Confidential Computing Market Report Scope & Overview:

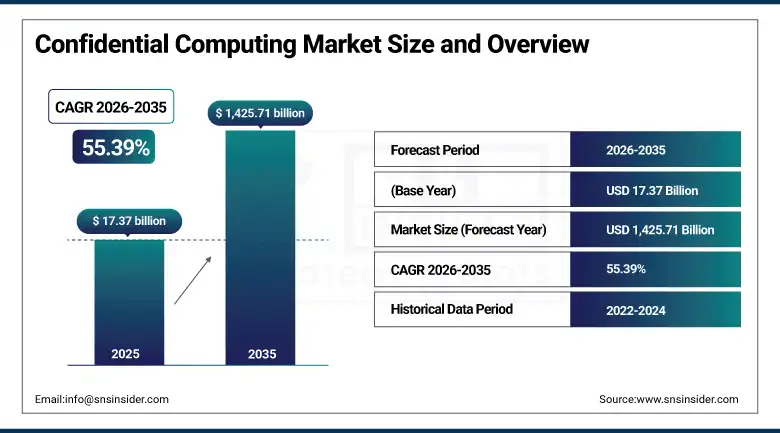

The confidential computing market was valued at USD 17.37 billion in 2025 and is expected to reach USD 1,425.71 billion by 2035, growing at a CAGR of 55.39% from 2026–2035.

Confidential computing addresses a fundamental gap in conventional data security architectures: while encryption has long protected data at rest in storage systems and data in transit across networks, sensitive workloads processed in memory have historically been exposed in plaintext, creating a window of vulnerability during the most active phase of data handling. This technology closes that gap by executing computations inside a hardware-enforced Trusted Execution Environment that shields code and data from the host operating system, the hypervisor, cloud provider administrators, and other applications running on the same physical machine. The result is a cryptographic guarantee that data remains protected throughout processing, not merely during storage or network transmission, which is the assurance that regulated industries, multi-party collaboration scenarios, and sensitive government workloads have long required but been unable to obtain from standard cloud computing deployments.

The acceleration of AI adoption across regulated industries is creating a new and particularly compelling use case for confidential computing, where AI model training on sensitive healthcare records, financial transaction data, or proprietary enterprise datasets requires processing guarantees that only hardware-based TEEs can provide while satisfying the privacy obligations of data owners who would not otherwise consent to pooling their sensitive information.

Market Size and Forecast

-

Market Size in 2026E: USD 26.98 Billion

-

Market Size by 2035: USD 1,425.71 Billion

-

Growth Rate (2026–2035): 55.39%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Confidential Computing Market - Request Free Sample Report

Confidential Computing Market Trends

-

Rising adoption of confidential AI training pipelines enabling healthcare consortia, pharmaceutical companies, and financial institutions to pool sensitive datasets for collaborative model training without any participant exposing raw data to other parties or to the cloud provider infrastructure.

-

Growing deployment of confidential virtual machines from all three major hyperscale cloud providers allowing enterprises to migrate regulated workloads to public cloud infrastructure without waiving control over data-in-use protection guarantees mandated by sector-specific privacy regulations.

-

Expanding use of confidential computing in federated learning architectures for both consumer device privacy protection and enterprise multi-party analytics, where gradient aggregation servers use TEEs to prevent inference attacks on participating devices' local training contributions.

-

Increasing standardisation of remote attestation protocols and confidential computing APIs through industry bodies such as the Confidential Computing Consortium, reducing the integration complexity that previously limited adoption to organisations with specialised security engineering capabilities.

-

Accelerating interest from government and defence sector customers in confidential computing as a foundation for multi-domain data sharing between agencies with different classification levels, supported by emerging zero-trust architecture mandates that require cryptographic proof of workload integrity.

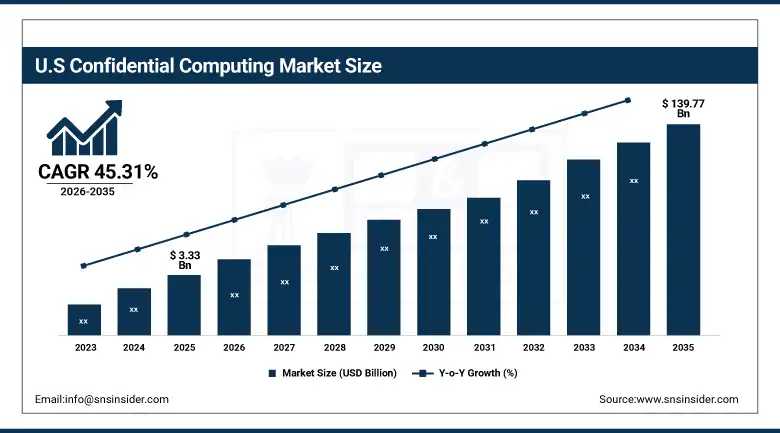

The U.S. Confidential Computing Market Outlook

The U.S. Confidential Computing Market was valued at approximately USD 3.33 billion in 2025 and is expected to reach approximately USD 139.77 billion by 2035, growing at a CAGR of 45.31% over the forecast period, driven by the high rate of enterprise cloud adoption, stringent financial and healthcare privacy regulations, and concentrated demand from the federal government for data-in-use protection technologies.

The United States leads the global confidential computing market through its position as the headquarters of the foundational technology providers including Intel, AMD, NVIDIA, Microsoft Azure, Amazon Web Services, Google Cloud, and IBM Cloud, all of which have embedded TEE capabilities into their core hardware platforms and cloud service offerings and are actively competing to expand confidential computing adoption across enterprise and government customer bases. U.S. federal agencies including the Department of Defence, intelligence community organisations, and the Department of Veterans Affairs are meaningful early customers for confidential computing technology, motivated by the combination of zero-trust security mandates under Executive Order 14028 and the need to share sensitive data across agency boundaries without creating unacceptable intelligence exposure risk.

The convergence of AI adoption mandates, zero-trust architecture requirements, and sector-specific privacy regulations across BFSI, healthcare, and government is creating a policy-driven demand wave for confidential computing in the United States that is separate from and additive to the technology-driven adoption occurring in commercial cloud deployments.

Confidential Computing Market Segment Analysis

-

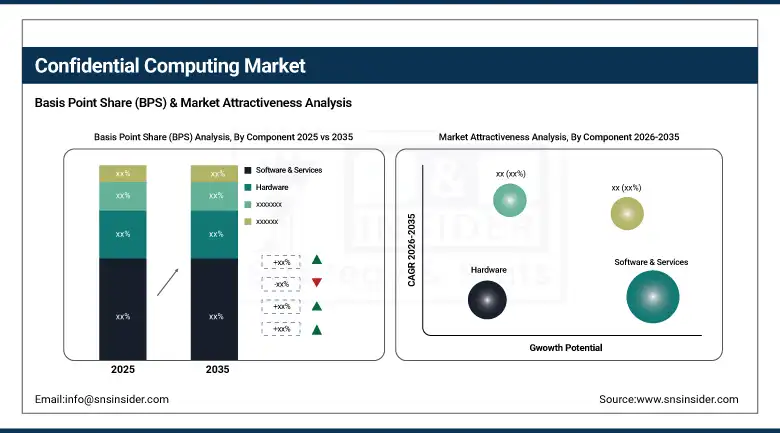

By Component, software & services dominated with approximately 44.50% of revenues in 2025 through scalable, cloud-integrated solutions preferred by enterprises across industry segments. Hardware is the fastest-growing component driven by the proliferation of TEE-enabled CPUs, GPUs, and specialised secure enclaves into new product generations from every major semiconductor vendor.

-

By Deployment, cloud led with approximately 65% of revenues in 2025 as hyperscale confidential VM and confidential container services bring the technology to enterprises without requiring on-premise hardware investment. Edge/on-premise is the fastest-growing deployment driven by IoT, telecom, and real-time analytics applications requiring data protection outside the data centre perimeter.

-

By Enterprise Type, large enterprises dominated with approximately 70% of revenues in 2025 through higher IT budgets, complex regulatory obligations, and sensitive workloads requiring the strongest available protection; SMEs are the fastest-growing enterprise type at a CAGR of 50% as managed confidential computing services lower the adoption barrier for organisations without in-house security engineering teams.

-

By Application, privacy & security held the largest share at approximately 45% in 2025 as compliance, risk management, and sensitive data protection remain the primary purchase motivations across industries; IoT & edge is the fastest-growing application segment driven by demand for secure data collection and AI inference at network edge locations.

-

By Industry, BFSI led with approximately 30% of revenues in 2025 as banks, insurers, and financial institutions deploy confidential computing to protect transaction processing, fraud analytics, and sensitive customer financial data; Healthcare & Life Sciences is the fastest-growing industry segment at a CAGR of 50% driven by genomics research collaborations, clinical AI development, and patient data privacy mandates.

By Component, software & services lead market share, hardware growing fastest

Software & services retained the leading component position with approximately 44.50% of the Confidential Computing Market in 2025, reflecting the practical reality that most enterprise buyers access confidential computing capabilities through managed cloud services, software development kits, and confidential AI platforms rather than through independent hardware procurement. The software layer encompasses TEE orchestration platforms that provision and attest confidential workloads across heterogeneous hardware environments, cryptographic libraries that enable secure multi-party computation and homomorphic encryption for cases where hardware TEEs are impractical, and management consoles that provide audit logging, key management, and compliance reporting for regulated workloads processed in confidential environments.

Hardware is the fastest-growing Confidential Computing component at a CAGR of 67.10% through 2033, driven by the systematic expansion of TEE capabilities from specialised security processors into mainstream CPUs, GPUs, and data processing units manufactured by Intel, AMD, NVIDIA, and Arm licensees. Each successive silicon generation is extending TEE support to larger memory enclave sizes, higher computational throughput within protected environments, and new hardware attestation mechanisms that make remote verification of workload integrity more reliable and more auditable.

By Deployment, cloud dominates, edge/on-premise is expected to grow fastest

Cloud retained the dominant deployment position with approximately 65% of Confidential Computing Market revenues in 2025, reflecting the strong alignment between the technology's value proposition and the security concerns that have historically constrained regulated workload migration to public cloud infrastructure. Microsoft Azure Confidential Computing, AWS Nitro Enclaves, and Google Cloud Confidential VMs provide managed TEE environments that give enterprise customers cryptographic assurance of workload isolation from cloud provider access, the single most frequently cited barrier to migrating sensitive workloads from on-premise data centres to public cloud. The cloud deployment model eliminates the hardware procurement and maintenance overhead that would otherwise make confidential computing inaccessible to mid-market enterprises, and the integration of confidential computing services into existing cloud management consoles makes them available to any organisation already operating cloud workloads without requiring specialised security engineering capability.

Edge and on-premise is the fastest-growing deployment category at a CAGR of 52% through 2033, driven by the expansion of confidential computing beyond its original data centre context into the distributed edge environments where IoT sensors, industrial control systems, autonomous vehicles, and 5G network function virtualisation require data-in-use protection at locations remote from and often physically unsecured relative to enterprise or cloud data centres. The processing of sensitive sensor data and proprietary operational technology data at edge nodes that may be located in publicly accessible or physically exposed locations creates clear security requirements that standard operating system-level isolation controls cannot satisfy, and hardware TEE technology is increasingly being embedded in edge computing platforms, industrial gateways, and automotive-grade processors to address this requirement.

By Enterprise Type, large enterprises dominate, SMEs is expected to grow fastest

Large enterprises held the dominant position with approximately 70% of the Confidential Computing Market in 2025, reflecting the concentration of the most compelling adoption use cases in organisations with the largest regulatory obligations, the most sensitive data estates, and the IT budget scale to invest in relatively early-stage security technology. Global systemically important banks computing credit risk models on customer data shared with external rating agencies, pharmaceutical companies conducting multi-institution genomics research on patient genetic information, and defence contractors processing classified AI training datasets all represent large-enterprise use cases where the security and legal requirements make confidential computing investment straightforwardly justified regardless of the current technology cost premium.

SMEs are the fastest-growing enterprise type at a CAGR of 50% through 2033, driven by the progressive commoditisation of confidential computing access through managed cloud services that remove the hardware and specialised expertise barriers that previously made adoption practical only for well-resourced large organisations. A healthcare software company building an AI diagnostic tool on multi-hospital patient data, a fintech processing transaction patterns for multiple banking clients, or a legal technology firm handling privileged attorney-client communications can now access confidential computing protection through standard API calls to hyperscale cloud platforms without acquiring dedicated hardware or hiring specialised security engineers.

By Application, privacy & security dominates, IoT & edge is expected to grow fastest

Privacy & security retained the leading application position with approximately 45% of Confidential Computing Market revenues in 2025, as the foundational use case of protecting sensitive data during processing remains the most universally applicable and most immediately comprehensible value proposition for enterprise buyers across all industry segments. The primary purchase driver is the need to process regulated data categories including personally identifiable information, protected health information, financial transaction records, and legally privileged communications in shared computing environments while maintaining cryptographic proof that the data has not been accessible to the infrastructure provider or to other tenants.

IoT and Edge is the fastest-growing application segment at a CAGR of 55% through 2033, as the deployment of connected sensors, industrial controllers, autonomous vehicles, and smart city infrastructure at massive scale creates an enormous attack surface of data collection and processing points that operate outside the physical security perimeter of enterprise or cloud data centres. Confidential computing at the edge addresses the specific threat model of a physically accessible device or gateway where an attacker who gains physical access to the hardware might otherwise extract sensitive data or manipulate AI inference workloads.

By Industry, BFSI dominates, Healthcare & Life Sciences is expected to grow fastest

BFSI retained the leading industry position with approximately 30% of Confidential Computing Market revenues in 2025, reflecting the financial services sector's combination of the largest sensitive data volumes, the most stringent regulatory obligations, the greatest financial consequences from data breach events, and the highest organisational awareness of advanced security technologies. Banks deploying anti-money laundering AI models that process transaction data shared from multiple counterparty institutions, insurance underwriters running predictive models on health and actuarial data contributed by competing policyholders, and investment firms protecting proprietary trading algorithm execution from cloud provider infrastructure access represent specific BFSI use cases where confidential computing provides unique and compelling security guarantees unavailable from conventional cloud security controls.

Healthcare & life science is the fastest-growing industry segment at a CAGR of 50% through 2033, driven by the intersection of enormous potential value from AI-powered clinical insights and genomics research with exceptionally stringent patient privacy requirements that have historically prevented the data pooling and computational collaboration necessary to realise that value. Federated learning for clinical AI, where hospital networks contribute local model updates without sharing patient records, gains additional security guarantees when the aggregation server operates in a confidential computing environment that can be cryptographically attested to participating institutions.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82% |

|

Europe |

Germany |

30% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

UAE |

26% |

|

Latin America |

Brazil |

40% |

North America Confidential Computing Market Insights

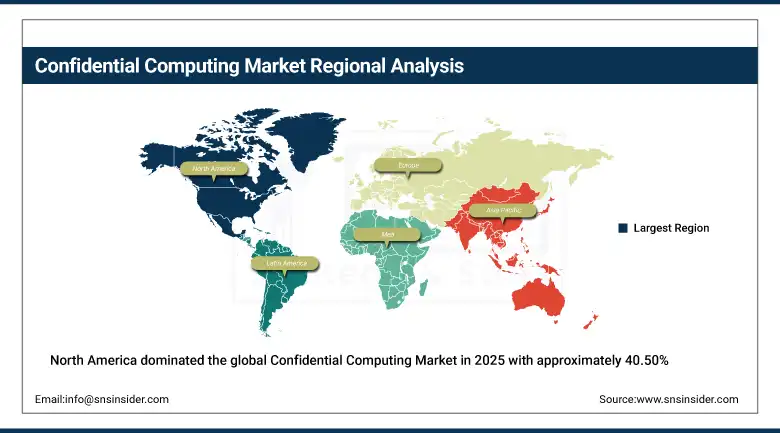

North America dominated the global Confidential Computing Market in 2025 with approximately 40.50% of revenues, led by the United States at approximately 82% of North American revenues. The United States' market leadership reflects the co-location of the world's most capable cloud computing infrastructure, the headquarters of the foundational hardware TEE technology providers, and the regulatory environment that creates the most financially consequential consequences for data-in-use breaches across banking, healthcare, and government sectors. Federal executive orders mandating zero-trust architecture adoption across civilian agencies, combined with the Department of Defence's growing investment in secure AI infrastructure, are creating a sustained government procurement market for confidential computing that supplements and accelerates private sector adoption driven by commercial regulatory requirements.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Confidential Computing Market Insights

Europe is a technically sophisticated and regulation-driven confidential computing market where GDPR's requirements for data protection by design and by default, combined with sector-specific regulations for financial services under DORA and healthcare under the European Health Data Space framework, are providing clear regulatory mandates for technologies that protect sensitive data during processing. Germany's combination of strong data protection enforcement culture, world-leading industrial manufacturing requiring proprietary process data protection, and advanced banking sector creates the most active national market within Europe. The European Commission's investment in confidential computing research through Horizon Europe programmes and the GAIA-X cloud data infrastructure initiative reflects official recognition of the technology's strategic importance for European digital sovereignty.

Asia Pacific Confidential Computing Market Insights

Asia Pacific is the fastest-growing regional market for confidential computing with a projected CAGR of 46.65% from 2026 to 2033, driven by rapid digital transformation across financial services, healthcare, and government sectors in China, Japan, South Korea, Singapore, and Australia, combined with growing data sovereignty regulations across the region that are pushing enterprises and cloud providers to demonstrate stronger data-in-use protection capabilities. China's domestic confidential computing ecosystem is developing through investment in indigenous TEE hardware alternatives to Western semiconductor platforms as part of the country's broader technology self-sufficiency strategy. Singapore and Australia's status as Asia Pacific cloud infrastructure hubs for multinational enterprises is generating demand for confidential computing services that meet the data protection requirements of European and North American parent organisations operating regional workloads in Asia.

Latin America and MEA Confidential Computing Market Insights

Latin America and MEA are growing confidential computing markets driven primarily by financial services and government sector adoption in their most advanced digital economies. Brazil leads Latin American adoption through its large banking sector with sophisticated cybersecurity requirements, supported by the Lei Geral de Protecao de Dados privacy regulation that creates compliance motivation for stronger data protection technologies. MEA adoption is concentrated in the UAE and Saudi Arabia, where smart city programmes, sovereign wealth fund-backed digital infrastructure investments, and the ambition to attract multinational financial services and technology firms create demand for cloud environments that meet international data protection standards.

Market Dynamics

Growth Drivers: Escalating data-in-use security mandates across regulated industries and the emergence of AI workloads requiring protection of proprietary training datasets at unprecedented scale

The primary structural growth drivers for the confidential computing market are the systematic tightening of data protection regulations across jurisdictions worldwide that are creating legal obligations for data-in-use protection that standard cloud security controls cannot satisfy, combined with the explosive growth of enterprise AI adoption that is forcing organisations to confront the data-in-use exposure risk of sensitive training datasets in ways that were not commercially relevant before the AI investment wave began. Financial regulators in the European Union, United Kingdom, United States, and Singapore are all moving toward requirements for demonstrable technical controls over data access during processing, not merely access controls at the database layer, as part of their response to the rising frequency and sophistication of cloud infrastructure attacks. Healthcare privacy enforcement actions under HIPAA in the United States and under GDPR in Europe are establishing precedent that legacy technical safeguards are insufficient for cloud-deployed workloads processing the most sensitive categories of personal health information.

Restraints: Performance overhead within TEE environments, complexity of attestation and key management, and the fragmented hardware TEE landscape requiring application-layer adaptation across multiple vendor implementations

A significant restraint on the confidential computing market is the performance overhead inherent in executing workloads within hardware-enforced Trusted Execution Environments, where the cryptographic operations required to encrypt memory pages, validate attestation chains, and enforce access controls add computational cost and latency that can materially affect the performance of throughput-sensitive applications including large-scale AI training, real-time transaction processing, and high-frequency data analytics. The attestation and key management infrastructure required to operate confidential computing environments securely is substantially more complex than the access control and encryption key management used in conventional cloud security architectures, requiring specialised expertise that most enterprise security teams do not currently possess and that adds meaningful deployment timeline and cost overhead.

Opportunities: AI regulatory compliance driving mandatory confidential AI deployment, sovereign cloud mandates creating new geographic market segments, and multi-party computation unlocking data collaboration markets

The emerging regulatory requirement for AI systems processing personal data to incorporate technical safeguards against model inversion, membership inference, and training data extraction attacks is creating a pathway for confidential computing to become a compliance-mandated feature of enterprise AI infrastructure, similar to the role that database encryption plays in current data protection compliance programmes. The European Union's AI Act provisions for high-risk AI system transparency and data governance are expected to create specific technical requirements that confidential computing is well positioned to satisfy, potentially making TEE-based AI training and inference a compliance standard in the world's most comprehensive AI regulatory jurisdiction. Sovereign cloud mandates from governments requiring that sensitive public sector data be processed exclusively on hardware operated within national borders and on infrastructure that can demonstrate cryptographic data protection guarantees are creating new market segments for confidential computing deployments in dedicated government cloud environments.

Recent Developments:

-

2025: Microsoft rolled out the Azure Integrated HSM security chip across all Azure server hardware, strengthening cryptographic performance and lowering attestation latency across the full Azure Confidential Computing service portfolio, including confidential virtual machines, confidential containers, and Always Encrypted database services.

-

2025: NVIDIA expanded Hopper Confidential Computing capabilities to support larger GPU memory enclaves and improved attestation tooling, enabling pharmaceutical and financial services customers to run sensitive AI training workloads on NVIDIA H100 GPUs with cryptographic isolation guarantees.

Confidential Computing Market Key Players are:

-

Microsoft

-

Google Cloud

-

Amazon Web Services (AWS)

-

IBM

-

Intel Corporation

-

AMD (Advanced Micro Devices)

-

Arm Holdings

-

NVIDIA

-

Oracle

-

Alibaba Cloud

-

Huawei Cloud

-

Fortanix

-

R3

-

Cosmian

-

Anjuna Security

-

Accenture

-

Thales Group

-

VMware

-

Edgeless Systems

-

PhoenixNAP

Confidential Computing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.37 Billion |

| Market Size by 2035 | USD 1,425.71 Billion |

| CAGR | CAGR of 55.39% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (Hardware, Software & Services) •By Deployment (On-premise, Cloud) •By Enterprise Type (Large Enterprises, Small and Mid-sized Enterprises) •By Application (Privacy & Security, Blockchain, Multi-party Computing, IoT & Edge, Personal Computing Devices) •By Industry (BFSI, Manufacturing, Retail & Consumer Goods, Healthcare & Life Science, IT & Telecom, Government & Public Sector, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Microsoft, Google Cloud, Amazon Web Services (AWS), IBM, Intel Corporation, AMD (Advanced Micro Devices), Arm Holdings, NVIDIA, Oracle, Alibaba Cloud, Huawei Cloud, Fortanix, R3, Cosmian, Anjuna Security, Accenture, Thales Group, VMware, Edgeless Systems, PhoenixNAP |

Frequently Asked Questions

Ans: North America dominated with approximately 40.50% of revenues in 2025.

Ans: Software & Services dominated with approximately 44.50% of revenues in 2025.

Ans: Rising regulatory requirements for data-in-use protection across BFSI, healthcare, and government sectors combined with explosive enterprise AI adoption requiring secure processing of sensitive training datasets.

Ans: The Confidential Computing Market was valued at USD 17.37 billion in 2025

Ans: The Confidential Computing Market is expected to grow at a CAGR of 55.39% from 2026 to 2033.

Get in Touch