Molecular Modeling Market Report Scope and Overview:

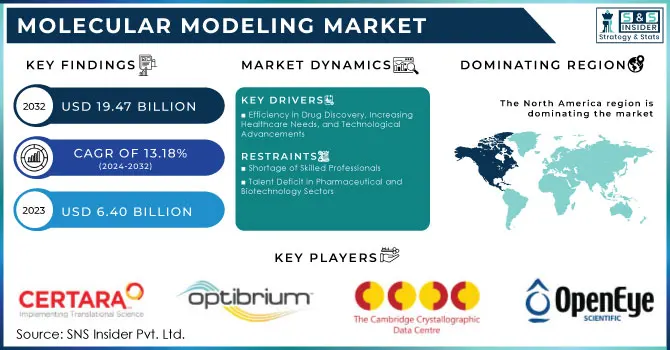

The Molecular Modeling Market Size was valued at USD 7.24 billion in 2024 and is expected to reach USD 19.50 billion by 2032 and grow at a CAGR of 13.18% over the forecast period 2025-2032.

The molecular modeling market is growing rapidly because of its vital contribution to ongoing drug discovery, materials science, biotechnology, and more. High efficiency in the process of research and development simplifies processes, which stimulates demand for tools in these areas, especially for the biotechnology and pharmaceutical industries. Organizations invest much of their resources in molecular modeling technology to promote drug discovery and development. This helps researchers predict molecular interactions and behaviors that can help them identify promising drug candidates faster and more economically.

Market dynamic innovation was recently evidenced by the Sandbox AQ's announcement of its AQBioSim platform. Through the use of leapfrog technology, it works with AstraZeneca Sanofi, and UCSF, to model the intricate molecular structures of diseases like cancer, Alzheimer's, and Parkinson's. It uses advanced tools, including Absolute Free Energy Perturbation software, that allow for very high-precision predictions of molecular interactions, greatly increasing the possibility of discovering drugs at the early stages. A fine example is the Pangu Drug Molecule Model applied by researchers at Xi'an Jiaotong University of Huawei Cloud. Therein, AI-powered systems support a faster and less costly design of drugs by creating opportunities for a healthier research and development process while trimming considerable costs.

Get more information on Molecular Modeling Market - Request Sample Report

An additional significant force behind the increase in molecular modeling demand is an emerging trend of chronic conditions: cancer and neurodegenerative diseases. This can be attributed to the ever-increasing elderly population, better healthcare infrastructures, and the expanding need for more targeted and effective therapeutics. Molecular modeling helps develop new generations of pharmaceuticals by enabling the use of structural biology methods and a better understanding of molecular behaviors. However, this is not free from a few limitations, such as difficulty in modeling complex interactions, like hydrogen bonding. Innovations like Japan's BasePairPuzzle, which aims to represent DNA base pairing accurately, address some of these challenges and make biochemical applications even further expandable in the capabilities of molecular modeling.

Despite such challenges as the scarcity of skilled professionals, the growth in AI and computational tools is driving the molecular modeling market forward. Growth is expected to be influenced by the increasing investment in R&D and the ongoing demand for innovative solutions in drug discovery, materials science, and other fields. Thus, the molecular modeling market is an important part of modern scientific research that can help achieve faster and cheaper breakthroughs across multiple disciplines.

Molecular Modeling Market Size and Forecast:

-

Market Size in 2024: USD 7.24 Billion

-

Market Size by 2032: USD 19.50 Billion

-

CAGR: 13.18% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

Molecular Modeling Market Highlights:

-

Efficiency in Drug Discovery helps accelerate development of safer, targeted, and commercially viable drugs while reducing experimental costs

-

Rising Healthcare Needs from growing chronic disease prevalence and healthcare spending drive demand for advanced molecular modeling tools

-

Technological Advancements including AI-enabled drug design, cloud platforms, high-performance computing, and quantum chemistry enhance R&D efficiency

-

Talent Deficit with shortage of skilled professionals in computational biology, bioprocessing, and AI-driven drug discovery hampers innovation

-

Precision Medicine and Biologics Growth with adoption of personalized therapies, peptides, and novel modalities increases the need for modeling solutions

-

Investment and R&D Expansion as pharmaceutical and biotech companies increasingly invest in molecular modeling to optimize drug efficacy and reduce side effects

Molecular Modeling Market Drivers:

-

Efficiency in Drug Discovery, Increasing Healthcare Needs, and Technological Advancements

Increasing requirements for efficient drug discovery methodologies and increasing medication development needs are the main drivers for the molecular modeling market. Researchers and scientists have applied molecular modeling tools in testing therapeutic efficacy in more affordable and safer manners and also accelerated the launching of drugs into the market. Such technology is most relevant as it addresses the rise of chronic diseases around the globe, where proper drugs to treat them become imperative. This has led to the enormous investment of pharmaceutical and biotech companies in R&D, which has resulted in the development of more powerful and targeted drugs that also are commercially viable.

Favorable factors include a growing population, increased awareness of health issues among the public, improved healthcare infrastructure, and healthcare spending. The sector still attracts a lot of investment, in which companies work on developing new molecular modeling tools to help them improve the lead compounds in terms of higher affinity and specificity and desirable pharmacokinetic characteristics. This optimization reduces possible side effects and raises drug efficacy; therefore, it contributes significantly to the effectiveness of the drug discovery and development process.

The long-term demand for molecular modeling remains high, as there is an increased prevalence of chronic illnesses in low- and middle-income countries. Consequently, the increase in the demand for better drug development methods will continue to propel growth in the molecular modeling market through the next few years.

Molecular Modeling Market Restraints:

-

Talent Deficit in Pharmaceutical and Biotechnology Sectors

The pharmaceutical and biotechnology sectors are facing a significant talent deficit driven by rapid technological advancements, growing R&D demands, and an expanding global healthcare market. The shortage is most pronounced in areas such as bioprocessing, computational biology, regulatory affairs, and advanced therapeutics, where specialized expertise is essential. Companies struggle to fill critical roles due to limited qualified candidates, competition among industry players, and the lengthy training required for emerging technologies like cell and gene therapy or AI-driven drug discovery. This talent gap hampers innovation, slows product development, and increases operational costs, making workforce development a strategic priority for the industry.

Molecular Modeling Market Opportunities:

-

Emerging Growth Horizons and Innovation-Driven Opportunities in the Global Molecular Modeling Market

The Molecular Modeling Market presents strong opportunities driven by the rising adoption of AI-enabled drug design, the growing need for faster and cost-effective R&D, and the expansion of precision medicine. Increasing use of computational tools to reduce experimental failures, optimize lead identification, and model complex biomolecular interactions is accelerating demand across pharmaceutical, biotechnology, and academic research sectors. Cloud-based modeling platforms, integration with high-performance computing, and advancements in quantum chemistry are opening new growth avenues. Additionally, the surge in biologics, peptides, and novel therapeutic modalities further expands the market’s potential, as modeling tools become essential for structure prediction and mechanism-of-action analysis.

Molecular Modeling Market Segment Analysis:

By Product

In 2024, software was a leading molecular modeling market in terms of the provision of necessary computational tools and drug discovery and development platforms. The demand for advanced model software is due to higher requirements for efficient drug designs, molecular simulations, and virtual screenings. The preferred segment for the software for its scalability, precision, and integration into different research environments can be very high. It should have a strong market share with a high share, earning more than 60% of the revenues of the market.

The services market is the fastest-growing part of this business, in large part because of the rising complexity in drug discovery that requires more customized molecular modeling solutions. Companies and institutions are outsourcing services related to molecular modeling to ensure their projects run efficiently without expending on infrastructure. Included in the services segment, therefore, are consulting and training and cloud-based solutions, with the latter experiencing most of the demand as such organizations look for expert opinions and bespoke solutions.

By Application

Drug discovery remained the application segment leader, accounting for the highest share of the molecular modeling market in 2024. This is mainly due to the continued necessity of fast and cost-effective methods in identifying and developing new drugs especially as the industry shifts more towards targeting a specific mechanism of disease as well as increasing success rates. The drug discovery process is strongly benefited by molecular modeling tools, such as in silico screening, target identification, and lead optimization. In 2024, the drug discovery segment accounted for more than half of the total market revenue. Drug development is identified to be the fastest application segment, driven by increased demand for accurate and rapid development pipelines. In terms of drug development processes, the integration of molecular modeling helps improve drugs in their pharmacokinetics, less side effects with high overall efficacy. High demand due to the method adopted by computational methods and designs to develop drugs is highly desired with optimal characteristics; and rapid market expansion by a CAGR of 18-20%.

Molecular Modeling Market Regional Highlights:

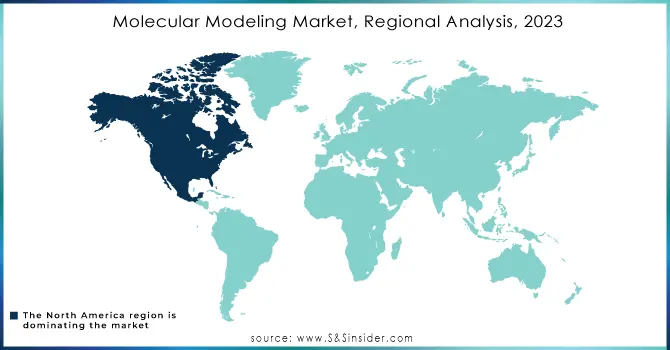

North America Molecular Modeling Market Trends:

North America dominated the Molecular Modeling Market in 2024 due to the presence of major research institutes, academic organizations, and leading pharmaceutical innovators that provide open access to advanced research resources. This environment has accelerated technological advancements in molecular simulations and computational chemistry. Strong strategic alliances among biotech firms have boosted R&D investments, resulting in more potent drug candidates aligned with stringent regulatory standards. Rising cases of cancer and cardiovascular diseases continue to drive the use of molecular modeling for precision drug development.

Europe America Molecular Modeling Market Trends:

Europe represents the second-largest market, with an expected CAGR of 17.3%. Strong public and private research funding, along with rising adoption of clinical trials integrating computational models, significantly supports market expansion. Horizon Europe’s €95.5 billion budget is central to promoting innovation across biomedical sciences. Germany currently holds the largest market share, supported by its advanced pharmaceutical manufacturing base, while the UK is emerging as the fastest-growing country due to rapid adoption of AI-driven molecular analysis techniques and strong academic-industry collaborations.

Asia-Pacific Molecular Modeling Market Trends:

The Asia-Pacific region is projected to grow at the fastest pace, driven by rising disposable income, expanding healthcare infrastructure, and a growing number of research institutions adopting computational drug design tools. Countries such as China, India, South Korea, and Japan are rapidly increasing investments in biotechnology, genomics, and AI-based drug discovery. Government-led digital health and pharmaceutical innovation initiatives further strengthen the region’s position. As demand for cost-effective therapeutics rises, molecular modeling is becoming essential to accelerate local drug development pipelines.

Latin America Molecular Modeling Market Trends:

Latin America is emerging as a promising market due to increased investment in pharmaceutical R&D, expansion of biotech startups, and rising awareness of computational modeling in drug development. Brazil and Mexico lead the region with growing adoption of molecular simulation tools in academic research and early-stage drug discovery programs. Government-led modernization of healthcare systems and improved access to scientific funding are also promoting market expansion. As clinical trial activity grows, especially in oncology and infectious diseases, the need for advanced molecular modeling techniques is increasing steadily.

Middle East & Africa Molecular Modeling Market Trends:

The Middle East & Africa market is experiencing moderate but accelerating growth as countries invest in strengthening healthcare infrastructure and developing national biotech capabilities. The UAE, Saudi Arabia, and South Africa are key contributors, with growing academic collaborations and government initiatives supporting biomedical innovation. The rise of precision medicine programs and increased prevalence of chronic diseases are encouraging pharmaceutical companies to adopt molecular modeling for faster and more accurate drug development. While the region is still developing technologically, partnerships with global research institutions are boosting adoption rates.

Need any customization research on Molecular Modeling Market - Enquiry Now

Molecular Modeling Market Key Players:

-

Schrödinger LLC

-

Dassault Systèmes (BIOVIA)

-

Chemical Computing Group (CCG)

-

OpenEye Scientific

-

Simulations Plus Inc.

-

Optibrium Ltd.

-

Cresset Acellera Ltd

-

BioSolveIT GmbH

-

Cambridge Crystallographic Data Centre (CCDC)

-

Centera LP

-

Wavefunction Inc.

-

ChemAxon

-

Gaussian Inc.

-

Inte:Ligand GmbH

-

Molecular Networks GmbH (Altamira)

-

Acellera

-

Q-Chem Inc.

-

CSC – IT Center for Science (Finland)

-

AMBER Development Consortium

-

Open Molecular Software Foundation / community-driven modeling organizations

Molecular Modeling Market Competitive Landscape:

Simulations Plus, Inc., founded in 1996, is a U.S.-based leader in modeling and simulation software for the pharmaceutical industry. Its flagship products, including ADMET Predictor® and GastroPlus®, integrate AI/ML with PBPK and QSP modeling to accelerate drug discovery, optimize compounds, and support regulatory submissions. The company also offers consulting services to streamline R&D and improve decision-making

-

In June 2025, Simulations Plus released ADMET Predictor® 13, adding advanced AI/ML models, enhanced PBPK simulations, and enterprise-ready automation for drug discovery.

BIOVIA, a brand of Dassault Systèmes established in 2001, provides advanced software solutions for molecular modeling, simulation, and scientific informatics. Its platforms integrate AI, machine learning, and computational chemistry tools to accelerate drug discovery, materials research, and chemical development. BIOVIA supports enterprises with end-to-end solutions for modeling, lab informatics, and regulatory compliance, fostering innovation in life sciences and materials science.

-

In April 2025, BIOVIA announced its ongoing collaboration with UC Berkeley’s MSSE program, integrating AI and neural-network tools for protein design and stability prediction to drive innovation in molecular sciences.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 7.24 Billion |

| Market Size by 2032 | USD 19.50 Billion |

| CAGR | CAGR of 13.18% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product(Software and Services) • By Application(Drug Development, Drug Discovery and Others) • By End-User(Pharmaceutical & Biotechnology Companies and Research & Academic Centers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Schrödinger LLC; Dassault Systèmes (BIOVIA); Chemical Computing Group (CCG); OpenEye Scientific; Simulations Plus Inc.; Optibrium Ltd.; Cresset Acellera Ltd; BioSolveIT GmbH; Cambridge Crystallographic Data Centre (CCDC); Centera LP; Wavefunction Inc.; ChemAxon; Gaussian Inc.; Inte:Ligand GmbH; Molecular Networks GmbH (Altamira); Acellera; Q-Chem Inc.; CSC – IT Center for Science (Finland); AMBER Development Consortium; Open Molecular Software Foundation / community-driven modeling organizations. |

Frequently Asked Questions

Ans: The Molecular Modeling Market is to grow at a CAGR of 13.18% over the forecast period 2025-2032.

Ans: The major players are BioSolveIT GmbH, OpenEye Scientific Software, Certara, L.P, Cambridge Crystallographic Data Centre, Optibrium, Cresset, Dassault Systèmes, Schrödinger, LLC, Chemical Computing Group, Acellera Ltd., and others in the final report.

- The increased prevalence of several chronic diseases has encouraged the development of novel medications.

- Pharmaceutical and biotechnology firms are expanding their R&D expenditures.

Ans: The North American region is dominating the market.

Ans: The Molecular Modeling Market Size was valued at USD 7.24 billion in 2024.

Get in Touch