live behavioral signals.

-

2025: Microsoft introduced Copilot for Teams, embedding generative AI meeting summaries, action item extraction, and real-time translation into Teams calls across its 320 million monthly active user bases.

-

2025: RingCentral expanded its AI-powered contact center platform with real-time agent coaching, customer sentiment monitoring, and automated post-call summaries, strengthening its position in the enterprise contact center market.

Cloud Communication Platform Market Key Players are:

-

Twilio Inc.

-

RingCentral Inc.

-

Vonage (Ericsson)

-

Microsoft Corporation (Teams)

-

Zoom Video Communications Inc.

-

Cisco Systems Inc. (Webex)

-

8x8 Inc.

-

Bandwidth Inc.

-

Sinch AB

-

MessageBird (Bird)

-

Avaya Inc.

-

Mitel Networks Corporation

-

Genesys

-

Five9 Inc.

-

NICE Systems Ltd.

-

Infobip Ltd.

-

Plivo Inc.

-

Kaleyra Inc.

-

Telnyx LLC

-

Dialpad Inc.

Cloud Communication Platform Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.91 Billion |

| Market Size by 2035 | USD 116.4 Billion |

| CAGR | CAGR of 22.03% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Unified Communication and Collaboration (UCC), Communication Platform as a Service (CPaaS), Others) • By Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud) • By Application (IT & Telecom, BFSI, Healthcare, Retail, Education, Others) • By Enterprise Size (Large Enterprises, Small & Medium Enterprises) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Twilio Inc., RingCentral Inc., Vonage, Microsoft Corporation, Zoom Video Communications Inc., Cisco Systems Inc., 8x8 Inc., Bandwidth Inc., Sinch AB, MessageBird, Avaya Inc., Mitel Networks Corporation, Genesys, Five9 Inc., NICE Systems Ltd., Infobip Ltd., Plivo Inc., Kaleyra Inc., Telnyx LLC, Dialpad Inc.. |

Frequently Asked Questions

North America dominated the Cloud Communication Platform Market in 2025.

Unified Communication and Collaboration dominated with approximately 60.20% of revenues in 2025.

Rising enterprise cloud adoption and the permanent shift to hybrid and remote work are driving growth. AI integration into communication workflows has elevated platform value and expanded enterprise spending on premium tiers.

The Cloud Communication Platform Market was valued at USD 15.91 Billion in 2025.

The Cloud Communication Platform Market is expected to grow at a CAGR of 22.03% from 2026 to 2035.

Get in Touch