Cloud Native Applications Market Report Scope & Overview:

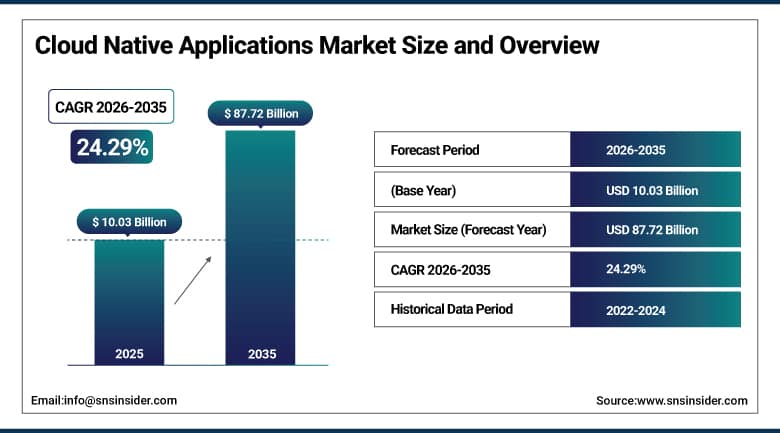

The Cloud Native Applications Market was valued at USD 10.03 Billion in 2025 and is expected to reach USD 87.72 Billion by 2035, growing at a CAGR of 24.29% from 2026 to 2035.

The global cloud native applications market is experiencing exceptional growth driven by enterprises’ systematic shift from monolithic legacy application architectures to microservices-based, containerised, and serverless application development paradigms that fully leverage the scalability, resilience, and operational efficiency of cloud computing infrastructure. Cloud native applications are purpose-built to run on cloud platforms, exploiting distributed computing resources through container orchestration, continuous integration and delivery pipelines, DevOps practices, and infrastructure as code methodologies that enable organisations to release software updates faster, scale resources elastically, and achieve higher availability than traditional on-premise application deployment permits. The market is driven by accelerating digital transformation investment, the proliferation of microservices architecture enabled by container platforms including Docker and Kubernetes.

In 2024, Google Cloud announced significant enhancements to its Kubernetes Engine and Cloud Run serverless platform, expanding automatic scaling capabilities, improving cold start latency for serverless workloads, and introducing Gemini AI-assisted application performance optimisation that enables cloud native application developers to identify and resolve performance bottlenecks through natural language queries rather than manual metric analysis. These enhancements directly address the operational monitoring and performance management requirements that sustain cloud native platform adoption among enterprise development teams transitioning from traditional application lifecycle management practices.

Market Size and Forecast:

-

Market Size in 2026E: USD 12.47 Billion

-

Market Size by 2035: USD 87.72 Billion

-

CAGR: 24.29% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Cloud Native Applications Market - Request Free Sample Report

Cloud Native Applications Market Trends:

-

Serverless computing is accelerating cloud-native application development by simplifying infrastructure management and enabling scalable, event-driven deployments.

-

GitOps adoption is streamlining cloud-native deployments through automated, declarative infrastructure management and continuous delivery pipelines.

-

eBPF-powered observability and security are enhancing real-time monitoring and threat detection for containerized cloud-native workloads.

-

Platform engineering is enabling self-service developer platforms that simplify Kubernetes and cloud infrastructure management.

-

Multi-cloud cloud-native strategies are gaining traction as enterprises leverage Kubernetes and cloud-agnostic architectures to improve workload portability and avoid vendor lock-in.

U.S. Cloud Native Applications Market Outlook

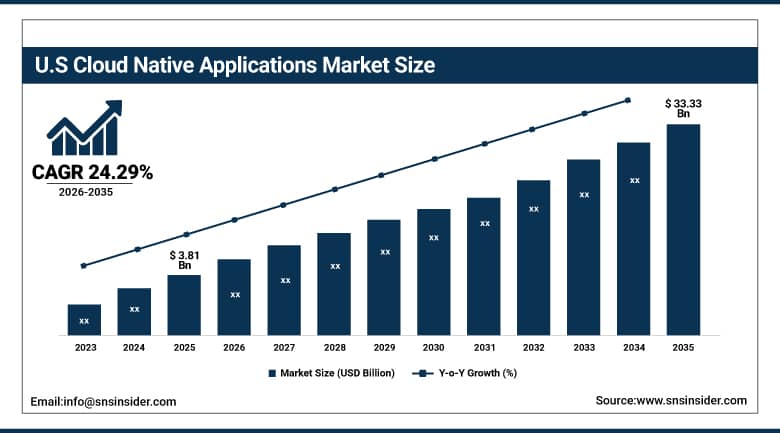

The U.S. Cloud Native Applications Market was valued at approximately USD 3.81 Billion in 2025 and is expected to reach approximately USD 33.33 Billion by 2035, growing at a CAGR of approximately 24.29%.

In the North American region, the United States stands out to be the most commercially impactful market for cloud native application usage in the world. Cloud native platforms' commercial landscape is defined by the offerings of Amazon Web Services, Google Cloud, Microsoft Azure, Red Hat, IBM, and VMware with their management of Kubernetes, serverless, and containers. 80 percent adoption by the technology industry, 65 percent by the financial services industry, and 55 percent by the healthcare industry highlight the tremendous adoption of cloud native technology architecture in the development of enterprise applications in the United States. Netflix, Uber, Airbnb, and Lyft have provided examples of cloud native architecture adoption which support future adoption of cloud native technology.

In 2023, Amazon Web Services launched AWS Application Composer, a visual development tool enabling developers to design and build cloud native serverless applications through a drag-and-drop interface that automatically generates AWS CloudFormation infrastructure-as-code templates, reducing the expertise barrier to cloud native serverless application development. This product launch demonstrates the commercial direction of cloud native platform development toward developer experience improvement that expands the addressable developer population capable of building production-grade cloud native applications.

Cloud Native Applications Market Segment Analysis:

-

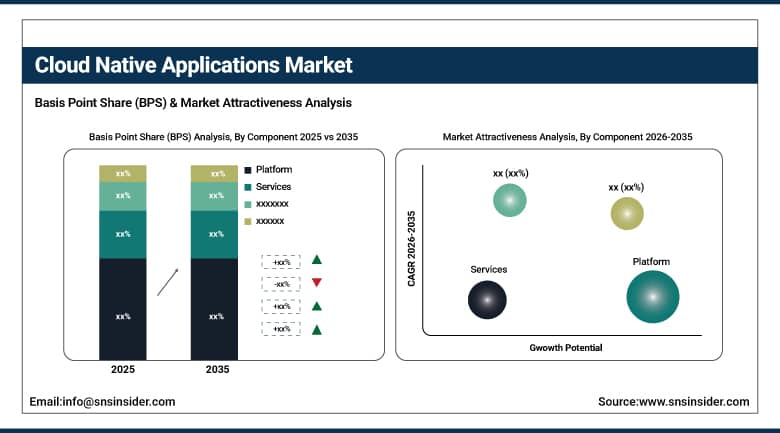

By Component, the platform segment dominated the cloud native applications market with approximately 58% share in 2025, while the services segment is the fastest growing at approximately 25.89% CAGR.

-

By Deployment Mode, the public cloud segment dominated the cloud native applications market with approximately 52% share in 2025, while the hybrid cloud segment is the fastest growing at approximately 26.37% CAGR.

-

By Enterprise Size, the large enterprises segment dominated the cloud native applications market with approximately 67% share in 2025, while the SME segment is the fastest growing at approximately 25.98% CAGR.

-

By End User, the BFSI segment dominated the cloud native applications market with approximately 26% share in 2025, while the retail and e-commerce segment is the fastest growing.

By Component, platform dominates, services grow fastest

The platform segment retained the dominant component position with approximately 58% of the cloud native applications market in 2025. Cloud native platform commercial primacy reflects the foundational role of platform infrastructure in enabling every cloud native application development capability. Container orchestration platforms led by Kubernetes and its managed derivatives on AWS EKS, Google GKE, and Azure AKS, continuous integration and delivery platforms including GitHub Actions, GitLab CI, and CircleCI, service mesh platforms including Istio and Linkerd, and API gateway platforms including Kong, AWS API Gateway, and Azure API Management collectively constitute the platform investment that precedes and enables all cloud native application development. Red Hat OpenShift's enterprise Kubernetes platform, whose commercial subscription provides the compliance, security, and support guarantees that enterprise adoption requires.

Services are the fastest growing component because the complexity of cloud native architecture adoption creates consulting, implementation, and managed services demand that companies cannot fully self-serve even with strong internal technology capability. Each enterprise digital transformation programme that adopts cloud native architecture creates cloud native consulting engagement whose scope encompasses architecture design, team training, tooling selection, and migration planning. The global shortage of Kubernetes certified administrators and cloud native development expertise sustains demand for managed services that operate cloud native infrastructure on behalf of enterprises whose internal talent gap prevents self-managed deployment.

By Deployment Mode, public cloud dominates, hybrid cloud grows fastest

Public cloud retained the dominant deployment position with approximately 52% of the cloud native applications market in 2025. Public cloud's dominance as the preferred deployment for cloud native applications reflects the native availability of managed container orchestration, serverless compute, container registries, and CI/CD tooling from AWS, Google Cloud, and Microsoft Azure that eliminates the infrastructure management burden that self-managed private cloud deployment creates. The pay-as-you-go pricing model's capital expenditure elimination advantage, the managed platform's automatic update and security patching, and the elastic scaling capability whose instant resource provision responds to traffic demand variation collectively sustain public cloud specification preference for new cloud native application workloads across startup and enterprise development organisations.

Hybrid cloud is the fastest growing deployment model because enterprise data residency requirements, regulatory compliance obligations for sensitive financial and healthcare data, and the need to modernise existing private cloud workloads alongside new cloud native public cloud deployments create a structured hybrid architecture requirement. Each financial institution whose customer data sovereignty regulation prevents public cloud storage creates hybrid cloud native architecture procurement whose private cloud component sustains hybrid deployment model growth. The Kubernetes portability advantage, whose consistent container orchestration API across public and private cloud enables workload migration between environments, sustains hybrid cloud native adoption as the architecture for compliance-constrained enterprise workloads.

By End User, BFSI dominates, retail and e-commerce grows fastest

BFSI retained the dominant end-user position with approximately 26% of the cloud native applications market in 2025. The financial services industry's combination of high application performance requirements, real-time transaction processing scale, stringent availability mandates, and the competitive pressure from fintech disruptors creates the most commercially intensive cloud native application investment of any industry vertical. Each digital banking platform, real-time payments processing system, fraud detection engine, and risk management application that financial institutions develop as cloud native microservices creates platform and services procurement whose per-application commercial value substantially exceeds equivalent applications in less performance-critical industry verticals. Goldman Sachs’ internal developer platform, JPMorgan's microservices architecture investment, and fintech platforms’ Kubernetes-native architecture collectively demonstrate the commercial depth of BFSI cloud native application adoption.

Retail and e-commerce is the fastest growing end user because digital commerce acceleration, the extreme traffic variability of promotional events including Black Friday and Cyber Monday, and the rapid development of AI-powered personalisation and recommendation features create above-average cloud native application adoption. Each e-commerce platform that adopts microservices architecture to enable independent scaling of product catalogue, checkout, recommendations, and inventory services creates cloud native procurement whose architecture complexity sustains ongoing platform and services investment. The retail sector's requirement for 99.99% availability during peak trading periods creates the strongest commercial case for cloud native auto-scaling and fault tolerance architecture of any consumer-facing industry application.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Cloud Native Applications Market Insights

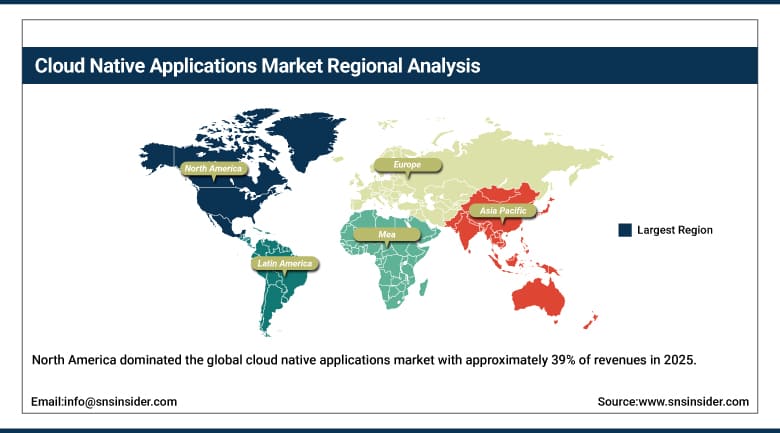

North America dominated the global cloud native applications market with approximately 39% of revenues in 2025, driven by early adoption of advanced cloud technologies, the strong presence of key cloud service providers including AWS, Microsoft Azure, and Google Cloud, and mature infrastructure across large enterprises seeking scalable and efficient application development solutions. The United States accounts for approximately 87.4% of North American revenues through these commercial platform operations combined with Red Hat, IBM, and VMware's enterprise cloud native software commercial relationships.

Canada contributes approximately 12.6% of North American revenues through its technology sector's cloud native adoption, the financial services industry's digital banking platform development, and the government's digital services modernisation investment that creates public sector cloud native application procurement.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Cloud Native Applications Market Insights

Europe is a technically sophisticated cloud native applications market where the EU Digital Strategy's cloud adoption targets, GDPR's data sovereignty requirements driving hybrid cloud native adoption, and the technology sector's strong cloud native engineering community create consistent institutional demand. Germany accounts for approximately 22.3% of European revenues through SAP's cloud native platform development, Deutsche Telekom's cloud native network infrastructure, and the manufacturing sector's industrial application modernisation investment.

The United Kingdom, the Netherlands, and France are significant secondary markets where the fintech industry's cloud native platform adoption, ASML's cloud native engineering investment, and BNP Paribas’ digital banking cloud native development create consistent procurement. Red Hat's European operations and VMware's Tanzu platform sustain regional supply.

Asia Pacific Cloud Native Applications Market Insights

Asia Pacific is the fastest growing regional cloud native applications market, driven by China's extraordinary technology sector investment, India's IT services industry's cloud native practice development, Japan's enterprise digital transformation, South Korea's Samsung and SK Telecom cloud native programmes, and Southeast Asia's rapidly expanding digital economy. China accounts for approximately 44.8% of Asia Pacific revenues through Alibaba Cloud's Kubernetes platform, Tencent Cloud's cloud native application services, and the Chinese technology sector's above-average cloud native adoption driven by hyperscale internet application requirements.

India represents the most commercially dynamic emerging market within Asia Pacific where the IT services industry's cloud native skill development and client delivery, the startup ecosystem's cloud native architecture adoption, and the enterprise digital transformation wave create above-average cloud native application market growth from both domestic and export service delivery perspectives.

MEA & Latin America Cloud Native Applications Market Insights

The UAE leads MEA revenues at approximately 31.2% through Abu Dhabi's cloud infrastructure investment, ADNOC's digital transformation programme, and the fintech sector's cloud native platform adoption. Saudi Arabia's Vision 2030 digital economy initiatives add substantial complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its fintech ecosystem's cloud native adoption, the e-commerce sector's scalable platform investment, and the technology sector's cloud migration. Mexico's enterprise IT modernisation and Colombia's digital startup ecosystem collectively sustain regional growth through 2035.

Market Dynamics:

Growth Drivers: Enterprise digital transformation mandating cloud native architecture and DevOps practice adoption accelerating application delivery velocity

Enterprise digital transformation investment is the cloud native applications market's most commercially pervasive structural growth driver. Each enterprise that initiates a digital transformation programme that requires faster application delivery, greater deployment frequency, and improved application reliability creates cloud native architecture adoption whose platform and services procurement compounds with the breadth of application portfolio being modernized. The competitive pressure from digital-native disruptors in financial services, retail, healthcare, and media whose cloud native architecture enables faster product iteration creates transformation urgency among incumbent enterprises whose legacy application architectures cannot match the development velocity advantage.

DevOps practice adoption, which accelerates application delivery by breaking down development and operations team silos through shared responsibility and automated CI/CD pipeline deployment, creates cloud native application market growth by increasing the frequency of application updates and the developer population capable of deploying containerized microservices. Each organization that adopts DevOps practices creates demand for the container orchestration, CI/CD tooling, and observability platforms that constitute the cloud native application development and operations stack.

Restraints: Kubernetes operational complexity and security skill gap limiting SME adoption pace

Kubernetes operational complexity creates adoption barriers for organizations without dedicated platform engineering teams whose deep knowledge of container orchestration, networking, storage, and security configuration is required to operate production-grade Kubernetes environments reliably. Each organization whose application development team encounters Kubernetes cluster management complexity without access to a dedicated platform engineering team creates adoption friction that delays or limits the scope of cloud native migration, sustaining demand for managed Kubernetes services that abstract operational complexity at subscription cost.

The cloud native security skill gap creates vulnerability exposure in organizations whose adoption of container orchestration and microservices architecture outpaces their security team's capability to implement cloud native security controls including container image scanning, Kubernetes RBAC policy, network policy enforcement, and runtime anomaly detection. Each cloud native application deployment without adequate security controls creates organizational risk whose consequences sustain demand for cloud native security platforms and managed security services.

Opportunities: AI-native application development and edge cloud native deployment

AI-native application development represents the most commercially transformative near-term cloud native application market opportunity whose integration of large language model APIs, vector databases, and AI inference infrastructure into cloud native application architectures creates new application categories and expanded cloud platform consumption. Each enterprise that builds AI-powered customer service, code assistant, content generation, or data analysis application as a cloud native microservice creates cloud native platform procurement whose AI API consumption and inference compute usage creates above-average per-application cloud spend relative to conventional application workloads.

Edge cloud native deployment represents the most commercially expansive geographic opportunity whose extension of cloud native application deployment to edge computing nodes at telecommunications provider facilities, retail locations, and manufacturing plants creates cloud native platform procurement beyond centralized data centre perimeters. Each 5G edge computing deployment that hosts latency-sensitive cloud native applications including real-time analytics, AR/VR streaming, and autonomous system control creates edge cloud native platform procurement whose commercial aggregate compounds with the extraordinary scale of global 5G infrastructure deployment.

Recent Developments:

-

2024: Google Cloud announced significant enhancements to Kubernetes Engine and Cloud Run in 2024, expanding automatic scaling capabilities and introducing Gemini AI-assisted application performance optimization for cloud native application developers.

-

2024: Red Hat launched OpenShift AI in 2024, an integrated cloud native platform for building, training, and deploying AI and machine learning models within Kubernetes environments, enabling enterprises to develop AI-powered cloud native applications using the same container orchestration and CI/CD pipelines as conventional microservices.

-

2023: Amazon Web Services launched AWS Application Composer in 2023, a visual development tool enabling developers to design and build cloud native serverless applications through drag-and-drop interface that automatically generates AWS CloudFormation infrastructure-as-code templates.

Cloud Native Applications Market Key Players are:

-

Amazon Web Services Inc. (AWS)

-

Microsoft Corporation (Azure)

-

Google LLC (Google Cloud)

-

Red Hat Inc. (IBM)

-

VMware Inc. (Broadcom)

-

IBM Corporation

-

Oracle Corporation

-

SAP SE

-

Infosys Limited

-

Cognizant Technology Solutions

-

Alibaba Cloud (Alibaba Group)

-

Tencent Cloud

-

Pivotal Software Inc.

-

HashiCorp Inc.

-

Datadog Inc.

-

Dynatrace Inc.

-

New Relic Inc.

-

Sysdig Inc.

-

Rancher Labs (SUSE)

-

Portworx Inc. (Pure Storage)

Cloud Native Applications Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.03 Billion |

| Market Size by 2035 | USD 87.72 Billion |

| CAGR | CAGR of 24.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Platform, Services) • By Deployment Mode (Public Cloud, Private Cloud, Hybrid Cloud) • By Enterprise Size (Large Enterprises, Small and Medium-sized Enterprises) • By End User (BFSI, IT and Telecom, Retail and E-commerce, Healthcare, Government, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amazon Web Services Inc. (AWS), Microsoft Corporation (Azure), Google LLC (Google Cloud), Red Hat Inc. (IBM), VMware Inc. (Broadcom), IBM Corporation, Oracle Corporation, SAP SE, Infosys Limited, Cognizant Technology Solutions, Alibaba Cloud (Alibaba Group), Tencent Cloud, Pivotal Software Inc., HashiCorp Inc., Datadog Inc., Dynatrace Inc., New Relic Inc., Sysdig Inc., Rancher Labs (SUSE), and Portworx Inc. (Pure Storage) |

Frequently Asked Questions

The Cloud Native Applications Market is expected to grow at a CAGR of 24.29% from 2026 to 2035.

The Cloud Native Applications Market was valued at USD 10.03 Billion in 2025.

Enterprise digital transformation investment mandating cloud native microservices architecture for faster application delivery and greater scalability, and DevOps practice adoption accelerating CI/CD pipeline deployment that creates demand for container orchestration, service mesh, and cloud native observability platform procurement.

Platform dominated the Cloud Native Applications Market with approximately 58% share in 2025.

North America dominated the Cloud Native Applications Market with approximately 39% of revenues in 2025.

Get in Touch