Construction Software Market Report Scope & Overview:

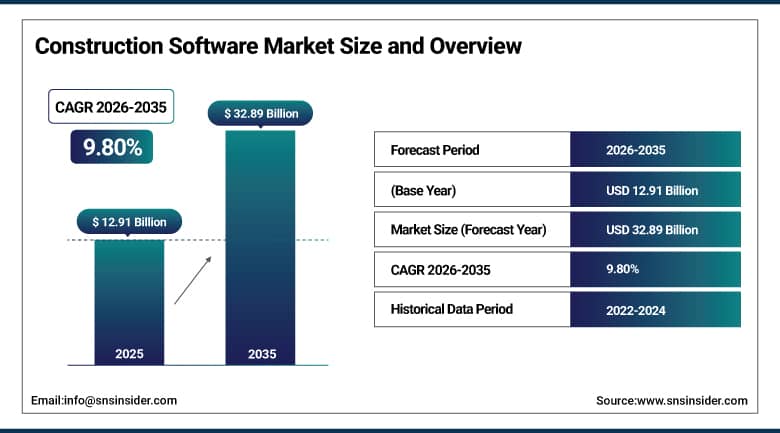

The Construction Software Market was valued at USD 12.91 Billion in 2025 and is expected to reach USD 32.89 Billion by 2035, growing at a CAGR of 9.80% from 2026 to 2035.

The Construction Software Market is growing steadily due to digitalization in the construction industry along with growing need for effective project planning, cost management, and workforce management. Cloud-based construction software is being used by businesses to increase collaboration, improve workflow and improve project visibility in real-time. Integration of Artificial Intelligence (AI), BIM, IoT, and analytics technology is making it easier to execute projects effectively and efficiently. Increasing investment in infrastructure, compliance with regulations, and reducing project delays, cost overruns, and safety hazards are some other factors responsible for the growth of construction software market.

Procore introduced AI-driven agents and a connected resource management platform at its Groundbreak 2024 conference, enhancing coordination of labor, equipment, and materials across construction sites and reflecting the industry's broader shift toward intelligent, automated project management tools.

Market Size and Forecast

-

Market Size in 2026E: USD 14.18 Billion

-

Market Size by 2035: USD 32.89 Billion

-

CAGR: 9.80% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Construction Software Market - Request Free Sample Report

Construction Software Market Trends

-

Construction firms are quickly implementing digital tools like project management, financial management, and field productivity software to adapt to growing project complexity.

-

Cloud deployment continues gaining ground as it offers flexibility, scalability, and real-time access to project data for teams working across multiple locations.

-

Building Information Modeling, AI, and IoT adoption keeps expanding software capability well beyond basic scheduling and document management.

-

Sub-contractors are increasingly adopting digital tools to boost site-level productivity, manage tasks, and improve collaboration with contractors and architects.

-

Quality and safety management modules are becoming standard features as firms face growing pressure to demonstrate regulatory compliance and reduce on-site risk.

U.S. Construction Software Market Outlook

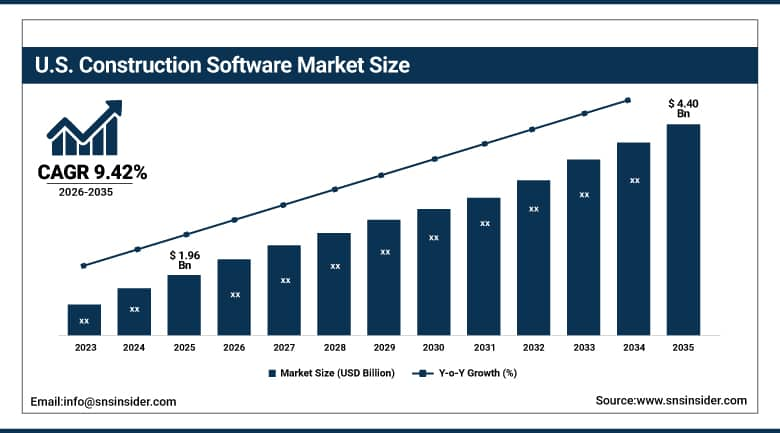

The U.S. Construction Software Market was valued at approximately USD 1.96 Billion in 2026 and is expected to reach approximately USD 4.40 Billion by 2035, growing at a CAGR of approximately 9.42%.

Growth in the U.S. market is being driven by high technological adoption, increasing digital project management, cloud-based solutions, AI integration, and stringent safety and regulatory compliance requirements, all of which are enhancing efficiency, collaboration, and cost control across large-scale construction projects nationwide. American construction firms have been comparatively early adopters of digital project management tools, and that head start, combined with a genuinely deep bench of established construction software vendors headquartered domestically, keeps the U.S. positioned as both the largest single national market and a key innovation hub for the category.

Procore Technologies continued expanding its AI-driven capability throughout 2024 and 2025, layering connected resource management and intelligent agents on top of its core project management platform to help U.S. general contractors coordinate labor, equipment, and materials across increasingly complex, multi-site construction projects.

Construction Software Market Segment Analysis

-

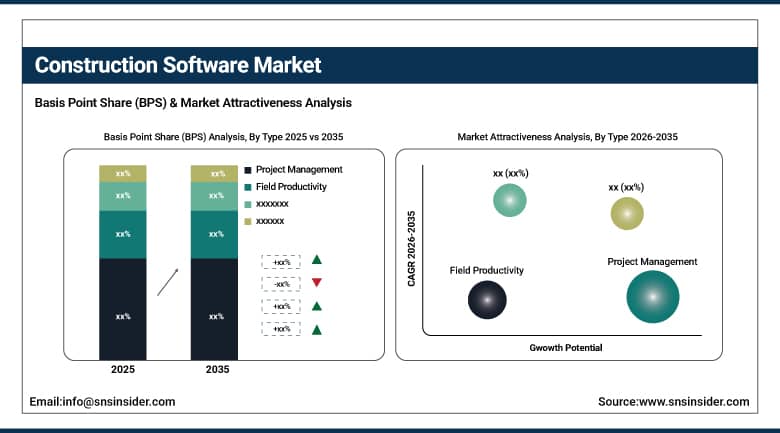

By Type, Project Management segment dominated the Construction Software Market in 2025 with 36% share; Field Productivity segment is the fastest growing segment.

-

By Deployment Mode, Cloud segment dominated the market in 2025 with 71% share; Cloud segment is also the fastest growing segment.

-

By Organization Size, Large Enterprise segment dominated the market in 2025 with 63% share; Medium and Small Enterprise segment is the fastest growing segment.

-

By Application, General Contractors segment dominated the market in 2025 with 34% share; Building Owners segment is the fastest growing segment.

By Type, Project Management Dominates the Construction Software Market While Field Productivity Emerges as the Fastest-Growing

Project Management dominates the Construction Software Market because of its crucial nature with regards to planning, scheduling, budgeting, resource allocation, documentation management, and project coordination. Construction businesses use project management software to increase their efficiency, decrease project delays, manage costs effectively, and collaborate with contractors, architects, engineers, and other stakeholders. The increased uptake of construction management processes via digital methods has made project management the largest revenue-earning software type.

Field Productivity is the fastest-growing type because construction businesses adopt digital methods of managing their activities in the field through mobile apps, real-time reporting, workforce management, machine management, and digital inspection. With the rising usage of mobile phones, tablets, Internet-of-Things, and cloud-based collaboration technologies, the field workers are able to increase their productivity and communication levels.

By Deployment Mode, Cloud Dominates the Construction Software Market and Registers the Fastest Growth

Cloud dominates the Construction Software Market because it offers scalable and cost-effective software solutions that do not require substantial on-site infrastructure. Cloud-based deployment facilitates collaboration in real time, monitoring of projects remotely, software upgrades automatically, and centralized data management in different construction sites. Digital construction processes, building information modeling, and mobile workforce management practices are continuously making cloud deployment more attractive for construction companies. Cloud is currently the most rapidly growing deployment model because construction companies prefer flexibility, accessibility from a distance, and fast deployment of software solutions.

By Organization Size, Large Enterprises Lead the Construction Software Market While Medium and Small Enterprises Grow at the Fastest Rate

Large Enterprise dominates the Construction Software Market because of its capacity to make heavy investments in digital transformation on an enterprise level as well as advanced construction management solutions. Large construction companies operate complicated and multifaceted projects across various locations and require software solutions for project planning, procurement, workforce management, accounting, and compliance. Larger budgets and more sophisticated infrastructure portfolios, along with automation and analytics initiatives, qualify large enterprises to be the top users of construction software.

Medium and Small Enterprise is the fastest-growing organization size because of affordable cloud-based construction software solutions that allow SMEs to manage projects more efficiently and collaborate better without spending a lot on initial software costs. The subscription model, easy implementation, and accessibility through mobile devices have attracted many SMEs to use construction software. Awareness of digital construction techniques, government infrastructure development projects, and increasing competition are driving this trend.

By Application, General Contractors Dominate the Construction Software Market While Building Owners Witness the Fastest Growth

General Contractors dominate the Construction Software Market because they manage all aspects of project planning, scheduling, budgeting, subcontractor coordination, procurement and project execution. The role played by General Contractors in managing multiple stakeholders, project timelines, and regulatory compliance generates strong demand for an integrated construction management software solution. More project complexity, digital collaboration and visibility requirements drive General Contractors to remain the biggest application segment.

Building Owners are the fastest-growing application segment due to the investments made by property developers and asset owners into construction software solutions in order to enhance their visibility and budget management, lifecycle planning and building operations. With more adoption of digital twins, Building Information Modeling (BIM), cloud collaboration solutions and data-driven decision making, Building Owners will have better control of their construction projects.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

79.30% |

|

Europe |

Germany |

24.20% |

|

Asia Pacific |

China |

30.15% |

|

Middle East & Africa |

UAE |

27.05% |

|

Latin America |

Brazil |

35.95% |

North America Construction Software Market Insights

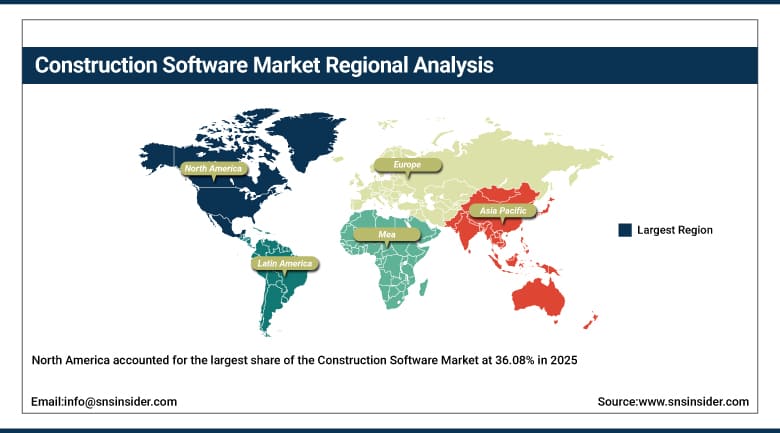

North America accounted for the largest share of the Construction Software Market at 36.08% in 2025, owing to high digitization level, advanced infrastructure, and presence of leading vendors in this region. It is this combination of leading vendors in the region and high technological adoption that has ensured that North America maintains the pole position in almost all construction software categories analyzed in this report.

The US alone accounts for about 79.30% of revenue generated in the region owing to high technological adoption, increasing digitization of projects management, and strict safety and compliance standards driving companies towards advanced software solutions. Canada also makes for an additional contributor for regional demand through rising construction technology adoption. Together, these factors are expected to ensure North America retains the largest addressable market share for construction software providers over the forecast period.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Construction Software Market Insights

Europe holds a meaningful share of the global construction software market, because of huge investments in infrastructure and increasing emphasis on the safety and sustainability of buildings, as well as greater use of Building Information Modeling in many of the major construction markets in Europe. Those countries where there is a lot of infrastructure and construction work have shown a steady demand for software related to project management and compliance.

Germany represents 24.20% of the total revenue of Europe and this is mainly due to Germany's significant construction and manufacturing sector. The UK and France contribute significantly to the demand and ongoing investments in infrastructure and sustainable buildings in Europe will continue to drive demand in the region for construction software.

Asia Pacific Construction Software Market Insights

Asia Pacific is the fastest-growing Construction Software Market, with a CAGR of approximately 10.68%, driven by rapid urbanization, infrastructure building, and investments in construction projects in the region's largest economies. The use of construction software solutions that improve productivity and resource management is increasing in various countries such as China, India, Japan, and Australia, and the growing number of initiatives on developing smart cities by government bodies continue to drive demand for construction software solutions.

China is the leader in the region, making up about 30.15% of regional revenues, which can be attributed to its enormous infrastructure and construction industries together with rapid technology adoption. Countries such as India, Japan, and South Korea generate significant additional demand, and growing awareness about the importance of safety compliance and quality management, together with extensive usage of BIM, AI, and IoT, continues to drive software adoption in the region.

MEA & Latin America Construction Software Market Insights

The Middle East & Africa and Latin America are experiencing consistent growth in the use of construction software due to the increasing investment in infrastructure and development in these regions. With the two regions developing major infrastructural projects, there is an increased need for construction software to help businesses in managing these large projects.

In the Middle East & Africa, the UAE accounts for about 27.05% of the total revenue from this region due to its plans on infrastructure development and the presence of construction firms which are advanced in technology. On the other hand, Saudi Arabia and South Africa play important roles in generating demand for construction software through the implementation of infrastructure plans. In Latin America, Brazil accounts for about 35.95% of the revenue generated in this region.

Growth Drivers: Rising project complexity and demand for digital collaboration

Demand for construction software is mostly determined by the growing complexity and large scale of construction projects worldwide. Organizations use digital solutions in order to enhance the process of project management and workflow management in general, and since these solutions provide companies with the chance to collaborate effectively in real time and make optimal use of resources without raising expenses, they play a considerable part in minimizing the level of uncertainty associated with the project that would otherwise be managed via spreadsheets, phone calls, and paperwork.

The need for quality and safety management solutions is another factor that enhances the above-mentioned trend and contributes to the growing demand for construction software, as the need for regulatory compliance and safety keeps driving firms to adopt technologies that enable them to manage risks while adhering to industry regulations. The growing geographic distribution and the number of participants involved in the process make the coordination issue, which software addresses, more challenging, thus making the industry's steady growth possible.

Restraints: High implementation costs and workforce digital literacy gaps

Construction is still very much a traditional and relationship-oriented business in many ways, and the cost of rolling out new software throughout the whole business organization, starting from the office workers to the people in the field, is a genuine obstacle to this process in many cases, especially among smaller companies that work with limited profit margins. The difficulty in training field workers who are not so comfortable with technology to use the new software becomes another obstacle on top of the initial cost of licensing and implementation of new software.

Integration issues with existing financial, scheduling, and old project management software represent another constraint because many construction companies have spent several years developing their processes based on old software that cannot simply be abandoned at once.

Opportunities: AI-driven project intelligence and expanding subcontractor adoption

Increasingly pervasive adoption of AI and IoT in construction software is a legitimate big opportunity for companies that go beyond mere scheduling and documentation towards advanced predictive project management. Those who provide means to detect possible delay, budget overruns, or safety issues before they arise will continue to gain an advantage over other players in the industry, and the AI-powered agents introduced by Procore during Groundbreak 2024 demonstrate the future of the category.

Another big opportunity comes with greater adoption by subcontractors and smaller businesses, as the availability of cloud-based products makes project management software more accessible than ever before, removing the barrier that has historically limited it to the most advanced general contractors only. With general contractors demanding their entire subcontractor network to be connected on the same platform, companies that will cater to the increasing number of less technologically savvy buyers have a legitimate chance to achieve success.

Recent Developments

-

2024: Procore introduced AI-driven agents and a connected resource management platform at Groundbreak 2024, enhancing labor, equipment, and materials coordination across construction sites.

-

2024: Autodesk launched Informed Design, a cloud-based solution that connects design and manufacturing workflows, enabling architects to use customizable, pre-defined building products for accurate results.

-

2024: Bentley Systems introduced an advanced open visualization platform for displaying infrastructure digital twins, transforming geospatial, engineering, and architectural data into immersive, hyper-realistic environments.

Construction Software Market Key Players

-

Oracle Corporation

-

Autodesk Inc.

-

Bentley Systems

-

Trimble Inc.

-

Sage Group plc

-

Microsoft Corporation

-

SAP SE

-

RIB Software SE

-

Jonas Construction Software

-

Buildertrend

-

Fieldwire

-

CMiC

-

Newforma

-

Heavy Construction Systems Specialists (HCSS)

-

Kahua

-

Intelvision, LLC

-

Vectorworks, Inc.

-

E-Builder, Inc.

Construction Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.91 Billion |

| Market Size by 2035 | USD 32.89 Billion |

| CAGR | CAGR of 9.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Project Management, Financial Management, Quality and Safety, Field Productivity, Others) • By Deployment Mode (Cloud, On-premise) • By Organization Size (Large Enterprise, Medium and Small Enterprise) • By Application (General Contractors, Building Owners, Architects and Engineers, Sub-Contractors, Specialty Contractors) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Procore Technologies, Oracle Corporation, Autodesk Inc., Bentley Systems, Trimble Inc., Sage Group plc, Microsoft Corporation, Constellation Software Inc., SAP SE, RIB Software SE, Jonas Construction Software, Buildertrend, Fieldwire, CMiC, Newforma, Heavy Construction Systems Specialists (HCSS), Kahua, Intelvision, LLC, Vectorworks, Inc., E-Builder, Inc. |

Frequently Asked Questions

The Construction Software Market is expected to grow at a CAGR of 9.80% from 2026 to 2035.

The Construction Software Market was valued at USD 12.91 Billion in 2025.

The major growth factor is increasing complexity and scale of construction projects worldwide, driving demand for digital tools to improve productivity, workflows, and project management.

The Project Management segment dominated the Construction Software Market in 2025.

North America dominated the Construction Software Market in 2025 with a 36.08% share of total global market revenue.

Get in Touch