Automotive Aftermarket Fuel Additives Market Report Scope & Overview:

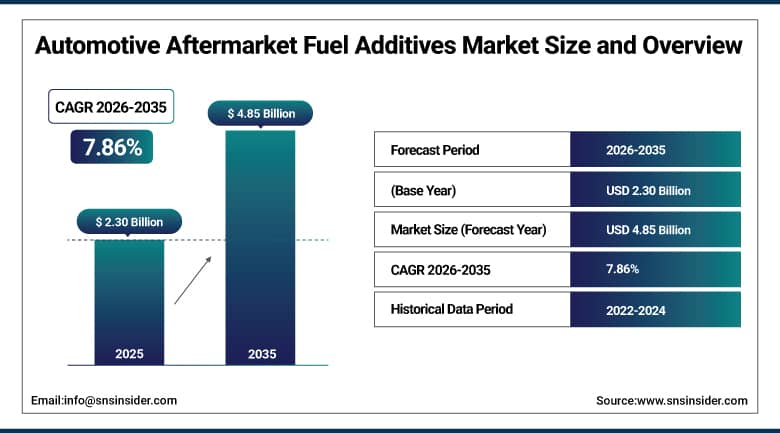

The Automotive Aftermarket Fuel Additives Market was valued at USD 2.30 billion in 2025 and is expected to reach USD 4.85 billion by 2035, growing at a CAGR of 7.86% from 2026 to 2035.

Global vehicle population continues to age, and with the average age of passenger cars on the road exceeding twelve years across major markets, the automotive aftermarket has never been a more commercially dynamic or structurally important segment of the global auto industry. At the center of this expanding aftermarket lies a category of chemical solutions that most drivers barely think about yet that deliver measurable and immediate benefits to engine performance, fuel economy, and emissions output. Aftermarket fuel additives work by restoring and maintaining the cleanliness and functional efficiency of fuel delivery systems that progressively accumulate combustion deposits, varnish, and contaminants that degrade both engine performance and fuel consumption over time. The combination of rising global fuel prices, increasingly stringent emission regulations that older vehicles struggle to comply with through mechanical means alone, growing consumer awareness of preventive vehicle maintenance, and the practical difficulty and cost of engine replacement or rebuilding has created a structural demand environment where fuel additives offer one of the most cost effective vehicle maintenance value propositions available to consumers and fleet operators across every income level and geography.

The global automotive fleet's gradual aging is one of the most powerful and durable structural demand catalysts for the aftermarket fuel additives industry, with data from major markets confirming that vehicles over ten years old are significantly more likely to use aftermarket fuel system treatments than newer vehicles, and with the global fleet of vehicles exceeding ten years of age growing consistently each year, the addressable consumer base for fuel additives is expanding in scale and maintenance urgency simultaneously, creating a compounding demand dynamic that underpins the market's strong CAGR through the forecast period.

Automotive Aftermarket Fuel Additives Market Size and Forecast

-

Market Size in 2025: USD 2.30 Billion

-

Market Size by 2035: USD 4.85 Billion

-

CAGR: 7.86% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026 to 2035

-

Historical Data: 2022 to 2024

To Get More Information On Automotive Aftermarket Fuel Additives Market - Request Free Sample Report

Automotive Aftermarket Fuel Additives Market Trends

-

Growing formulation innovation toward bio based and low toxicity fuel additive chemistries that meet both consumer preference for environmentally responsible products and increasing regulatory scrutiny of volatile organic compound content in consumer chemical formulations.

-

Rising adoption of multi-function or all in one fuel system treatment products that combine injector cleaning, octane enhancement, fuel stabilization, and corrosion protection in a single dosing product, appealing to time constrained consumers seeking simplified vehicle maintenance solutions.

-

Accelerating e-commerce penetration of the fuel additives retail channel, driven by consumer preference for online price comparison, subscription-based auto replenishment models, and the expanding availability of premium additive brands that were previously limited to specialty auto parts stores.

-

Growing demand for ethanol compatible fuel additives across markets where government biofuel blending mandates have increased the ethanol content of pump gasoline, creating phase separation, corrosion, and combustion instability challenges that specialized fuel treatment products address effectively.

-

Increasing use of fuel additives in two-wheeler and small engine applications across Asia Pacific and Latin America, where motorcycles and scooters represent the primary personal transportation mode for large populations and where fuel quality variability creates consistent demand for performance and protection additives.

U.S. Automotive Aftermarket Fuel Additives Market Size Outlook:

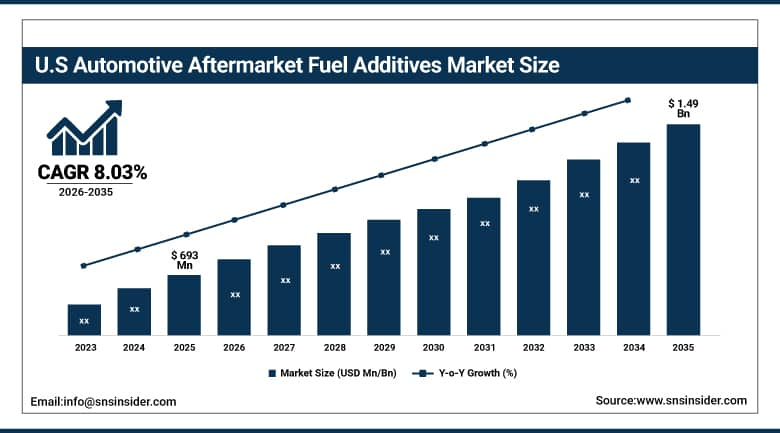

The U.S. Automotive Aftermarket Fuel Additives Market was valued at USD 693 million in 2025 and is expected to reach USD 1.49 billion by 2035, registering a CAGR of 8.03% during 2026 to 2035.

United States is the single largest national market for automotive aftermarket fuel additives, supported by the world's largest per capita vehicle fleet, a deeply ingrained consumer culture of vehicle self-maintenance driven by a robust auto parts retail infrastructure, and strong product awareness cultivated by decades of marketing investment from established additive brands. The large installed base of high mileage vehicles that dominate the U.S. vehicle population creates consistent first use demand for fuel injector cleaners and system treatments that deliver noticeable performance restoration benefits. Cold climate conditions across the northern states create strong seasonal demand for cold flow improvers and fuel stabilizers in diesel powered trucks and equipment. The widespread availability of fuel additive products through a dense network of auto parts retailers, big box stores, gas stations, and online channels ensures excellent consumer accessibility. Chevron's expansion of its Techron additive line to over 4,000 retail locations in 2023 exemplifies the competitive intensity and distribution investment driving U.S. market growth.

The increasing prevalence of high ethanol content gasoline blends including E10, E15, and E85 across the U.S. fuel supply is creating a growing and specialized demand category for ethanol stabilizer and phase separation prevention additives, particularly among consumers operating older vehicles designed for conventional gasoline, seasonal equipment, marine engines, and collector cars where ethanol's hygroscopic properties and material compatibility limitations create specific maintenance challenges that purpose designed fuel treatment products address effectively.

Automotive Aftermarket Fuel Additives Market Segment Insights

-

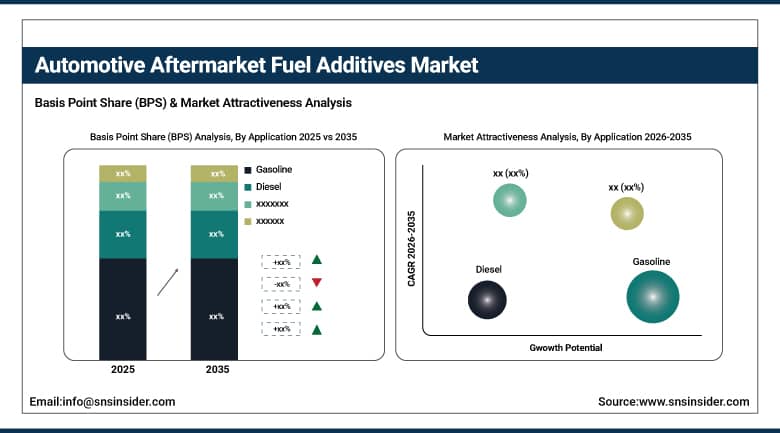

Based on Application, Gasoline accounted for the largest market share in 2025; Diesel expected to grow at a competitive CAGR through 2035 driven by commercial vehicle demand.

-

Based on Type, Fuel Injector Cleaners accounted for the largest market share in 2025; Cetane Improvers expected to register the fastest growth through the forecast period.

-

Based on Vehicle Type, Passenger Cars accounted for the largest market share in 2025; Two Wheelers expected to register the fastest growth driven by Asia Pacific demand.

-

Based on Supply Mode, Third Party suppliers accounted for the dominant market share in 2025; OEM Supplied additives expected to grow as dealer channel integration expands.

-

Based on Distribution Channel, Automotive Workshops and 4S Stores accounted for the largest combined share in 2025; E-Commerce expected to be the fastest growing distribution channel through 2035.

By Application, Gasoline dominates; Diesel growing strongly on commercial vehicle demand

Gasoline fuel additive applications were expected to account for the largest share of aftermarket fuel additive sales revenues in 2025, due to the predominance of gasoline engines in the global light vehicle fleet as well as a large consumer market for gasoline fuel additive products in North America, Asia Pacific, and certain European countries. The gasoline fuel additive category includes injector cleaners, octane boosters, fuel stabilizers, and ethanol fuel additive products formulated to meet the unique technical needs associated with gasoline combustion chemistry, port and direct injector deposits, and ethanol blending requirements in the global gasoline vehicle fleet.

The diesel fuel additive application category is an increasingly strategic source of fuel additive sales revenues, based on a range of products including cetane boosters, diesel fuel injector cleaners, cold flow improver additives, and lubricity additives which address the technical issues associated with diesel engine operations. Underlying demand momentum for diesel fuel additive products was driven by the substantial diesel vehicle fleets in Europe, including passenger cars and commercial vehicles, as well as a rapidly growing diesel commercial vehicle fleet in Asia Pacific. Increased environmental emissions requirements for diesel vehicles were also promoting fleet operators to utilize fuel additive programs.

By Type, Fuel Injector Cleaners dominate; Cetane Improvers fastest growing

Fuel injector cleaners emerged as the leading type of additive in 2025 because of the widespread usage of fuel injectors in gasoline and diesel engines, their ability to quickly restore the engine performance in high-mileage cars, and the fact that they already have a well-established retail presence in auto parts stores, gasoline stations, and online channels in all major markets. The new generation of direct injection gasoline engines are prone to develop injector deposits as a result of higher temperatures and injection pressures used in their operation, which makes injector cleaning treatments essential elements of preventive maintenance of GDI and TGDI engine vehicles. Fleet managers can also be considered institutional consumers of these additives.

Cetane improvers are expected to register the fastest CAGR through 2035, driven by growing commercial vehicle fleet demand across emerging markets where diesel fuel quality can be inconsistent, and by the expanding diesel vehicle population in Europe and Asia where cetane enhancement delivers measurable improvements in cold start performance, combustion smoothness, and exhaust emission quality. Cold flow improvers serve an important seasonal demand in northern hemisphere markets, where diesel gelling in cold temperatures is a significant operational concern for truck and equipment operators. Fuel stabilizers address a growing niche need among owners of seasonal equipment, classic vehicles, and small engine applications where fuel sits unused for extended periods and can degrade in ways that cause significant starting and operational problems.

By Vehicle Type, Passenger Cars dominate; Two Wheelers fastest growing

Passenger cars accounted for the largest vehicle type share of the automotive aftermarket fuel additives market in 2025, reflecting the scale of the global passenger vehicle fleet and the strong consumer demand for fuel economy and performance restoration treatments that reduce operating costs and extend vehicle service life. The large and growing population of older passenger vehicles that increasingly exceed efficient engine performance thresholds due to deposit accumulation creates a structurally expanding addressable market for preventive and restorative fuel treatments in the passenger car segment across all major vehicle markets.

Light commercial vehicles represent the second largest segment, with van and pickup truck operators seeking to manage fuel costs and maintain engine reliability across high annual mileage operational profiles. Heavy commercial vehicles represent an important institutional segment where fleet operators apply fuel additive programs systematically to manage fuel consumption across large diesel-powered truck and bus fleets. Two wheelers are expected to register the fastest CAGR through 2035, driven by the extraordinary scale of the motorcycle and scooter fleet across Asia Pacific and Latin America, where hundreds of millions of two-wheeler operators are progressively being reached by growing retail distribution networks and rising consumer awareness of fuel additive benefits for small displacement engines that are particularly sensitive to fuel quality variation.

By Supply Mode, Third Party dominates; OEM Supplied growing through dealer integration

Third party fuel additive suppliers accounted for the dominant majority of supply mode revenue in 2025, reflecting the inherent competitive advantages of independent additive brands in the aftermarket channel, including broader product portfolios, more aggressive retail pricing, stronger consumer brand recognition in the automotive chemical category, and wider distribution across independent auto parts retailers, online platforms, and general merchandise stores. Third party suppliers compete vigorously on formulation performance claims, packaging convenience, consumer communication, and retail promotional support, creating a dynamic and innovative marketplace that consistently delivers new product formats and treatment concepts to consumers.

OEMs supplying aftermarket fuel additives, which are usually sold via an OEM approved dealer service network and OEM branded or OEM approved brand names, gain advantage from the added weight of factory recommendation and warranty-aligned marketing messages, which appeal to the vehicle owners who are keen on upholding the manufacturer's service standards. With vehicle manufacturers now looking to tap into the aftermarket revenues via the dealer channel, the market share of the OEM fuel additive category within the supply mode category is projected to expand further over the forecast period, especially among premium and luxury cars consumers.

By Distribution Channel, Workshops and 4S Stores lead; E-Commerce fastest growing

Automotive workshops and 4S stores collectively accounted for the largest combined share of the distribution channel segment in 2025, reflecting the strong professional service application pathway for fuel additives where mechanics and service advisors recommend and apply fuel treatments during scheduled maintenance visits. Workshop channel sales benefit from professional credibility, service based upselling opportunities, and the ability to administer concentrated professional grade additive formulations that are not available in retail consumer packaging formats. 4S store dealer channels combine vehicle sales, service, spare parts, and surveys under one roof, creating an integrated environment where fuel additive recommendations by service staff carry significant consumer persuasion weight aligned with manufacturer endorsed maintenance programs.

E-commerce is expected to be the fastest growing distribution channel from 2026 to 2035, driven by online price transparency, consumer review driven purchase confidence, subscription-based replenishment models, and the ability of premium specialty additive brands to reach consumers beyond the geographic footprint of traditional retail distribution networks.

Automotive Aftermarket Fuel Additives Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

31% |

|

Europe |

Germany |

30% |

|

Asia Pacific |

China |

41% |

|

Middle East & Africa |

Saudi Arabia |

28% |

|

Latin America |

Brazil |

46% |

North America Automotive Aftermarket Fuel Additives Market Insights

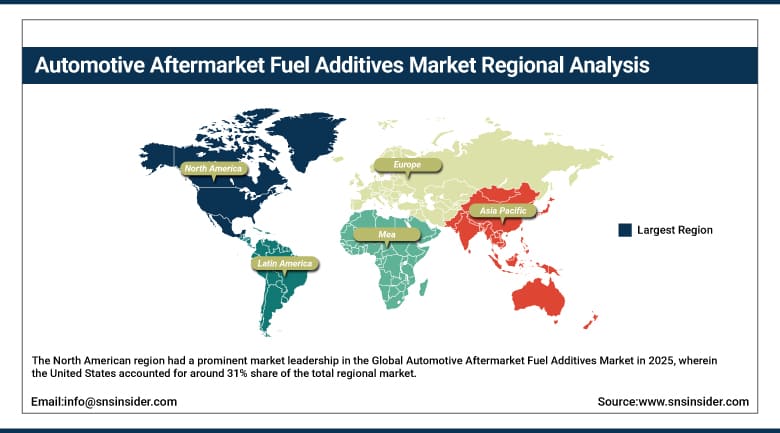

The North American region had a prominent market leadership in the Global Automotive Aftermarket Fuel Additives Market in 2025, wherein the United States accounted for around 31% share of the total regional market. The U.S. market was estimated to be worth USD 693 million in 2025 and is expected to rise to USD 1.49 billion by 2035, on account of the highest vehicle miles traveled, large high mileage vehicles, highly developed retail networks, and strong consumer maintenance practices. Canada will add to the regional market through its large commercial diesel vehicle base and high demand for additives due to its cold climate. Mexico, on the other hand, will help in increasing the market penetration through its expanding automotive aftermarket.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Automotive Aftermarket Fuel Additives Market Insights

Asia Pacific is the fastest growing region in the global Automotive Aftermarket Fuel Additives Market through 2035, driven by rapidly expanding vehicle ownership, rising consumer awareness of vehicle maintenance, fuel quality variability challenges in several markets, and the sheer scale of the region's two-wheeler and commercial vehicle populations. China holds the largest share of Asia Pacific revenue at approximately 41%, supported by the world's largest national vehicle fleet, growing consumer sophistication in vehicle care, and a well-developed e-commerce channel that is making premium additive brands accessible to consumers across the country's vast geography. India, Indonesia, Vietnam, and Thailand represent high growth markets were rising incomes, expanding vehicle ownership, and fuel quality challenges in regional markets create strong structural demand for fuel additive solutions.

Europe Automotive Aftermarket Fuel Additives Market Insights

The region of Europe held a significant share in the worldwide Automotive Aftermarket Fuel Additives Market in 2025, where Germany, France, and the United Kingdom were the major countries that contributed to the revenues generated in the region. The market in Europe was noted for high demand for diesel-specific additives such as cetane improver, injector cleaner, and diesel particulate filter treatment additives owing to the high penetration rate of diesel vehicles in the region and the strict Euro 6d emissions standards which cannot be met by old diesel cars without the help of chemicals. Germany topped the market in Europe due to high penetration rate of diesel cars and strong automotive culture in Germany.

Middle East & Africa and Latin America Automotive Aftermarket Fuel Additives Market Insights

The Middle East and Africa and Latin America represent growing markets with significant untapped potential for aftermarket fuel additives, driven by large and aging vehicle fleets, fuel quality variability challenges, expanding retail infrastructure, and rising consumer awareness of vehicle maintenance benefits. Saudi Arabia leads the MEA market with approximately 28% of regional revenue, supported by one of the highest vehicle ownership rates globally, large commercial fleet operations, and growing consumer interest in premium automotive maintenance products. Brazil dominates Latin America with approximately 46% of regional share, driven by its large vehicle fleet, widespread use of ethanol blended fuels that require specialized additive treatment, and growing distribution network penetration of aftermarket chemical products through both traditional retail and rapidly expanding e-commerce channels.

Automotive Aftermarket Fuel Additives Market Growth Drivers:

-

Rising global fuel prices and increasingly stringent emission regulations creating sustained consumer demand for fuel efficiency and performance solutions

The most fundamental and consistent driver of the Automotive Aftermarket Fuel Additives Market is the straightforward financial motivation that drives vehicle owners and fleet operators to seek cost effective solutions that improve fuel economy, extend engine service life, and defer expensive mechanical maintenance. As fuel prices remain elevated across major markets and the cost of vehicle maintenance and repair continues to rise with increasing engine complexity, the economic return on investment from regular fuel additive use, whether in improved miles per gallon, reduced service interval costs, or extended engine component life, becomes increasingly compelling for cost conscious consumers and efficiency focused fleet managers. At the regulatory level, emission standards that are tightening progressively across all major vehicle markets are creating additional demand for additive solutions that can help aging vehicles meet current emission requirements, particularly in urban areas implementing low emission zone access restrictions that create strong financial incentives for vehicle owners to demonstrate compliance or face significant access fees.

Survey data consistently shows that approximately 55% of vehicle owners globally are aware of and actively use fuel additives as part of their vehicle maintenance routine, and with awareness levels in fast growing markets like India, China, and Southeast Asia still significantly below those in mature markets, the consumer education and brand building opportunity for additive manufacturers in these geographies represents one of the most commercially significant growth vectors available to the industry over the coming decade as vehicle ownership rates and maintenance sophistication converge toward the standards established in North America and Western Europe.

Automotive Aftermarket Fuel Additives Market Restraints:

-

Growing electric vehicle penetration and consumer skepticism about efficacy claims moderating long term demand growth in mature markets

The most significant structural restraint facing the Automotive Aftermarket Fuel Additives Market over the long term is the progressive penetration of battery electric vehicles into the global vehicle fleet, which fundamentally eliminates the addressable market for conventional fuel additives in the portion of the fleet they replace. While the transition from internal combustion engines to electric powertrains is measured in decades rather than years and the existing ICE vehicle fleet will remain large for the foreseeable future, the directional trend is clear, and in markets where EV adoption is accelerating fastest, the long term growth potential of the fuel additive category is structurally constrained. Consumer skepticism about the efficacy claims of some fuel additive products, particularly in categories where product performance is difficult to independently verify without sophisticated testing equipment, also represents an ongoing challenge for the industry's credibility and ability to sustain premium pricing across product ranges.

Automotive Aftermarket Fuel Additives Market Opportunities:

-

Bio based formulations, hybrid vehicle specific additives, and emerging market distribution expansion

The development of bio based and low environmental impact fuel additive formulations represents a meaningful innovation opportunity for the industry, as consumer and regulatory pressure on the environmental footprint of consumer chemical products creates commercial space for premium products that deliver proven engine protection and fuel efficiency benefits through more sustainable chemistry platforms. The rapidly growing global population of hybrid vehicles, which operate internal combustion engines in stop start duty cycles and at variable load profiles distinctly different from conventional vehicle operation, creates demand for additives specifically formulated to address the deposit accumulation and combustion efficiency challenges unique to hybrid powertrain architectures. Emerging market distribution expansion, particularly across Southeast Asia, Sub Saharan Africa, and Latin America, where organized retail penetration of automotive chemical products is still in relatively early stages despite large and growing vehicle populations, represents an important volume growth opportunity for producers with the distribution capabilities and locally relevant product formulations to serve these markets effectively.

Recent Developments:

-

2026: BASF SE introduced a new generation of bio derived fuel system cleaning chemistry for both gasoline and diesel aftermarket applications, combining detergency performance validated at OEM standard test protocols with a significantly reduced petroleum chemical content that positions the formulation for markets implementing consumer chemical VOC restrictions.

-

2025 (April): Innospec Inc. expanded its aftermarket fuel additive distribution network across India and Southeast Asia through a series of new distributor partnerships that significantly increased retail point of sale coverage in motorcycle and light commercial vehicle dominant markets where fuel quality variability creates strong consumer demand for protective additive solutions.

-

2024 (September): Liqui Moly GmbH received Euro 6d certified performance validation for its diesel system cleaner formulation from an independent testing authority, providing the company with a significant marketing and sales support tool for the European market where emission standard compliance claims are subject to rigorous regulatory scrutiny by national enforcement agencies.

-

2024 (March): Lucas Oil Products Inc. launched a dedicated hybrid vehicle fuel system treatment formulated specifically for the deposit management and combustion efficiency requirements of stop start hybrid powertrain operation, becoming one of the first major aftermarket additive brands to address hybrid specific engine challenges with a purpose designed product.

-

2023: Chevron USA expanded its fuel additive product line to over 4,000 service stations and retail store locations across the United States, significantly increasing consumer accessibility and purchase convenience for its established additive range and reinforcing brand visibility at point of need retail locations that serve high frequency vehicle maintenance purchase occasions.

Automotive Aftermarket Fuel Additives Market Key Players:

-

Chevron Corporation

-

BASF SE

-

Afton Chemical Corporation

-

Infineum International Limited

-

The Lubrizol Corporation

-

TotalEnergies Additives & Special Fuels

-

Innospec Inc.

-

Clariant AG

-

BG Products Inc.

-

Lucas Oil Products Inc.

-

Red Line Synthetic Oil Corporation

-

Liqui Moly GmbH

-

Royal Purple LLC

-

Gold Eagle Co.

-

Millers Oils Ltd.

-

STP Products Company

-

Ashland Inc.

-

Cerion Energy

-

Evonik Industries AG

-

Rislone Engine Treatment

Automotive Aftermarket Fuel Additives Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.30 Billion |

| Market Size by 2035 | USD 4.85 Billion |

| CAGR | CAGR of 7.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Fuel Injector Cleaners, Octane Boosters, Cetane Improvers, Fuel Stabilizers, Cold Flow Improvers, Others) • By Application (Gasoline, Diesel) • By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two Wheelers) • By Supply Mode (Third Party, OEM Supplied) • By Distribution Channel (Automotive Workshops, 4S Stores, E-Commerce, Big Stores, Gas Stations, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Chevron Corporation, BASF SE, Afton Chemical Corporation, Infineum International Limited, The Lubrizol Corporation, TotalEnergies Additives & Special Fuels, Innospec Inc., Clariant AG, BG Products Inc., Lucas Oil Products Inc., Red Line Synthetic Oil Corporation, Liqui Moly GmbH, Royal Purple LLC, Gold Eagle Co., Millers Oils Ltd., STP Products Company, Ashland Inc., Cerion Energy, Evonik Industries AG, Rislone Engine Treatment |

Frequently Asked Questions

Diesel additives and deposit control additives are the top drivers, while passenger vehicles dominate the vehicle-type segment. E-commerce and gas stations are major distribution channels fueling accessibility.

The Automotive Aftermarket Fuel Additives Market is expected to grow at a CAGR of 7.86% from 2026 to 2035.

The Automotive Aftermarket Fuel Additives Market was valued at USD 2.30 billion in 2025.

Rising global fuel prices and increasingly stringent emission regulations creating strong consumer demand for cost effective fuel efficiency solutions, combined with a growing global fleet of aging vehicles that benefit most from fuel system cleaning and performance restoration treatments, constitute the primary structural demand drivers of the market through 2035.

Fuel Injector Cleaners held the dominant type segment position in 2025, driven by their broad applicability across gasoline and diesel engines, their immediate perceptible performance restoration benefits for high mileage vehicles, and their strong established retail presence across all major markets globally.

North America and Europe led the global market in 2025 based on established consumer awareness and regulatory frameworks, while Asia Pacific is the fastest growing region through 2035, driven by rapidly expanding vehicle ownership, rising maintenance awareness, and the large and growing two wheeler fleet population across China, India, and Southeast Asia.

Get in Touch