Concentrated Nitric Acid Market Report Scope & Overview

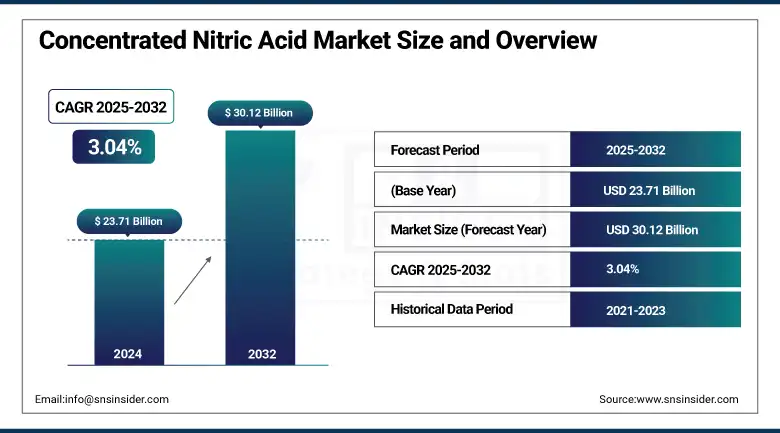

The Concentrated Nitric Acid Market size was valued at USD 23.71 billion in 2024 and is expected to reach USD 30.12 billion by 2032, growing at a CAGR of 3.04% over the forecast period of 2025-2032.

Concentrated Nitric Acid Market Analysis highlights the surging demand for fertilizer as a key driver of market expansion. The growth of the concentrated nitric acid market is driven by the rising need for fertilizers globally. In the face of a growing global population, the demand for more agricultural output has been increasing, driving the trend of extreme fertilizer consumption. The usage of concentrated nitric acid is in the production of ammonium nitrate, an essential nitrogen component in nitrogen-based fertilizers that boost crop yield. This use is acute in developing areas, in which food security and agricultural productivity are national priorities. Furthermore, favorable government subsidies and various initiatives to encourage the use of efficient fertilizers are also driving the concentrated nitric acid market growth.

To Get more information On Concentrated Nitric Acid Market - Request Free Sample Report

Fertilizer consumption in India has been continuously increasing according to the Economic Survey 2023–24, indicating the country's focus on improving agricultural productivity. The country manufactured around 15.7 million tonnes of nitrogenous fertilizers while importing around 5.1 million tonnes in the FY 2022–23, resulting in a total consumption of about 20.8 million tonnes. Such a trend reminds the world about the increasing dependency on fertilizers to provide food security from crops.

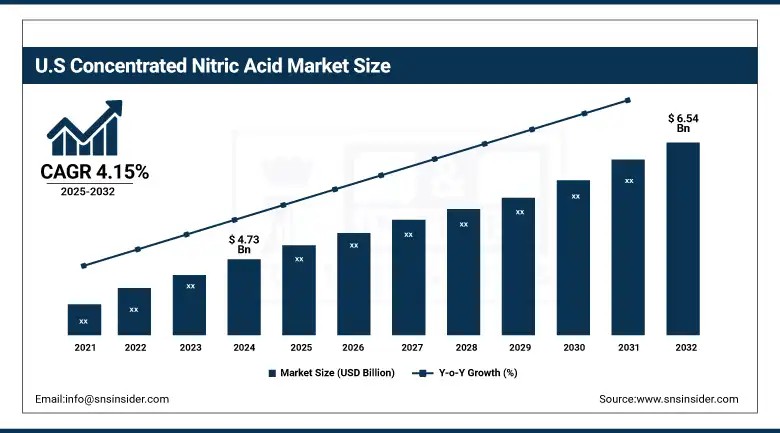

The U.S. Market size was valued at USD 4.73 billion in 2024 and is expected to reach USD 6.54 billion by 2032, growing at a CAGR of 4.15% during the forecast period of 2025-2032. It is due to the substantial agricultural sector in this region and the mature industrial ecosystem; the U.S. dominates the concentrated nitric acid market. The U.S. is one of the world's leading producers and consumers of nitrogen-based fertilizers, relying on concentrated nitric acid for the production of major fertilizers such as ammonium nitrate, an important input driving crop yields and food security. High purity nitric acid is widely produced and locally available, and the presence of major chemical companies in the country provides large-scale production capabilities and a focus on innovative nitric acid technologies.

Market Dynamics:

Drivers:

-

Growth in the Mining and Explosives Industries Drives Market Growth

The mining and explosives industries are one of the major growth drivers of the entire concentrated nitric acid market. Nitric acid is primarily used to manufacture ammonium nitrate, a key ingredient in many explosives. These explosives play an important role in many different types of mining and resource extraction, such as minerals, metals, and fossil fuels. Mining has grown considerably as the global hunger for minerals and metals has climbed, driven by industrialization and urban infrastructure, construction, and energy-sector growth. The increase in mining, especially in emerging economies, has led to a direct rise in the use of explosives, and thereby, concentrated nitric acid. In addition, the improved blasting technologies and industrial safety standards have increased demand for nitric acid due to its high quality and stability as a chemical compound.

According to the European Commission, the turnover of the EU raw materials industry, including mining and quarrying, amounts to about USD 223 billion and employs more than 3.4 million people.

Restraints:

-

Volatility in Raw Material Prices may Hamper Market Growth

The growth of the concentrated nitric acid market is hindered by the volatility in the price of raw materials, mainly ammonia and natural gas. These raw materials are important feedstocks used to manufacture nitric acid, and any increase or decrease in their prices will be directly reflected into their production costs. Factors ranging from global supply-demand mismatches to geopolitical tensions to energy policy changes often drive price volatility. With rising production costs, manufacturers will have a harder time keeping the profit margins intact or will need to increase costs to end-users, which will only have an overall negative effect on end-user demand. This uncertainty can also lead to a lack of long-term investment in production facilities and infrastructure, hindering the gradual development of the market.

Opportunities:

-

Innovation in Production Technologies is Creating Opportunities for Market Growth

The global market for concentrated nitric acid is experiencing significant growth due to the innovation of several production technologies. The traditional processes of making nitric acid are carbon-intensive and are associated with high nitrous oxide (N₂O) emissions, which is also a highly potent climate-change gas. As a result, concentrated nitric acid companies are investing in advanced technologies that reduce CO2 emissions, increase overall process sustainability, and improve energy efficiency. Advancements, such as better catalysts, automation of processes, and waste heat recovery systems not only lower operational costs but also make them comply with strict environmental regulations, and they drive the concentrated nitric acid market trends.

The Nitric Acid Climate Action Group (NACAG) has enabled investment of USD 28.8 million for eleven plant operators globally to install N₂O abatement technologies in countries including Pakistan, Peru, and Georgia.

In 2024, Yara opened their first industrial unit of a green nitric acid production facility that makes use of renewable energy sources for green nitric acid production, located in Norway, to reduce the carbon emissions of Nitric acid. Yara has previously committed to carbon-neutral production by 2050, and the development follows in line with this ambition.

Segmentation Analysis:

By Type

Strong Nitric Acid held the largest concentrated nitric acid market share, around 64%, in 2024 owing to its versatile industrial applications and efficacy in different industrial sectors. Its industrial value is in that it has a high concentration and is used for fertilizers, especially ammonium nitrate, which plays a necessary role as an enabler of the output of food growing production globally. Moreover, concentrated nitric acid finds wide application in the production of explosives, metal processing, and the synthesis of chemicals, where its strong oxidation ability is highly valuable. Additionally, its dominance is reinforced by the growing need for high-purity and high-strength nitric acid in electronics and semiconductor applications.

Fuming nitric acid held a significant market share and is expected to be the fastest-growing segment in the forecast period due to their high purity and concentrated solution, fuming nitric acid occupies the major share of the nitric acid market and is crucial for many specialized but important industrial applications. As it has the same component as concentrated nitric acid but with an increased amount of nitrogen dioxide, this makes it reactive, and its utilization in other processes, such as nitration during manufacturing explosives, pharmaceuticals, and dyes, among others. Fuming nitric acid is in high demand for the synthesis of performance explosives utilized in mining, construction, and defense industries due to its higher nitrating property.

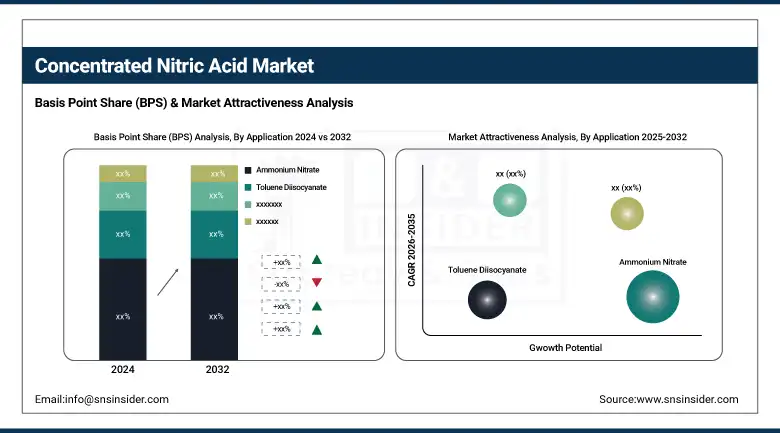

By Application

The ammonium nitrate segment held the largest market share of around 32%, in 2024. The segment’s growth is propelled by its usage as an indispensable raw material in fertilizer production and explosives. Ammonium nitrate, as a major nitrogen fertilizer, improves crop performance, which is one of the key ingredients for global food production, to meet population and agricultural expansion needs. Also, its use in industrial explosives for mining, quarrying, and construction material contributes to the demand. Its widespread use and ability to meet the demands of the agricultural and mining sectors keep ammonium nitrate at the forefront of the market.

The adipic acid segment held a significant market share and was the fastest-growing segment during the forecast period owing to the high level of use of concentrated nitric acid as a key raw material in the production of nylon or other types of synthetic fibers over the forecast period. Most adipic acid is produced by oxidizing cyclohexanol and cyclohexanone with nitric acid, and thus, concentrated nitric acid industry is a key intermediate in its production. The increased usage of nylon in automotive, textile, and packaging continues to drive the demand for adipic acid, which is expected to have a positive impact on concentrated nitric acid demand.

By End-use Industry

The agrochemicals segment held the largest market share, around 32%, in 2024 due to the high usage of nitric acid as an intermediate in the manufacture of fertilizers and pesticides, the agrochemicals segment dominates the concentrated nitric acid market in terms of market share. Concentrated nitric acid is used to produce nitrogenous fertilizers such as ammonium nitrate, which play a critical role in increasing crop yields and agricultural output. As the world population grows and more food is needed, there is an ongoing demand for agrochemical products that can assist farmers in growing crops sustainably.

Automotive held a significant market share owing to the rising number of high-performance materials and components required for automotive production. Concentrated nitric acid is an important precursor to specialty chemicals, including adipic acid, a primary precursor for nylon used in automotive parts. Besides, nitric acid is used in corrosion-resistant coating and metal finishing in automotive component production to improve durability and safety. The automotive sector is changing towards sustainable, lightweight, fuel-efficient, and long-lasting vehicles, driving the demand for new materials and chemicals, aided by concentrated nitric acid.

Regional Analysis:

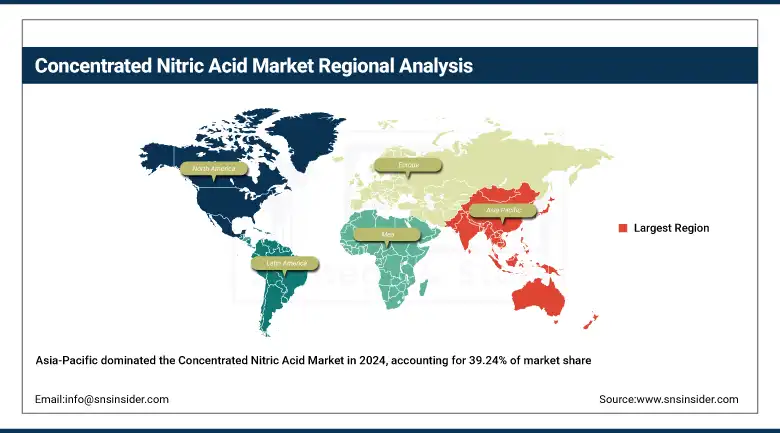

Asia Pacific held the largest market share, around 39.24%, in 2024 as it is a very fast-developing region, as industrialization in China and India grows together with the agricultural activities in these two countries. Asia Pacific is one of the elderly fertilizer production centers, largely caused by the high demand for nitrogen fertilizer to feed its huge and increasing population. Furthermore, the flourishing manufacturing industries such as automotive, electronics and chemicals, and others, also boost the consumption of concentrated nitric acid as an essential feedstock in numerous industrial applications. Asia Pacific is a strategic market for nitric acid with government programs that encourage agricultural productivity and infrastructure, and the presence of chemical manufacturing facilities.

Get Customized Report as per Your Business Requirement - Enquiry Now

In March 2024, KBR reported its latest milestone with GNFC with the successful commissioning of its 2nd plant based on KBR's Magnac Cna technology in Gujarat, India. It utilizes sustainable technologies that recycle process water without treatment, boost energy efficiency, and reduce emissions.

North America held a significant market share and is projected to witness significant growth during the forecast period. This expansion is driven by the presence of established industrial base along with higher demand from end-use industries, such as agriculture, automotive, and electronics. Access to advanced manufacturing infrastructure and widespread technological adoption within the area enables quick and versatile production of concentrated nitric acid. North America is also a major producer and consumer of nitrogen-based fertilizers, which leads to stable demand from crops. The demand for cleaner production technology for nitric acid due to government regulations and environmental standards has also contributed positively to the nitric acid industry.

For instance, in 2023, Trammo is a producer of a nitric acid production plant located in North Bend, Ohio, part of the U.S. nitric acid supply chain. This expansion helped the company expand its expansion in market.

Europe held a significant market share in 2024. It is owing to the high demand from the industries in the region combined with a well-established chemical manufacturing infrastructure. The region encompasses a large number of global chemical producers who manufacture nitric acid for different end uses such as tubes, automotive components, fertilizers, explosives, and pharmaceuticals. Europe leads in production, sustainably, and environmental friendliness, and hence trend in nitric acid technologies has driven the market growth in the region. This is expected to increase the demand for high-quality concentrated nitric acid, as production processes are ensured through stringent environmental regulations in European countries to use of advanced and cleaner production processes.

Key Players:

The leading players operating in the market are BASF SE, Linde plc, CF Industries Holdings, Inc., Nutrien Ltd., Yara International ASA, OCI Nitrogen, Deepak Fertilizers and Petrochemicals Corporation Ltd., Dyno Nobel, Sinopec, and Mitsubishi Chemical Corporation.

Recent Developments:

-

In October 2023, BASF introduced a new high-purity nitric acid grade specifically for the production of lithium-ion battery cathodes. The release of this product is in line with the rapidly increasing battery material demand within the electric vehicle sector.

-

In 2024, Yara International ASA opened its first commercial-scale green nitric acid production facility in Norway. Running on renewable energy and primarily serving the fertilizer sector, the facility is designed to minimize carbon emissions.

-

In January 2023, Grupa Azoty S.A. opened a new site to manufacture concentrated nitric acid in January 2023 in Poland which expanded their former capacity. With the new facility, the designed capacity adds up to 40,000 metric tons per year, yielding fully 80,000 tons annually.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 23.71 Billion |

| Market Size by 2032 | USD 30.12 Billion |

| CAGR | CAGR of3.04% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Strong Nitric Acid, Fuming Nitric Acid) • By Application (Ammonium Nitrate, Adipic Acid, Nitrobenzene, Toluene Diisocyanate, Others) • By End-use Industry (Agrochemicals, Explosives, Automotive, Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BASF SE, Linde plc, CF Industries Holdings, Inc., Nutrien Ltd., Yara International ASA, OCI Nitrogen, Deepak Fertilisers and Petrochemicals Corporation Ltd., Dyno Nobel, Sinopec, Mitsubishi Chemical Corporation. |

Frequently Asked Questions

Ans: Asia Pacific led the Concentrated Nitric Acid Market in the region with the highest revenue share in 2023.

Ans: Growth in the mining and explosives industries drives the market growth.

Ans: Strong Nitric Acid will grow rapidly in the Concentrated Nitric Acid Market from 2024 to 2032.

Ans: The expected CAGR of the global Concentrated Nitric Acid Market during the forecast period is 3.04%

Ans: The Concentrated Nitric Acid Market was valued at USD 23.71 billion in 2024.

Get in Touch