Cloud Security Posture Management Market Report Scope & Overview:

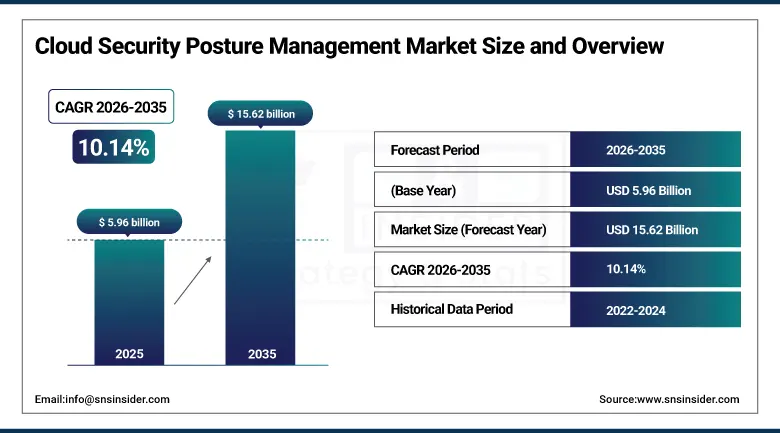

The Cloud Security Posture Management Market was valued at USD 5.96 Billion in 2025 and is expected to reach USD 15.62 Billion by 2035, growing at a CAGR of 10.14% from 2026–2035.

CSPM refers to a security technology that helps assess, monitor, and fix any misconfigurations in cloud systems in order to mitigate any security threats as well as meet compliance standards. As more companies use multi-cloud and hybrid cloud architecture, the level of complexity in cloud security configuration management has increased. CSPM vendors offer an automated way to manage cloud assets, enforce security policies, detect potential vulnerabilities, and comply with regulatory standards. This market is expected to be fueled by the increase in breach incidents due to cloud misconfiguration, higher adoption of cloud technology, and risk management.

In 2025, Wiz introduced its AI Security Posture Management capability as an extension of its CSPM platform, enabling security teams to automatically discover, inventory, and assess the security posture of AI models, training datasets, and AI pipeline infrastructure deployed across cloud environments.

Market Size and Forecast

-

Market Size in 2026E: USD 6.56 Billion

-

Market Size by 2035: USD 15.62 Billion

-

CAGR: 10.14% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Cloud Security Posture Management Market - Request Free Sample Report

Cloud Security Posture Management Market Trends

-

The use of artificial intelligence in CSPM systems helps in better risk prioritization by determining the most pressing issues of cloud security that require attention.

-

CSPM can be integrated with other cloud security products, making it possible for organizations to manage not only their cloud posture but also workload protection, identity controls, and runtime security from one single platform.

-

Security scanning in infrastructure as code helps organizations identify cloud misconfigurations early during the development phase and fix them before moving to production.

-

Multi-cloud usage is increasing, and hence there is an increased need for CSPM platforms that can provide a consolidated view of multiple cloud environments.

-

The automation of compliance functions makes it easier for companies to remain compliant with regulatory requirements and facilitate audits.

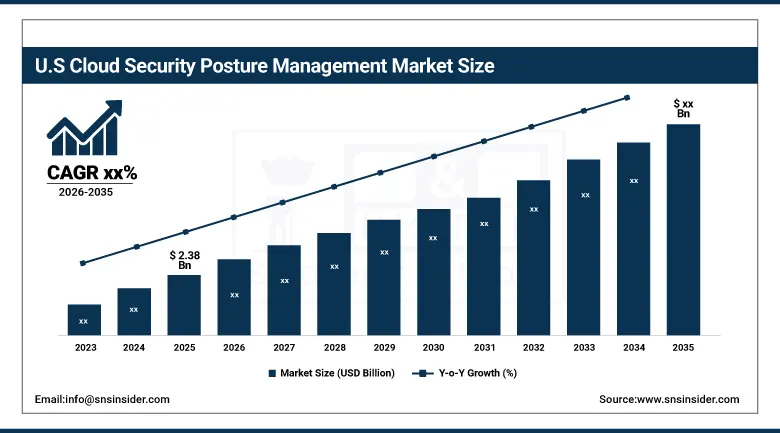

U.S. Cloud Security Posture Management Market Outlook

The U.S. Cloud Security Posture Management Market was valued at approximately USD 2.38 Billion in 2025 and is expected to grow significantly through 2035.

The U.S. is currently the biggest CSPM Market due to high levels of cloud adoption in enterprises and governments. Fears about cybersecurity issues coupled with heavy regulations and the high risks that accompany cloud breaches in terms of money and reputation have led companies to adopt sophisticated CSPM tools. The regulatory landscape, together with the need for compliance and transparency, continues to reinforce the trend towards cloud security monitoring.

Cloud Security Posture Management Market Segment Analysis

-

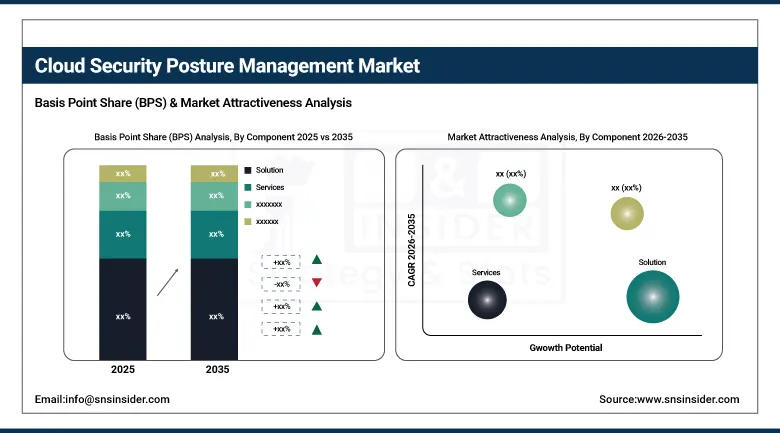

By Component, the Solution segment dominated the Cloud Security Posture Management Market with approximately 70% share in 2025, while the Services segment is the fastest growing.

-

By Cloud Type, the Public Cloud segment dominated the Cloud Security Posture Management Market with approximately 52% share in 2025, while the Hybrid Cloud segment is the fastest growing cloud type with a CAGR of approximately 12.18%.

-

By Organization Size, the Large Enterprises segment dominated the Cloud Security Posture Management Market with approximately 63% share in 2025, while the Small & Medium-Sized Enterprises segment is the fastest growing at 11.33% CAGR.

-

By End User, the BFSI segment dominated the Cloud Security Posture Management Market with the largest share in 2025, while the Healthcare segment is the fastest growing end user.

By Component, solution dominates, services grow fastest

Solutions constituted the largest share of the CSPM market in 2025, making up around 70% of the total market due to increased usage of automated cloud security and compliance management software solutions. Cloud Security Posture Management software solutions feature functionalities such as real-time monitoring, configuration management, policy compliance, compliance reporting, and remediation among others, aiding organizations in safeguarding their cloud computing networks. Increased demand for cloud-based security solutions and agentless scanning techniques has played a pivotal role in boosting the usage of CSPM software solutions due to ease of operation and installation.

The Services segment emerged as the fastest-growing part of the CSPM market as companies are looking to leverage the skills and expertise of third-party vendors to make full use of cloud security offerings. Enterprises need external help with CSPM software implementation, customization of policies, cloud security evaluations, compliance management, platform integration, and monitoring services.

By Organization Size, large enterprises dominate, SMEs grow fastest

The Large Enterprises category dominated the CSPM Market, contributing about 63% in 2025. The domination of the category was a result of the use of multi-cloud and hybrid clouds deployment model by most of the larger companies. Many enterprises operating across diverse sectors such as banking, health care, IT, and governments have advanced cloud infrastructure that requires monitoring, compliance, and risk assessment. Such enterprises understand the importance of securing their clouds in terms of money and reputation losses due to the consequences of cloud security failures.

SMEs is the fastest-growing segment in the CSPM market, growing at a CAGR of around 11.33%. Increasing cloud adoption by small and medium enterprises (SMEs) exposes them to various threats related to cloud computing and compliance issues. CSPM offers an affordable method to manage the configuration of the security system and avoid any compliances. With the increasing realization of the risk associated with cybercrimes and the availability of scalable CSPM solutions, SMEs have been rapidly adopting these solutions worldwide.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

India |

34.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

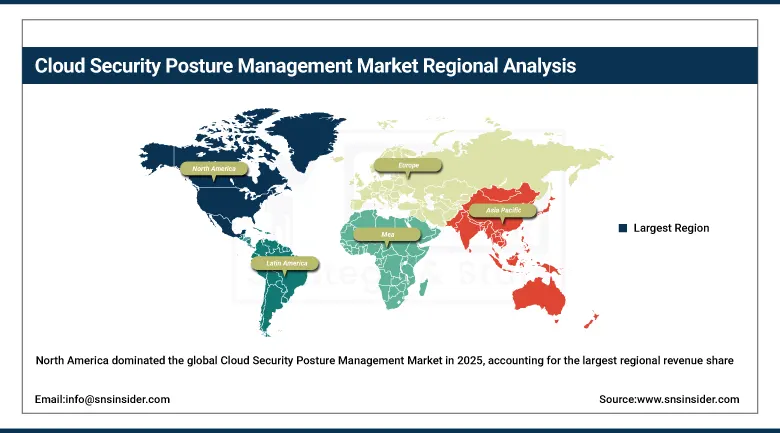

North America Cloud Security Posture Management Market Insights

North America dominated the global Cloud Security Posture Management Market in 2025, accounting for the largest regional revenue share. The United States accounts for approximately 82.5% of North American revenues through the combination of the highest enterprise cloud adoption rate, the most active cybersecurity regulatory enforcement environment, and the commercial concentration of leading CSPM platform providers whose innovation and go-to-market capabilities sustain North American market leadership.

Canada contributes supplementary demand through its growing cloud adoption, the financial services sector's OSFI cloud security guidance requirements, and the healthcare sector's provincial privacy regulation compliance obligations that create CSPM adoption incentives aligned with the U.S. market's regulatory-driven demand pattern.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cloud Security Posture Management Market Insights

Europe held a significant share of the global CSPM Market in 2025. GDPR's extensive obligations for technical security measures protecting personal data processed in cloud environments, the EU's NIS2 Directive's cloud security requirements for critical infrastructure operators, and the DORA regulation's cloud risk management requirements for financial services collectively create the world's most comprehensive regulatory framework for cloud security investment whose compliance mandates drive CSPM adoption independent of voluntary security improvement motivations.

Germany accounts for approximately 28.5% of European revenues through its large financial services sector, the commercial presence of major enterprise software companies, and the BSI's cloud security guidelines whose technical requirements create CSPM adoption incentive across German enterprises managing cloud workloads.

Asia Pacific Cloud Security Posture Management Market Insights

Asia Pacific is the fastest-growing regional CSPM market, driven by aggressive digital transformation across financial services, healthcare, and government sectors whose rapid cloud adoption is creating security posture management requirements at a pace that internal security team development cannot match. India accounts for approximately 34.8% of Asia Pacific revenues through its extraordinary IT services sector's cloud security posture management requirements, the rapid adoption of cloud-first architecture among Indian digital-native enterprises, and the implementation of the Digital Personal Data Protection Act 2023 whose compliance requirements create CSPM investment motivation across organisations processing Indian citizen data.

China, Singapore, Japan, and Australia each contribute significant regional demand through their respective cloud adoption trajectories, regulatory cybersecurity frameworks, and the growing enterprise awareness of cloud misconfiguration risk whose high-profile breach incidents create CSPM investment urgency. Asia Pacific's projected CAGR of 25% through the forecast period reflects the combination of rapid cloud adoption pace, regulatory framework development, and enterprise security maturity investment across the region's diverse national markets.

MEA & Latin America Cloud Security Posture Management Market Insights

The UAE leads MEA revenues at approximately 22.8% of the regional total through its advanced digital economy infrastructure, the comprehensive cybersecurity regulatory framework of the Telecommunications and Digital Government Regulatory Authority, and the cloud-first digital transformation investment of government and financial services sectors whose cloud environment security management creates growing CSPM demand.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its LGPD personal data protection law's cloud security implications, the large financial services sector's cloud adoption and regulatory compliance obligations under Banco Central do Brasil's cloud computing guidelines, and the growing enterprise cloud adoption across retail, manufacturing, and technology sectors.

Market Dynamics

Growth Drivers: Escalating cloud misconfiguration as the leading cloud breach cause and multi-cloud environment complexity exceeding manual security management capacity

The Cloud Security Posture Management market is experiencing rapid growth because companies are embracing cloud technology at an accelerated pace, regardless of whether they use public, private, or hybrid clouds. As cloud computing becomes increasingly complex, the number of configurations, identities, access permissions, and network policies needed to monitor also rise considerably. This development has been making it increasingly difficult to conduct manual cloud security management, which is fueling demand for tools that offer automated, continuous security assessment and monitoring.

The rising number of cloud-related security attacks caused by improper configuration of the infrastructure or lack of sufficient security measures is another key driver behind the growth of the market in question. Companies have been embracing cloud security posture management to automate the process of identifying vulnerabilities and implementing necessary security policies to minimize the risks of data breaches. The adoption of multi-cloud environments has also been fueling market growth.

Restraints: Integration complexity across heterogeneous cloud environments and alert fatigue from misconfiguration volume overwhelming security team remediation capacity

The implementation of CSPM technologies in large enterprise settings can be complicated due to the fact that CSPM tools need to be integrated into many cloud accounts, cloud regions, and service providers. Integration with cloud APIs, DevOps workflows, IT service management systems, and security analytics tools is required, thus increasing costs and time related to implementation, as well as requiring specific technical knowledge. The use of CSPM solutions therefore increases the overall complexity and costliness of cloud deployments.

One more issue associated with the use of CSPM technologies in enterprises is their tendency to generate a huge number of security findings upon their implementation for the first time. Thousands of policy and compliance violations and configuration weaknesses are detected, which requires the involvement of a security team with adequate cloud expertise in addressing all such findings. Otherwise, a backlog will arise and some findings might not be addressed at all.

Opportunities: AI-powered attack path contextualisation and Infrastructure as Code security integration represent transformative CSPM capability frontiers

Attack path analysis using artificial intelligence is a great opportunity for CSPM vendors since the technology can help customers analyze the risk related to potential vulnerabilities that can result from misconfigurations, too many permissions, and exposure to threats via network access. Attack path analysis provides an efficient way of managing remediation efforts, eliminating alert fatigue, and focusing on high-risk vulnerabilities.

The adoption of CSPM in Infrastructure as Code (IaC) projects is another promising trend. It allows organizations to detect any issues related to the configuration of their cloud resources during deployment. This approach to security can help organizations lower costs associated with the process of remediation, accelerate the time-to-market of cloud applications, and stay compliant with security requirements at all times.

Recent Developments:

-

Wiz introduced AI Security Posture Management as a CSPM platform Wiz introduced the concept of AI Security Posture Management as an expansion of CSPM to manage and assess the security posture of the AI model, training data, and AI pipeline infrastructure across the cloud environment in response to the new attack surface created by the proliferation of LLMs and generative AI workloads.

-

Palo Alto Networks introduced Prisma Cloud Darwin in 2023, which provides attack path analysis powered by artificial intelligence to visualize the resultant impact of misconfiguration, identity permissions, and exposure through network access. This will enable the user to prioritize their remediation activities based on breach risk.

-

In December 2023, Upwind – a runtime-powered CNAPP vendor – teamed up with RealCloud to offer their cloud security/CSPM services to Latin America.

Cloud Security Posture Management Market Key Players

-

Wiz Inc.

-

Palo Alto Networks Inc.

-

CrowdStrike Holdings Inc.

-

Microsoft Corporation

-

Amazon Web Services Inc

-

Google LLC

-

Check Point Software Technologies Ltd.

-

Trend Micro Inc.

-

Lacework Inc.

-

Orca Security Ltd.

-

Tenable Holdings Inc.

-

Rapid7 Inc.

-

Qualys Inc.

-

Zscaler Inc.

-

Aqua Security Software Ltd.

-

Sysdig Inc.

-

Ermetic Ltd.

-

Sonrai Security

-

Accurics Inc.

-

Upwind Security Inc.

Cloud Security Posture Management Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.96 Billion |

| Market Size by 2035 | USD 15.62 Billion |

| CAGR | CAGR of 10.14% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Solution, Services) • by Cloud Type (Public Cloud, Private Cloud, Hybrid Cloud) • by Organization Size (Large Enterprises, Small & Medium-Sized Enterprises) • by End User (BFSI, Healthcare, IT & Telecom, Government, Retail & E-Commerce, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Wiz Inc., Palo Alto Networks Inc., CrowdStrike Holdings Inc., Microsoft Corporation, Amazon Web Services Inc, Google LLC, Check Point Software Technologies Ltd., Trend, Micro Inc., Lacework Inc., Orca Security Ltd., Tenable Holdings Inc., Rapid7 Inc., Qualys Inc., Zscaler Inc., Aqua Security Software Ltd., Sysdig Inc., Ermetic Ltd., Sonrai Security, Accurics Inc., Upwind Security Inc. |

Frequently Asked Questions

The Cloud Security Posture Management Market is expected to grow at a CAGR of 10.14% from 2026 to 2035.

The Cloud Security Posture Management Market was valued at USD 5.96 Billion in 2025.

Regulatory frameworks including GDPR, HIPAA, PCI DSS, and NIS2 creating compliance-driven CSPM investment.

The Public Cloud segment dominated the Cloud Security Posture Management Market with approximately 52% share in 2025, while the Hybrid Cloud segment is the fastest growing at approximately 12.18% CAGR.

North America dominated the Cloud Security Posture Management Market in 2025 with the largest regional share, with the United States accounting for approximately 82.5%

Get in Touch