Core Banking Software Market Report Scope & Overview:

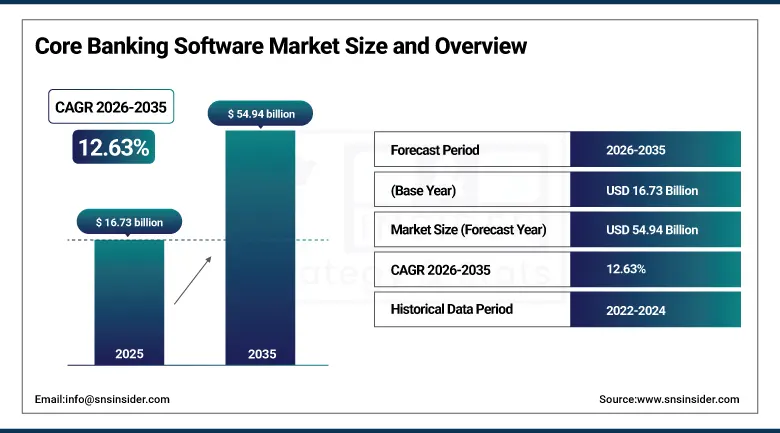

The Core Banking Software Market was valued at USD 16.73 billion in 2025 and is expected to reach USD 54.94 billion by 2035, growing at a CAGR of 12.63% from 2026-2035.

The core banking software market is anticipated to witness significant growth in the coming years, considering the rising trend of digitalization in the banking and finance industry worldwide. The growing demand for instant transaction procedures, mobile banking, and cloud banking software is responsible for the growth in the demand for software. Financial institutions have realized the importance of automation, artificial intelligence, and security software technology to enhance efficiency and experience. Moreover, there has been an increase in collaboration within the fintech industry and the adoption of digital payment solutions.

JPMorgan Chase revealed that it increased technology investments to nearly USD 18 billion in 2025, deploying more than 175 AI use cases across banking operations. The bank reported that AI-driven systems reduced servicing costs by almost 30% and improved customer engagement by 25%, demonstrating the increasing role of intelligent automation in modern banking infrastructure.

Market Size and Forecast

-

Market Size 2026E: USD 18.84 Billion

-

Market Size 2035: USD 54.94 Billion

-

CAGR 2026-2035: 12.63%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Core Banking Software Market - Request Free Sample Report

Core Banking Software Market Trends

-

Rising digital transformation initiatives in the banking sector are driving the core banking software market.

-

Growing adoption of cloud-based banking platforms and omnichannel banking services is boosting market growth.

-

Expansion of digital payments, mobile banking, and real-time transaction processing is fueling software deployment.

-

Increasing focus on operational efficiency, customer experience, and regulatory compliance is shaping adoption trends.

-

Advancements in AI, automation, API integration, and analytics are enhancing banking functionality and scalability.

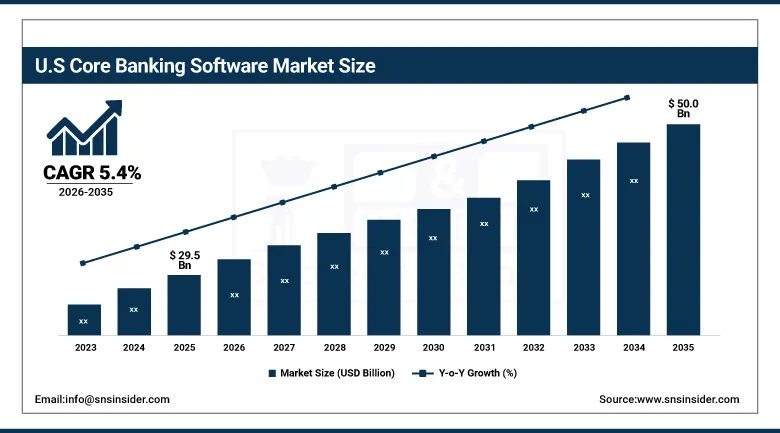

The U.S. Core Banking Software Market Size Outlook

The U.S. Core Banking Software Market was valued at USD 29.5 billion in 2025 and is expected to reach USD 50 billion by 2035, growing at a CAGR of 5.4% from 2026-2035.

The United States core banking software market is expanding as a result of the rising use of digital banking software, cloud-based financial services, and automated transaction management systems. Banks have made investments in high-end security, artificial intelligence analytics, and real-time payment services.

Core Banking Software Market Segment Analysis

-

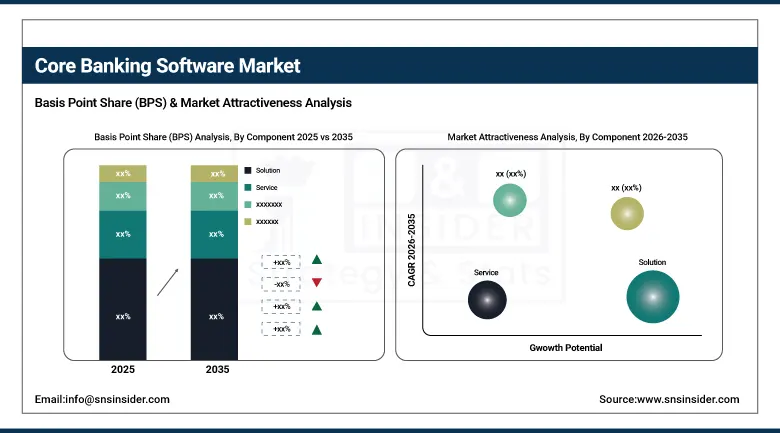

By Component, solution segment dominated the core banking software market in 2025 with around 70% share; services segment fastest growing.

-

By Deployment, on-premise segment dominated the core banking software market in 2025 with around 59% share; cloud segment fastest growing.

-

By End Use, banks segment dominated the core banking software market in 2025 with around 63% share; financial institutions segment fastest growing.

-

By Banking Type, large banks (greater than usd 30 billion in assets) segment dominated the core banking software market in 2025 with around 38% share; community banks (less than usd 5 billion in assets) segment fastest growing.

By Component, solution segment dominates the market, services segment expected to grow fastest

The solution segment held a dominant position in the core banking software market in 2025 owing to the growing need for integrated banking software to manage accounts, process transactions, perform customer relationship management, process loans, and facilitate digital banking activities. Banks have been implementing advanced core banking solutions in order to streamline their operations and enhance the overall customer experience as well as facilitate real-time transactions. There has been a significant emphasis on banking automation, regulatory compliance, and digitalization trends, which have helped the solution segment dominate the market.

The services segment is the fastest-growing segment in the core banking software market due to the increasing requirement for consulting, implementation, integration, maintenance, and managed services related to banking software. The growing need for technical expertise to upgrade the existing legacy infrastructure and deploy advanced banking technology has helped propel the demand for services. Cloud-based banking systems, cybersecurity solutions, and regular software updates have been driving the demand for services.

By Deployment, on-premise segment dominates the market, cloud segment expected to grow fastest

The on-premise segment is expected to lead the market in 2025 owing to the preference of many financial institutions for retaining control over their customers' data, security of transactions, and regulatory compliance mechanisms. Major banks heavily depended on the on-premise model for ensuring operational reliability, customized system integration, and improved cybersecurity management. Legacy IT infrastructure investments and issues related to data privacy, risk, and compliance also fueled the growth of the on-premise core banking software deployment segment.

The cloud segment represents the fastest-growing segment in the market owing to rising demand for scalable and flexible banking infrastructure solutions. Increasing adoption of cloud technology by financial institutions is driven by the need for providing digital banking services, remote access, software updates, and fast data processing capabilities. Rising importance of agility and cost reduction in infrastructure investments are key reasons for the growing popularity of cloud-based banking software solutions among financial institutions.

By End Use, banks segment dominates the market, financial institutions segment expected to grow fastest

Banks held the largest market share in the market in 2025, owing to extensive use of digital banking platforms, transaction management systems, and customer-oriented financial solutions by commercial and retail banks. The increasing adoption of core banking technology systems by banks helped in improving their operations, ensuring enhanced security, and providing efficient multi-channel banking solutions. Growing customer preferences for instant financial transactions and customized banking services have further fueled the growth of the banks segment in the market.

The financial institutions segment is the fastest-growing segment in the core banking software market, as there is an increase in digitalization efforts by credit unions, non-banking financial companies, cooperative financial organizations, and microfinance institutions. These financial institutions are actively adopting advanced banking platforms in order to provide better customer services and automate their financial processes. Increasing demand for flexible financial solutions, regulatory compliance management, and cloud-based banking solutions is expected to drive rapid adoption in the coming years.

By Banking Type, large banks (greater than USD 30 billion in assets) segment dominates the market, community banks (less than USD 5 billion in assets) segment expected to grow fastest

Large banks (greater than USD 30 billion in assets) segment led the market in 2025 owing to the fact that large banking organizations have a large number of customers, transaction volume, and heavy investment in advanced digital banking solutions. Large banking organizations have been increasingly implementing sophisticated core banking software to facilitate real-time processing, multichannel banking solutions, fraud detection, and regulation. Financial strength and operational efficiency and security measures were the main factors contributing to the success of this segment.

Community banks (less than USD 5 billion in assets) segment is expected to grow at the highest rate in the core banking software market due to rising adoption of cost-effective digital banking solutions by community banks. These banks are looking for new-age technologies to enhance their customer experience and offer online banking services as well as to compete with larger banks. The availability of cloud-based platforms and cost-effective banking software is expected to drive the growth of this segment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

92.7% |

|

Europe |

United Kingdom |

25.9% |

|

Asia Pacific |

Australia |

8.6% |

|

Middle East & Africa |

UAE |

18.1% |

|

Latin America |

Brazil |

53.4% |

North America Core Banking Software Market Insights

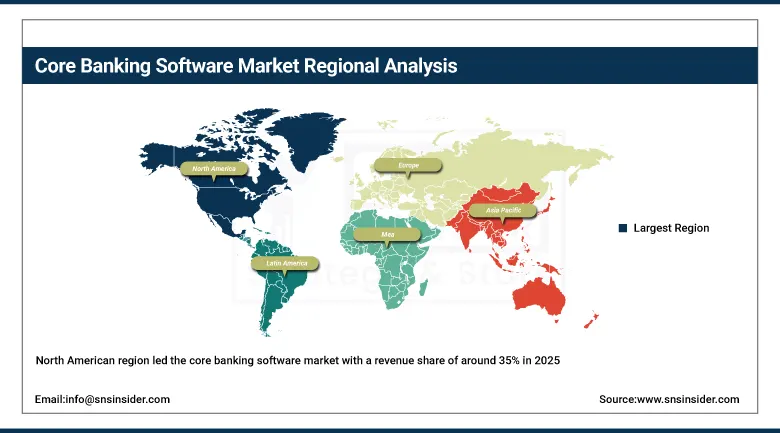

The North American region led the core banking software market with a revenue share of around 35% in 2025 owing to the rapid digital transformation witnessed by banking firms and rising usage of financial technologies. There is substantial investment being made by banks in the region in cloud-based banking platforms, automation technology, and AI-driven financial management software. The presence of prominent software vendors and banking infrastructure contributes to the dominance of the region. Furthermore, there is a high demand for secure real-time transaction processing, digital banking, and regulatory compliance software.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Core Banking Software Market Insights

The Europe core banking software market is experiencing consistent growth due to the increased implementation of digital banking technology and modernization of traditional banking software. Various financial institutions operating within the region have been integrating cloud core banking solutions, automation software, and cybersecurity technologies to enhance their operations and service delivery. Robust regulatory policies and the need for real-time transactions are other factors that are fostering growth within the market. Moreover, collaborations between banks and fintech firms are driving innovation within the digital financial services sector in Europe.

Asia Pacific Core Banking Software Market Insights

The Asia Pacific is projected to record the highest CAGR of 14.30% in the core banking software market owing to increasing digitization within the banking and financial sector. Adoption of mobile banking, cloud banking solutions, and real-time payments has been increasing rapidly, driving market growth in the region. The focus on development of advanced banking technology by governments and financial institutions is expected to drive the growth of the market. Growing internet penetration, development of fintech, and increasing demand for secure online banking solutions from the unbanked population will offer growth opportunities for core banking software vendors.

Middle East & Africa and Latin America Core Banking Software Market Insights

The Middle East & Africa and Latin America core banking software market are showing steady growth owing to the increased rate of digital transformation in financial institutions and growing acceptance of online banking services. Banks in these regions are upgrading their existing technology infrastructure in order to enhance efficiency, customer engagement, and security of transactions. The development of the fintech ecosystem, higher usage of smartphones, and greater availability of the internet are some of the factors that are driving digital banking services.

Market Dynamics

Growth Drivers:Increasing adoption of cloud-based banking platforms and automation technologies is strengthening digital transformation across financial institutions worldwide rapidly

The banking industry is increasingly adopting cloud-based core banking systems that enhance scalability, flexibility, and efficiency. Automation tools used in conjunction with core banking software enable banks to operate efficiently, minimize mistakes, and manage regulatory compliance effectively. The increasing need for data analytics, AI-driven customer insight, and automation in financial transactions is fueling efforts to modernize software applications within the banking industry. In addition, there is an increasing emphasis on cybersecurity measures and transaction monitoring tools for safe banking operations through the internet. Moreover, collaboration between fintech firms and banks has made it necessary for banks to adopt advanced banking technologies.

In 2025, Infosys Finacle announced that Uniting Financial Services Australia successfully migrated to its cloud-based digital banking suite in less than five months, highlighting rising adoption of SaaS core banking platforms and real-time banking capabilities.

Restraints:Rising cybersecurity risks and strict regulatory compliance requirements are creating operational challenges for modern core banking software providers globally

The core banking software systems deal with confidential data of their customers and banks, and hence, have become an easy target for cyber threats. The cases of ransomware, phishing, and unauthorized financial access are becoming more common nowadays and creating a cause for concern for banking software security. Financial institutions need to adhere to strict regulations concerning data protection, transaction monitoring, and cloud banking, thus adding complexity to operations. Changes in regulations lead to frequent updates in software, which results in substantial maintenance costs for the bank and software provider. Moreover, customer concerns about privacy and transaction safety have led many financial institutions to adopt cloud banking software cautiously.

Opportunities:Growing integration of artificial intelligence and advanced analytics technologies is expanding innovation potential within next-generation digital banking platforms globally

The financial services industry continues to adopt AI technologies, such as machine learning and analytics, in core banking systems to enhance the customer experience and operational intelligence. AI-enabled banking solutions help in detecting fraud, conducting predictive financial analysis, providing personalized banking suggestions, and offering automated customer services. The growing need for data-driven and intelligent risk management systems is pushing banks towards innovation and development of new technologies within the banking software industry. Additionally, banking solutions providers are looking at incorporating blockchain technology, open banking, and banking via APIs into their offerings. Such technological developments will result in many growth opportunities for core banking solutions.

Plaid stated that its platform now connects over 10,000 financial institutions and is used by one in two Americans for digital financial connectivity. The company also emphasized rising investments in AI-powered fraud prevention and secure payment infrastructure as digital banking adoption expands globally.

Recent Developments:

-

2025: nCino expanded intelligent banking workflows through AI-powered lending and onboarding automation integrated with cloud-based banking systems. The platform improved operational efficiency, compliance management, and customer engagement for financial institutions adopting digital-first banking strategies.

-

2025: nCino strengthened its portfolio by acquiring Sandbox Banking, adding an Integration Platform as a Service (iPaaS) to enhance interoperability, connectivity, and efficiency across banking systems and customer journeys.

-

2024: Allied Banking Corporation (Hong Kong) migrated from Finastra’s Equation to its cloud-first Essence core banking system, modernizing operations and launching Retail Analytics for greater efficiency.

Core Banking Software Market Key Players are:

-

Finastra

-

FIS

-

Fiserv, Inc.

-

Tata Consultancy Services (TCS)

-

Mambu

-

Avaloq

-

EdgeVerve Systems (Finacle)

-

Backbase

-

nCino

-

Forbis

-

Securepaymentz

-

Novatti

-

Capital Banking Solutions

-

Infosys Limited

-

Jack Henry & Associates, Inc.

-

Oracle Corporation

-

Temenos Group

-

Unisys

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 16.73 Billion |

| Market Size by 2035 | USD 54.94 Billion |

| CAGR | CAGR of 12.63% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solution, Service) • By Deployment (Cloud, On-premise) • By End Use (Banks, Financial Institutions, Others) • By Banking Type (Large Banks – Greater than USD 30 billion in Assets, Midsize Banks – USD 10 billion to USD 30 billion in Assets, Small Banks – USD 5 billion to USD 10 billion in Assets, Community Banks – Less than USD 5 billion in Assets, Credit Unions) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Capgemini, Finastra, FIS, Fiserv, Inc., HCL Technologies Limited, Tata Consultancy Services (TCS), Mambu, Avaloq, EdgeVerve Systems (Finacle), Backbase, nCino, Forbis, Securepaymentz, Novatti, Capital Banking Solutions, Infosys Limited, Jack Henry & Associates, Inc., Oracle Corporation, Temenos Group, Unisys |

Frequently Asked Questions

North America dominated the Core Banking Software Market in 2025.

The Solution segment dominated the Core Banking Software Market in 2025.

Increasing adoption of cloud-based banking platforms and automation technologies is strengthening digital transformation across financial institutions worldwide rapidly.

The Core Banking Software Market was valued at USD 16.73billion in 2025.

The Core Banking Software Market is expected to grow at a CAGR of 12.63% from 2026 to 2035.

Get in Touch