Corporate Bond Market Report Scope & Overview:

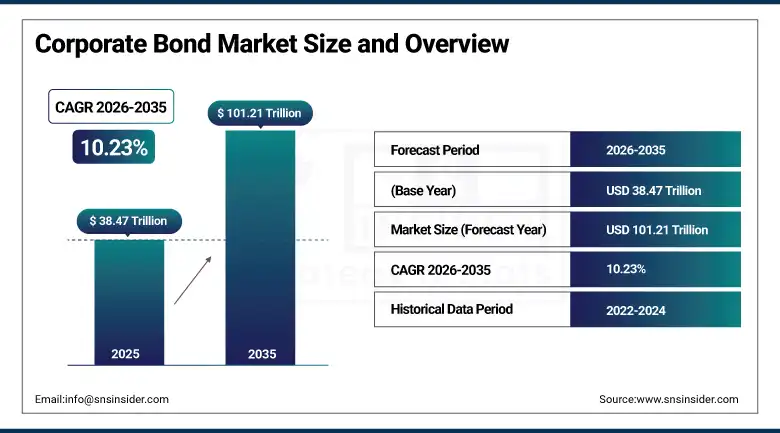

The Corporate Bond Market was valued at USD 38.47 Trillion in 2025 and is expected to reach USD 101.21 Trillion by 2035, growing at a CAGR of 10.23% from 2026–2035.

The global corporate bond market is going through a period of structural growth as the usage of capital markets for the purpose of financing operations and acquisitions grows rapidly across the globe. In 2023, corporate bond issuance was responsible for funding over 40% of total expenditures by non-financial companies globally, and the participation by institutional and individual investors has increased consistently due to improved transparency within the market environment and the development of electronic trading platforms which facilitate the efficient functioning of the secondary market. The enduring popularity of the corporate bond market can be attributed to the status of bonds as risk-reward hybrid products situated between government and equity securities.

Goldman Sachs published commentary in 2024 indicating that borrowers could issue USD 1.5 trillion or more of U.S.-dollar corporate bonds in 2025, reflecting the investment bank’s expectation of continued strong issuance supported by corporate refinancing demand, acquisition financing, and the favourable spread environment that attracted institutional investors seeking yield above government securities. The projection proved prescient as 2025 issuance volumes affirmed the structural strength of corporate bond market activity.

Market Size and Forecast

-

Market Size in 2026E: USD 42.41 Trillion

-

Market Size by 2035: USD 101.21 Trillion

-

CAGR: 10.23% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

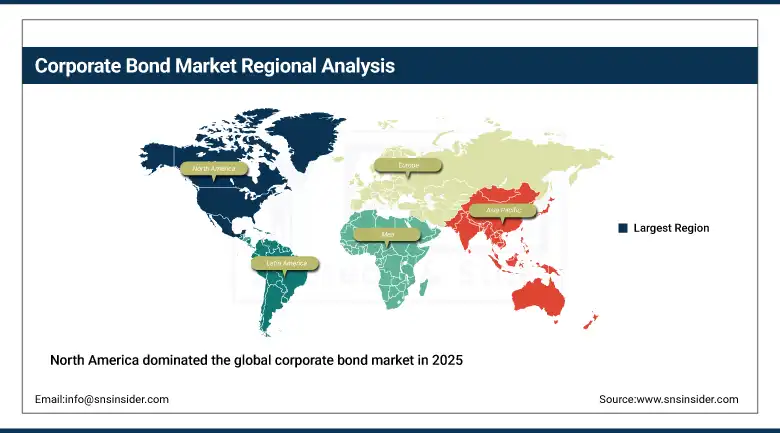

Largest Region: North America

To Get more information On Corporate Bond Market - Request Free Sample Report

Corporate Bond Market Trends

-

Rising ESG and green bond issuance is reshaping the corporate bond market as institutional investors apply sustainability criteria to fixed-income portfolio allocation and corporations issue labelled bonds to finance decarbonisation and transition investments.

-

Growing retail investor participation through digital bond platforms, fractional ownership models, and exchange-listed bond products is democratising corporate bond market access beyond institutional investors for the first time at commercial scale.

-

Increasing adoption of blockchain-based bond issuance and settlement infrastructure is reducing settlement risk, lowering transaction costs, and improving post-trade transparency across both primary issuance and secondary market trading workflows.

-

Rising demand for floating rate notes and variable coupon structures is attracting issuers and investors seeking instruments that naturally hedge against interest rate volatility in uncertain central bank policy environments.

-

Expanding Asia Pacific corporate bond issuance, particularly in China, India, and Southeast Asia, is creating new regional market depth that progressively reduces reliance on U.S. dollar-denominated bond markets for corporate financing in these economies.

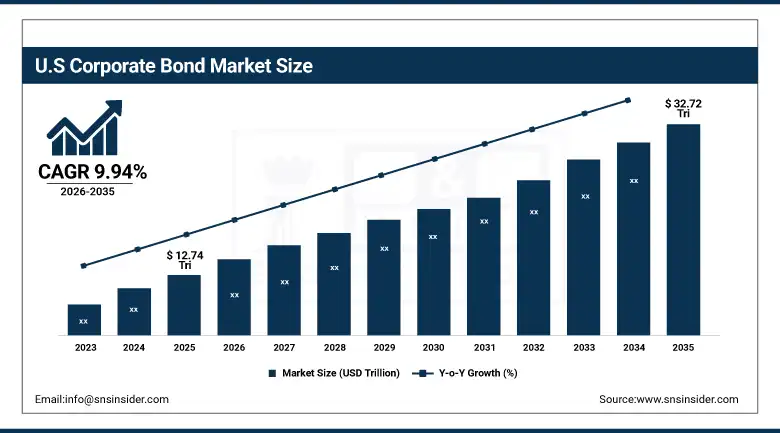

U.S. Corporate Bond Market Outlook

The U.S. Corporate Bond Market was valued at approximately USD 12.74 Trillion in 2025 and is expected to reach approximately USD 32.72 Trillion by 2035, growing at a CAGR of approximately 9.94%.

The United States operates the world’s largest and most liquid corporate bond market, whose deep institutional investor base, transparent disclosure requirements under SEC regulation, and active secondary market trading infrastructure collectively create the most commercially accessible corporate debt financing environment of any national market. Investment-grade issuance dominates total volume, with strong institutional demand from pension funds, insurance companies, and asset managers whose liability-matching and yield-seeking mandates sustain consistent corporate bond absorption at every credit quality tier.

Citigroup and JPMorgan Chase each led record-volume investment-grade bond underwriting syndicates in early 2025, collectively arranging the largest quarterly primary market issuance in U.S. corporate bond history as corporations front-loaded borrowing ahead of anticipated rate and spread volatility later in the year, validating the structural strength of institutional demand for investment-grade corporate fixed income at current yield levels.

Corporate Bond Market Segment Analysis

-

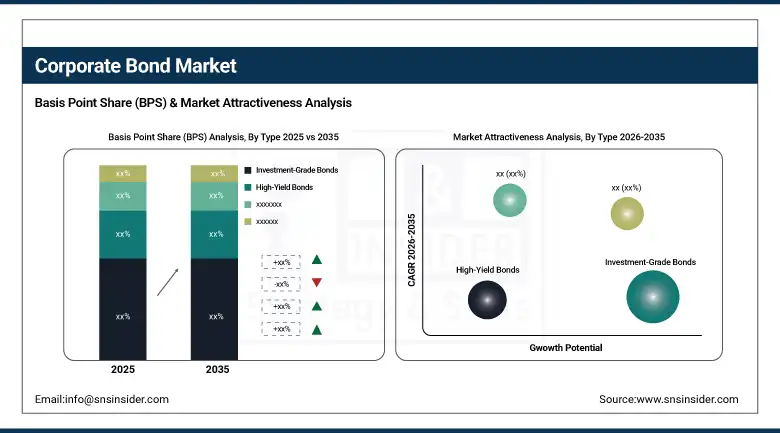

By Type, the Investment-Grade Bonds segment dominated the Corporate Bond Market in 2025, while the High-Yield Bonds segment is the fastest growing during 2026–2035.

-

By Issuer, the Financial Institutions segment dominated the Corporate Bond Market in 2025, while the Non-Financial Corporates segment is the fastest growing.

-

By Investor, the Institutional Investors segment dominated the Corporate Bond Market in 2025, while Retail Investors are the fastest-growing segment.

-

By Maturity, the Medium-Term segment dominated the Corporate Bond Market in 2025, while the Long-Term segment is the fastest growing.

By Type, investment-grade dominates, high-yield grows fastest

Investment-grade bonds retained the dominant type position in the corporate bond market in 2025. Their commercial primacy reflects the fundamental investment logic of the institutional investor base whose fiduciary mandates, capital adequacy requirements, and liability management frameworks systematically allocate a substantial and regulated proportion of assets to investment-grade fixed income. Pension funds with defined benefit obligations, insurance companies managing duration-matched liability portfolios, and sovereign wealth funds seeking stable income returns collectively generate investment-grade bond demand that is structurally anchored in institutional portfolio construction requirements rather than discretionary investment preference.

High-yield bonds are the fastest-growing type in the corporate bond market, driven by the yield-seeking environment that institutional investors face when government and investment-grade spreads compress to levels that make high-yield’s excess return attractive relative to its credit risk on a risk-adjusted basis.

By Investor, institutional dominates, retail grows fastest

Institutional investors retained the dominant investor position in the corporate bond market in 2025. The commercial logic of institutional dominance is grounded in the structural alignment between corporate bonds’ income, duration, and credit characteristics and the portfolio management requirements of pension funds, insurance companies, sovereign wealth funds, and mutual funds whose combined assets under management represent the world’s largest pool of investable capital. BlackRock, PIMCO, Vanguard, and Fidelity collectively manage trillions of fixed-income assets whose corporate bond allocation sustains primary market demand at every credit quality tier. Institutional investors’ market making participation in secondary trading simultaneously provides the liquidity that supports price discovery and enables issuers to access capital markets with confidence that their bonds will trade actively post-issuance.

Retail investors are the fastest-growing investor segment in the corporate bond market, driven by the progressive democratisation of bond market access through digital investment platforms, exchange-listed bond products, and fractional ownership structures that enable individual investors to build diversified fixed-income portfolios without the large minimum investment denominations that institutional primary market participation historically required.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

48.6% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Corporate Bond Market Insights

North America dominated the global corporate bond market in 2025, driven by the United States’ position as the world’s largest and most liquid corporate debt market whose combination of the broadest issuer universe, deepest institutional investor base, and most active secondary trading infrastructure makes it the reference market for global fixed-income pricing and issuance benchmarking. North American dominance is reinforced by the U.S. dollar’s reserve currency status, which enables American corporations to issue in their home currency at terms that non-U.S. issuers accessing dollar markets cannot match.

Canada contributes approximately 16.6% of North American volumes through its active corporate bond market whose financial services, energy, and resources sector issuers access both domestic CAD-denominated and cross-border USD markets for capital raising, supported by sophisticated institutional investor demand from major Canadian pension funds whose fixed-income allocation practices sustain consistent primary market absorption.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Corporate Bond Market Insights

Europe is the world’s second-largest corporate bond market, characterised by the co-existence of euro-denominated investment-grade issuance that benefits from ECB monetary policy support and a rapidly growing sustainable finance bond segment whose green, social, and sustainability-linked bond issuance is the most commercially developed of any regional market.

Germany accounts for approximately 22.3% of European corporate bond issuance as the region’s largest national market, driven by the capital markets financing requirements of its large industrial enterprises, automotive OEMs, and financial sector whose combined bond issuance programmes represent the most commercially significant national European corporate debt market.

Asia Pacific Corporate Bond Market Insights

Asia Pacific is the fastest-growing regional corporate bond market, driven by the financial market liberalisation and deepening of China’s onshore bond market, India’s progressive capital market development, and Southeast Asian economies’ growing corporate debt financing capacity as their financial systems mature and domestic institutional investor bases expand.

China accounts for approximately 48.6% of Asia Pacific corporate bond volumes through its position as the world’s second-largest bond market by volume, where ongoing financial market reforms are progressively opening the market to international investors and enabling Chinese corporations to access both domestic and international capital markets for financing.

MEA & Latin America Corporate Bond Market Insights

The Middle East and Africa and Latin America are growing corporate bond markets where economic diversification investment, regional capital market development initiatives, and the progressive inclusion of regional bonds in global indices are creating new issuance and investor participation. Saudi Arabia leads MEA revenues at approximately 31.2% of the regional total through Vision 2030’s extraordinary capital market development investment, Saudi Aramco and Saudi Basic Industries’ large-scale international bond issuance programmes, and the Tadawul’s progressive capital market reforms that are attracting international investors to Saudi corporate debt.

Brazil leads Latin American corporate bond volumes at approximately 44.2% of the regional total through its large and commercially sophisticated capital markets whose real-denominated corporate debenture market and external USD bond issuance programmes collectively sustain the region’s most active corporate debt market, supported by the substantial domestic institutional investor base of Brazilian pension funds and insurance companies whose fixed-income allocation requirements create consistent primary market demand.

Market Dynamics

Growth Drivers: Rising global capital expenditure creating corporate financing demand, institutional investor fixed-income allocation sustaining primary market absorption

The structural growth driver for the corporate bond market is the compounding growth of global corporate capital expenditure and refinancing requirements whose scale progressively exceeds what bank lending alone can fund at the cost efficiency that capital market bond issuance achieves for investment-grade issuers. As corporations in technology, energy transition, healthcare, and infrastructure execute investment programmes whose multi-year funding requirements benefit from long-term bond market capital, the primary issuance volume of the corporate bond market grows proportionally with the ambition and scale of corporate investment cycles globally.

The institutional investor community’s structural fixed-income allocation requirements create a demand floor that sustains corporate bond issuance through economic cycle variations. Pension funds with defined benefit obligations, insurance companies managing liability portfolios, and sovereign wealth funds seeking stable income collectively generate demand for investment-grade corporate debt that is largely independent of market sentiment cycles, as their mandate-driven allocation requirements must be satisfied across market conditions.

Restraints: Rising interest rates compressing bond valuations, credit spread volatility creating issuance window uncertainty, and default cycle risk in high-yield market creating investor caution

Interest rate volatility is the most commercially significant restraint on corporate bond market activity, as rising rates simultaneously reduce the mark-to-market value of existing bond portfolios, increasing unrealised losses for institutional holders, and elevate the borrowing cost that new issuers face when accessing the primary market. Corporate treasury teams manage this constraint by concentrating issuance in favourable rate windows and adjusting deal size and maturity profile to market conditions, creating volume concentration in low-rate environments and issuance hesitation when rate uncertainty is elevated.

Credit spread widening episodes, triggered by macroeconomic deterioration or sector-specific credit concerns, create issuance windows that disadvantage corporate borrowers through higher all-in financing costs and investor pricing expectations that reduce deal economics relative to tighter spread periods. High-yield issuers are disproportionately affected by spread volatility, as their already elevated credit risk creates larger spread movements that can temporarily close primary market access for speculative-grade borrowers whose refinancing timelines cannot accommodate extended market inaccessibility periods.

Opportunities: Digital bond issuance platforms reducing friction, green and sustainability bond premium attracting ESG investor capital, and emerging market corporate bond index inclusion expanding global investor reach

Digital bond issuance platforms, including blockchain-based distributed ledger technology and electronic book-building systems, are progressively reducing the transaction cost, settlement time, and minimum issuance size that have historically limited corporate bond market access to large investment-grade issuers. As digital infrastructure matures, the accessible issuer universe expands toward mid-market corporations whose financing needs can be served by smaller, more frequent bond issuances whose economics are improved by lower underwriting overhead and automated settlement workflows.

ESG bond market development represents a commercially significant opportunity expansion as the premium pricing that green, social, and sustainability-linked bonds achieve over conventional equivalents in the primary market creates a direct financial incentive for corporate issuers to invest in the use-of-proceeds frameworks, impact reporting, and sustainability-linked covenant structures that qualify bonds for ESG labelling. The growing institutional investor community that applies ESG screens to fixed-income allocation is creating structural demand for labelled bonds whose supply is currently insufficient to satisfy the allocation requirements of large-scale ESG-mandated funds.

Recent Developments:

-

2025: JPMorgan Chase and Citigroup led record quarterly investment-grade bond underwriting in Q1 2025, collectively arranging the largest primary market issuance quarter in U.S. corporate bond history as corporations front-loaded borrowing ahead of anticipated spread and rate volatility, demonstrating the structural depth of institutional demand for investment-grade corporate fixed income at current yield levels.

-

2025: Goldman Sachs and Bank of America co-managed Apple’s multi-tranche investment-grade bond offering in 2025, one of the largest single corporate bond transactions of the year, demonstrating the continued appetite of cash-generating technology companies to access debt capital markets for capital structure optimisation and returning capital to shareholders through bond-financed buybacks.

-

2024: European Investment-Grade Corporate Bond issuance reached record levels in 2024 driven by refinancing of maturing obligations and financing of European energy transition capital programmes, with underwriting activity concentrated among BNP Paribas, Deutsche Bank, and Barclays whose European corporate debt capital markets franchises served the highest volume of issuer mandates in a single calendar year.

Corporate Bond Market Key Players

-

JPMorgan Chase

-

Goldman Sachs

-

Citigroup

-

Bank of America

-

Morgan Stanley

-

Barclays

-

Deutsche Bank

-

BNP Paribas

-

BlackRock

-

PIMCO

-

Vanguard

-

Fidelity Investments

-

UBS

-

Credit Suisse

-

HSBC

-

Nomura

-

Societe Generale

-

Wells Fargo

-

T. Rowe Price

-

Allianz Global Investors

Corporate Bond Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 38.47 Trillion |

| Market Size by 2035 | USD 101.21 Trillion |

| CAGR | CAGR of 10.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Investment-Grade Bonds, High-Yield Bonds, Convertible Bonds, Floating Rate Notes, Others) • By Issuer (Financial Institutions, Non-Financial Corporates, Utilities & Infrastructure, Others) • By Investor (Institutional Investors, Retail Investors, Others) • By Maturity (Short-Term, Medium-Term, Long-Term) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | JPMorgan Chase, Goldman Sachs, Citigroup, Bank of America, Morgan Stanley, Barclays, Deutsche Bank, BNP Paribas, BlackRock, PIMCO, Vanguard, Fidelity Investments, UBS, Credit Suisse, HSBC, Nomura, Societe Generale, Wells Fargo, T. Rowe Price, Allianz Global Investors |

Frequently Asked Questions

Get in Touch