Conductive Silicone Rubber Market Report Scope & Overview:

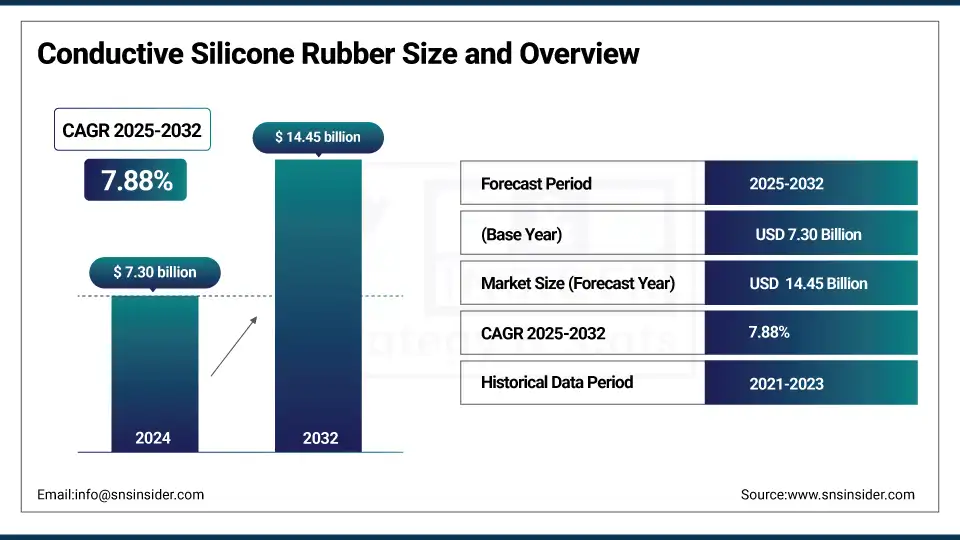

The Conductive Silicone Rubber Market size was valued at USD 7.30 billion in 2024 and is expected to reach USD 14.45 billion by 2032, growing at a CAGR of 7.88% over the forecast period of 2025-2032.

Increasing adoption of EVs, 5G infrastructure, and electronic components is driving the conductive silicone rubber market. Growing battery systems demand for thermally conductive silicone sheets and increasing EMI shielding requirements for electrically conductive silicone sheets are leading the key players to focus on the conductive silicone rubber market. The market is influenced by the invention of conductive elastomer and the environmental-friendly formulations trends. As conductive silicone rubber businesses, such as WACKER unveiled ELASTOSIL N9189 for power generation at CWIEME2025, production was expanded at Karlovy Vary, Czech Republic.

To Get more information On Conductive Silicone Rubber Market - Request Free Sample Report

IEA stated that global sales of EVs reached 17 million in 2024, increasing by 25% YoY, and contributing to the growth of the conductive silicone rubber market share. The Dow and Carbice collaboration accelerate the pace of the thermal interface industry, including the conductive silicone market. These factors validate a robust incidence of conductive silicone rubber and reveal sustained conductive silicone rubber market growth owing to the technological, regulatory, and environmental aspects in target end-use industries.

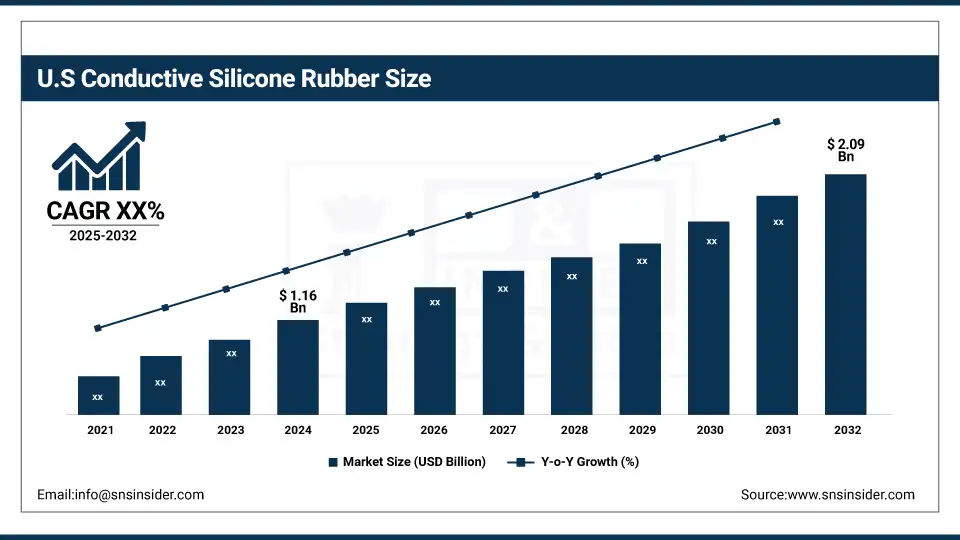

The U.S. dominates the North American conductive silicone rubber market with a market size of USD 1.16 billion in 2024 and is projected to reach a value of USD 2.09 billion by 2032 with a market share of about 67%. The dominance is due to strong EV sales, robust aerospace programs, and local manufacturing strength. According to the U.S. Department of Energy, U.S. EV sales grew 50% year-over-year in 2023. Dow and DuPont, headquartered in the U.S., are among the top conductive silicone rubber companies investing in thermally conductive silicone innovations. The U.S. military and defense sectors are increasingly integrating electrically conductive silicone sheets in EMI shielding for sensitive systems, boosting domestic demand for specialized conductive elastomers.

Conductive Silicone Rubber Market Dynamics:

Drivers:

-

Increasing Adoption of Lightweight, High-Performance Materials in Electric Vehicles Enhances the Conductive Silicone Rubber Market Share

The conductive silicone rubber industry is highly influenced by the demand for lightweight and thermally conductive materials in electric vehicles. Thermally conductive silicone sheet is also common in battery system construction to control heat. Global EV sales reached 17 million in 2024, up 25% on the year, according to the International Energy Agency. This is also driving the conductive silicone rubber manufacturers to develop super-light conductive silicone rubber. The demand is also surging in the conductive silicone rubber market, and along with it, the conductive silicone rubber market size in the automotive and mobility sectors.

-

Expansion of 5G Infrastructure Accelerates Demand for EMI Shielding with Electrically Conductive Silicone Sheets

Demand for electrically conductive silicone sheets is rising due to the increasing build-out of 5G networks and the associated need for EMI shielding. The Global Mobile Suppliers Association reported that over 160 commercial 5G networks were launched globally in 2024. ELASTOSIL N 9189 was introduced for such applications by conductive silicone rubber producers, such as WACKER. Silicon sheet is in demand for shielding of much smaller telecom equipment. This trend is changing the size of the conductive silicone rubber market and driving its growth in the telecommunications and smart electronics applications.

Restraints:

-

Global Supply Chain Uncertainties and Export Controls Constrain Raw Material Sourcing for Conductive Silicone Rubber Companies

The conductive silicone rubber industry is challenged by stringent regulations on raw materials and unpredictability in the supply chain globally. The U.S. export controls on precursors for carbon nanotubes in 2024 constrained access to critical feeds. Firms in conductive silicone rubber have stated that they are experiencing higher sourcing costs and longer lead times owing to geopolitics. These factors are likely to risk the conductive silicone market and challenge the conductive silicone rubber market growth. Organizations need to decouple their supply chain to maintain their standing in hot application areas.

Conductive Silicone Rubber Market Segmentation Analysis:

By Product

Thermally conductive segment dominated the conductive silicone rubber market in 2024 with a 47.80% market share. This dominance is driven by a thermally conductive silicone sheet that is popular with electric vehicle (EV) battery modules for heat release. According to the International Energy Agency, global EV sales were 17 million in 2024, a 25% increase year over year. Auto OEMs use these materials to improve the safety and performance of their batteries. Key manufacturers in the conductive silicone rubber industry, such as Dow and Elkem, are concentrating on improvements in this sub-segment to gain a stronghold over the mobility and power electronics systems on a global level.

The electrically conductive segment is the fastest growing over 2025-2032 with a CAGR of 8.22%. One of the most significant contributors to this trend is electrically conductive silicone sheet, which is widely used for electromagnetic interference (EMI) shielding in small electronics. More than 160 commercial 5G network deployments were accounted for by the Global Mobile Suppliers Association, which has raised the consumption of EMI solutions. Such trends are being embraced by WACKER with the introduction of ELASTOSIL N9189, particularly in the areas of telecommunications and wearable electronics. Growing digital infrastructure globally, the subsegment electrically conductive is expected to change the conative silicone rubber market landscape across smart appliances and telecom equipment applications.

By Application

The automotive and transportation segment dominated in 2024 with a 37.20% market share. This growth is attributed to the increasing use of thermally conductive elastomers in EV battery packs, sensors, and ADAS modules. Electric vehicle sales increased 25% over the previous year in 2024, the International Energy Agency reported. There is a growing role in the supply of advanced thermal interface solutions as conductive silicone rubber companies partner with OEMs to develop these solutions. Thermally conductive silicone sheets for EV cooling systems remain the sub-segment leader, which as seen in new material developments from the likes of Shin-Etsu and Momentive targeting the mobility market.

Electrical and electronics is the fastest-growing application segment with the highest CAGR of 8.22% over 2025-2032. This segment is boosted by the demand for 5G, IOT, and consumer electronics, where electrically conductive silicone sheet is required for EMI shielding and sealing. 5G networks saw significant expansion in 2024, the Global Mobile Suppliers Association reported. Silicone rubber conductive with broad coverage in compact unit mounting. Manufacturers including WACKER and DuPont are launching novel conductive elastomers, and electrical and electronics are the most rapidly growing sub-segment of the conductive silicone rubber market.

Conductive Silicone Rubber Market Regional Outlook:

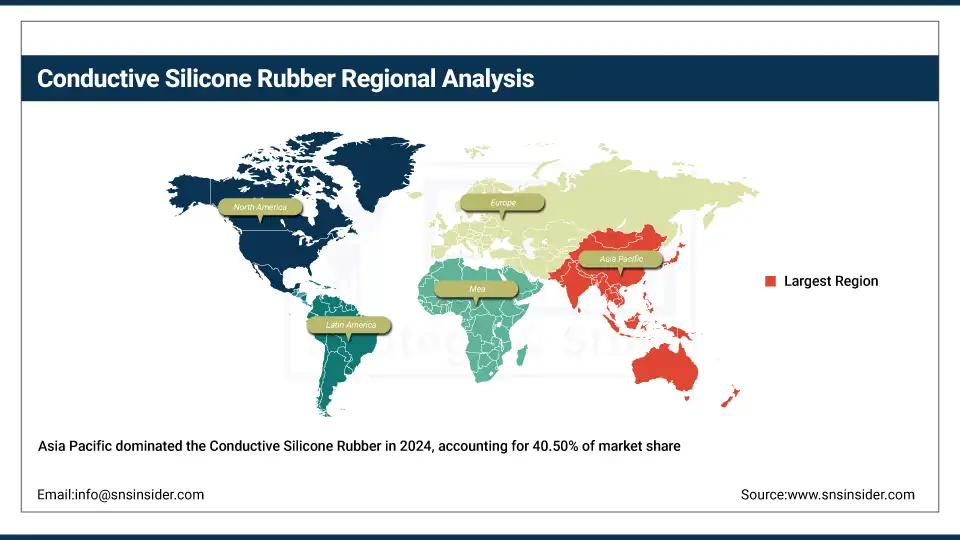

Asia Pacific dominated the conductive silicone rubber market in 2024 with a 40.50% market share, driven by strong electronics and EV manufacturing in China, Japan, and South Korea. China accounted for over 60% of global EV sales in 2024 (IEA), significantly boosting demand for thermally conductive silicone sheets. Japan and South Korea support this growth through the advanced semiconductor and automotive sectors. Companies including Shin-Etsu and Momentive lead the region in innovations for conductive elastomers, securing Asia Pacific’s leadership in the conductive silicone rubber market size and application diversity.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is the fastest-growing region in the conductive silicone rubber market during 2025–2032, led by Germany and supported by strong green energy policies and EV adoption. Germany’s automotive sector and WACKER’s silicone innovations have advanced demand for conductive elastomers. The European Commission’s Fit for 55 package encourages low-emission technologies, boosting the conductive silicone rubber market growth. France and the Netherlands are expanding in 5G and electronics, accelerating the use of electrically conductive silicone sheet across digital infrastructure and transportation, making Europe a major growth center in the forecast period.

North America held a 22.00% share in the conductive silicone rubber market in 2024, ranking third globally. The region's growth is supported by high investment in electric vehicles, aerospace, and defense applications, where both thermally and electrically conductive silicone sheets are required. The U.S. Department of Energy reported that over 1.4 million EVs were sold in the U.S. in 2023, driving strong adoption of conductive elastomers for battery packs and charging infrastructure. The region also benefits from advanced R&D and the local presence of major conductive silicone rubber companies.

Key Players in the Conductive Silicone Rubber Market are:

The major conductive silicone rubber market competitors include Dow, Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Momentive Performance Materials, KCC Corporation, Elkem AS, China National Bluestar (Group) Co., Ltd., Nusil Technology LLC, Reiss Manufacturing, Inc., and Specialty Silicone Products, Inc.

Recent Developments:

-

In September 2024, Shin‑Etsu launched its ST‑OR Type heat‑shrinkable silicone tubing for EV and HEV busbar covering, offering 1.0 W/m·K thermal conductivity and −40 °C to +200 °C performance.

-

In October 2024, Dow and Carbice formed a strategic partnership at The Battery Show North America to co‑develop CNT‑enhanced thermal interface materials for e‑mobility and electronics.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 7.30 billion |

| Market Size by 2032 | USD 14.45 billion |

| CAGR | CAGR of 7.88% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Thermally Conductive, Electrically Conductive, and Others), •By Application (Automotive & Transportation, Electrical & Electronics, Industrial Machines, Construction, Food & Beverage, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Dow, Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Momentive Performance Materials, KCC Corporation, Elkem AS, China National Bluestar (Group) Co., Ltd., Nusil Technology LLC, Reiss Manufacturing, Inc., and Specialty Silicone Products, Inc. |

Frequently Asked Questions

By product: thermally and electrically conductive; by application: automotive dominates, electronics grows fastest due to 5G.

Major players include Dow, WACKER, Shin-Etsu, Elkem, Momentive, DuPont, KCC, Bluestar, and Nusil.

EV adoption, 5G infrastructure, and EMI shielding demand are key drivers for the conductive silicone rubber market growth.

Asia Pacific dominates with a 40.50% share due to strong EV and electronics manufacturing in China, Japan, and South Korea.

The conductive silicone rubber market is valued at USD 7.30 billion in 2024 with a projected CAGR of 7.88%.

Get in Touch