Container Orchestration Market Report Scope:

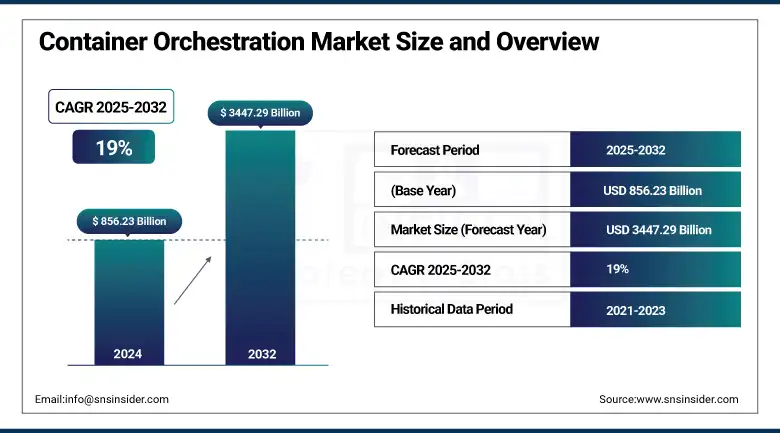

The Container Orchestration Market size was valued at USD 856.23 billion in 2024 and is projected to reach USD 3447.29 billion by 2032, growing at a CAGR of 19% from 2025 to 2032.

Its scale and digital transformation are indirectly impacting healthcare and IT infrastructure. With pharmaceutical firms and healthcare organisations increasingly using digital technologies to handle data-rich drug development and distribution, the demand for scalable, automated, and secure IT systems increases. This trend is driving demand for container orchestration platforms that help simplify deployment, enhance system reliability, and enable regulatory compliance across intricate, cloud-native healthcare landscapes.

To Get more information On Container Orchestration Market - Request Free Sample Report

According to resources 87% see significant value in leveraging cloud analytics for improved clinical trial design, pricing strategies, and fraud detection.

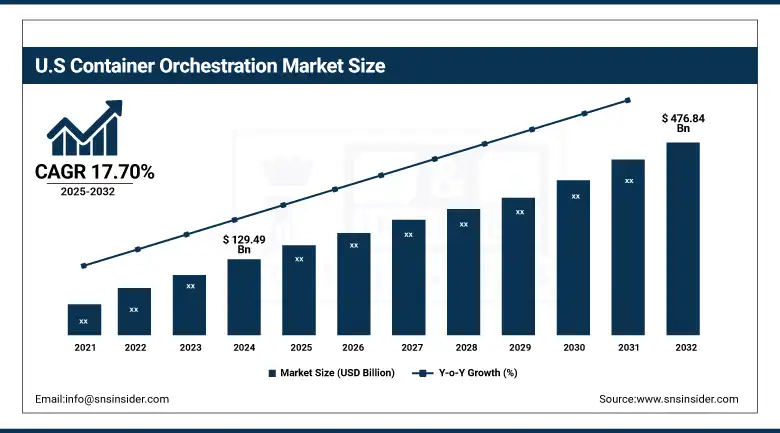

The U.S Container Orchestration Market reached USD 129.49 billion in 2024 and is expected to reach USD 476.84 billion by the end of 2032 at a CAGR of 17.70% from 2025 to 2032.

The strong growth is fueled by the extensive use of microservices, DevOps, and hybrid cloud strategies in large industries. The U.S. leads the world in terms of market share because of its sophisticated IT infrastructure, high rate of cloud adoption, and robust presence of major players like Google, Amazon, and Red Hat, which promotes ongoing innovation in orchestration technologies.

Container Orchestration Market Dynamics

Drivers

-

Surging demand for hybrid and multi-cloud deployments accelerates adoption of container orchestration platforms

The increasing complexity of IT landscapes has driven companies towards hybrid and multi-cloud strategies to enhance scalability, flexibility, and resilience. Container orchestration facilitates effective application management across such infrastructures, enhancing operational agility. Top platforms such as Kubernetes are being extended with AI-based automation for real-time resource provisioning. Recent innovation includes Google's integration of Gemini AI into GKE and Red Hat OpenShift's edge-oriented enhancements, signaling a wider industry trend towards smart orchestration in distributed environments.

Restraints

-

Security and compliance challenges in containerized ecosystems hinder widespread adoption of orchestration solutions

Though advantageous, containers present new threats with their distributed and dynamic nature. Workload security, identity and access management, and meeting worldwide regulations continue to be top challenges. Security and compliance challenges are often exacerbated by inconsistent visibility across diverse container orchestration tools used within enterprise ecosystems. With the advent of container security platforms like Aqua Security and Sysdig, lack of end-to-end, standardized security frameworks is hindering adoption and necessitating cautious approaches to implementation.

Opportunities

-

Integration with edge computing opens new frontiers for orchestrated application deployment across remote environments

Edge computing is picking up momentum with the increasing demand for edge processing of data. Edge container orchestration facilitates handling light payloads near the end-users, reducing latency and bandwidth consumption. Vendors now optimize platforms for edge deployments like K3s from Rancher for low-resource environments. This creates huge opportunities in manufacturing, healthcare, and logistics sectors where uptime and real-time insights are paramount. Integration with edge computing is expanding the capabilities of container orchestration technologies by enabling lightweight deployments in latency-sensitive environments.

Challenges

-

Lack of skilled professionals restricts the effective implementation of advanced orchestration architectures

Container orchestration platform deployment and management known for its specialized skills in DevOps, networking, and cloud-native technologies. A talent shortage is an ongoing issue, though. Most organizations are unable to scale their container projects because of inadequate in-house talent. Efforts to provide training are in overdrive, with entities such as CNCF and cloud vendors developing certifications and learning platforms.

Container Orchestration Market Segment Analysis

By Component

The platform segment accounted a 56.27% revenue share in 2024 due to the rampant adoption of Kubernetes and other orchestration platforms. Businesses are trusting these solutions for simplified container management, automated deployments, and improved scalability. Container orchestration market companies such as Google, AWS, and Red Hat are introducing advanced features that support enterprise-level scalability and security. These features add to platform supremacy, particularly in enterprise use cases where scalability and reliability matter.

The services segment is expanding at the fastest CAGR of 20.26% during the forecasting period as there is rising demand for managed services, consulting, and training. Organizations are collaborating with vendors such as Accenture, IBM, and Capgemini for smooth orchestration deployment and lifecycle management. With the increased complexity in orchestration solutions, the importance of expert-driven services in ensuring successful implementation, ongoing optimization, and cost management becomes more pivotal, particularly for digitally transforming businesses.

By Organization Size

Large enterprises held a 46.42% revenue share in 2024, utilizing container orchestration to streamline high-scale deployments across hybrid and multi-cloud environments. Their emphasis on microservices-based architectures, DevOps pipelines, and real-time analytics necessitates scalable and fault-tolerant orchestration platforms. Industry giants Microsoft and IBM continue to fine-tune their products to these requirements, including improved automation, policy management, and integration with enterprise-level security frameworks ensuring their place in large business environments.

SMEs are experiencing fastest growth at a CAGR of 18.58% due to growing adoption of streamlined orchestration solutions and cloud services. The cost-friendly distributions of Docker Swarm and K3s provide an economic on-ramp for these organizations. Vendors aim at this space with cost-friendly, simple-to-deploy offerings, and managed orchestration services reduce the technical hurdle. These trends enable SMEs to enhance application deployment responsiveness, lower infrastructure expenses, and stay ahead in dynamic markets.

By Vertical

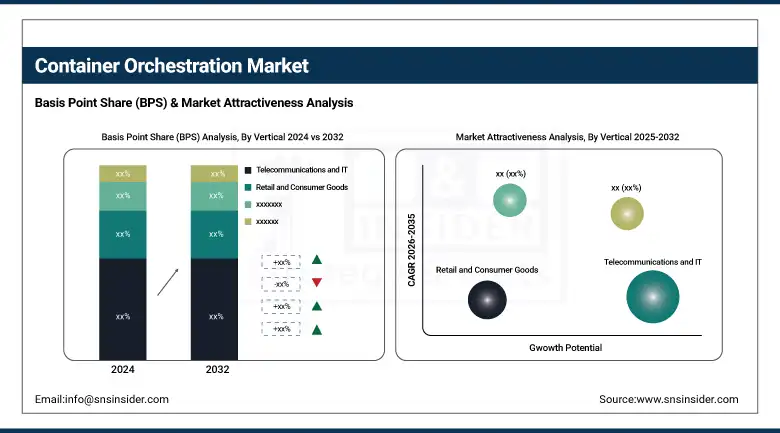

Telecom and IT accounted for a 19.98% share in 2024, led by the trend toward network function virtualization and 5G rollout. Orchestration platforms enable fast service provisioning, minimize operational overhead, and enhance network agility. Vendors such as Ericsson and Cisco are integrating orchestration capabilities into telecom infrastructure offerings. With data-intensive workloads and continuous innovation cycles, this industry requires agile deployment mechanisms, and hence, orchestration technologies are pivotal to digital network transformation.

The retail and consumer goods industry is expected to advance at a CAGR of 20.47%, indicative of increasing investment in e-commerce sites, automated supply chains, and customized experiences. Orchestration facilitates dynamic scaling of applications to manage seasonal traffic and accommodates integration with customer analytics solutions. Retailers such as Walmart and Target are utilizing containerized microservices for omnichannel capabilities.

Container Orchestration Market Regional Analysis

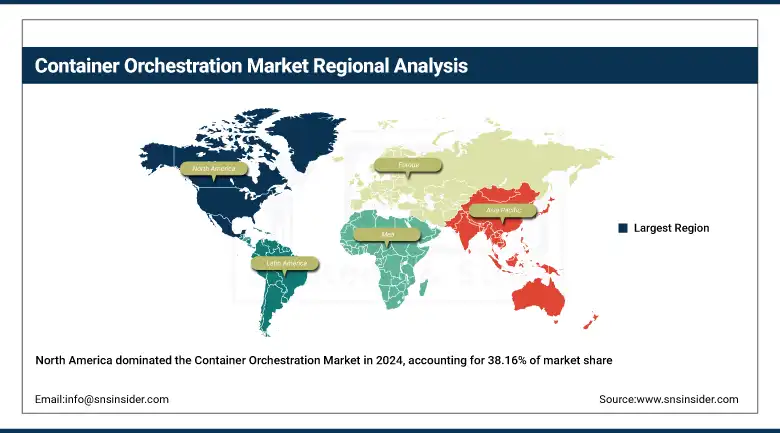

North America held a 38.16% container orchestration market share in 2024 due to the region's dominance in cloud adoption and digital innovation. The U.S. and Canadian enterprises are quickly adopting DevOps and microservices patterns, backed by robust cloud-native ecosystems. Key players like AWS, Microsoft Azure, and Google Cloud are headquartered here and keep upgrading their orchestration services with AI and security-centric features. Robust R&D activity and enterprise IT investments further support the region's dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States dominates the region because it has a superior cloud infrastructure, early Kubernetes adoption, and leadership in AI-driven orchestration platforms via AWS and Google Cloud.

Europe is observing steady growth in container orchestration fueled by industry-wide digital transformation, robust data regulations, and rising cloud investment. Western European nations are adopting orchestration as part of cybersecurity and edge computing to provide safe, scalable deployment of applications, particularly in financial services, healthcare, and governments.

Germany is leading the region through high enterprise cloud adoption, a rise in the number of containerized projects across automotive and manufacturing, and alliances with global orchestration platform providers.

Asia Pacific is the fastest growing region in the market with 19.89% CAGR, for container orchestration based on swift digital transformation, modernization of SMEs, and high demand for scalable cloud-native applications. Nations such as India, China, and Australia are investing heavily in hybrid cloud and microservices-based development environments, and this contributes immensely to container orchestration adoption.

China leads through strong cloud infrastructure, huge digital innovation across industries, and inorganic investment by local tech players such as Alibaba Cloud and Tencent Cloud in container orchestration technology.

Middle East & Africa and Latin America are experiencing increasing adoption of container orchestration, fueled by digital government programs, smart city initiatives, cloud infrastructure growth, and modernization in industries such as banking, logistics, oil & gas, and public services.

Key Players

The major key players of Container Orchestration Market are, Kubernetes, Docker, Red Hat, AWS, Google, Microsoft, Rancher Labs, Hashicorp, Cisco, Oracle and others.

Recent Developments

-

In April 2025, researchers introduced KubeFence, a security framework that enhances Kubernetes by reducing its attack surface through fine-grained API filtering, outperforming traditional RBAC in threat prevention.

-

In January 2025, Microsoft announced plans to invest approximately $80 billion in AI-enabled data centers for fiscal year 2025, with over half allocated to U.S. projects. This investment aimed to bolster the company's AI infrastructure to meet the growing demand for AI and cloud-based applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 856.23 Million |

| Market Size by 2032 | USD 3447.29 Million |

| CAGR | CAGR of 19.0% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | By Component (Platform, Services) By Organization Size (Small and Medium-sized Enterprises (SMEs), Large Enterprises) By Vertical (Telecommunications and IT, BFSI, Government and Public Sector, Healthcare, Retail and Consumer Goods, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Kubernetes, Docker, Red Hat, AWS, Google, Microsoft, Rancher Labs, Hashicorp, Cisco, Oracle |

Frequently Asked Questions

Healthcare and pharmaceuticals are key drivers, needing secure, scalable systems to manage complex, data-rich drug development and distribution environments.

North America held a 38.16% market share in 2024, driven by early Kubernetes adoption and dominant cloud providers.

The sector is projected to grow at a CAGR of 20.47%, due to investments in e-commerce, supply chain automation, and omnichannel experiences.

The platform segment led with 56.27% revenue share in 2024, due to Kubernetes adoption and enterprise demand for automated container management.

The market was valued at USD 856.23 billion in 2024, with strong growth expected due to increasing cloud-native and hybrid IT deployments.

Get in Touch