Cloud Discovery Market Report Scope & Overview:

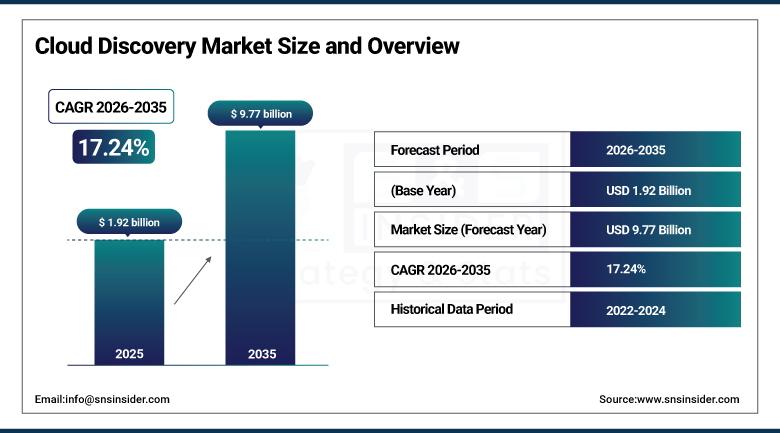

The Cloud Discovery Market was valued at USD 1.92 Billion in 2025 and is expected to reach USD 9.77 Billion by 2035, growing at a CAGR of 17.24% from 2026–2035.

The global cloud discovery market is experiencing rapid growth across key industry verticals including IT, BFSI, and healthcare due to rising demand for real-time cloud asset visibility and automated cloud infrastructure management. Cloud discovery solutions enable organizations to automatically identify, catalogue, and continuously monitor all cloud resources, services, and workloads deployed across public, private, and hybrid cloud environments, providing the visibility foundation for security, compliance, cost optimization, and operational governance. The market is driven by the increasing prevalence of shadow IT whose unmanaged cloud services create security risk that advanced discovery tools must address, the adoption of multi-cloud strategies creating complex asset management requirements, and regulatory compliance mandates requiring comprehensive cloud data inventory and access control documentation.

In November 2025, Amazon API Gateway rolled out its fully managed Developer Portal functionality, which allows companies to manage their APIs’ discoverability, access, documentation, analysis, and developer experience from a single integrated management plane. The enhancement reflects the commercial convergence of API management and cloud discovery whose combined capability enables organizations to simultaneously discover cloud resources and manage the API interfaces through which those resources communicate, creating integrated cloud governance value above standalone discovery or API management solutions.

Market Size and Forecast:

-

Market Size in 2026E: USD 2.25 Billion

-

Market Size by 2035: USD 9.77 Billion

-

CAGR: 17.24% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Cloud Discovery Market - Request Free Sample Report

Cloud Discovery Market Trends:

-

AI and machine learning technologies are enhancing cloud discovery platforms by enabling automated asset identification, anomaly detection, resource classification, and cloud cost optimization

-

Integration of Cloud Security Posture Management (CSPM) capabilities is creating unified platforms that combine asset discovery with continuous security and compliance monitoring

-

Multi-cloud discovery solutions are becoming essential as organizations seek centralized visibility and management across AWS, Azure, Google Cloud, and private cloud environments

-

Growing adoption of FinOps practices is driving demand for cloud discovery tools that provide detailed cost attribution, usage analytics, and resource optimization insights

-

Expansion of edge computing and IoT deployments is extending cloud discovery requirements beyond traditional cloud resources to include distributed edge infrastructure and connected devices

U.S. Cloud Discovery Market Outlook:

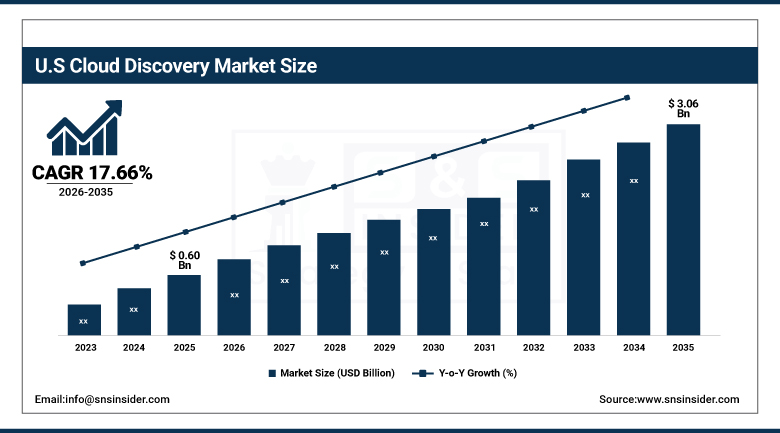

The U.S. Cloud Discovery Market was valued at approximately USD 0.60 Billion in 2025 and is expected to reach approximately USD 3.06 Billion by 2035, growing at a CAGR of approximately 17.66%.

The U.S. is the world's most commercially sophisticated cloud discovery market within North America's dominant revenue position. AWS CloudTrail, Microsoft Azure Arc, Google Cloud Asset Inventory, IBM Cloud Pak for Multi-cloud Management, and ServiceNow Cloud Management collectively define the domestic cloud discovery technology standard. The U.S. cloud market's multi-cloud adoption intensity, whose above-average deployment across AWS, Azure, and Google Cloud creates the world's most complex cloud asset management environment, drives above-average cloud discovery investment. Federal cloud security mandates including FedRAMP, FISMA, and the CISA Known Exploited Vulnerabilities catalogue create compliance-driven cloud discovery investment that sustains procurement independently of commercial ROI calculation.

In 2024, Microsoft expanded Azure Arc's cloud discovery capabilities to include automated inventory and configuration assessment for Kubernetes clusters deployed across on-premises, edge, and third-party cloud environments, extending cloud governance visibility to hybrid and multi-cloud Kubernetes workloads. The expansion reflects the commercial direction of cloud discovery toward unified hybrid infrastructure governance that encompasses cloud-native, containerized, and legacy on-premise workloads within single discovery and compliance assessment platforms.

Cloud Discovery Market Segment Analysis:

-

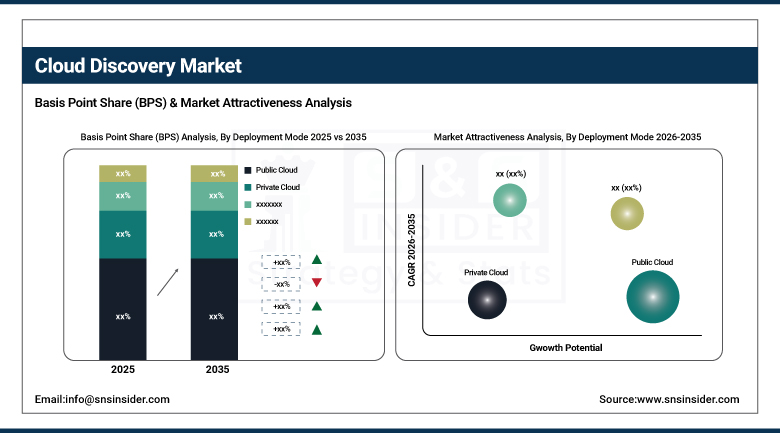

By Deployment Mode, the Public Cloud segment dominated the Cloud Discovery Market with approximately 58% share in 2025, while the Hybrid Cloud segment is the fastest growing.

-

By Organization Size, the Large Enterprises segment dominated the Cloud Discovery Market with approximately 62% share in 2025, while the Small & Medium Enterprises segment is the fastest growing.

-

By Application, the Security & Compliance segment dominated the Cloud Discovery Market with approximately 34% share in 2025, while the Cost Optimization segment is the fastest growing.

-

By Industry Vertical, the IT & Telecom segment dominated the Cloud Discovery Market with approximately 28% share in 2025, while the BFSI segment is the fastest growing.

By Deployment Mode, public cloud dominates, hybrid grows fastest

Public cloud deployment retained the dominant position with approximately 58% of the cloud discovery market in 2025. Cloud discovery solutions’ own deployment as cloud-native SaaS products creates a natural alignment with public cloud environments whose API-based resource enumeration enables agentless discovery across AWS, Azure, and Google Cloud without infrastructure installation complexity. Each organization that adopts public cloud infrastructure creates cloud discovery procurement whose automatic resource enumeration, continuous configuration monitoring, and compliance assessment capabilities deliver immediate security and governance value without additional infrastructure. The public cloud hyperscale’s’ native discovery tools including AWS CloudTrail, Azure Security Center, and Google Cloud Asset Inventory create the installed base foundation from which commercial discovery platform vendors differentiate through multi-cloud normalization, deeper compliance mapping, and financial management integration.

Hybrid cloud is the fastest-growing deployment type because enterprise cloud adoption increasingly spans on-premises infrastructure, private cloud, and multiple public cloud providers whose combined asset inventory creates discovery complexity that cloud-only tools cannot address. Each enterprise whose digital transformation involves both legacy on-premise workload continuation and greenfield cloud-native development creates hybrid discovery procurement whose unified visibility requirement sustains above-average platform complexity and commercial value. Microsoft Azure Arc's 2024 expansion to multi-cloud Kubernetes discovery demonstrates the commercial investment in hybrid-capable discovery capability that sustains the segment's fastest-growing status.

By Organization Size, large enterprises dominate, SMEs grow fastest

Large enterprises retained the dominant organization size position with approximately 62% of the cloud discovery market in 2025. Their complex multi-cloud deployments spanning multiple business units, regions, and cloud providers create asset inventory management challenges whose scale and compliance documentation requirements sustain above-average cloud discovery investment. Each large enterprise whose cloud estate encompasses thousands of compute instances, hundreds of managed services, and multiple cloud accounts creates discovery procurement whose per-organization commercial value substantially exceeds equivalent SME procurement. Regulatory compliance requirements that mandatorily apply at enterprise scale, including GDPR's data location documentation, SOX’s IT control audit requirements, and healthcare HIPAA cloud risk management, create non-discretionary discovery investment that sustains large enterprise market leadership.

SMEs are the fastest-growing organization size because the democratization of cloud discovery through SaaS pricing models accessible at hundreds rather than tens of thousands of dollars monthly creates first-time cloud discovery adoption among cloud-native SMEs whose entire infrastructure resides in public cloud. Each startup that reaches the organizational maturity level where cloud cost attribution, security misconfiguration monitoring, and compliance documentation become operational requirements creates cloud discovery procurement whose SaaS accessibility makes adoption feasible without enterprise-scale technology budgets.

By Application, security & compliance dominates, cost optimization grows fastest

Security and compliance retained the dominant application position with approximately 34% of the cloud discovery market in 2025. The commercial primacy of security and compliance discovery reflects the non-discretionary investment motivation that cloud misconfiguration risk, shadow IT proliferation, and regulatory audit requirements create for cloud asset visibility. Each cloud security incident whose root cause investigation reveals undetected misconfigured resources creates post-incident discovery investment motivation. The financial services, healthcare, and government sectors’ regulatory compliance documentation requirements create structured cloud discovery procurement whose compliance deadline and audit requirement motivation sustains investment through budget constraint cycles.

Cost optimization is the fastest-growing application because the extraordinary growth of cloud spending across all enterprise sectors is creating executive-level financial accountability motivation for granular resource utilization visibility and waste elimination. Each USD 1 million of cloud spending creates commercial motivation for discovery platform investment whose waste identification return on investment typically delivers multiple times the discovery platform cost through unused resource termination, right-sizing, and reserved instance optimization. The FinOps Foundation's growing enterprise membership and the CFO community's increasing scrutiny of cloud expenditure collectively sustain cost optimization discovery’s fastest-growing status.

By Industry Vertical, IT & Telecom dominates, BFSI grows fastest

IT and telecommunications retained the dominant industry vertical position with approximately 28% of the cloud discovery market in 2025. Technology companies’ above-average cloud adoption intensity, whose infrastructure-as-a-service and platform-as-a-service consumption substantially exceeds other industry verticals, creates the most commercially concentrated cloud discovery procurement. Each software company whose product infrastructure resides entirely in cloud creates cloud discovery procurement whose asset visibility, security assessment, and cost management requirements are fundamental operational capabilities rather than optional enhancement investments. Telecom operators’ progressive cloud-native network function migration creates above-average cloud asset management complexity whose discovery requirements sustain the vertical’s market leadership.

BFSI is the fastest-growing industry vertical because financial services regulatory requirements are creating the most structured compliance-driven cloud discovery procurement of any industry sector. Basel IV operational risk management requirements, PCI-DSS payment card data cloud storage documentation, SOX IT control audit evidence requirements, and the SEC's cloud risk disclosure mandate collectively create regulatory motivation for comprehensive cloud asset inventory and continuous compliance monitoring whose non-discretionary investment character sustains above-average discovery procurement growth through regulatory implementation cycles.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Cloud Discovery Market Insights

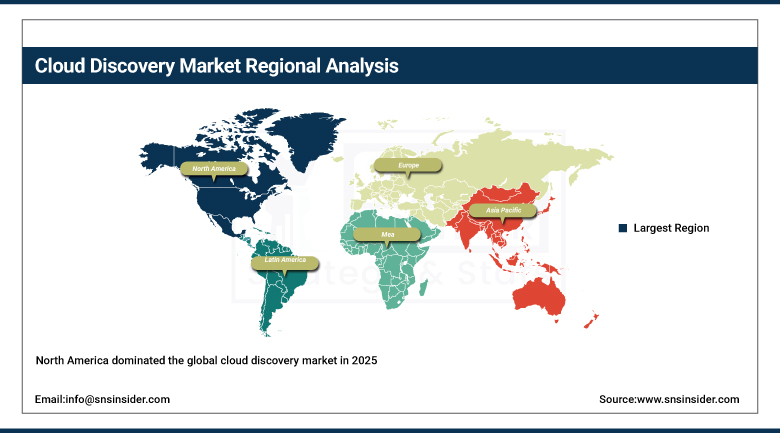

North America dominated the global cloud discovery market in 2025, driven by the high concentration of cloud service providers, robust digital infrastructure, and stringent data protection regulations that drive comprehensive cloud asset visibility adoption. The United States accounts for approximately 87.4% of North American revenues through AWS, Microsoft Azure, Google Cloud, IBM, ServiceNow, and Cisco's commercial cloud discovery operations.

Canada contributes approximately 12.6% of North American revenues through its financial services sector's cloud compliance investment, the government’s cloud security mandate, and the technology sector’s multi-cloud asset management procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cloud Discovery Market Insights

Europe is a compliance-driven cloud discovery market where GDPR's data location documentation requirement, NIS2's cybersecurity asset visibility mandate, and DORA's financial sector IT risk management framework create regulatory structured cloud discovery investment. Germany accounts for approximately 22.3% of European revenues through its financial services sector, the automotive and manufacturing industry's cloud transformation investment, and the BSI's cloud security standards creating compliance-driven discovery procurement.

The United Kingdom, France, and the Netherlands are significant secondary markets where financial services GDPR compliance, technology sector cloud adoption, and government cloud security initiatives create consistent discovery procurement. Microsoft Azure’s Dublin-based European operations and Amazon Web Services’ Frankfurt and Dublin regions create regional cloud infrastructure that sustains European cloud discovery market supply.

Asia Pacific Cloud Discovery Market Insights

Asia Pacific is the fastest-growing regional cloud discovery market, fueled by rapid cloud adoption in China, India, Japan, South Korea, and Southeast Asia where digital transformation investment, data localization regulations, and expanding cloud infrastructure create above-average discovery procurement growth. China accounts for approximately 44.8% of Asia Pacific revenues through its domestic cloud providers—Alibaba Cloud, Tencent Cloud, and Huawei Cloud—whose massive enterprise customer bases create cloud asset management requirements.

India represents the most commercially dynamic emerging market within Asia Pacific where the IT sector’s above-average cloud adoption, SEBI and RBI cloud compliance mandates for financial services, and the government’s digital transformation creating cloud asset management requirements drive above-average cloud discovery first-time adoption growth.

MEA & Latin America Cloud Discovery Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through Vision 2030’s cloud-first government infrastructure investment, SAMA’s cloud framework compliance requirements for financial services, and the technology sector’s cloud adoption creating structured discovery procurement. The UAE’s Dubai Internet City cloud ecosystem adds complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its financial services LGPD compliance investment, the growing technology sector’s cloud adoption, and BACEN’s cloud risk management regulation sustaining structured cloud discovery procurement across both markets through 2035.

Market Dynamics:

Growth Drivers: Multi-cloud adoption complexity and shadow IT security risk creating structured discovery investment

Multi-cloud strategy adoption is the cloud discovery market’s most commercially certain structural growth driver. Each organization that deploys workloads across multiple cloud providers creates exponentially more complex asset inventory management challenges whose visibility, security assessment, and cost attribution requirements sustain cloud discovery platform investment. The majority of large enterprises now operate across two or more public cloud providers whose separate management consoles, different API schemas, and distinct compliance documentation requirements create unified discovery platform demand whose commercial value grows with multi-cloud deployment complexity.

Shadow IT proliferation whose unmanaged cloud services create unmonitored security risk is reshaping security strategies and emphasizing the need for advanced discovery tools. Each employee who deploys unauthorized cloud services outside IT governance creates security risk whose detection and remediation requires cloud discovery capabilities that network perimeter security tools cannot provide. The shift to remote work accelerated shadow IT adoption whose security consequence creates structured enterprise cloud discovery investment in CASB and cloud discovery platform procurement.

Restraints: Integration complexity with diverse cloud environments and data privacy concerns

Integration complexity with diverse cloud provider APIs, legacy on-premise systems, and proprietary private cloud platforms creates implementation barriers for cloud discovery deployments whose multi-environment coverage requires extensive connector development and maintenance. Each new cloud provider API version and each infrastructure-as-code deployment methodology creates discovery platform maintenance investment whose cost scales with environment diversity.

Data privacy concerns arise when cloud discovery platforms collect and centralize sensitive cloud configuration and workload data whose aggregation creates new security risk if the discovery platform itself is compromised. Each discovery platform that ingests cloud environment credentials, resource configurations, and network topology creates a high-value attack target whose security assurance requirement moderates adoption pace in security-conscious environments.

Opportunities: FinOps integration and AI-powered autonomous cloud governance

FinOps integration with cloud discovery creates the most commercially accessible near-term market expansion opportunity whose financial accountability motivation sustains adoption investment independent of security and compliance procurement drivers. Each organization whose cloud spending exceeds budget creates FinOps programme investment whose cloud discovery integration enables granular cost attribution, utilization analysis, and waste elimination recommendations that deliver measurable ROI.

AI-powered autonomous cloud governance whose anomaly detection, automated remediation, and predictive optimization capability reduces the human expertise requirement for continuous cloud management creates the most commercially premium product differentiation opportunity for cloud discovery platform vendors whose AI capability creates measurable operational value that sustains premium subscription pricing above conventional inventory-only alternatives.

Recent Developments:

-

2025: Amazon API Gateway launched fully managed Developer Portal functionality in November 2025, enabling companies to manage API discoverability, access, documentation, and developer experience from a single integrated cloud management plane combining API governance and cloud asset discovery.

-

2024: Microsoft expanded Azure Arc’s cloud discovery capabilities in 2024 to include automated inventory and configuration assessment for Kubernetes clusters across on-premises, edge, and third-party cloud environments, extending hybrid cloud governance visibility.

-

2024: Google Cloud enhanced its Cloud Asset Inventory service in 2024 with real-time asset change notification and policy compliance monitoring integration, enabling organizations to detect unauthorized cloud resource creation and configuration drift within seconds of occurrence.

-

2024: ServiceNow launched enhanced cloud discovery modules within its IT Operations Management (ITOM) platform in 2024, providing automated multi-cloud asset discovery integrated with CMDB, incident management, and governance workflows for enterprise IT operations.

-

2023: IBM expanded Cloud Pak for Multicloud Management in 2023 with enhanced AI-powered cloud resource classification and cost optimization recommendations, enabling enterprises to automatically identify underutilized resources and rightsizing opportunities across hybrid multi-cloud deployments.

Cloud Discovery Market Key Players:

-

Amazon Web Services Inc. (AWS CloudTrail)

-

Microsoft Corporation

-

Google LLC

-

IBM Corporation

-

Cisco Systems Inc.

-

VMware Inc.

-

ServiceNow Inc.

-

Oracle Corporation

-

Qualys Inc.

-

Orca Security Ltd.

-

Wiz Inc.

-

Lacework Inc.

-

Prisma Cloud

-

Ermetic Ltd.

-

Sysdig Inc.

-

Cloudability

-

CloudHealth by VMware

-

Flexera Software LLC

-

Zscaler Inc.

-

Axonius Inc.

Cloud Discovery Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.92 Billion |

| Market Size by 2035 | USD 9.77 Billion |

| CAGR | CAGR of 17.24% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud) • by Component (Software, Services) • by Organization Size (Large Enterprises, Small & Medium Enterprises) • by Application (Security & Compliance, Cost Optimization, Performance Monitoring, Asset Management, Shadow IT Detection, Others) • by Industry Vertical (IT & Telecom, BFSI, Healthcare, Retail & E-commerce, Manufacturing, Government & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Amazon Web Services Inc., Microsoft Corporation, Google LLC, IBM Corporation, Cisco Systems Inc., VMware Inc., ServiceNow Inc., Oracle Corporation, Qualys Inc., Orca Security Ltd., Wiz Inc., Lacework Inc., Prisma Cloud, Ermetic Ltd., Sysdig Inc., Cloudability, CloudHealth by VMware, Flexera Software LLC, Zscaler Inc., Axonius Inc. |

Frequently Asked Questions

The Cloud Discovery Market is expected to grow at a CAGR of 17.24% from 2026 to 2035.

The Cloud Discovery Market was valued at USD 1.92 Billion in 2025.

Multi-cloud strategy adoption creating complex asset inventory management requirements across multiple cloud providers, and the increasing prevalence of shadow IT whose unmanaged cloud services create security risk that advanced automated discovery tools must identify and remediate continuously.

Security & Compliance dominated the Cloud Discovery Market with approximately 34% share in 2025, while Cost Optimization is the fastest growing segment.

North America dominated the Cloud Discovery Market in 2025 due to the high concentration of cloud service providers and robust digital infrastructure, while Asia Pacific is the fastest-growing region.

Get in Touch