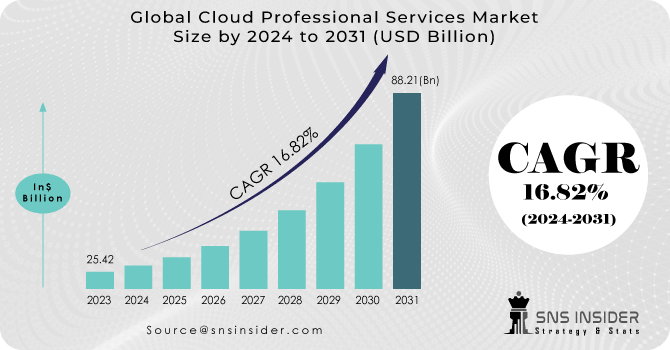

Cloud Professional services Market size was valued at USD 25.42 Bn in 2023 and is expected to reach USD 88.21 Bn by 2031 and grow at a CAGR of 16.82 % over the forecast period 2024-2031.

Cloud professional services assist businesses in creating sophisticated cloud solutions across private cloud, public, and hybrid cloud models, improving operational efficiency, flexibility, and infrastructure scalability. Vendors offer various services such as application modernization, custom development, consulting, integration, migration, and support to enhance existing cloud systems. These services cut implementation costs and deliver comprehensive solutions that greatly benefit business and technical operations in enterprises.

Get More Information on Cloud Professionl Services Market - Request Sample Report

The surge in public cloud adoption drives market growth, boosting demand for cloud professional services due to the widespread popularity of cloud computing. This trend encourages businesses of all sizes and industries to embrace diverse cloud services. As more providers enter the market, the demand for professional cloud services rises, benefiting companies of all scales and fueling market expansion.

Market Dynamics

Drivers:

Increasing adoption of digital transformation strategies by businesses is driving the demand for cloud professional services.

Cloud services offer cost-effective solutions compared to traditional IT infrastructure, encouraging businesses to adopt cloud-based professional services for improved cost management.

Cloud platforms provide scalability and flexibility, allowing businesses to scale resources as per demand, leading to a higher demand for professional services.

Outsourcing cloud management and maintenance allows organizations to focus on their core competencies, driving the need for professional services.

The rising adoption of digital transformation strategies among businesses is aimed at modernizing operations and maintaining competitiveness. This surge is driving the need for cloud professional services, as companies look for specialized assistance in migrating, managing, and optimizing their cloud infrastructures to effectively support their digital initiatives.

Restraints:

Integrating legacy systems with cloud environments can be complex and costly, acting as a restraint for businesses considering cloud adoption.

The shortage of skilled professionals in cloud technologies can hinder the growth of the cloud professional services market, leading to talent acquisition challenges.

Concerns about vendor lock-in and dependency on specific cloud service providers may deter some businesses from fully embracing cloud professional services.

The cloud professional services market faces challenges due to a scarcity of skilled professionals in cloud technologies, which can impede its growth trajectory. This shortage results in difficulties in acquiring the necessary talent, leading to potential delays in service delivery and project execution. Moreover, the competitive landscape intensifies as companies vie for experienced cloud experts, further exacerbating talent acquisition challenges. Consequently, addressing this skill gap becomes paramount for sustained growth and success within the cloud professional services sector.

Opportunities:

The integration of AI and machine learning technologies into cloud services presents opportunities.

The increasing adoption of hybrid and multi-cloud strategies creates opportunities for professional service providers to offer consulting, integration, and management services across diverse cloud environments.

Developing industry-specific cloud solutions and services tailored to sectors like healthcare, finance, and manufacturing can unlock new opportunities for cloud professional services providers.

The rise of edge computing presents opportunities for professional service providers to offer edge-to-cloud integration, management, and optimization services.

Challenges:

Ensuring robust security measures and compliance with evolving regulations poses a significant challenge for cloud professional services providers.

Managing complex cloud environments, especially in hybrid and multi-cloud setups, requires advanced skills and technologies, posing operational challenges.

Balancing cost-effectiveness while delivering high-quality cloud services can be challenging for providers, especially with pricing pressures and competition.

Addressing data governance issues, data sovereignty concerns, and ensuring data integrity across cloud environments present ongoing challenges for providers and their clients.

Impact of Russia-Ukraine War:

The cloud professional services market has been notably affected by the Russia-Ukraine war, primarily due to geopolitical and economic uncertainties. This conflict has heightened global market volatility, impacting investor confidence and overall business outlooks. Consequently, companies may postpone or review their cloud adoption and digital transformation strategies, resulting in a potential slowdown in the demand for cloud professional services. Moreover, disruptions in supply chains and heightened cybersecurity concerns arising from the conflict can further complicate the landscape for cloud services providers, necessitating adaptive strategies to navigate these challenging conditions effectively.

Impact of Economic Downturn:

An economic downturn can significantly impact the cloud professional services market. It may cause businesses to reduce IT spending, leading to decreased demand for cloud services and consultancy as they prioritize cost-saving measures. Furthermore, uncertainties and financial constraints can prompt companies to postpone or scale down digital transformation projects, affecting cloud service demand. Intensified competition among providers may also emerge, but amidst challenges, opportunities arise as companies seek cost-efficient solutions to navigate economic hardships.

Market segmentation

By Service Type

Consulting

Application Development and Modernization

Implementation and Migration

Integration and Optimization

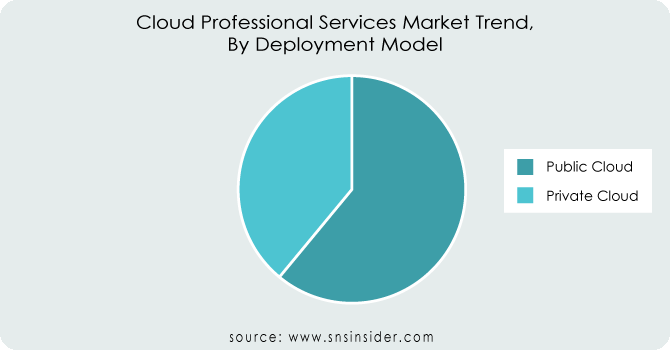

By Deployment Model

Public Cloud

Private Cloud

On the Basis of the Deployment Model, the public cloud segment dominates the market holding a revenue share of More than 62%. It encompasses computing services provided by third-party vendors via the public internet, accessible to all users. This model offers a range of resources like applications, storage, and virtual servers over the internet, ensuring scalability, pay-as-you-go pricing, and simple deployment for enterprises.

Get Customized Report as per Your Business Requirement - Request For Customized Report

By organization size

Small and Medium-sized Enterprises

Large Enterprises

By verticals

BFSI

Manufacturing

Healthcare and Lifesciences

IT and ITES

Government

Telecommunications

Retail and Consumer Goods

Energy and utilities

Others

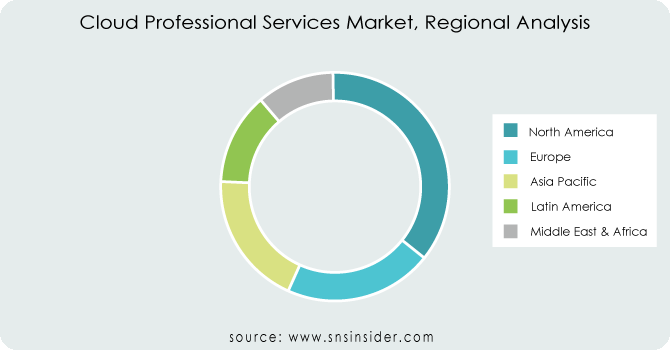

Regional Analysis

North America region dominates the market with holding Revenue share of more than 39%, the US and Canada, are leading the Cloud Professional Services market, boasting advanced technology infrastructure and a competitive landscape with numerous solution providers. The region's connectivity and innovation enable top-quality services, making it an early adopter of 5G technology. APAC region is the second-largest market contributor, with India, Japan, China, and Australia leading in AI, IoT, analytics, and cloud computing, driving demand for cloud professional services. Conversely, the Middle East and Africa market is forecasted for growth.

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Key Players

The major key players are Alibaba group holding limited, Amazon web services, Inc., Cisco Systems, Inc., Dell, technologies Inc., Google LLC, Hewlett Packard enterprise development lp, international business machines corporation, Microsoft Corporation, Oracle Corporation, Rackspace Hosting, Inc. and other key players mentioned in the final report.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 25.42 Billion |

| Market Size by 2031 | US$ 88.21 Billion |

| CAGR | CAGR 16.82 % From 2024 to 2031 |

| Base Year | 2022 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2021 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Consulting, Application Development, and Modernization, Implementation and Migration, Integration and Optimization) • By Deployment Model (Public Cloud and Private Cloud) • By Organization Size (Small And Medium-Sized Enterprises And Large Enterprises) • By Verticals (BFSI, Manufacturing, Healthcare and Lifesciences, IT And ITES, Government, Telecommunications, Retail And Consumer Goods, Energy And Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Alibaba group holding limited, Amazon web services, Inc., Cisco Systems, Inc., Dell, technologies Inc., Google LLC, Hewlett Packard enterprise development lp, international business machines corporation, Microsoft Corporation, Oracle Corporation, Rackspace Hosting, Inc. |

| Key Drivers | • Increasing adoption of digital transformation strategies by businesses is driving the demand for cloud professional services.

• Cloud services offer cost-effective solutions compared to traditional IT infrastructure, encouraging businesses to adopt cloud-based professional services for improved cost management. |

| Market Restraints | • Integrating legacy systems with cloud environments can be complex and costly, acting as a restraint for businesses considering cloud adoption. • The shortage of skilled professionals in cloud technologies can hinder the growth of the cloud professional services market, leading to talent acquisition challenges. |

Ans. The Compound Annual Growth rate for the Cloud Professional Services Market over the forecast period is 16.82 %.

Ans. The projected market size for the Cloud Professional Services Market is USD 88.21 Bn by 2031.

Ans: The Public Cloud Deployment Model segment dominated the Cloud Professional services Market with the highest revenue share.

Ans: The major key players are Alibaba Group Holding Limited, Amazon Web Services, Inc., Cisco Systems, Inc., Dell, technologies Inc., Google LLC, Hewlett Packard Enterprise Development lp, International Business Machines Corporation, Microsoft Corporation, Oracle Corporation, Rackspace Hosting, Inc. and Other Players

Ans: Yes, you can ask for the customization as per your business requirement.

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.9 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Cloud Professional services Market, By Service Type

9.1 Introduction

9.2 Trend Analysis

9.3 Consulting

9.4 Application Development and Modernization

9.5 Implementation and Migration

9.6 Integration and Optimization

10. Cloud Professional services Market, By Deployment Model

10.1 Introduction

10.2 Trend Analysis

10.3 Public Cloud

10.4 Private Cloud

11. Cloud Professional services Market, By Organization size

11.1 Introduction

11.2 Trend Analysis

11.3 Small and Medium-sized Enterprises (SMEs)

11.4 Large Enterprises

12. Cloud Professional services Market, By Vertical

12.1 Introduction

12.2 Trend Analysis

12.3 Banking, Financial Services, and Insurance (BFSI)

12.4 Manufacturing

12.5 Healthcare and Lifesciences

12.6 IT and ITES

12.7 Government

12.8 Telecommunications

12.9 Retail and Consumer Goods

12.10 Energy and utilities

12.11 Others

13. Regional Analysis

13.1 Introduction

13.2 North America

13.2.1 USA

13.2.2 Canada

13.2.3 Mexico

13.3 Europe

13.3.1 Eastern Europe

13.3.1.1 Poland

13.3.1.2 Romania

13.3.1.3 Hungary

13.3.1.4 Turkey

13.3.1.5 Rest of Eastern Europe

13.3.2 Western Europe

13.3.2.1 Germany

13.3.2.2 France

13.3.2.3 UK

13.3.2.4 Italy

13.3.2.5 Spain

13.3.2.6 Netherlands

13.3.2.7 Switzerland

13.3.2.8 Austria

13.3.2.9 Rest of Western Europe

13.4 Asia-Pacific

13.4.1 China

13.4.2 India

13.4.3 Japan

13.4.4 South Korea

13.4.5 Vietnam

13.4.6 Singapore

13.4.7 Australia

13.4.8 Rest of Asia Pacific

13.5 The Middle East & Africa

13.5.1 Middle East

13.5.1.1 UAE

13.5.1.2 Egypt

13.5.1.3 Saudi Arabia

13.5.1.4 Qatar

13.5.1.5 Rest of the Middle East

13.5.2 Africa

13.5.2.1 Nigeria

13.5.2.2 South Africa

13.5.2.3 Rest of Africa

13.6 Latin America

13.6.1 Brazil

13.6.2 Argentina

13.6.3 Colombia

13.6.4 Rest of Latin America

14. Company Profiles

14.1 Alibaba group holding limited

14.1.1 Company Overview

14.1.2 Financials

14.1.3 Products/ Services Offered

14.1.4 SWOT Analysis

14.1.5 The SNS View

14.2 Amazon web services, Inc.

14.2.1 Company Overview

14.2.2 Financials

14.2.3 Products/ Services Offered

14.2.4 SWOT Analysis

14.2.5 The SNS View

14.3 Cisco Systems, Inc.

14.3.1 Company Overview

14.3.2 Financials

14.3.3 Products/ Services Offered

14.3.4 SWOT Analysis

14.3.5 The SNS View

14.4 Dell, technologies Inc.

14.4 Company Overview

14.4.2 Financials

14.4.3 Products/ Services Offered

14.4.4 SWOT Analysis

14.4.5 The SNS View

14.5 Google LLC.

14.5.1 Company Overview

14.5.2 Financials

14.5.3 Products/ Services Offered

14.5.4 SWOT Analysis

14.5.5 The SNS View

14.6 Hewlett Packard enterprise development lp.

14.6.1 Company Overview

14.6.2 Financials

14.6.3 Products/ Services Offered

14.6.4 SWOT Analysis

14.6.5 The SNS View

14.7 International business machines corporation

14.7.1 Company Overview

14.7.2 Financials

14.7.3 Products/ Services Offered

14.7.4 SWOT Analysis

14.7.5 The SNS View

14.8 Microsoft Corporation

14.8.1 Company Overview

14.8.2 Financials

14.8.3 Products/ Services Offered

14.8.4 SWOT Analysis

14.8.5 The SNS View

14.9 Oracle Corporation

14.9.1 Company Overview

14.9.2 Financials

14.9.3 Products/ Services Offered

14.9.4 SWOT Analysis

14.9.5 The SNS View

14.10 Rackspace Hosting, Inc.

14.10.1 Company Overview

14.10.2 Financials

14.10.3 Products/ Services Offered

14.10.4 SWOT Analysis

14.10.5 The SNS View

15. Competitive Landscape

15.1 Competitive Benchmarking

15.2 Market Share Analysis

15.3 Recent Developments

15.3.1 Industry News

15.3.2 Company News

15.3.3 Mergers & Acquisitions

16. USE Cases and Best Practices

17. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The AI governance Market Size was valued at USD 167.5 Million in 2023 and is expected to reach USD 1926.2 Million by 2031 and grow at a CAGR of 35.7 % over the forecast period 2024-2031.

The Low Code Development Platform Market size was valued at USD 17.98 billion in 2022 and is expected to grow to USD 164.9 billion by 2030 and grow at a CAGR of 31.92 % over the forecast period of 2023-2030.

The AI Trust, Risk and Security Management (AI TRISM) Market was valued at USD 1.74 Billion in 2023 and is expected to be worth USD 5.88 Billion by 2031, increasing at a 16.4% CAGR between 2024 and 2031.

The Enterprise Video Market size was valued at USD 18.34 billion in 2022 and is expected to grow to USD 48.37 billion By 2030 and grow at a CAGR of 12.89 % over the forecast period of 2023-2030.

The Law Enforcement Software Market size was USD 15.2 billion in 2022 and is expected to Reach USD 31.1 billion by 2030 and grow at a CAGR of 9.4% over the forecast period of 2023-2030.

The Data Monetization Market was estimated to be worth USD 2.8 billion in 2022, and it is anticipated to reach USD 12.11 billion by 2030, growing at a CAGR of 20.1% from 2023 to 2030.

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd